Hemostasis Valve Market Growth, Trends, Industry Report, 2025-2034

REPORT DETAILS

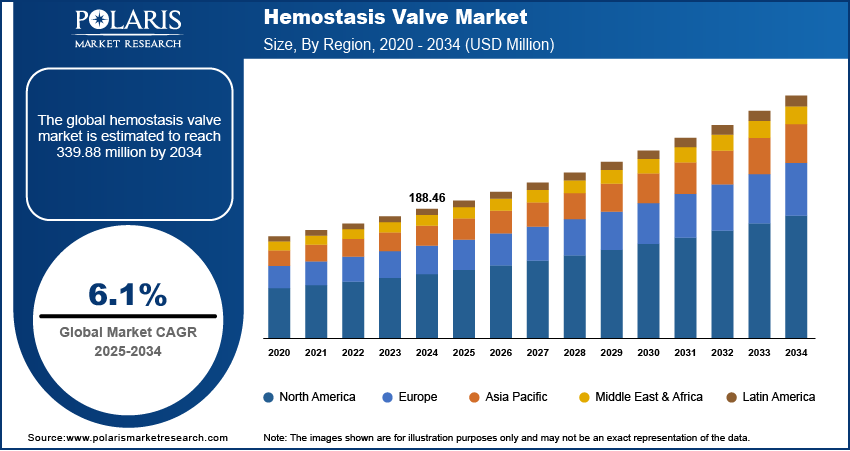

Hemostasis Valve Market Summary

The global hemostasis valve market size was valued at USD 188.46 million in 2024, growing at a CAGR of 6.1% from 2025 to 2034. The growth is driven by rising number of cardiovascular and interventional procedures and growth in minimally invasive surgeries.

Market Statistics

Key Takeaways

- In 2024, the hemostasis valve Y- connectors segment dominated with the largest share due to their widespread use in various interventional procedures.

- The one- handed hemostasis valves segment is expected to experience significant growth during the forecast period due to its ergonomic design and ease of operation.

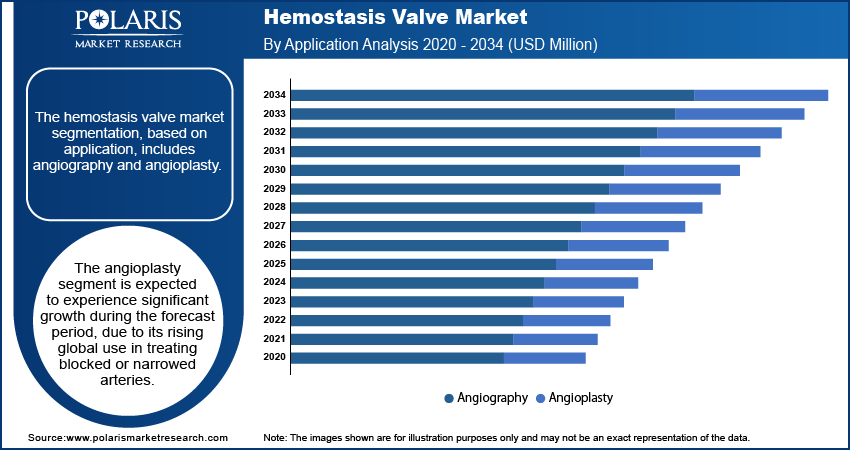

- The angioplasty segment is expected to experience significant growth during the forecast period due to its rising global use in treating blocked or narrowed arteries.

