Data Center Accelerator Market Share, Size, Trends, Industry Analysis Report, 2022 - 2030

REPORT DETAILS

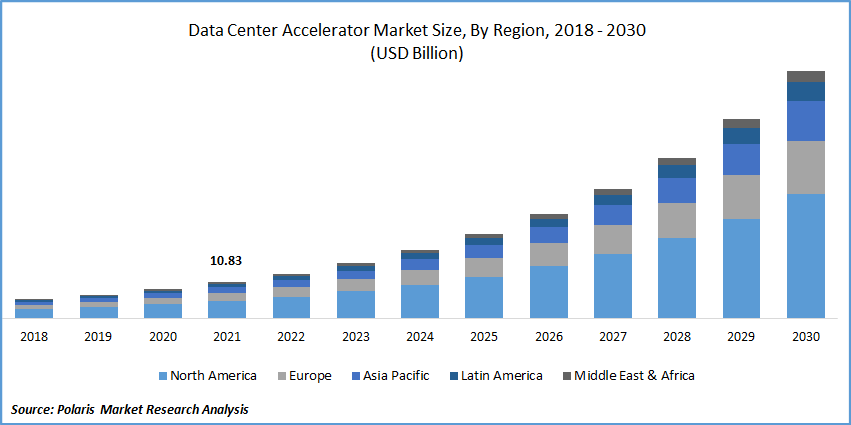

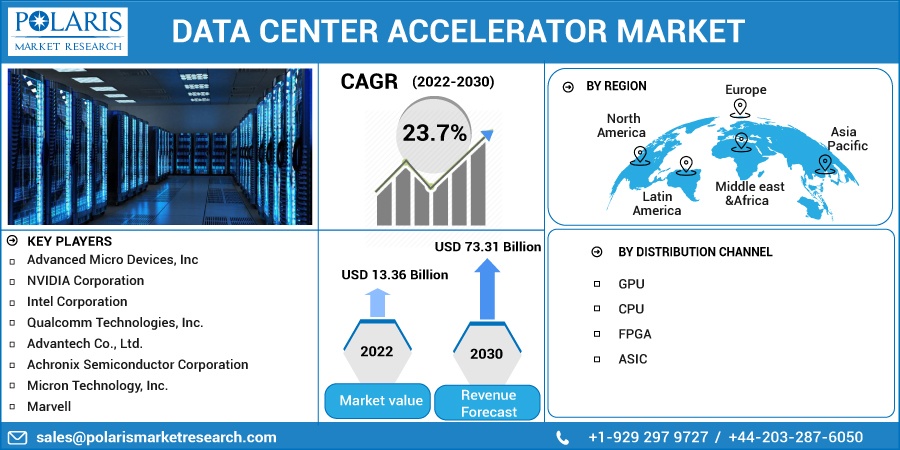

The global data center accelerator market was valued at USD 10.83 billion in 2021 and is expected to grow at a CAGR of 23.7% during the forecast period. The data center accelerator market is expanding due to increased deployment and cloud-based services. Furthermore, the growing adoption of technologies such as artificial intelligence (AI), big data analytics, and internet of things (IoT) is fueling the market’s growth.

Source: Polaris Market Research Analysis

Know more about this report: Download Sample Report

Data center acceleration supports various HPC workloads, including genomics, astrophysics, cyber security, machine learning, big data analysis, modular dynamics, oil and gas, and weather and climate.

There are some difficulties associated with programming and deploying multiple FPGAs. The first difficulty in programming a cluster of FPGAs is determining how to abstract and use the communication links between the FPGAs and how to connect the kernels on multiple FPGAs. A second challenge in building FPGA clusters is deciding how to distribute, coordinate, and manage a multi-FPGA application once it is built. In industrial applications, IoT is expected to generate large amounts of data. Quicksilver Capital estimates that a smart factory will generate 5 petabytes of data per week, while an offshore oil rig will generate 1 to 2 terabytes per day.

New business models that use artificial intelligence, platforms, and algorithms to transform massive amounts of data into insights and value. The World Economic Forum predicts that digitally enabled platform business models will create 70% of new economic value over the next decade.

Increased corporate awareness of the benefits cloud services can provide, increased board pressure to provide more secure and robust IT environments and the establishment of local data centers all contributed to the market growth. Business demand relying on digital infrastructure has increased, resulting in a significance for data center network services across various industries. As more businesses and educational institutions move online, data centers ensure program availability and data security. Healthcare, aerospace, manufacturing, finance, and urban planning are the top industries that use HPC.

University of Texas researchers at Austin are using HPC to advance the science of cancer treatment. In a groundbreaking project in 2017, Researchers examined petabytes of data to look for links between cancer patients' genomes and tumor characteristics. This enabled the university to use HPC for additional cancer research, now expanded to include the diagnosis and treatment of prostate, blood, liver, and skin cancer cases.

The COVID-19 pandemic positively impacted the market because it shifted the focus to digital transformation. Widespread lockdowns have led many universities and institutions to switch to operating and delivering online courses quickly. The education sector is highly receptive to cloud technologies for carrying out and managing tuition, admission exams, and assessments.

