Gypsum board Market Share, Size, Industry Analysis Report, 2026 - 2034

REPORT DETAILS

Gypsum board Market Summary

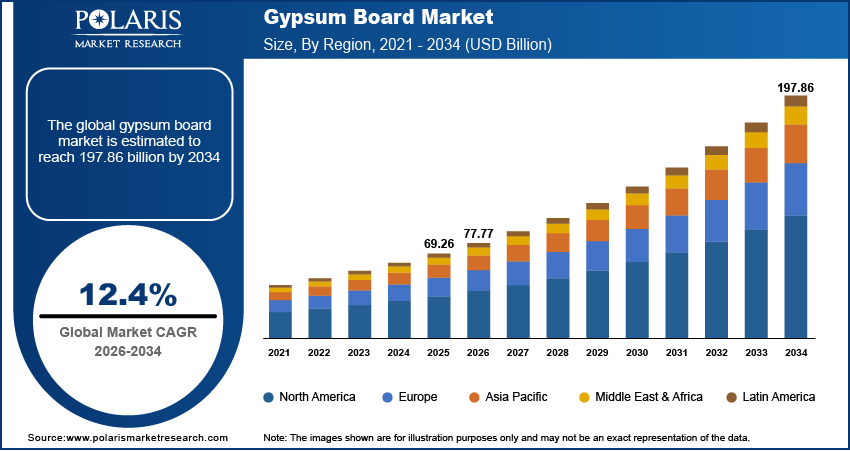

The global gypsum board market is estimated around USD 69.26 billion in 2025,with consistent growth anticipated during 2026–2034. The market is projected to grow at a CAGR of 12.4% during the forecast period. This is driven by expanding residential and commercial construction, rising use of lightweight, cost-efficient wall systems, and increased adoption of gypsum boards in renovation and remodeling projects globally.

Market Statistics

Key Takeaways

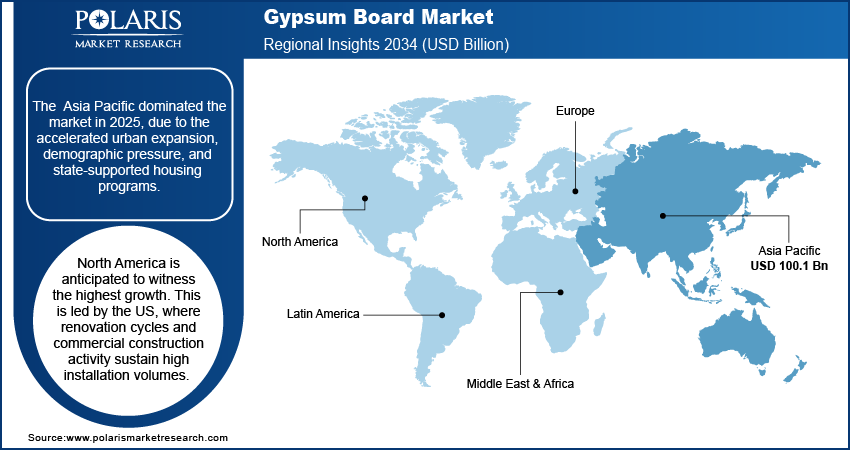

- The Asia Pacific dominated the market with a 44.9% revenue share in 2025. This is due to the growing urban expansion and state-supported housing programs.

- North America is anticipated to witness the fastest growth at a 13.1% CAGR. Renovation cycles and commercial construction contribute to the regional market growth.