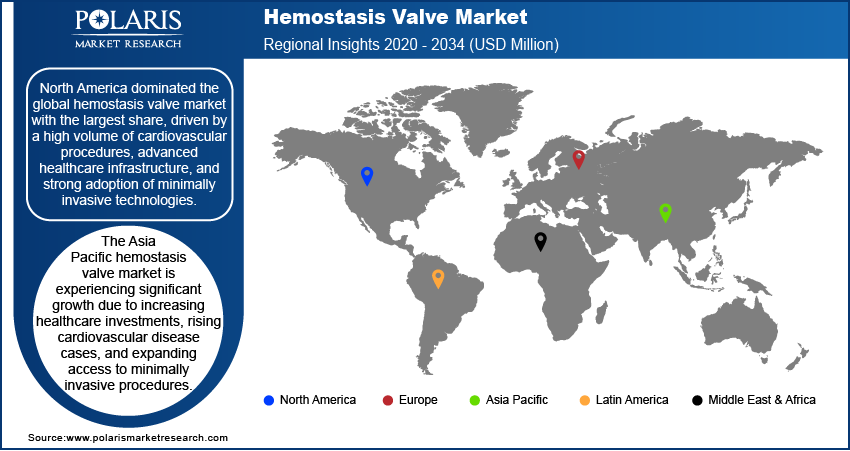

- The market in North America dominated with the largest share in 2024, driven by a high volume of cardiovascular procedures, advanced healthcare infrastructure, and strong adoption of minimally invasive technologies.

- The market in the U.S. is expected to witness significant growth in the coming years due to its high healthcare spending, advanced hospital systems, and large aging population affected by heart disease.

- The market in Asia Pacific is projected to witness substantial growth during 2025–2034 due to increasing healthcare investments, rising cardiovascular disease cases, and expanding access to minimally invasive procedures.

A hemostasis valve is a medical device used during catheter-based interventional procedures to prevent blood loss while allowing instruments to pass through vascular access sites. It typically features a sealing mechanism that maintains hemostasis when guidewires, catheters, or other devices are introduced or withdrawn. These valves are essential for maintaining a sterile field and minimizing the risk of complications such as bleeding or air embolism.

Interventional radiology and cardiology are rapidly growing medical fields due to their non-surgical, image-guided approach to diagnosing and treating diseases. These procedures involve inserting catheters into blood vessels, requiring devices that maintain hemostasis to prevent bleeding and maintain sterility. Hemostasis valves are indispensable in such procedures for controlling blood flow during device exchange. The demand for efficient, easy-to-use hemostasis valves rise as hospitals expand their interventional departments and adopt more catheter-based treatments for cancer, vascular diseases, and neurological conditions, thereby driving the growth.

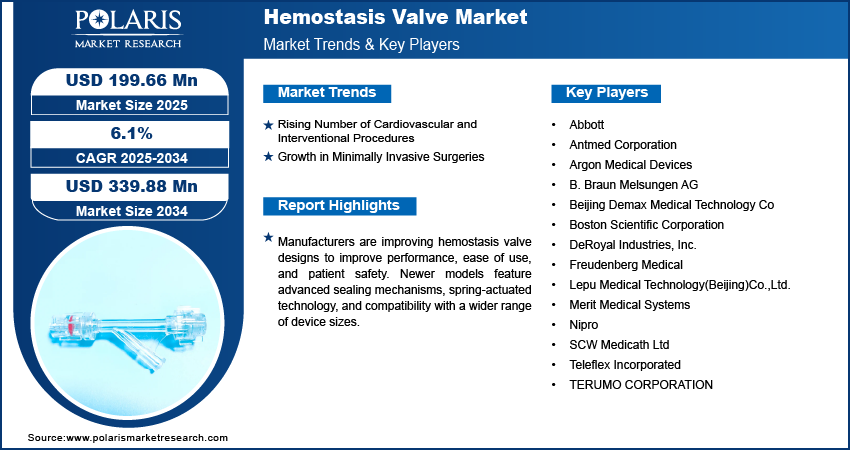

Manufacturers are improving hemostasis valve designs to improve performance, ease of use, and patient safety. Newer models feature advanced sealing mechanisms, spring-actuated technology, and compatibility with a wider range of device sizes. These innovations reduce blood leakage, improve operator control, and shorten procedure time. Additionally, valves are increasingly being designed to integrate smoothly with other interventional devices and procedure packs, increasing their utility in streamlined workflows. Advanced hemostasis valves are becoming preferred choices as hospitals and clinicians seek reliable, efficient tools for complex procedures, thereby driving the growth.

