Flexible Electronics Market Demand, Growth Analysis, 2026-2034

REPORT DETAILS

REPORT DETAILS

ABOUT THIS REPORT

Flexible Electronics Market Summary

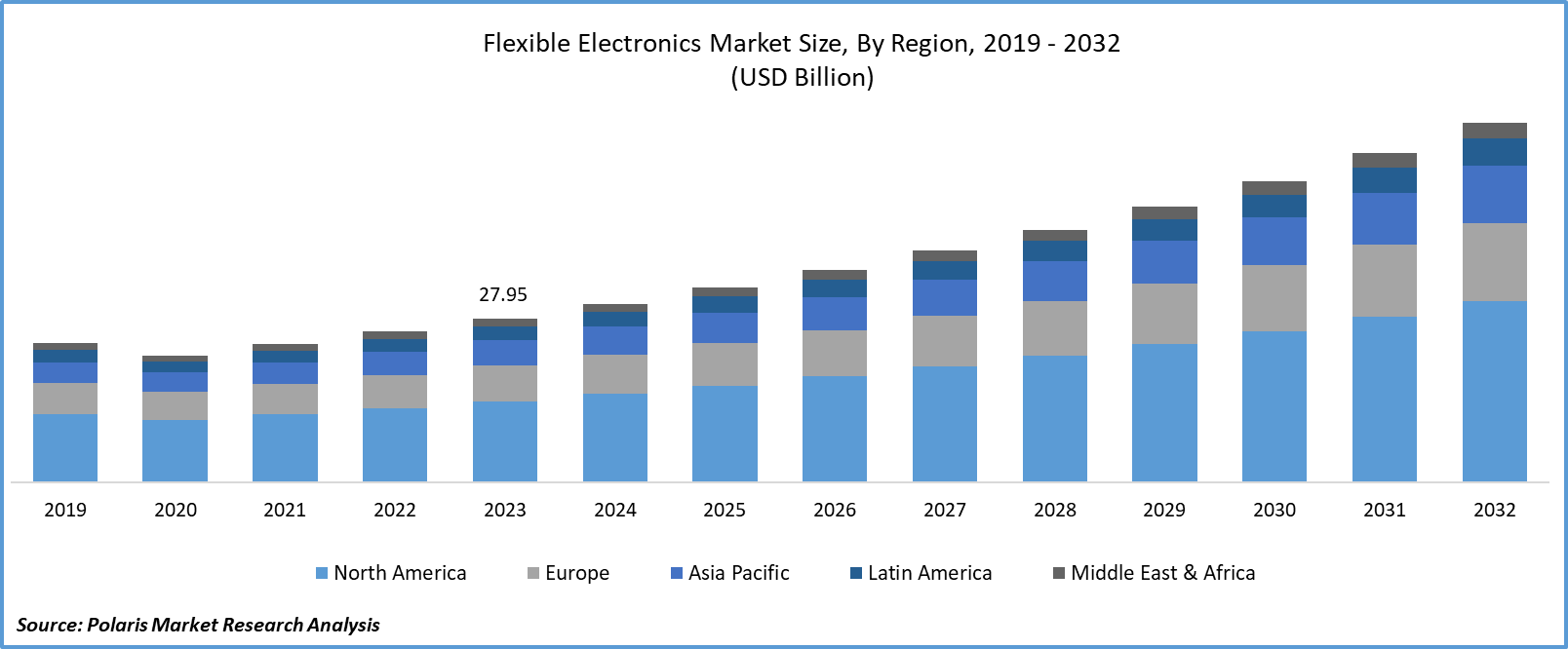

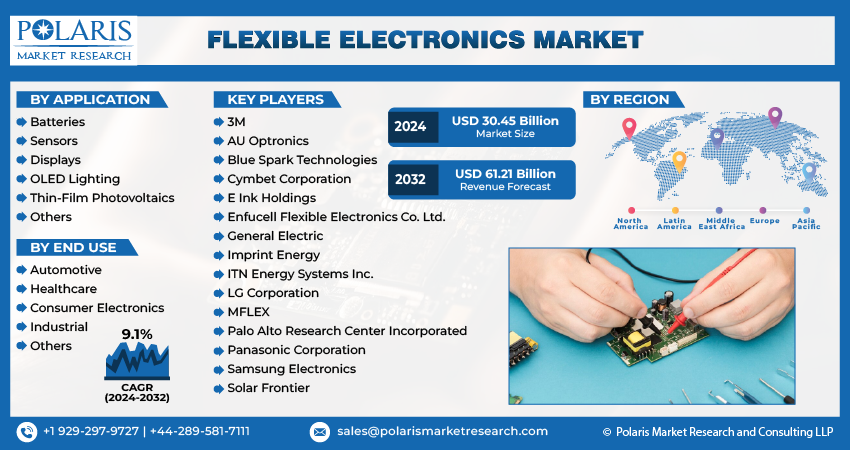

The global flexible electronics market size was valued at USD 32.68 billion in 2025 and is expected to grow at a CAGR of 10.4% 2026 to 2034. Expansion is driven by demand for wearable devices, foldable smartphones, and lightweight electronics across healthcare, automotive, and consumer electronics sectors.