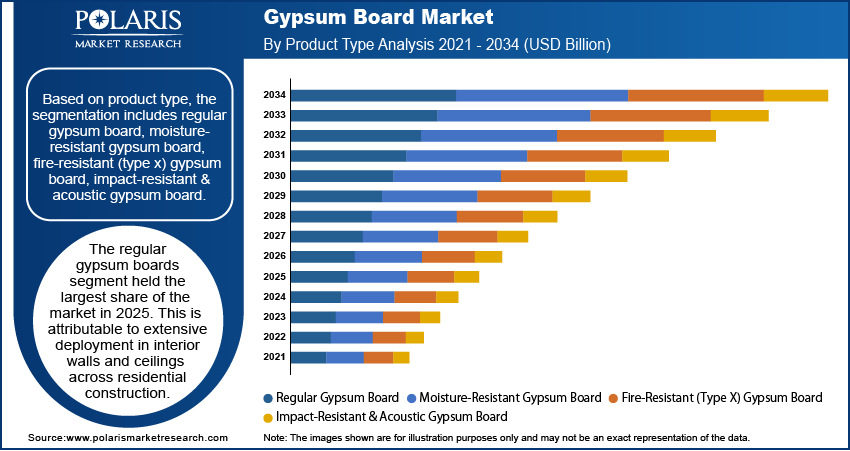

- The regular gypsum boards segment accounted for a 58.7% market share in 2025. This is primarily due to the widespread use of regular boards in the interior walls and home ceilings.

- The residential construction segment led with a 52.4% revenue share in 2025. Housing expansion and infrastructure investment contribute to the segment’s leading position.

- The commercial construction segment accounted for a 38.6% share in 2025. Higher usage rates of fire-resistant and acoustic gypsum boards drive the segment’s growth.

Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations.

Future Demand Scenarios

- Base scenario: Demand grows steadily with ongoing residential and commercial construction activity, supported by renovation, interior finishing, and drywall replacement projects.

- Upside scenario: Faster adoption of gypsum boards in green buildings, rising investment in large commercial complexes and healthcare infrastructure, and wider use of fire-resistant and moisture-resistant board variants.

- Conservative scenario: Slowdown in construction spending, delays in real estate projects, and reduced renovation activity across residential and commercial sectors.

Industry Dynamics

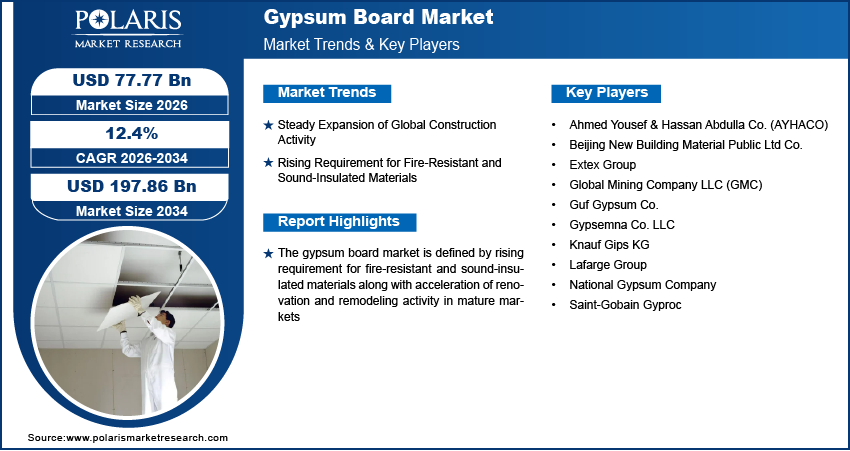

- Steady Expansion of Global Construction Activity

- Rising Requirement for Fire-Resistant and Sound-Insulated Materials

- Moisture Sensitivity Constraints Restraining market growth

- Sustainable Construction Adoption Creating Opportunities

AI Impact on Gypsum Board Market

- AI technology helps increase efficiency in the production process of gypsum boards through the reduction of waste materials.

- It aids in quality control through the detection of flaws and the uniformity in board thickness and durability.

- AI facilitates predictive maintenance through early detection of any equipment problems, leading to lower machine downtime.

- It enables effective supply chain and demand forecasting management.

What is Gypsum Board and Why It Matters

Gypsum boards also known as drywall or plasterboard support modern interior construction by improving build speed, cost control, and finish consistency. This gypsum board definition refers to prefabricated panels made from a gypsum core with paper liners, enabling fast and uniform installation. The gypsum wall board finds applications in walling, ceilings, partitioning, and linings in the plasterboard market, which is creating a concise market analysis in terms of efficiency and scalability. The usage of gypsum wall boards in the market is increasing as they improve the duration of projects in the construction industry and reduce cost on the overall project expenditure. The usage of gypsum wall boards in the market is steady in the residential, business, and industrial sectors.

