Coolant Distribution Unit Market Demand, Industry Report, 2026-2034

REPORT DETAILS

Coolant Distribution Unit Market Summary

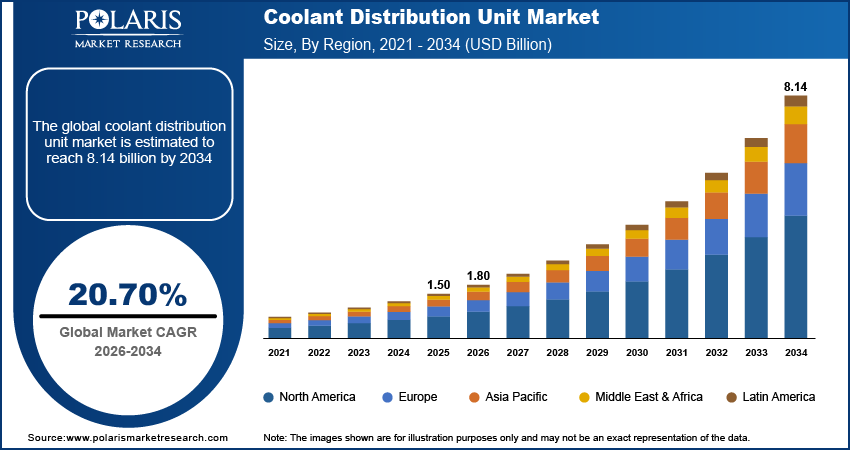

The global coolant distribution unit market is estimated around USD 1.50 billion in 2025,?with consistent growth anticipated during 2026–2034. Driven by AI infrastructure expansion coupled with hyperscale data center construction. The market is projected to grow at a CAGR of 20.70% during the forecast period.

Market Statistics

Key Takeaways

- North America accounted for the largest regional share of around 38.6% in 2025, driven by rapid expansion of hyperscale data centers, strong investments in AI infrastructure, and increasing deployment of high-density GPU clusters.

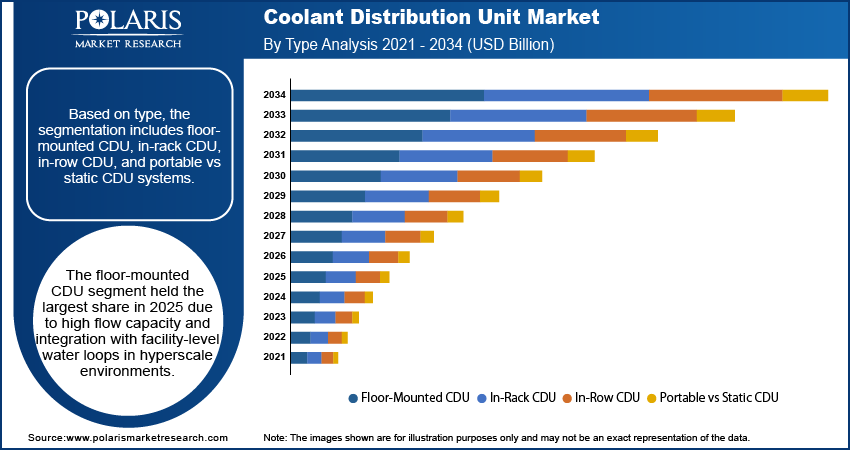

- By Type, Floor-Mounted CDU segment accounted for the largest share of approximately 57.4% in 2025, supported by its ability to handle high coolant flow rates and centralized liquid cooling infrastructure in hyperscale facilities.

- By Cooling Technology, Direct-to-Chip Cooling segment accounted for the largest share of around 62.1% in 2025, driven by efficient processor-level heat removal, enhanced thermal performance, and support for high rack power densities.

- By End Use, Hyperscale Data Centers segment accounted for the largest share of nearly 64.8% in 2025, driven by rapid expansion of AI training clusters, GPU-based computing infrastructure, and large-scale cloud deployments.

Industry Dynamics

- Escalating AI GPU cluster density is driving structural transition from air cooling to liquid-based data center coolant distribution systems.

- Hyperscale data center construction pipelines are embedding liquid cooling CDU architectures into greenfield and large-scale retrofit projects.