Source: Polaris Market Research Analysis

Industry Dynamics

- The rising number of cardiovascular and interventional procedures is driving the demand for coating pretreatments.

- Growth in preference for minimally invasive surgeries is fueling the industry.

- Manufacturers are improving hemostasis valve designs to improve performance, ease of use, and patient safety.

- High cost of advanced hemostasis valves and limited access in low-resource settings restrict widespread adoption, especially in developing regions.

Rising Number of Cardiovascular and Interventional Procedures: The growing prevalence of cardiovascular diseases, such as heart attacks, coronary artery disease, and arrhythmias, has significantly increased the number of catheter-based interventional procedures. According to the World Health Organization, in Europe alone, cardiovascular disease causes 10,000 deaths every day. Hemostasis valves play a major role in these procedures by minimizing blood loss while allowing safe passage of catheters and guidewires. The demand for minimally invasive interventions is on the rise with aging populations and sedentary lifestyles contributing to heart-related conditions globally. This, in turn, drives consistent demand for hemostasis valves as essential components in angioplasty, electrophysiology, and structural heart procedures across hospitals and specialty clinics worldwide, thereby driving the growth.

Growth in Minimally Invasive Surgeries: Minimally invasive surgeries (MIS) are gaining popularity due to their various benefits such as shorter recovery times, fewer complications, and reduced hospital stays. Procedures such as angioplasty, catheter ablation, and embolization rely heavily on catheter-based access systems where hemostasis valves are used. The demand for such valves is rising in parallel with the broader shift from traditional open surgeries to image-guided, catheter-driven techniques. The requirement for reliable vascular access management tools grows as more healthcare systems and patients opt for MIS, making them essential for safe, efficient procedural outcomes.

Source: Polaris Market Research Analysis

Segmental Insights

Type Analysis

The segmentation, based on type, includes hemostasis valve Y- connectors, double Y- connector hemostasis valves, one- handed hemostasis valves, and others. In 2024, the hemostasis valve Y- connectors segment dominated with the largest share due to their widespread use in various interventional procedures. These connectors offer dual-port access, allowing simultaneous insertion of devices while effectively maintaining hemostasis, making them essential in complex cardiovascular and radiology interventions. Their compatibility with different catheter sizes and high sealing efficiency make them a preferred choice among healthcare professionals. The Y-connector’s ease of use, reliability, and integration with other vascular access tools drives their adoption, thereby driving the segment growth.

The one- handed hemostasis valves segment is expected to experience significant growth during the forecast period due to its ergonomic design and ease of operation. These valves allow clinicians to maintain control with a single hand during device exchanges, improving procedural efficiency and reducing the risk of blood exposure. Their user-friendly nature makes them especially useful in fast-paced environments or emergency interventions. The demand for these advanced, intuitive valves is rising as healthcare providers prioritize workflow efficiency and operator safety, thereby driving the segment growth.

Application Analysis

The segmentation, based on application, includes angiography and angioplasty. The angioplasty segment is expected to experience significant growth during the forecast period, due to its rising global use in treating blocked or narrowed arteries. The procedure relies heavily on catheters and guidewires, making hemostasis valves essential to control bleeding during device manipulation. The volume of angioplasty procedures is growing rapidly as the incidence of coronary artery disease increases worldwide. This directly boosts the demand for reliable hemostasis valves that ensure safety and efficiency throughout the procedure, thereby driving the segment growth.

End Use Analysis

The segmentation, based on end use, includes hospitals, ambulatory surgical centers, and others. In 2024, the hospitals segment dominated with the largest share due to their role as primary centers for complex interventional procedures. Hospitals are equipped with advanced cath labs and interventional radiology units that routinely perform procedures requiring vascular access management. Hospitals have become the largest end users of hemostasis valves with rising patient admissions, growing adoption of minimally invasive treatments, and a preference for integrated procedure packs. Additionally, strong purchasing power and established supplier partnerships allow hospitals to maintain consistent usage, thereby driving the segment growth.