Source: Polaris Market Research Analysis

The gypsum board market is becoming more competitive as construction activity shifts toward faster execution and tighter cost control, with gypsum board demand rising across housing, commercial interiors, and infrastructure projects. The is due to the adoption of dry construction technology, characterized by minimal construction work, come from the influence of urbanization, energy conservation construction, and the shortage of construction labor. The adoption of modular construction materials and building materials takes precedence in regions where the construction technique has gained popularity, and construction material is based on installing pre-manufactured panels. The gypsum board industry has now undergone a transformation, where it has increased in value in terms of a construction material in construction.

Gypsum Board vs Plaster vs Cement Board

| Property | Gypsum Board | Plasterboard |

| Ease of Installation | Easy and quick | Tedious |

| Weight | Low | High |

| Finish | Smooth and consistent | Needs finishing |

| Resistance to Fire | Excellent | Good |

| Resistance to Moisture | Moderate (special gypsum boards) | Low |

| Areas of Use | Walls, ceilings and interiors | Plastering walls |

Source: Polaris Market Research Analysis

Drivers & Opportunities

Steady Expansion of Global Construction Activity

Continuous growth in construction activities are significantly increasing the demand for gypsum board globally. This growth is most visible in developing nations, where growth in construction is seen in sync with population migration. According to Oxford Economics, global construction output is projected to expand from USD 9.7 trillion in 2022 to USD 13.9 trillion by 2037, led by China, the US, and India, supported by urbanization and green infrastructure development. The factors driving the demand for drywalling are bolstered by the growing importance of rapid cycle times and cost-effective interior systems. Gypsum boards facilitate this growth by offering shorter construction periods. With increasing developments in housing, non-residential structures, and civic construction, gypsum boards continue to be favored in the construction of interiors.

Rising Requirement for Fire-Resistant and Sound-Insulated Materials

Stricter building safety norms increase the use of building fire safety materials across residential and commercial projects. It leads to increased usage of fire-resistant coatings gypsum board systems that function to slow the spread of fire and hold strength. Type X and fire-rated gypsum or plasterboard finds increased application in high occupancy and healthcare buildings, and in relation to transportation infrastructure. Noise control demands further drive this trend. Gypsum board offers acoustic insulation without contributing to the structural load.

Acceleration of Renovation and Remodeling Activity in Mature Markets

Aging buildings in North America and Europe creating continuous demand in the market for renovation of gypsum board. According to the European Commission, the Renovation Wave strategy aims to upgrade the renovation of 35 million buildings by 2030, doubling the pace of energy-efficient renovations per annum in the EU. Property owners invest in drywall remodeling demand to improve energy performance, safety compliance, and interior layouts. Gypsum boards facilitate easy rearrangement in renovation cycles. Renovation materials in buildings are tending towards drywall construction due to its compatibility with improvements in insulation, firefighting, and acoustic enhancement.

Restraints & Challenges

Moisture Sensitivity Constraints

Moisture exposure continues to surface as a practical constraint across several use cases, placing clear gypsum board limitations on where standard panels perform reliably. In high-humidity regions or wet-area installations, moisture sensitive drywall faces durability risks that shorten service life and raise maintenance needs. These plasterboard disadvantages push builders to specify moisture-resistant variants or alternative materials, which adds cost and narrows design flexibility in price-sensitive projects.

Raw Material and Energy Cost Volatility

Unstable input pricing remains a persistent pressure point, as gypsum board raw material costs fluctuate alongside energy markets and logistics conditions. Economies of manufacturing are made visible. Energy-intensive drying processes as well as transport costs make drywall production more difficult in terms of margins, especially when fuel and electricity costs are high. This reflects the complexity of construction materials that face market volatilities in pricing, contract, and capacity programming.

Emerging Opportunities

Sustainable Construction Adoption

Sustainability priorities are driving changes in material selection for the construction industry, which is fueling the sustainable gypsum board market. With energy efficiency regulations, environment-friendly emission standards, and certification needs for sustainable development, sustainable construction materials are employed by constructors and real estate participants. This presents emerging market pockets for eco-friendly drywall materials that avoid any damage to the environment and are less expensive in terms of installation.