- High upfront capital expenditure and integration complexity create financial and engineering barriers for mid-sized operators.

- Net-zero data center initiatives and modular colocation deployment models are creating long-term expansion opportunities across the liquid cooling CDU market.

Why Coolant Distribution Unit Matters in the Circular Economy

The coolant distribution unit market forms a core component of modern liquid-based thermal architectures, supporting high-density rack cooling requirements driven by AI data center cooling expansion and next-generation compute workloads. A coolant distribution unit regulates flow, pressure, and temperature within a data center coolant distribution system, acting as the controlled interface between the facility loop and the secondary loop: the facility loop circulates water from central plant infrastructure, while the CDU-managed secondary loop isolates and delivers conditioned coolant directly to IT equipment through heat exchangers, protecting sensitive hardware and enabling precise thermal management. Rising rack power densities and accelerated GPU deployments are expanding the liquid cooling CDU market and strengthening CDU market size growth, positioning CDUs as essential infrastructure for scalable, energy-efficient data center operations.

Source: Polaris Market Research Analysis

To Understand More About this Research:Download Sample Report

Drivers & Opportunities

AI infrastructure expansion: The growing need for scaling AI applications is contributing to the rise in rack power densities in today’s data centers, thereby fueling the demand for efficient liquid cooling solutions. According to a market research report published by UN Trade and Development (UNCTAD), the global artificial intelligence market was expected to grow from USD 189 billion in 2023 to around USD 4.8 trillion in 2033, thus registering a 25-fold increase in a decade. The training compute clusters for large language models and HPC applications produce heat that surpasses the handling capacity of air cooling. This trend, in turn, directly fuels the adoption of liquid cooling CDU market solutions in the AI data center cooling ecosystem. With the increasing density of GPUs in racks, there is a need for accurate coolant flow control and redundancy planning.

Hyperscale data center construction: The continuous build-out of hyperscale facilities across North America, Europe, and Asia Pacific strengthens the coolant distribution unit market. UN Trade and Development (UNCTAD) reported that data centers emerged as a major global investment industry in 2025, with announced foreign direct investment exceeding USD 270 billion. Hyperscale operators are designing new campuses around high-density rack cooling frameworks from the outset. This architectural shift embeds liquid cooling CDU market systems at the facility loop and secondary loop levels. With the growing power capacity ranging into multi-megawatt systems, the integration of CDUs becomes imperative rather than optional. The growing hyperscale development pipeline continues to drive equipment demand in the long term for both greenfield and retrofit developments.

Restraints & Challenges

High upfront CDU cost: The coolant distribution unit requires specialized heat exchangers, pumps, and monitoring systems, thereby increasing the capital investment barrier. Compared to traditional air-cooled systems, the total cost of ownership starts with a higher capital expenditure point. The additional plumbing, leak detection systems, and facility upgrades continue to raise the deployment costs. This is a cost impediment for mid-sized companies and colocation facilities with small budgets, thereby hindering adoption in the coolant distribution unit market.

Opportunity

Net-zero data center initiatives: The shift to net-zero data centers opens structural opportunities for energy-efficient cooling solutions. Liquid cooling solutions improve power usage effectiveness (PUE) by minimizing the need for air conditioning, which consumes a significant amount of energy. For instance, in January 2026, Data Center Industry Denmark initiated the Net-Zero Start-Up Hub incubation program in Fredericia to encourage innovation in sustainable and low-carbon data center solutions. CDUs optimize thermal transfer rates and simplify the process of implementing waste heat recovery solutions. As companies make commitments to reduce carbon emissions, there is increasing investment in advanced AI data center cooling solutions.

Modular deployment in colocation facilities: The colocation market is adopting a modular infrastructure design to meet the dynamic tenant density requirements. The modular CDUs enable scalable deployment in line with the incremental rack deployments. As enterprise customers deploy GPU-intensive workloads within shared facilities, modular high-density rack cooling solutions become commercially attractive. The expansion of flexible colocation environments therefore opens incremental opportunities within the data center coolant distribution system ecosystem.