Source: Polaris Market Research Analysis

Know more about this report: Download Sample ReportIndustry Dynamics

Growth Drivers

The growing need to improve application performance is expected to drive demand for data center accelerators. Other factors driving market demand include increased data storage requirements, increased use of mobile data, and increased internet usage in businesses. Globally, SMEs and large enterprises are shifting their businesses to a cloud-based module, which is expected to strain data centers and increase demand for accelerators in the coming years. One of the industry's challenges is achieving economies of scale to cover the cost of accelerator deployment and development. They use less power because they can share resources with the main processor and reduce overall costs by improving power efficiency.

Because of the coronavirus disease (COVID-19), a shift toward remote working culture has positively influenced using artificial intelligence (AI) to ease business operations. This necessitates the use of data center accelerators to manage AI workloads. This contributes to the market's growth. In addition, many businesses are providing machine learning (ML) as a cloud service for applications such as voice recognition, voice search, fraud detection, image recognition, recommendation engines, sentiment analysis, and motion detection. This is expected to broaden the applications of data center accelerators worldwide.

Report Segmentation

The market is primarily segmented based on processor and region.

| By Processor | By Region |

|

|

Source: Polaris Market Research Analysis

Know more about this report: Download Sample Report

The GPU Segment Accounted for the Maximum Revenue in 2021

The increasing use of GPU in supercomputing, AI training and inference, drug research, medical imaging, and financial modeling can be attributed to the segment's growth. Furthermore, GPUs are helpful in machine learning and AI in hyper-scale networks and enterprise data centers to perform various calculations.

Cloud service providers such as Microsoft, Amazon, Alibaba, Baidu, and Tencent have adopted FPGAs as a reconfigurable heterogeneous processing asset. Furthermore, advancements in architecture, programming paradigms, and security are expected to result in a broader range of FPGA-based cloud deployment applications around the globe.

North America Accounted for the Largest Revenue in 2021

Significant contributors to regional market growth include prominent market players such as Advanced Micro Devices, Inc., Intel, NVIDIA Corporation, Qualcomm Technologies, Inc., and others, as well as developed technology and data center infrastructure.

During the forecast period, Asia-Pacific is expected to grow the fastest. The region's market growth can be attributed to the increasing adoption of cloud-based services such as IoT and big data analytics. Furthermore, appropriate government policies and the need for data center infrastructure upgrades in Asia Pacific are driving the region's data center accelerator market growth in the given forecast period.

Competitive Insight

Some major players operating in the global market include:

- Advanced Micro Devices, Inc,

- Advantech Co., Ltd.,

- Intel Corporation,

- NVIDIA Corporation,

- Qualcomm Technologies, Inc.,

- Achronix Semiconductor Corporation,

- Marvell,

- KIOXIA Holdings Corporation,

- Micron Technology, Inc.,

- Western Digital Technologies.

Recent Developments

In August 2025: Intel Corporation entered a USD 2.00 billion investment deal with SoftBank Group. This partnership aims to strengthen Intel's semiconductor innovation and meet the rising demand for AI accelerators in data centers.

In August 2025: Alphabet's Google Cloud secured a six-year cloud computing deal worth over USD 10.00 billion with Meta Platforms. The agreement covers servers, storage, networking, and other cloud services to support Meta's AI infrastructure growth.

In January 2025: Amazon Web Services (AWS) announced a USD 100.0 million expansion of its Generative AI Innovation Center. This effort aims to speed up the development of AI systems and provide customers with tools to use advanced AI in their operations.

In November 2024: Alphabet's Google Cloud launched a new AI accelerator for large language models (LLMs). Built on custom tensor processing units (TPUs), it improves the performance and efficiency of LLMs in data centers, meeting the growing need for AI-based applications.

Data Center Accelerator Market Report Scope

| Report Attributes | Details |

| Market size value in 2022 | USD 13.36 billion |

| Revenue forecast in 2030 | USD 73.31 billion |

| CAGR | 23.7% from 2022 - 2030 |

| Base year | 2021 |

| Historical data | 2019 - 2021 |

| Forecast period | 2022 - 2030 |

| Quantitative units | Revenue in USD billion and CAGR from 2022 to 2030 |

| Segments covered | By Processor, By Region |

| Regional scope | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Key Companies | Advanced Micro Devices, Inc, NVIDIA Corporation, Intel Corporation, Qualcomm Technologies, Inc., Advantech Co., Ltd., Achronix Semiconductor Corporation, Micron Technology, Inc., Marvell, KIOXIA Holdings Corporation, Western Digital Technologies |

Source: Polaris Market Research Analysis

Data Center Accelerator Market FAQ's

The global Data Center Accelerator Market is expected to reach USD 73.31 billion by 2030, driven by rising demand for AI, deep learning, and high-performance computing.

Data center accelerators improve computing performance by handling intensive workloads like AI, machine learning, and analytics faster and more efficiently than traditional processors.

Technologies such as artificial intelligence (AI), deep learning, big data analytics, and cloud computing are major growth drivers as they require high-speed parallel processing.

The GPU segment dominates because GPUs offer strong parallel processing power essential for AI training, inference, and high-performance workloads.

High implementation costs and power consumption remain obstacles, especially for smaller data centers and cost-sensitive operations.

North America holds a major portion of market revenue due to advanced tech infrastructure, while Asia Pacific is expected to grow rapidly with rising cloud and AI adoption.

Use cases include AI model training, natural language processing, deep learning tasks, big data processing, and high-performance cloud services, where standard CPUs struggle to keep up.

Download Sample Report of Data Center Accelerator Market

Please fill out the form to request a customized copy of the research report.