High-Performance Product Expansion

High performance gypsum board offerings such as acoustic drywall for noise control and impact resistant plasterboard for high-traffic environments are boosting across commercial buildings, healthcare facilities, and institutional projects. These products enjoy better pricing due to their enhanced durability and application-specific benefits that create premium growth opportunities within the gypsum board market.

Renovation and Remodeling Trends

An increased emphasis on renovation and interior remodeling across sectors, including residential, commercial, and institutional buildings, is boosting global demand for gypsum boards. Houses, companies, hotels, offices, and retail stores are increasingly allocating budgets for interior renovation to enhance appearance, performance, and asset value. Gypsum boards are gaining popularity in renovation applications owing to their light weight, ease of installation, and lower construction duration when compared to regular wall structures. Also, due to their smooth surface and good looks, they can be used in modern ceilings, partition walls, decorative walls, and customized interior purposes. In commercial renovations, using gypsum boards helps reduce disruptions during installation as it is fast and neat. Moreover, city redevelopment initiatives and modernizing existing infrastructure will boost the use of gypsum boards for renovation purposes.

Source: Polaris Market Research Analysis

Segmental Insights

This report provides granular coverage of the gypsum board market product type, installation type, application, enabling readers to identify the fastest-growing and most profitable demand pockets.

By Product Type

-

Regular Gypsum Board

The regular gypsum boards segment accounted around 38–40% of the market in 202 and has retained the leading market position among the standard plasterboards. This is primarily due to widespread use of regular boards in the interior walls and ceilings of homes. Ease of use and cost-effectiveness make regular boards the popular option for mass housing construction, especially for developing nations. The basic plasterboard market has traditional links with mass housing activities.

-

Moisture-Resistant Gypsum Board

Moisture-resistant gypsum boards represented nearly 18% of the market in 2025. Demand concentrates in kitchens, bathrooms, basements, and coastal regions where humidity exposure is persistent. Water resistant drywall adoption is reinforced by heightened awareness of mold prevention and indoor air quality. The bathroom drywall market continues to expand as residential and mixed-use buildings prioritize moisture control within interior envelopes.

-

Fire-Resistant (Type X) Gypsum Board

Fire-resistant gypsum boards accounted for around 22% of total revenue in 2025. The enforcement of fire safety norms in the case of commercial and institutional structures is currently maintaining the size of this particular market. The Type X gypsum board market is currently driven by the compulsory requirement for fire-rated wall construction. The fire rated drywall industry is expected to register a CAGR of more than 6% by the year 2034.

-

Impact-Resistant & Acoustic Gypsum Board

Specialty plasterboard, including impact-resistant and acoustic variants, collectively held about 20–22% market share in 2025. These are increasingly used in heavy-traffic areas. Use of impact-resistant gypsum board is increasing in the education and healthcare sectors, whereas the acoustic drywall market is driven by the hospitality and office segments, which want controlled sound performance.

Gypsum Board Market - Product Type Comparison

| Product Type | Typical Usage | Cost Position | Key Advantage | Primary Applications |

| Regular Gypsum Board | Standard interior wall and ceiling construction | Low | Cost efficiency and ease of installation | Residential housing, mass apartments, basic commercial interiors |

| Moisture-Resistant Gypsum Board | Interior areas exposed to humidity | Medium | Reduced moisture absorption and mold risk | Bathrooms, kitchens, basements, coastal residential and commercial buildings |

| Fire-Resistant (Type X) Gypsum Board | Fire-rated wall and ceiling assemblies | Medium–High | Enhanced fire resistance and code compliance | Commercial buildings, hospitals, schools, corridors, stairwells |

| Impact-Resistant Gypsum Board | High-traffic and abuse-prone environments | High | Improved surface durability and impact tolerance | Educational institutions, healthcare facilities, public buildings |

| Acoustic Gypsum Board | Noise-sensitive interior environments | High | Sound absorption and noise control | Hotels, offices, auditoriums, studios, conference rooms |

| Specialty Gypsum Board (Hybrid Variants) | Projects requiring multiple performance attributes | High | Combined fire, moisture, and acoustic performance | Premium commercial projects, institutional infrastructure |

Source: Polaris Market Research Analysis

By Installation Type

-

New Construction

New construction represented about 62% of the gypsum board demand in the year of 2025. Growth is driven by housing expansion and infrastructure investment across emerging markets. The building construction materials for new projects are increasingly shifting towards the use of gypsum boards due to their speed of construction and the ability of the vendors to control costs.