Market Statistics

Key Takeaways

- The display segment led the global flexible electronics market in 2025. This is due to the increased demand for foldable smartphone displays, flexible OLED displays for wearables, and rollable TVs.

- The consumer electronics division led the market in 2025, driven by the widespread adoption of foldable phones and flexible screens in tablets.

- The Asia Pacific flexible electronics market led the market in 2025, driven by China's production prowess, the adoption of foldables, and spending on high-end display technology.

- North America is expected to experience rapid growth with the adoption of thin, lightweight components for healthcare wearables, including glucose monitors and smart patches.

Flexible electronics, also referred to as flexible electronic circuits, are a design change that enables electronics to bend, fold, or stretch into any configuration without impairing function. Unlike inflexible electronics, they employ plastic film, conductive polymers, metal foils, and ultra-thin materials primarily composed of glass. Their malleability enables designers to craft lighter, slimmer, more comfortable electronics that will serve as drivers for a range of next-gen consumer and industrial electronics products of varying complexity.

Industry Dynamics

- The growth of connected vehicles is driving demand for flexible antennas. Flexible antennas are needed to ensure seamless connectivity. This is expanding market opportunities as global automobile manufacturing increases.

- The need for flexible electronics stems from the increased availability of information in the field of material science, which includes elastic nanomaterials as well as conductive polymers.

- More income to spend leads to faster replacement rates, as consumers are attracted to newer, more convenient electronics for enhanced user experience and cosmetic appeal.

- The flexible electronics market faces commercialization challenges, including high manufacturing costs and low production yields.

Increasing automobile production worldwide is a major factor positively affecting the market for flexible electronics. According to the European Automobile Manufacturers’ Association, 85.4 million vehicles were produced worldwide in the year 2022. This figure increased by 5.7 percent compared to production in 2021. In making vehicles, auto companies are employing flexible displays, sensors, and/or lighting systems to improve the user interface for users. In recent times, automobiles such as electric and self-driving cars are increasingly dependent on flexible materials to achieve lightweighting and greater space efficiency. Thus, the increasing production of automobiles worldwide is propelling the market.

The market demand for flexible electronics has emerged due to advances in materials science. With the growing development of conductive polymers, nanomaterials, and ultrathin materials, companies have the opportunity to develop flexible displays, foldable electronics, and wearable technologies to deliver the best strength and performance in their electronic devices. With advancements in materials science, the likelihood of failures in flexible electronics has decreased significantly. This has led different sectors of the economy to embrace the technology in their operations to achieve the best results in the production of smart wearables, flexible displays, and Internet of Things devices. Consequently, as materials science advances and innovates, the demand for flexible electronics will continue to grow.

How Flexible Electronics Work?

Flexible electronics result from the application of conductive materials to bendable substrates using advanced techniques, such as inkjet printing and roll-to-roll processing. The circuits continue to function properly even when bent or stretched. This makes flexible electronics technology well-suited for dynamic applications where rigid electronics are impractical.

Flexible vs Rigid Electronics

Flexible electronics are different from rigid electronics in shape and weight. They also differ in durability and how they are used. Rigid electronics are still mainly used in high-power computing. Flexible electronics find applications in wearables and portable devices. They work better in places with limited space.

Market Dynamics

Rising Adoption of Smartphones Globally

Consumers are increasingly adopting smartphones with curved-edge displays or rollable displays. These displays rely on a flexible display technology or bendable OLED panels. Furthermore, high-screen-size requirements without corresponding increases in phone dimensions have created a significant need for flexible display technology, enabling a smartphone to double in compact dimensions when needed. Flexible electronics, such as antennas, are becoming essential smartphone requirements as 5G smartphone adoption continues to grow among consumers. According to the State of Mobile Internet Connectivity Report 2023 released by the Groupe Spécial Mobile Association (GSMA) organization, over 54% of the world's population owns smartphones, including 5G smartphones. As a result, the growing number of smartphone consumers represents a significant opportunity to drive investments in areas such as the flexible electronics market.