Coolant Distribution Unit (CDU) Technology Landscape & How CDUs Work

High-density AI racks are pushing thermal loads beyond the limits of conventional air systems. Liquid cooling has transitioned from research to architectural, and the knowledge of the coolant distribution unit is key to scaling contemporary data centers. A CDU is the managed boundary between the facility chilled water and the IT equipment, where heat is transferred without enabling direct fluid mixing.

CDU Working Principle Explained

A CDU consists of two independent hydraulic systems. The first system is connected to the facility chilled water supply. The second system is responsible for carrying treated coolant to the servers or immersion tanks. The heat transfer process occurs in a plate heat exchanger, and temperature and pressure are controlled by pumps and associated control systems.

The secondary loop liquid cooling system design facilitates temperature control and complies with the recommendations offered by ASHRAE and OCP for high-density liquid cooling. The process of commissioning the system requires integrated air removal, pressure balancing, and leak testing.

Key Components

- Pumps: Variable-speed pumps control coolant flow; redundancy is provided for CDU redundancy systems.

- Heat Exchangers: Transfer heat from one loop to another without mixing fluids.

- Controls & PLCs: Control temperature set points and alarm logic.

- Filtration: Protects cold plates and piping from contamination.

- Sensors & Leak Detection: Monitor pressure, temperature, and fluid integrity.

Types of Coolant Distribution Units

- Rack-Mounted CDU: Integrated into a cabinet; suited for local high-density installation.

- In-Row Coolant Distribution Unit: Located between racks; balances density and accessibility.

- Floor-Mounted CDU: Supports high-density areas; suited for row-level or pod-based cooling.

- Modular Coolant Distribution Unit: Scalable systems that grow with rack density increases.

Coolant distribution unit placement affects redundancy, piping, and commissioning.

Cooling Technologies Supported by CDUs

- Direct-to-Chip Cooling: The direct-to-chip coolant distribution unit provides coolant directly to the CPU and GPU cold plates.

- Immersion Cooling CDU: An immersion cooling CDU supports dielectric fluid tanks where servers are submerged. Heat transfers from fluid to the CDU exchanger.

- Air-to-Liquid & Hybrid Systems: The rear-door heat exchangers and hybrid systems allow for the adoption of liquid cooling in a step-by-step fashion without requiring architectural changes. As mixed environments are becoming more prevalent.

Direct-to-Chip vs Immersion – Comparison

| Parameter | Direct-to-Chip | Immersion Cooling |

| Retrofit Capability | Moderate | Limited |

| Density Handling | High | Very High |

| Maintenance Familiarity | Higher | Moderate |

| Infrastructure Change | Lower | Higher |

Source: Polaris Market Research Analysis

Operational Implications

CDUs introduce hydraulic engineering into data center operations. Leak detection, redundancy design, pump calibration, and water quality issues are now of paramount importance. Accurate commissioning is what determines long-term system stability.

As AI clusters grow in size, CDUs will evolve from support equipment to primary thermal infrastructure. Architecture decisions made today directly shape efficiency, risk exposure, and expansion economics over the next decade.

Source: Polaris Market Research Analysis

Segmental Insights

This report offers detailed coverage of the coolant distribution unit market by type, cooling technology and end use to help readers identify the fastest expanding and most attractive demand segments.

By Type

-

Floor-Mounted CDU

The floor-mounted coolant distribution unit segment accounts for the largest revenue share. Such systems are prevalent in large-scale liquid cooling retrofits and greenfield hyperscale projects because of their ability to handle higher flow rates, ease of maintenance, and compatibility with water loops in larger facilities. The adaptability of such systems in managing large volumes of coolant further cements their prevalence in massive data halls.

-

In-Rack CDU

The in-rack CDU market is the fastest-growing market, which is driven by the growing adoption of AI GPU clusters and high-density racks. In-rack solutions involve the coolant distribution unit being located inside or near server racks, thus reducing the path length of the fluid. This technology allows for fine-grained cooling control and rack power densities, which are now shattering the air-cooling barrier in AI-infused data centers.

-

In-Row CDU

In-row solutions are a strong market in medium to high-density environments, where the need for scalability is emphasized. These solutions are located between server racks and provide balanced control and compactness. They continue to see steady adoption in colocation and enterprise data centers migrating from air-to-liquid CDU solutions.