-

Repair & Renovation

Repair and renovation represented 38% of total demand, with strong penetration across North America and Europe. Aging infrastructure, along with increasing investments in interior renovation, is responsible for sustaining this segment. Gypsum board renovation market is driven by drywall renovation trends, including renovation led by space remodeling & upgrading. The renovation building material market is increasing, attributing to shorter renovation life.

By Application

-

Residential Construction

Residential construction dominated the market with approximately 45% revenue share in 2025. The increased pace of real estate development in the Asia Pacific and the Middle East supports the leading market position. Drywall applications in the residential segment include apartments, villas, and low-cost housing due to the short cycle times associated with these products.

-

Commercial Construction

Commercial applications accounted for nearly 35% of global revenue in 205. Office structures, retail, hotels, as well as healthcare facilities comprise the major consumers. Higher usage rates of fire-resistant as well as acoustic gypsum boards determine commercial gypsum board market demand. Performance compliance, along with aesthetic flexibility, emphasizes commercial buildings made of drywall.

-

Industrial & Institutional

Industrial and institutional applications held around 20% market share. Factories, warehouses, institutions of learning, and public sector undertakings, demand gypsum boards of specific durability and regulatory requirements. The use of industrial gypsum board is essentially tied to institutional drywall demand where more attention is laid to compliance rather than costs. The construction materials sector is increasingly demanding standardized gypsum systems in public sector applications.

Application Segment Analysis

| Segment | Market Share Ranking | Fastest-Growing Indicator | Key Driver |

| Residential Construction | High | Yes | Large-scale urban housing development and cost-effective interior partitioning |

| Commercial Construction | High | No | Demand for fire-rated and acoustic drywall in offices, retail, and healthcare facilities |

| Industrial & Institutional | Medium | No | Compliance-driven demand in factories, warehouses, schools, and public infrastructure |

Source: Polaris Market Research Analysis

Source: Polaris Market Research Analysis

Regional Analysis

Asia Pacific Gypsum Board Market Assessment

Asia Pacific dominated the global gypsum board market in 202, accounting for over 38% of total revenue, driven by accelerated urban expansion, demographic pressure, and state-supported housing programs. According to UN-Habitat, it is estimated that by 2050, the urban population to increase by 50% in Asia, adding approximately 1.2 billion people. The large volumes absorbed by residential towers, public infrastructure, and mixed-use developments have marked the scale of the drywall market in the Asia Pacific gypsum board market. China, India, and Southeast Asia continue to record firm construction pipelines, placing construction growth in Asia Pacific as a sustained demand catalyst. The region is expected to record the fastest CAGR, reflecting continuous project launches and broad-based material consumption.

North America Gypsum Board Market Insights

North America represents the fastest-growing regional market, contributing roughly 24% of global revenue during forecast period. According to LIRA, homeowner spending on renovations reached USD 463 billion in the first quarter of 2024. The US spearheads the North America gypsum board market, driven by renovation cycles and commercial construction that keeps installation volumes high. In the US drywall market, demand is influenced by the preference for fire-rated and impact-resistant boards in multifamily housing, healthcare, and institutional buildings. This structural shift toward performance-oriented wall systems continues to elevate plasterboard demand in North America across new builds and retrofit projects.

Europe Gypsum Board Market Overview

Europe captured approximately 21% of the global market in 2025, driven by constant demands in the UK, Germany, and French markets, where there are more renovations compared to new buildings. Harmonized policies in the Europe region encourage the use of certified systems in the plasterboard sector. The Europe region's focus on low-carbon and recyclable resources drives the use of sustainable building materials.

