Antibiotic Resistance Market Size, Industry Analysis, 2026-2034

REPORT DETAILS

Antibiotic Resistance Market Summary

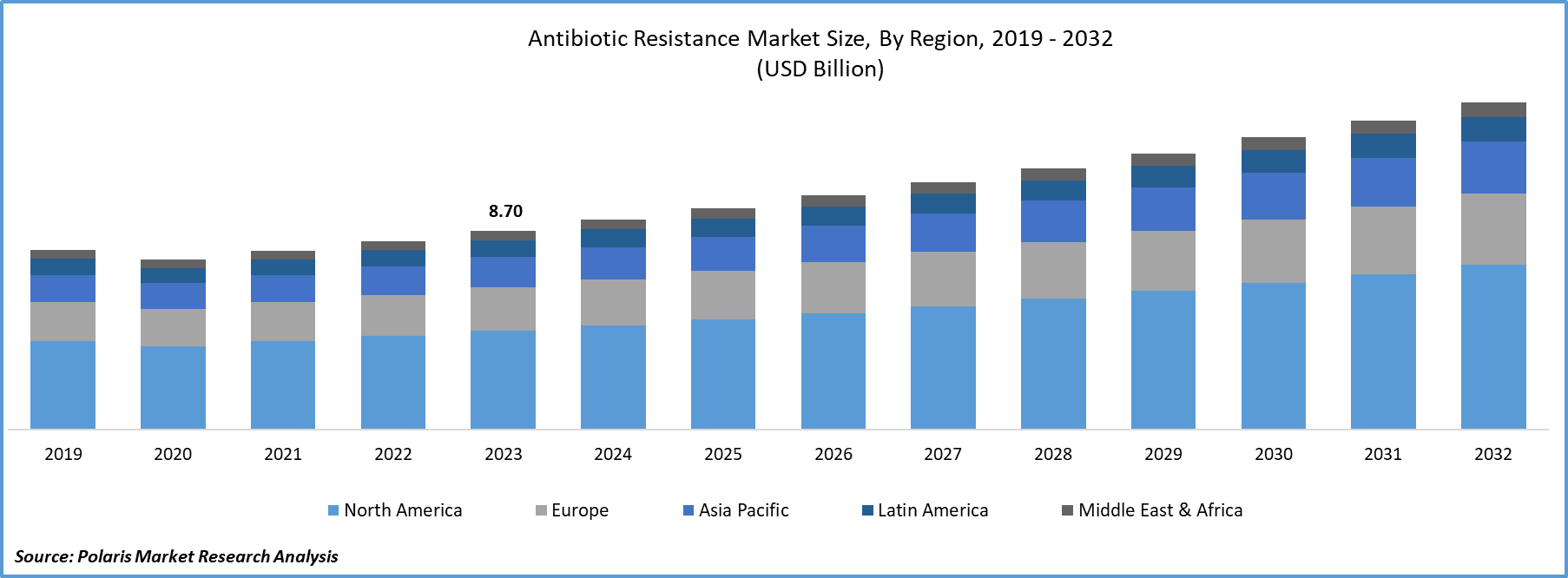

The antibiotic resistance market size was valued at USD 9.69 billion in 2025 and is anticipated to register a CAGR of 5.8% from 2026 to 2034. The antimicrobial resistance (AMR) market is gaining significant attention globally due to its growing impact on public health systems and healthcare economies. The rising prevalence of drug-resistant infections and increasing investments in novel antibiotic development boost the market growth. Also, rapid diagnostic technologies are expected to drive sustained market expansion.

Market Statistics

Key Takeaways

- North America dominated the global market with 49.80% revenue share in 2025. The dominance is attributed to growing funding or investments in scientific research of new drug classes and rising adoption of innovative antibiotic therapies.

- The Asia Pacific antibiotic resistance market is expected to register the highest CAGR of 6.40% during the forecast period. This growth is accelerated by the region’s greater prevalence of infectious diseases.