-

Portable vs Static CDU

Portable CDU systems are turning out to be a niche market but growing rapidly, especially in test lab setups and initial liquid-cooled rollouts. Static solutions remain dominant in the fixed environment, offering more capacity and integration headroom.

By Cooling Technology

-

Direct-to-Chip

The current market share leader is the direct liquid cooling CDU system. Direct-to-chip architecture enables processor-level cooling, which makes possible the high power densities that CDU requires in AI GPU supercomputing. Increased efficiency, reduced airflow usage, and improved cooling performance continue to propel the market share leader in hyperscale and HPC deployments.

-

Immersion Cooling

Immersion cooling distribution unit setups are the fastest-growing market. As server density increases and chip-level cooling power increases, full immersion cooling solutions provide improved heat transfer rates. The AI training supercomputer market and advanced computing segments are leading the growth in this sector.

-

Hybrid Cooling Systems

Hybrid or air-to-liquid CDU systems continue to see adoption in transitional data centers during the transition phase of partial liquid integration. Hybrid CDU systems integrate air management with secondary liquid cooling loops.

By End Use

-

Hyperscale Data Centers

CDU in hyperscale data centers currently holds the largest market share. The training of massive-scale AI models, cloud scaling, and the installation of GPU supercomputers demand centralized high-power liquid cooling solutions. Hyperscalers use floor-standing and direct liquid cooling CDU systems to provide rack densities above the conventional maximum.

-

Colocation Facilities

The use of colocation data centers is gaining popularity as customers demand higher density hosting capacity. Data centers are adopting modular CDU solutions to cater to different workloads of their tenants, including AI applications.

-

Enterprise Data Centers

The use of CDUs in enterprise data centers is selective, mainly in organizations that demand quick analytics or on-premises AI infrastructure. Financial constraints are a moderating influence on the pace of adoption from air-cooled infrastructure.

-

Edge Data Centers

The cooling infrastructure for edge data centers is a niche market that is expanding. Real estate limitations and local compute needs favor compact CDU designs, such as in-rack and portable designs.

-

High-Performance Computing (HPC)

CDU for HPC is the fastest-growing application market. Scientific modeling, national research initiatives, and engineering applications are fueling the need for high-density compute clusters with a steady heat load. Liquid cooling adoption within HPC environments is nearly structural, boosting market growth.

Source: Polaris Market Research Analysis

Regional Analysis

North America Coolant Distribution Unit Market Assessment

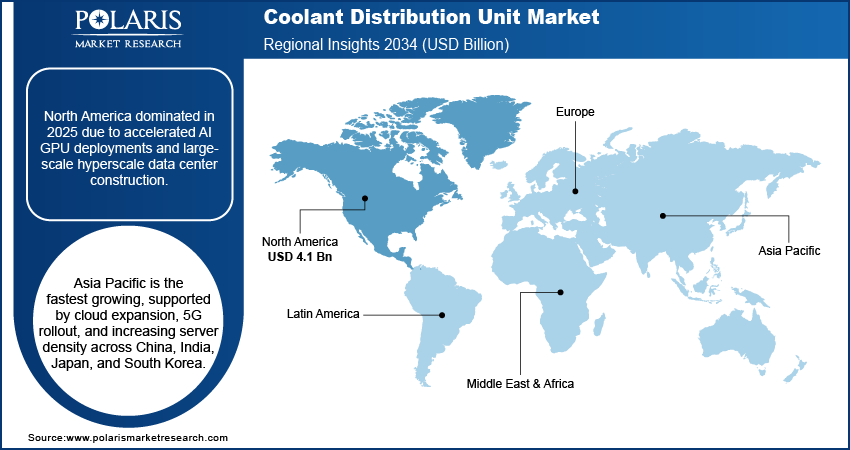

North America led the coolant distribution unit market, driven by rapid expansion of AI-focused hyperscale data centers, particularly in the US. Jones Lang LaSalle IP, Inc. reported that Texas accounted for 6.5 GW of data center capacity under construction, positioning the state to potentially surpass Virginia as the world’s largest data center market by 2030. Also, the top five hyperscalers announced USD 710 billion in planned 2026 capital expenditure to support approximately 35 GW of new or upgraded global capacity. Intensifying deployment of GPU-heavy clusters and AI accelerators pushes rack densities beyond air-cooling thresholds, accelerating transition toward liquid cooling infrastructure.