Middle East & Africa Gypsum Board Market Snapshot

The Middle East & Africa accounted for nearly 9% of global revenue, driven by infrastructure projects, commercial building projects for real estate, and tourism-related construction activities. As stated by the International Trade Administration, the government aims at increasing the direct contribution of tourism to the country’s GDP from 4.4% to 10% by the year 2030. The Middle East market for gypsum board is driven by several large projects in the GCC, thus securing strong GCC drywall demand in the hotel, commercial, and transport sector projects.

Latin America Gypsum Board Market Overview

Latin America maintained an almost 8% market share in the year 2025, with Brazil and Mexico showing prominence in the future demands. The Latin America gypsum board industry develops with the support of housing development. The demand for drywall in Latin America is a gradual process that is influenced by economic developments. Brazil maintains the dominance of the plasterboard industry of Brazil.

Heat Map Analysis

| Region | Demand Intensity | Construction Activity | Product Mix Sophistication | Regulatory Influence | Growth Momentum |

| Asia Pacific | Very High | Very High | Medium | Medium | Very High |

| North America | High | High | High | Medium–High | High |

| Europe | Medium–High | Medium | High | Very High | Medium |

| Middle East & Africa | Medium | Medium–High | Medium | Low–Medium | Medium |

| Latin America | Medium | Medium | Medium | Low–Medium | Medium |

Source: Polaris Market Research Analysis

Source: Polaris Market Research Analysis

Key Players & Competitive Analysis Report

The gypsum board industry is moderately concentrated, with a highly active gypsum board market due to the involvement of worldwide drywall producers along with traditional regional plasterboard makers. The major companies are enhancing their strength by developing their gypsum board products, focusing on their sustainable manufacturing processes based on the changing norms and widespread distribution networks of their products in the construction of residential, commercial, as well as infrastructure works. The key areas of focus are lightweight gypsum boards, moisture-resistant, fire-resistant, and recycled gypsum.

The gypsum board manufacturers’ strategy increasingly centers on partnerships with distributors, builders, and contractors to secure long-term supply relationships and improve market access. Regional drywall competition remains intense in Asia Pacific, where local producers compete aggressively on pricing and volume, while global gypsum board manufacturers in North America and Europe emphasize product performance, certifications, and compliance-driven differentiation. This dynamic continues to shape the competitive positioning of plasterboard market players across major construction regions.

Key companies operating in the global gypsum board market include Ahmed Yousef & Hassan Abdulla Co. (AYHACO), Beijing New Building Material (BNBM) Public Ltd Co., Extex Group, Global Mining Company LLC (GMC), Guf Gypsum Co., Gypsemna Co. LLC, Knauf Gips KG, Lafarge Group, National Gypsum Company, and Saint-Gobain Gyproc.

Key Players

- Ahmed Yousef & Hassan Abdulla Co. (AYHACO)

- Beijing New Building Material (BNBM) Public Ltd Co.

- Extex Group

- Global Mining Company LLC (GMC)

- Guf Gypsum Co.

- Gypsemna Co. LLC

- Knauf Gips KG

- Lafarge Group

- National Gypsum Company

- Saint-Gobain Gyproc

Premium Insights

Market Size Reconciliation Insight

Differences in gypsum board market sizing across published studies typically stem from scope mismatches. Some sources blend boards with installation services, others extend coverage unevenly by region, and many mix drywall market value vs volume metrics without clear separation. Polaris resolves these issues by identifying the sales of the factory gate board alone, with a specific narrow market definition for plasterboards that improves comparability and trend identification.

Sustainability & Circular Economy Insight

Sustainability has become part of purchasing decisions, moving from a compliance requirement to be part of the selection criteria. The sustainability trends for gypsum board indicate increasing market interest in sustainable products with recycled materials, sustainable sources, and environmental attributes. The popularity of the recycled drywall market continues to grow with more purchasing aligned with ESG goals, increasing the usage of green plasterboards.

Renovation-Led Growth Insight

In mature economies, the demand from renovation activities accounts for a large part of the consumption. Remodeling activity favors suppliers with dense distribution reach, rapid replenishment, and consistent SKU availability rather than sheer production scale. This places further reinforcement on drywall growth by remodeling, wherein speed to site and channel efficiency are more important for market share capture than installed capacity.