Growing Disposable Income Worldwide

Increasing disposable income is prompting consumers to invest in innovative technologies such as foldable smartphones, curved TVs, and wearable health trackers, all of which leverage flexible technologies. According to consumer disposable income data collected and made public by the Bureau of Economic Analysis, consumer disposable income was up by 0.3% in January 2025 as compared to December 2024. High consumer disposable income also drives demand for smart home systems, flexible automotive displays, and next-generation wearables, among others, thereby forcing manufacturers to adopt flexible, lightweight electronic components. Higher disposable incomes also support increasing replacement cycles, as buyers tend to move to the latest models of flexible electronics to enhance convenience and aesthetics. This increases the market base for advanced products, encouraging companies to fund research and production of flexible electronics amid rising consumer expectations.

Segment Insights

Market Evaluation by Component

Based on component, the market is divided into displays, batteries, sensors, memory devices, and others. The display segment accounted for the largest share of the global flexible electronics market in 2025, driven by the rapid adoption of foldable smartphones, flexible OLED screens in wearables, and rollable TVs. Many technology firms, such as Samsung and LG, have invested in advanced display technologies to meet demand for high-resolution, bendable screens with greater durability. Besides, there is an increase in the integration of curved and flexible displays into automotive dashboards and infotainment systems. This contributes to the segment’s leading market share.

The sensor segment is expected to grow rapidly in the near future. This is due to increasing demand for health-monitoring devices, such as smart patches and fitness trackers, that use flexible sensors to track metrics like heart rate and blood oxygen levels. The Internet of Things and smart packaging also contribute to the high growth of the flexible sensor market. These applications use ultra-thin, flexible sensors to continuously and precisely analyze the environment and the structure. Advancements in printed and flexible sensors are likely to increase their adoption across healthcare, automotive, and industrial applications.

Market Insight by Application

In terms of application, the market is segregated into consumer electronics, automotive, healthcare, industrial, and others. The consumer electronics segment led the flexible electronics market in 2025, driven by higher demand for foldable phones and display technologies in tablets. The major contributors to the segment’s growth are Samsung, Huawei, and Apple, which have designed high-performance, flexible display devices that have attracted consumer interest in portable technology. The wearable technology boom, especially flexible smartwatches, also helped increase demand for flexible displays, as wearable devices require components that are light, flexible, and durable to enhance user comfort.

Applications in healthcare and in the automotive industry are scaling beyond their initial adoption stages. In health care, smart patches implement flexible electronics for continuous monitoring. Automotive applications focus on curved dashboard solutions, flexible lighting, and the integration of lightweight sensors.

Regional Outlook

By region, the report provides flexible electronics market insight into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. Asia Pacific held a large market share in 2025 due to rising demand from countries such as China, South Korea, and Japan. China held a large market share due to their strong manufacturing base, higher adoption of foldable smartphones, and investments in emerging display technologies. Organizations like Samsung and Huawei have invested in increased production of flexible displays and wearable electronics in this region, driven by its strong electronics industry and greater use of semiconductor manufacturing facilities. Government investments in materials science and printed electronics have also made Asia Pacific the dominant region.

The North America flexible electronics market is expected to register robust growth. This is due to the rising use of flexible, thin, and light components in healthcare wearables, such as smart patches and continuous glucose monitoring probes. Another factor fueling market growth is the high adoption of IoT devices, military applications, and flexible energy storage in electric vehicles. Furthermore, high investment in research and development in this industry and geographic segment is expected to drive growth in the coming years.

Key Market Players & Competitive Analysis Report

The flexible electronics market is highly competitive. Players in this market are entering into strategic partnerships to enhance product portfolios and expand market presence. Major players in the flexible electronics market include Samsung, LG Electronics, Panasonic Corporation, and others. Players in the market are adopting strategic mergers and acquisitions to strengthen their market positions. Another shift in the flexible electronics market is collaboration between industry players and other research organizations.

The market is fragmented, with the presence of numerous global and regional market players. Leading players can be broadly grouped into display technology leaders, energy storage innovators, and sensor specialists. A few major players in the market are AU Optronics Corp.; Blue Spark Technologies, Inc.; Cymbet Corporation; E Ink Holdings Inc.; Enfucell SoftBattery; Imprint Energy Inc.; LG Electronics; Palo Alto Research Center Incorporated; Samsung Electronics Co. Ltd.; SEMI FlexTech; and Solar Frontier.