Source: Polaris Market Research Analysis

Regional Analysis

North America Hemostasis Valve Market Trend

The hemostasis valve market in North America dominated with the largest share in 2024, driven by a high volume of cardiovascular procedures, advanced healthcare infrastructure, and strong adoption of minimally invasive technologies. The region benefits from well-established hospitals, increased awareness of interventional care, and access to next-generation devices. Technological innovation and the presence of leading players further fuel product development and adoption. Favorable reimbursement policies and clinical training programs also support widespread use of hemostasis valves in both cardiology and radiology. The demand for reliable vascular access tools is growing as healthcare systems focus on efficiency and patient safety, thereby driving market expansion.

U.S. Hemostasis Valve Market Insight

The hemostasis valve market in the U.S. is expected to witness significant growth due to its high healthcare spending, advanced hospital systems, and large aging population affected by heart disease. A strong presence of key industry players and rapid integration of new technologies such as one-handed hemostasis valves contribute to its growth. The U.S. further experiences a high usage of angioplasty and catheter-based treatments, which rely heavily on hemostasis valves to manage bleeding and improve procedural outcomes. Ongoing investments in interventional care, combined with supportive regulatory frameworks and professional training, fuel the growth.

Asia Pacific Hemostasis Valve Market Analysis

The hemostasis valve market in Asia Pacific is projected to witness substantial growth due to increasing healthcare investments, rising cardiovascular disease cases, and expanding access to minimally invasive procedures. Countries such as China, India, Japan, and South Korea are modernizing healthcare systems, creating greater demand for advanced interventional tools. Hospitals in the region are adopting hemostasis valves more frequently with growing awareness about patient safety and cost-effective medical solutions. Additionally, the rise of local manufacturers offering affordable and compatible devices supports broader market penetration. The region’s rapid shift toward modern medical practices further fuels the growth.

China Hemostasis Valve Market Trends

The hemostasis valve market in China is expected to experience significant growth due to its large population, increasing rates of heart disease, and strong government focus on healthcare modernization. Urban hospitals are rapidly adopting interventional cardiology procedures, and the demand for vascular access management tools such as hemostasis valves is rising accordingly. Domestic medical device manufacturers are expanding their presence, offering competitively priced, locally produced valves. Additionally, increased training of interventional specialists and growing investments in hospital infrastructure are supporting the wider use of these devices, thereby driving the growth.

Europe Hemostasis Valve Market Insight

The hemostasis valve market in Europe is expected to experience rapid growth during the forecast period, driven by advanced healthcare systems, a strong focus on patient safety, and increasing adoption of minimally invasive procedures. Countries such as Germany, the UK, France, and the Netherlands have well-established interventional cardiology and radiology practices where hemostasis valves are essential. The region further benefits from favorable regulatory frameworks and growing investments in hospital infrastructure. Rising awareness of vascular access complications and the need for efficient blood control during procedures continues to drive demand. Moreover, European medical institutions are prioritizing integrated, high-performance devices, thereby driving growth.

Germany Hemostasis Valve Market Outlook

The market is expected to experience fastest growth in Europe due to its highly developed healthcare infrastructure and early adoption of innovative medical technologies. The country conducts a high volume of catheter-based procedures, especially in cardiology and neurology, where hemostasis valves are critical for ensuring safe and efficient vascular access. German hospitals and clinics favor precision-engineered, reliable equipment, which fuels demand for advanced valve designs such as Y-connectors and one-handed models. Additionally, strong public and private investments in healthcare, a focus on clinical training, and adherence to high regulatory standards further fuel the growth.