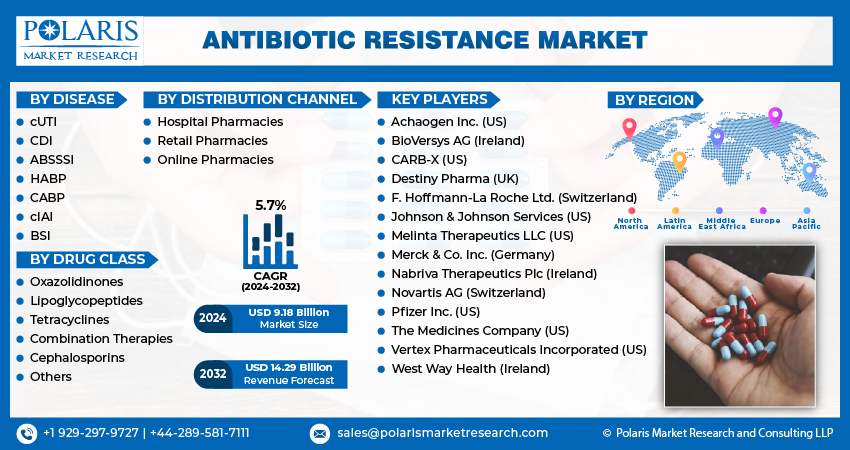

- The complicated urinary tract infections segment held the largest share of 36.80% in 2025. It is attributed to the increasing incidence of cUTIs globally and the emergence of UTI as a public health concern.

- The oxazolidinones segment held the largest share of 34.5% in 2025. Its higher effectiveness against various drug-resistant bacteria boosts the segment growth.

- The retail pharmacies segment is expected to register the highest CAGR of 6.2% during the forecast period. The rising emergence of digital pharmacies and telemedicine fostered the segment’s growth.

Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations

Industry Dynamics

- Growing prevalence of antibiotic-resistant and hospital-acquired infections (HAIs) drives the antibiotic resistance industry expansion.

- Rising development of new novel antibiotics boosts the market growth.

- Stringent government regulations and requirements hinder the growth of the market.

- Market players emphasize the development and discovery of new solutions that can combat antibiotic or antimicrobial resistance. This factor is expected to provide lucrative opportunities for the market in the coming years.

AI Impact on Antibiotic Resistance Market

- Accelerates discovery of novel antibiotics through AI-driven molecule screening and predictive modeling

- Reduces R&D time and costs by identifying viable drug candidates early

- Enhances rapid diagnostics with AI-based pathogen identification and susceptibility testing

- Improves precision medicine by enabling targeted antibiotic selection

- Supports antimicrobial resistance surveillance, as highlighted by the World Health Organization

- Strengthens antimicrobial stewardship programs through data-driven prescribing insights

- Minimizes antibiotic misuse and overprescription in clinical settings

- Integrates with electronic health records for real-time clinical decision support

- Enables predictive analytics for resistance trends and outbreak forecasting

- Improves hospital workflow efficiency and patient outcomes

Source: Polaris Market Research Analysis

To Understand More About this Research:Download Sample Report

What is the Antibiotic Resistance Market?

Antibiotic resistance occurs when bacteria evolve mechanisms that protect them from antibiotics, rendering standard treatments ineffective. This phenomenon falls under the broader scope of antimicrobial resistance (AMR). AMR includes resistance to antivirals, antifungals, and antiparasitic drugs. According to global health agencies, antibiotic resistance contributes to millions of infections annually. It remains a leading cause of mortality worldwide. The growing adoption of advanced diagnostic technologies influences the market. AI-based drug discovery platforms and combination therapies transform the market landscape. The rising consumption of antibiotics worldwide is driven by drastic population growth and rising incidences of various infectious diseases. Also, greater access to healthcare facilities boosts the consumption. It contributes to antibiotic resistance. Therefore, numerous companies are focusing on the development and discovery of new solutions capable of combating antibiotic and antimicrobial resistance.

Why this Market Matters Now?

The increasing burden of antibiotic-resistant infections drives the need for effective treatments. The increasing emphasis on addressing antibiotic resistance fuels market expansion. Also, the growing cases of overuse or misuse of antibiotics among humans, animals, and agriculture lead to the development of antibiotic resistance. This factor is further propelling the market growth. According to OECD analysis, resistance to third-line antimicrobials could more than double in OECD countries by 2035, compared to the levels in 2005. EU/EEA countries significantly observe this challenge, where resistance to third-line antibiotics could triple during the same period.