Asia Pacific Coolant Distribution Unit Market Insight

Asia Pacific is projected to grow at a rapid pace, supported by aggressive AI adoption, 5G rollout, and expansion of cloud infrastructure across China, India, Japan, and South Korea. As per Nokia’s annual Mobile Broadband Index (MBiT) report, the number of 5G subscribers in India was expected to grow 2.65 times to reach 770 million by 2028, up from 290 million in 2024. The increase in server density drives the need for direct-to-chip and scalable in-rack CDU solutions. Hyperscale campuses and colocation projects are further reinforced. Digital growth programs and AI ecosystem development further fuel the adoption of high-efficiency coolant distribution frameworks.

Europe Coolant Distribution Unit Market Overview

Europe advances through regulatory requirements to support carbon neutrality and sustainable data center performance. Energy efficiency constraints limit acceptable PUE levels, thereby necessitating a transition from air-cooled to liquid-cooled infrastructure. In-row CDU solutions are in high demand in retrofit applications, and modular solutions further fuel sovereign cloud and edge strategies.

Middle East Coolant Distribution Unit Market Assessment

The Middle East market grows with hyperscale and colocation investments in the UAE and Saudi Arabia. The hot climate fuels cooling demand, with liquid cooling solutions being preferred over air cooling. Floor-mounted CDU solutions are most popular in large greenfield deployments where centralized distribution is beneficial. AI-driven digital infrastructure investments will accelerate the adoption of innovative thermal management solutions.

Heat Map Analysis

| Region | Market Position | Growth Momentum | Regulatory Strength | Recycling Infrastructure | Secondary Lead Production Base |

| North America | Dominant | High | High | Medium | Low |

| Asia Pacific | High | Very High | Medium | Low–Medium | Low |

| Europe | Medium–High | Medium | Very High | Medium | Low |

| Middle East | Emerging | High | Low–Medium | Low | Low |

Source: Polaris Market Research Analysis

Source: Polaris Market Research Analysis

Cost, ROI & Buyer Guidance Coolant Distribution Unit Market

Liquid cooling decisions are density-driven. Below certain rack thresholds, air systems remain viable. Beyond them, airflow becomes inefficient and energy-intensive. Assessing the cost of coolant distribution units involves going beyond unit economics to density economics, total cost of ownership, and scalability of infrastructure.

Coolant Distribution Unit Cost Breakdown

The cost of CDU capital expense is a function of capacity (kW rating), redundancy scheme, pump design, control integration, and heat exchanger size. Rack-mounted and in-row solutions are generally used for local cooling, while floor-mounted solutions are used for multi-rack cooling.

Cost elements include:

- Heat exchanger and pump assemblies

- Redundant pump design (N or N+1)

- Controls, PLC integration, and monitoring

- Filtration and leak detection systems

- Installation and commissioning

The cost of liquid cooling system per rack improves as density increases because infrastructure is shared across higher compute loads.

CDU Price per kW

CDU price analysis is best evaluated on cost per installed kW:

- <20 kW per rack: Air cooling remains practical

- 20–40 kW: Hybrid economics

- 40–50 kW: Liquid cooling gains cost advantage

- 80 kW: Liquid becomes operationally necessary

This is where CDU vs CRAC vs CRAH economics decisively shift toward liquid architectures.

Total Cost of Ownership (TCO) Framework

A simplified TCO model includes:

- CAPEX: CDU hardware, piping, integration

- OPEX: Pump energy vs high fan energy in air systems

- Space Efficiency: Higher density per rack

- Maintenance: Pump servicing and coolant management

- Scalability: Modular expansion vs overbuilt air systems

In high-density AI clusters, the ROI for liquid cooling is enhanced because of lower energy intensity and higher rack revenue density. In comparison to CDU vs chiller or conventional CRAC/CRAH configurations, liquid cooling systems are less dependent on airflow and offer better thermal control.