Future Outlook

The gypsum board market forecast indicates steady expansion through 2034, anchored by sustained urban housing demand, rising renovation intensity, and product innovation linked to sustainability and performance standards. The growth momentum continues to remain strong in the Asia-Pacific region, as volume demand gets driven by large-scale residential development and infrastructure creation activities. The North American and European markets follow a different growth path, registering steady demand driven by replacement demand and renovation and upgrading activities. The drywall market is poised to favor manufacturers that balance scale and reactiveness as demand gets driven by factors of speed, availability, and compliance factors. The outlook for the plasterboard market also continues to remain fine and steady as it gets driven by construction and building practices and not mere growth.

What to Watch Next:

| Trend / Development | What to Monitor | Potential Market Impact |

| Urban housing expansion | New residential project approvals & affordable housing schemes | Sustained volume growth, or a baseline or "normal" volume |

| Renovation and remodeling activity | Residential and Non-Residential Spending Trends | Stable Replacement Demand and Accelerated Inventory Turns |

| Sustainable gypsum board adoption | Recycled material usage and environmental certification | Product differentiation and premium pricing potential |

| Shift toward prefabricated construction | Penetration of Modular and Off-Site Construction Practices | Demand for Standardized Fast-installation Boards |

| Raw material and energy cost trends | Gypsum, Paper Liner, and Power Price Movements | There is an |

| Distribution and logistics efficiency | Regional plant capacities and last-mile delivery capability | Volatility of margins and pricing adjustments |

Source: Polaris Market Research Analysis

Industry Developments

- In May 2025, Knauf India launched DewBloc Gypsum Plasterboard, a moisture-resistant gypsum board for high-humidity interior applications. The product strengthened gypsum board offerings by addressing durability and moisture-protection requirements in modern construction. (Source: constructionweekonline.in)

- In October 2024, Saint-Gobain Canada announced CarbonLow, a gypsum wallboard line with up to 60% lower embodied carbon, to be produced at North America’s first zero-carbon gypsum facility near Montreal. In June 2024, USG, a Knauf subsidiary, began gypsum production at its new Avery Quarry in Michigan, targeting 550,000 tons in 2025 to offset declining synthetic supply. (Source: saint-gobain.com)

Gypsum Board Market Segmentation

By Product Type Outlook (Revenue, USD Billion, 2021-2034)

- Regular Gypsum Board

- Moisture-Resistant Gypsum Board

- Fire-Resistant (Type X) Gypsum Board

- Impact-Resistant & Acoustic Gypsum Board

By Installation Type Outlook (Revenue, USD Billion, 2021-2034)

- New Construction

- Repair & Renovation

By Application Outlook (Revenue, USD Billion, 2021-2034)

- Residential Construction

- Commercial Construction

- Industrial & Institutional

By Regional Outlook (Revenue, USD Billion, 2021-2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Gypsum Board Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 69.26 Billion |

| Market Size in 2026 | USD 77.77 Billion |

| Revenue Forecast by 2034 | USD 197.86 Billion |

| CAGR | 12.4% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Gypsum board Market FAQ's

The global market size was valued at USD 69.26 billion in 2025 and is projected to grow to USD 197.86 billion by 2034.

The?Asia Pacific region holds the largest share in the gypsum board market, driven by accelerated urban expansion, demographic pressure, and state-supported housing programs.

Regular gypsum boards is the primary segment of product type due to extensive deployment in interior walls and ceilings across residential construction.

A few of the key players in the market are Ahmed Yousef & Hassan Abdulla Co. (AYHACO), Beijing New Building Material (BNBM) Public Ltd Co., Extex Group, Global Mining Company LLC (GMC), Guf Gypsum Co., Gypsemna Co. LLC, Knauf Gips KG, Lafarge Group, National Gypsum Company, and Saint-Gobain Gyproc.

Key factors include steady expansion of global construction activity coupled with rising requirement for fire-resistant and sound-insulated materials.

Download Sample Report of Gypsum board Market

Please fill out the form to request a customized copy of the research report.