Market Dynamics

Rising Prevalence of Antibiotic-Resistant and Hospital-Acquired Infections

Prevalence of antibiotic-resistant and hospital-acquired infections (HAIs) is rising across the world. According to the World Health Organization data, from over 100 countries, published in 2025, one in six bacterial infections is resistant to antibiotic treatment. The data highlight the growing global burden. Hospital settings intensify the issue. The increasing incidence of HAIs, coupled with rising resistance among key pathogens such as E. coli and Klebsiella, is drives the demand for advanced therapeutics, rapid diagnostics, and infection control measures.

Growing Development of Novel Antibiotics

The increasing development of new antibiotics is speeding up market growth. Key players are focusing on global research and development efforts and funding. Initiatives like CARB-X, along with support from organizations such as the Biomedical Advanced Research and Development Authority, are driving innovation through grants and partnerships. Growing investments in next-generation treatments, such as antimicrobial peptides and phage therapy, expand the pipeline. This increased focus on new methods of action is essential for fighting multidrug-resistant infections. It ensures long-term market growth.

Restraining Factors

Stringent Government Regulations and Requirements

Stringent government regulations and compliance requirements restrain the antibiotic resistance market development. Agencies such as the U.S. Food and Drug Administration and the European Medicines Agency impose rigorous clinical trial standards, safety evaluations, and post-market surveillance obligations. These processes increase development timelines and costs, discouraging new antibiotic innovation. Strict antimicrobial stewardship policies limit the use of newly approved drugs to prevent resistance. This reduces sales potential. Pricing and reimbursement pressures also restrict profitability, especially in cost-sensitive healthcare systems. As a result, despite strong clinical need, regulatory complexity and usage restrictions create major barriers for market entry and commercial sustainability.

Therapeutics vs Diagnostics vs Stewardship: Where the Real Opportunity Sits?

The AMR market is shifting from a drug-centric model to a diagnostics-led, stewardship-enabled ecosystem. While therapeutics remain essential, the real opportunity sits at the intersection of rapid diagnostics and antimicrobial stewardship, where clinical value, scalability, and health-economic benefits converge.

| Aspect | Therapeutics (Antibiotics & Alternatives) | Diagnostics (AMR Detection & Testing) | Stewardship (Programs & Systems) |

| Core Role | Treat resistant infections | Identify pathogen & resistance profile | Optimize antibiotic usage |

| Market Maturity | Established but declining ROI | Rapidly evolving, tech-driven | Emerging, policy-driven |

| Revenue Potential | Moderate but constrained | High and scalable | Indirect/service-driven |

| Growth Drivers | Need for novel drugs, superbug rise | Demand for rapid/POC testing, precision medicine | Regulatory mandates, hospital programs |

| Key Opportunity Areas | Phage therapy, CRISPR antibiotics, peptides | Molecular diagnostics, AI-based testing, point-of-care | Digital stewardship platforms, data analytics |

| Profitability Challenges | Low ROI due to short treatment duration & restricted use | Perceived as cost burden, reimbursement issues | Limited direct monetization, dependent on healthcare budgets |

| Adoption Barriers | High R&D cost, resistance emergence | Cost, infrastructure, turnaround time | Lack of funding, training, and awareness |

| Impact on AMR Control | Direct but short-term (resistance evolves) | High. It enables targeted therapy & reduces misuse | Very high. It reduces overuse and prolongs drug efficacy |

| Scalability | Limited (pipeline constraints) | High (platform-based, repeat testing) | Moderate (depends on system integration) |

| Strategic Value | Essential but economically challenged | Critical enabler of precision medicine | System-level long-term value driver |

Source: Polaris Market Research Analysis

Source: Polaris Market Research Analysis

Segmentation Insights

By Diseases Insights

The complicated urinary tract infections segment accounted for the largest share of 36.80% in 2025. Segment’s dominance is attributed to the rising prevalence of these infections globally and the emergence of UTI. According to the National Kidney Foundation, UTIs are responsible for more than 10 million healthcare visits each year. Increasing prevalence of UTIs leads to a public health concern. This factor contributed to the segment dominance.