Buyer Decision Framework

When to Choose a CDU

Select a CDU when:

- Rack density exceeds 40–50 kW

- GPU-heavy AI clusters are deployed

- Air systems approach thermal limits

- Floor space constraints limit airflow scalability

- Long-term expansion favors liquid infrastructure

Buyer Selection Checklist

Evaluate:

- Redundancy design (N+1 pump configuration)

- Maximum kW capacity per unit

- Compatibility with direct-to-chip or immersion systems

- Leak detection integration

- Commissioning support capability

- Modular expansion options

- Compliance with ASHRAE/OCP liquid guidance

RFP Evaluation Criteria

Focus on:

- Thermal efficiency at target load

- Control integration with DCIM/BMS

- Deployment timeline and commissioning plan

- Scalability without stranded capacity

- Proven AI deployment references

Future Outlook & Emerging Trends

The future of the coolant distribution unit market over the next three to five years is directly tied to the growth of hyperscale infrastructure for AI and the increasing rack density beyond the capabilities of air cooling solutions. The AI data center liquid cooling market reflects ongoing capital investment in liquid-ready infrastructure as the industry standardizes direct-to-chip and immersion architectures in greenfield deployments. As rack power draws near and exceeds 150kW, CDUs transition from nicety upgrades to critical infrastructure. At the same time, energy efficiency mandates and net-zero data center cooling commitments are further driving the adoption of liquid cooling solutions, while the growth of modular CDU solutions supports phased infrastructure development aligned with AI cluster deployments.

| Trend Area | What Is Changing | Market Impact (3–5 Year View) |

| AI-Driven Data Center Expansion | Hyperscale AI clusters scaling rapidly across regions | Sustained demand for high-capacity, AI-ready CDUs |

| 150kW+ Rack Era | Rack densities exceeding 100–150kW becoming mainstream in AI workloads | Liquid cooling becomes structural; higher flow and redundancy requirements |

| Liquid Cooling Standardization | Greater alignment with ASHRAE and OCP guidance | Reduced integration friction; faster CDU deployment cycles |

| ESG & Sustainability Impact | Focus on energy efficiency and heat reuse strategies | Increased adoption of liquid systems supporting net-zero data center cooling |

| Modular Deployment Models | Phased infrastructure scaling | Accelerated modular CDU systems growth across hyperscale campuses |

Source: Polaris Market Research Analysis

Key Players & Competitive Analysis Report

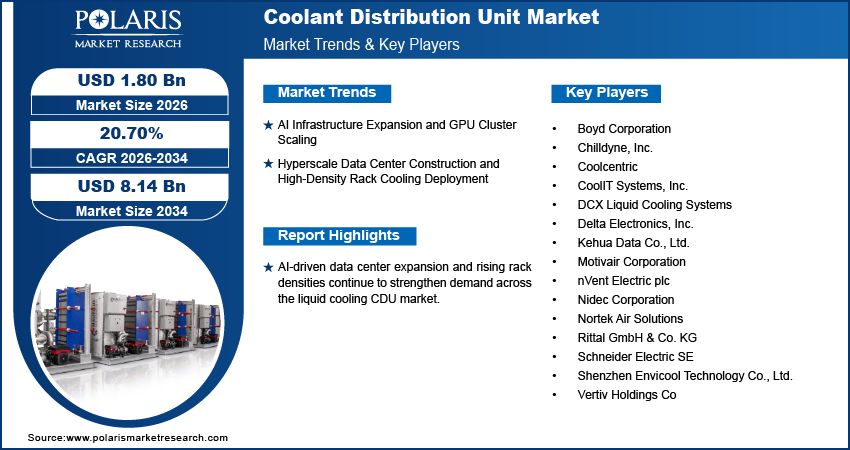

The coolant distribution unit market is moderately concentrated, with the presence of global thermal management firms and liquid cooling innovators. The coolant distribution unit market is differentiated by innovative pump redundancy architecture, control integration, and support for direct-to-chip and immersion cooling solutions as rack densities continue to increase. The major CDU suppliers are increasingly positioning themselves as full-stack liquid cooling infrastructure providers, using their global service infrastructure and strategic CDU OEM partnerships to integrate their solutions directly into rack-level deployments.