Source: Polaris Market Research Analysis

Key Players and Competitive Analysis

The industry is characterized by intense competition, driven by technological innovation, product differentiation, and global expansion strategies. Leading players such as Abbott, Boston Scientific Corporation, Terumo Corporation, and Merit Medical Systems dominate the market through extensive product portfolios, strong distribution networks, and ongoing R&D investments. B. Braun Melsungen AG, Teleflex Incorporated, and Nipro also hold significant market shares due to their well-established reputations and comprehensive interventional product offerings. Emerging players such as Antmed Corporation, Beijing Demax Medical Technology Co., and Lepu Medical Technology are rapidly gaining ground, particularly in Asia, by offering cost-effective and innovative valve solutions. Companies such as Argon Medical Devices, DeRoyal Industries, and Freudenberg Medical contribute niche products tailored for specific procedural needs. The market is witnessing trends toward miniaturization, improved sealing mechanisms, and integration with procedure kits, pushing manufacturers to enhance performance while meeting regulatory standards and user demand for efficiency and safety.

Key Players

- Abbott

- Antmed Corporation

- Argon Medical Devices

- B. Braun Melsungen AG

- Beijing Demax Medical Technology Co

- Boston Scientific Corporation

- DeRoyal Industries, Inc.

- Freudenberg Medical

- Lepu Medical Technology(Beijing)Co., Ltd.

- Merit Medical Systems

- Nipro

- SCW Medicath Ltd

- Teleflex Incorporated

- TERUMO CORPORATION

Industry Developments

In February 2025, Teleflex revealed that it had entered into a definitive agreement to acquire BIOTRONIK’s Vascular Intervention business for about EUR 760 million, expanding its presence within the interventional cardiology segment.

In October 2024, Boston Scientific presented clinical data for ACURATE neo2 at TCT 2024 and noted that ongoing discussions with the U.S. Food and Drug Administration are continuing to define the regulatory pathway.

In June 2023, SYNDEO Medical launched the Rover SA, a spring-actuated hemostasis valve supporting up to 9.5 French devices, enhancing interventional procedures with improved control, minimized blood loss, and compatibility. It became available standalone and within the SYNDEOPack.

Hemostasis Valve Market Segmentation

By Type Outlook (Revenue, USD Million, 2020–2034)

- Hemostasis Valve Y- Connectors

- Double Y- Connector Hemostasis Valves

- One- Handed Hemostasis Valves

- Others

By Application Outlook (Revenue, USD Million, 2020–2034)

- Angiography

- Angioplasty

By End Use Outlook (Revenue, USD Million, 2020–2034)

- Hospitals

- Ambulatory Surgical Centers

- Others

By Regional Outlook (Revenue, USD Million, 2020–2034)

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America

Hemostasis Valve Market Report Scope

| Report Attributes | Details |

| Market Size in 2024 | USD 188.46 Million |

| Market Size in 2025 | USD 199.66 Million |

| Revenue Forecast by 2034 | USD 339.88 Million |

| CAGR | 6.1% from 2025 to 2034 |

| Base Year | 2024 |

| Historical Data | 2020–2023 |

| Forecast Period | 2025–2034 |

| Quantitative Units | Revenue in USD Million and CAGR from 2025 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

FAQ's

The global market size was valued at USD 188.46 million in 2024 and is projected to grow to USD 339.88 million by 2034.

The global market is projected to register a CAGR of 6.1% during the forecast period.

North America dominated the market share in 2024.

A few of the key players in the market are Abbott; Antmed Corporation; Argon Medical Devices; B. Braun Melsungen AG; Beijing Demax Medical Technology Co.; Boston Scientific Corporation; DeRoyal Industries, Inc.; Freudenberg Medical; Lepu Medical Technology (Beijing) Co., Ltd.; Merit Medical Systems; Nipro; SCW Medicath Ltd.; Teleflex Incorporated; and TERUMO CORPORATION.

The hospital segment dominated the market share in 2024.

The angioplasty segment is expected to witness the significant growth during the forecast period.

Download Sample Report of Hemostasis Valve Market

Please fill out the form to request a customized copy of the research report.