LG Electronics, a multinational South Korean company headquartered in Seoul, South Korea, is a known innovation and technology leader in flexible technology, especially in flexible displays. The company has achieved a major leap forward with the invention of stretchable and bendable displays. Among LG's most popular inventions in the field of flexible displays is the LG OLED Flex, a 42-in 4K Flexible OLED TV that can switch from flat to curved via its flexible OLED technology.

Samsung Electronics Co., Ltd is a global company in flexible electronics. It pioneered several innovations that have reshaped the modern smartphone and display technology. As a leader in the development of foldable smartphones, in 2021 alone it shipped four times as many foldable devices compared to 2020. Samsung created the world's first folding glass display, necessitating rework inside the display-a new cooling system and dual-battery technology to maintain slim, functional designs. Samsung's flexible OLEDs sit at the heart of its flexible electronics portfolio. Its Flex OLED displays offer a remarkable ultra-tight 1.4R curvature, allowing display panels to bend sharper and devices to be smaller, while minimizing stress on panel material or fold. Samsung was the first to commercialize Ultra Thin Glass for foldable displays. It combines the durability of glass with the smoothness and flexibility, giving users a superior experience with all-around improved performance.

List of Key Companies

- AU Optronics Corp.

- Blue Spark Technologies, Inc.

- Cymbet Corporation

- E Ink Holdings Inc.

- Enfucell SoftBattery

- Imprint Energy Inc.

- LG Electronics

- Palo Alto Research Center Incorporated

- Samsung Electronics Co. Ltd.

- SEMI FlexTech

- Solar Frontier

Flexible Electronics Industry Developments

June 2025: KAIST researchers unveil heat‑activated “shape‑shifting electronic ink.”

April 2025: Naxnova Technologies unveiled India’s first flexible hybrid printed electronics research and development centre, representing a landmark milestone in the nation’s innovation ecosystem.

January 2024: Samsung Display showcased advanced technologies at CES 2024, featuring foldable, rollable, and slidable displays, micro-displays for extended reality, OLED solutions for automotive interiors, professional monitors, and a 360-degree display experience.

Flexible Electronics Market Segmentation

By Component Outlook (Revenue, USD Billion, 2021–2034)

- Displays

- Batteries

- Sensors

- Memory Devices

- Others

By Type Outlook (Revenue, USD Billion, 2021–2034)

- Flexible Printed Circuits

- Rigid-Flexible

By Circuit Structure Outlook (Revenue, USD Billion, 2021–2034)

- Single-Sided Flexible Circuit

- Double-Sided Flexible Circuit

- Multilayer Flexible Circuit

- Sculptured Flexible Circuit

- Others

By Application Outlook (Revenue, USD Billion, 2021–2034)

- Consumer Electronics

- Automotive

- Healthcare

- Industrial

- Others

By Regional Outlook (Revenue, USD Billion, 2021–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Flexible Electronics Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 32.68 billion |

| Market Size in 2026 | USD 36.02 billion |

| Revenue Forecast by 2034 | USD 79.49 billion |

| CAGR | 10.4% |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD billion, and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape | Flexible Electronics Industry Trend Analysis (2025) Company profiles/industry participants profiling include company overview, financial information, product/service benchmarking, and recent developments |

| Report Format | PDF + Excel |

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

The global market size was valued at USD 35.4 billion in 2024 and is projected to grow to USD 108.7 billion by 2034.

The global market is projected to register a CAGR of 12.50% during the forecast period.

Asia Pacific held the largest share of the global market in 2024.

A few of the key players in the market are AU Optronics Corp.; Blue Spark Technologies, Inc.; Cymbet Corporation; E Ink Holdings Inc.; Enfucell SoftBattery; Imprint Energy Inc.; LG Electronics; Palo Alto Research Center Incorporated; Samsung Electronics Co. Ltd.; SEMI FlexTech; and Solar Frontier.

The sensor segment dominated the market revenue share in 2024.

The consumer electronics segment is expected to grow at the fastest pace in the coming years.

The flexible electronics market is projected to reach USD 79.49 billion by 2034. It is expected to grow at a CAGR of 10.4% between 2026 and 2034.

Flexible electronics find applications in consumer electronics, automotive displays, healthcare devices, and industrial IoT solutions.

The display segment accounted for the largest share of the global flexible electronics market in 2025. This is due to the rapid adoption of foldable smartphones and flexible OLED screens.

Flexible electronics result from applying conductive materials to bendable substrates using advanced techniques, such as inkjet printing and roll-to-roll processing.

Asia Pacific held a large market share in 2025 due to rising demand from countries such as China, South Korea, and Japan.

Download Sample Report of Flexible Electronics Market

Please fill out the form to request a customized copy of the research report.