The key companies driving the global CDU market are Boyd Corporation, Chilldyne, Inc., Coolcentric, CoolIT Systems, Inc., DCX Liquid Cooling Systems, Delta Electronics, Inc., Kehua Data Co., Ltd., Motivair Corporation, nVent Electric plc, Nidec Corporation, Nortek Air Solutions, Rittal GmbH & Co. KG, Schneider Electric SE, Shenzhen Envicool Technology Co., Ltd., and Vertiv Holdings Co.

Key Players

- Boyd Corporation

- Chilldyne, Inc.

- Coolcentric

- CoolIT Systems, Inc.

- DCX Liquid Cooling Systems

- Delta Electronics, Inc.

- Kehua Data Co., Ltd.

- Motivair Corporation

- nVent Electric plc

- Nidec Corporation

- Nortek Air Solutions

- Rittal GmbH & Co. KG

- Schneider Electric SE

- Shenzhen Envicool Technology Co., Ltd.

- Vertiv Holdings Co

Industry Developments

- January 2026: DCX Data Centres introduced an 8 MW Coolant Distribution Unit with cooling capabilities to support high-density thermal management in data centre environments. The new product introduced efficient cooling performance, thereby increasing choices in Coolant Distribution Unit solutions. (Source: galesburg.com)

- September 2025: Flex enhanced its data center cooling offerings with the introduction of a modular rack-level Coolant Distribution Unit solution for scalable thermal management. The new product strengthened Coolant Distribution Unit solutions by providing efficient and flexible cooling solutions in rack-level environments. (Source: investors.flex.com)

- September 2025: Johnson Controls enhanced its thermal management solutions by introducing a scalable liquid cooling solution with modular Coolant Distribution Units for data center applications. The new solution improved the efficiency of Coolant Distribution Unit solutions, which are required to meet increasing cooling demands in high-density data centers. (Source: johnsoncontrols.com)

Coolant Distribution Unit Market Segmentation

By Type Outlook (Revenue, USD Billion, 2021-2034)

- Floor-Mounted CDU

- In-Rack CDU

- In-Row CDU

- Portable vs Static CDU

By Cooling Technology Outlook (Revenue, USD Billion, 2021-2034)

- Direct-to-Chip

- Immersion Cooling

- Hybrid Cooling Systems

By End Use Outlook (Revenue, USD Billion, 2021-2034)

- Hyperscale Data Centers

- Colocation Facilities

- Enterprise Data Centers

- Edge Data Centers

- High-Performance Computing (HPC)

By Regional Outlook (Revenue, USD Billion, 2021-2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Coolant Distribution Unit Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 1.50 Billion |

| Market Size in 2026 | USD 1.80 Billion |

| Revenue Forecast by 2034 | USD 8.14 Billion |

| CAGR | 20.70% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2022–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Coolant Distribution Unit Market FAQ's

The global market size was valued at USD 1.50 billion in 2025 and is projected to grow to USD 8.14 billion by 2034.

The hyperscale data center is currently dominating the market due to the growing requirement for centralized, high-capacity liquid cooling architectures for massive AI model training, cloud platform scaling, and GPU cluster.

A few of the key players in the market are Boyd Corporation, Chilldyne, Inc., Coolcentric, CoolIT Systems, Inc., DCX Liquid Cooling Systems, Delta Electronics, Inc., Kehua Data Co., Ltd., Motivair Corporation, nVent Electric plc, Nidec Corporation, Nortek Air Solutions, Rittal GmbH & Co. KG, Schneider Electric SE, Shenzhen Envicool Technology Co., Ltd., and Vertiv Holdings Co.

The North America region leads the market due to the fast-growing hyperscale data center market, the high GPU cluster deployment rate, and the quick adoption of liquid cooling infrastructure.

Growth is driven by AI infrastructure scaling, rising rack power densities, hyperscale campus construction, and energy-efficiency mandates supporting liquid cooling adoption.

Download Sample Report of Coolant Distribution Unit Market

Please fill out the form to request a customized copy of the research report.