By Drug Class Insights

The oxazolidinones segment held the majority share of 34.5% in 2025. This dominance is attributable to widespread utilization because of its higher effectiveness against several certain drug-resistant bacteria coupled with its greater efficacy against multidrug-resistant pathogens, including methicillin-resistant staphylococcus aureus and vancomycin-resistant Enterococcus.

The combination therapies segment will grow at the highest pace. This growth is due to its growing adoption and popularity worldwide, as it involves the use of several antibiotics to target infections. In addition, combining antibiotics with different mechanisms also allows for a broader spectrum of activity against several bacterial species.

By Distribution Channel Insights

The retail pharmacies segment will register a CAGR of 6.2% during the forecast period. Segment’s growth is attributable to the rising emergence of digital pharmacies and telemedicine and a growing number of healthcare companies focusing on establishing their online presence to allow their patients for remote consultation and easy access to antibiotics. Also, advancements in technology, such as digital health records and e-prescribing systems, resulted in enhanced tracking of patient health and monitoring their progress, which, in turn, fostered the segment’s growth.

The hospital pharmacies segment led the market. This dominance is accelerated by a larger patient pool opting for hospital pharmacies for their healthcare needs and a continuous increase in hospital infrastructure in emerging economies worldwide. Moreover, these pharmacies play a vital role in the management of antibiotics for several infections as they enable seamless coordination between healthcare professionals and ensure timely access to antibiotics for patients.

One Health Impact

The One Health approach is promoted by organizations such as the World Health Organization. It combines human, animal, and environmental health to tackle antimicrobial resistance in a comprehensive way. This approach, along with antimicrobial stewardship programs, greatly affects market demand patterns. Stewardship efforts are often led by agencies like the Centers for Disease Control and Prevention. Their goal is to reduce unnecessary antibiotic use. This helps reduce overall consumption in the short term. At the same time, it increases the need for targeted therapies, quick diagnostics, and monitoring systems. In veterinary and agricultural fields, stricter rules on antibiotic use shift demand toward alternatives and preventive measures. Overall, One Health and stewardship limit growth in volume. They foster higher-value and precision-focused demand. They shift the market from broad-spectrum antibiotic use to optimized, evidence-based treatment strategies.

Source: Polaris Market Research Analysis

Regional Insights

North America dominated the global market with 49.80% share in 2025. Region’s dominance is attributed to growing funding or investments for scientific research of new drug classes, technological advancements, and rising adoption of innovative antibiotic therapies. In addition, growing awareness among the general public and healthcare professionals regarding the consequences of antibiotics and the creation of educational campaigns focused on addressing such issues are further anticipated to propel the region’s growth. For instance, the National Microbiology Laboratory, Canada, announced that they understand the extent of antimicrobial resistance in the country. It aims to identify new threats and also properly assess the potential burden of AMR worldwide.

The Asia Pacific antibiotic resistance market is expected record a CAGR of 6.40% during the forecast period. This growth is accelerated by the region’sa greater prevalence of infectious diseases as a result of the vast population in the region and inefficient regulation or control over the use of antibiotics that led to overuse or misuse, contributing to the development of antibiotic resistance.

Source: Polaris Market Research Analysis

Regulatory and Reimbursement Landscape

The regulatory and reimbursement landscape for antibiotic resistance is structured in a unique way. It creates unusual commercialization dynamics. Regulatory bodies like the U.S. Food and Drug Administration (FDA) provide faster pathways and incentives to encourage antibiotic development. At the same time, global frameworks led by the WHO promote controlled usage through stewardship programs. However, reimbursement models do not align well. Antibiotics are priced and paid for based on volume, even though their use is intentionally limited to prevent resistance. This approach leads to lower revenues because treatments are often short and reserved for last-line therapies. New subscription-based models, such as those being tested in the UK, aim to separate sales from volume. However, their adoption is still low. Overall, antibiotics present a paradox: they have significant clinical value, but that value does not translate into strong commercial returns. This situation calls for new funding and reimbursement strategies.

Key Market Players & Competitive Insights

Getting regulatory approvals and implementing on strategic partnerships to drive competition

The antibiotic resistance market size is highly competitive in nature with the robust presence of global and regional companies in the market. Major companies are competing on various factors such as new drug development, growing R&D activities or efforts, focusing on regulatory approvals, creating awareness programs, and implementation of strategic partnerships & collaborations.

List of Major Players

- Achaogen Inc.

- BioVersys AG

- CARB-X

- Destiny Pharma

- F. Hoffmann-La Roche Ltd.

- Johnson & Johnson Services

- Melinta Therapeutics LLC

- Merck & Co. Inc.

- Nabriva Therapeutics Plc

- Novartis AG (Switzerland)

- Pfizer Inc.

- The Medicines Company

- Vertex Pharmaceuticals Incorporated

- West Way Health

Recent Developments

- In February 2025, the Gates Foundation, Novo Nordisk Foundation, and Wellcome introduced the Gram-Negative Antibiotic Discovery Innovator, a US$ 50 Mn initiative aimed at tackling antimicrobial resistance in low- and middle-income nations.

- In November 2024, India’s Union Minister, Dr. Jitendra Singh, unveiled India’s first homegrown antibiotic, Nafithromycin, designed to fight drug resistance. The three-day therapy is ten times more effective than existing antibiotics.

Antibiotic Resistance Market Segmentation

By Disease Outlook (Revenue – USD Billion, 2021–2034)

- cUTI (Complicated Urinary Tract Infections)

- CDI (Clostridioides Difficile Infection)

- ABSSSI (Acute Bacterial Skin and Skin Structure Infections)

- HABP (Hospital-acquired Bacterial Pneumonia)

- CABP (Community-acquired Pneumonia)

- cIAI (Complicated Intra-abdominal Infection)

- BSI (Bloodstream Infection)

By Drug Class Outlook (Revenue – USD Billion, 2021–2034)

- Oxazolidinones

- Lipoglycopeptides

- Tetracyclines

- Combination Therapies

- Cephalosporins

- Others

By Distribution Channel Outlook (Revenue – USD Billion, 2021–2034)

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

By Regional Outlook (Revenue – USD Billion, 2021–2034)

- North America

- U.S.

- Canada

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- South Korea

- Indonesia

- Malaysia

- Rest of Asia Pacific

- Latin America

- Argentina

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- UAE

- Saudi Arabia

- Israel

- South Africa

- Rest of Middle East & Africa

Report Coverage

The antibiotic resistance market report emphasizes on key regions across the globe to provide better understanding of the product to the users. Also, the report provides market insights into recent developments, trends and analyzes the technologies that are gaining traction around the globe. Furthermore, the report covers in-depth qualitative analysis pertaining to various paradigm shifts associated with the transformation of these solutions.

The report provides detailed analysis of the market while focusing on various key aspects such as competitive analysis, disease, drug class, distribution channel, and their futuristic growth opportunities.

Antibiotic Resistance Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 9.69 billion |

| Market Size in 2026 | USD 10.23 billion |

| Revenue Forecast in 2034 | USD 16.02 billion |

| CAGR | 5.8% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2022–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD billion, 2021–2034 and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Antibiotic Resistance Market FAQ's

The market size was valued at USD 9.69 billion in 2025. It is projected to reach USD 16.02 billion by 2034, at a CAGR of 5.8%.

Rising prevalence of infectious diseases and advancements in antibiotic resistance diagnosis propel market growth. Also, the growing number of R&D activities fuels the market expansion.

The oxazolidinones segment dominated with a 34.5% share in 2025. This is due to its growing importance in combating resistant Gram-positive infections, such as MRSA and VRE.

North America dominated the market with 49.80% revenue share in 2025. However, the Asia Pacific market is anticipated to witness the highest CAGR of 6.40%.

Creating a new antibiotic typically requires 10 to 15 years and higher costs. Low profit margins and stringent regulatory processes restrict pharmaceutical investments in this critical area. These factors hinder the market expansion.

Achaogen Inc., BioVersys AG, CARB-X, Destiny Pharma, F. Hoffmann-La Roche Ltd., Johnson & Johnson Services, Melinta Therapeutics LLC, Merck & Co. Inc., Nabriva Therapeutics Plc, Novartis AG (Switzerland), Pfizer Inc., The Medicines Company, Vertex Pharmaceuticals Incorporated, and West Way Health are among the major players.

Download Sample Report of Antibiotic Resistance Market

Please fill out the form to request a customized copy of the research report.