Injection Molded Plastic Market Size, Growth Report, 2026-2034

REPORT DETAILS

REPORT DETAILS

ABOUT THIS REPORT

Injection Molded Plastic Market Summary

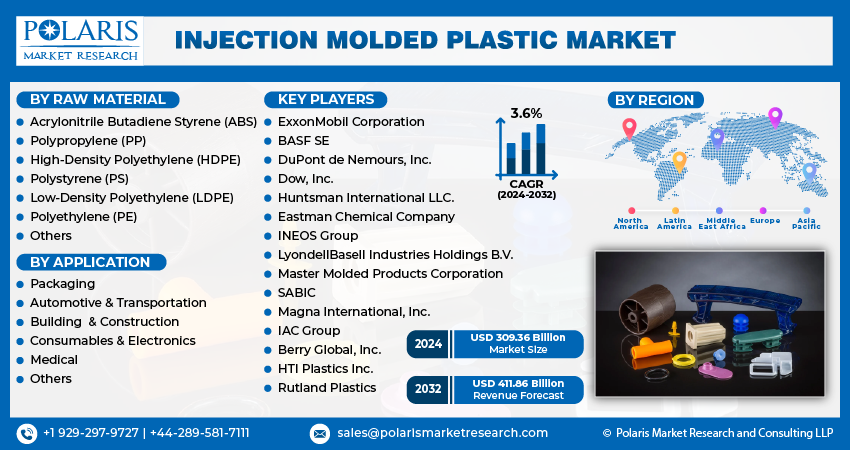

The injection molded plastic market size was valued at USD 349.47 billion in 2025 and is expected to register a CAGR of 3.0% from 2026 to 2034. The growing packaging industry globally propels the market growth. Further, the rising penetration of e-commerce platforms is expected to offer opportunities for the industry during the forecast period.

Market Statistics

Key Takeaways

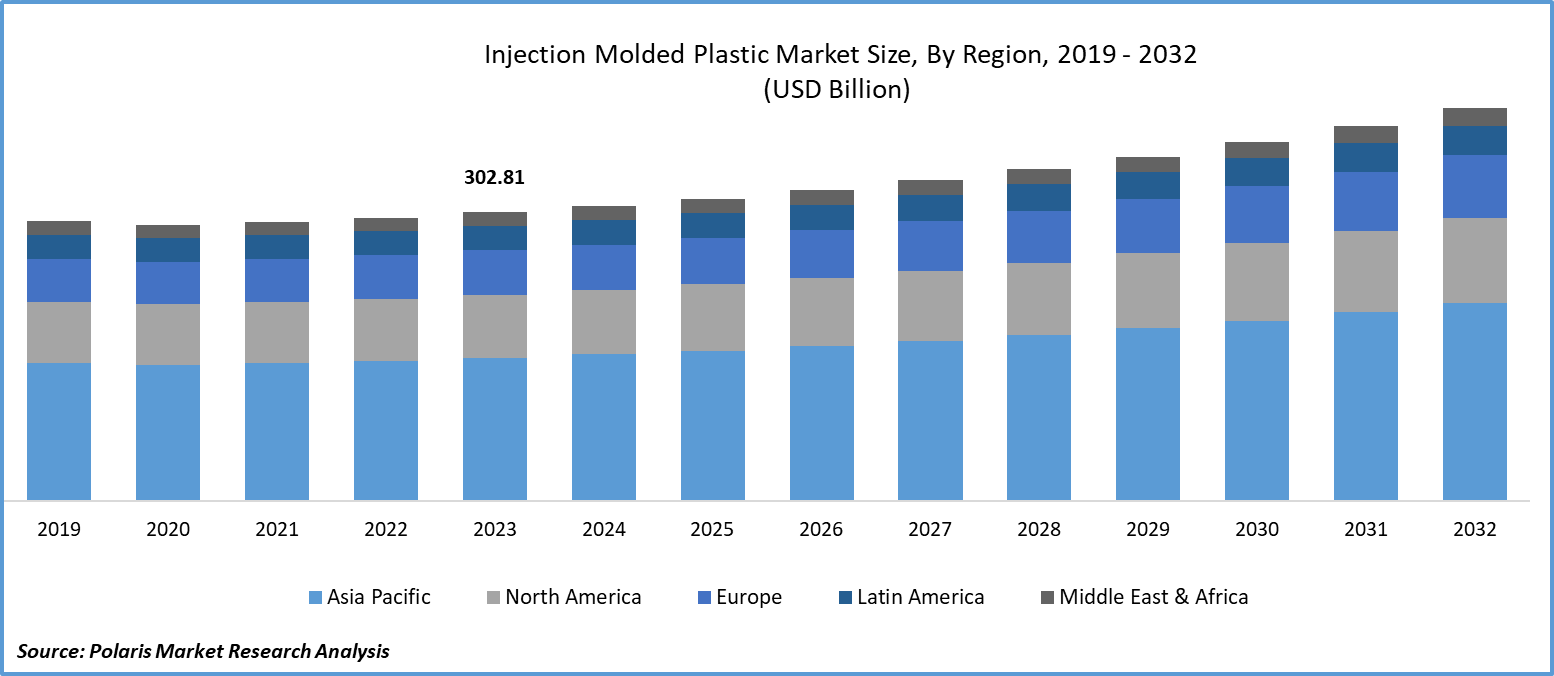

- In 2025, Asia Pacific accounted for the largest global revenue share of 34.98%. The Asia Pacific injection molded plastic market growth is attributed to robust manufacturing base, rising urbanization, and increasing consumer demand across key industries such as automotive, packaging, and electronics.

- The North America injection molded plastics market is expected to expand at a rapid pace with a CAGR of 2.70% in the coming years, owing to the technological advancements in precision injection molding and increasing adoption of high-performance polymers in the automotive and healthcare sectors.

- The polypropylene (PP) injection molding dominated the market with 23.96% share in 2025. Its cost-effectiveness and superior chemical resistance contributed to the segment dominance.

- Injection molded packaging dominated the revenue with 34.0% share in 2025. Rising demand for lightweight, durable, and cost-efficient packaging solutions across industries boosts the adoption of injection molded plastics across the segment.

- The acrylonitrile butadiene styrene (ABS) segment is expected to register a CAGR of 2.85% in 2026–2034. This is driven by increasing demand in automotive and electronics applications.

Industry Dynamics

- Surging popularity and adoption of electric vehicles (EVs) boost the demand for injection-molded plastics.

- Rising demand for molded plastics from various end-use industries such as packaging, construction, agriculture, and automotive drives the industry growth.

- Increasing use of 3D printing technology in commercial applications is expected to provide lucrative opportunities for the industry during the forecast period.

- Demand is increasingly shaped by precision injection molding and high-performance polymers for tighter tolerances, improved durability, and advanced functionality in medical and automotive lightweight components.

- Imposition of stringent rules and regulations on plastic use hinders the market expansion.

- Regulations are increasingly shifting from “plastic bans” to recyclability, recycled-content, and extended producer responsibility (EPR)-style compliance. It raises material qualification and documentation requirements, especially in packaging and consumer-facing applications. This factor boosts the demand for sustainable injection molded plastics.

- 3D printing is transforming this market through rapid prototyping and faster tooling iterations. It is accelerating time-to-market for injection molded plastic parts.

AI Impact on Injection Molded Plastic Market

- AI in injection molding helps monitor parameter adjustments in real time. Its adoption helps in ensuring consistent and high-quality output. The AI technology helps reduce defects, minimizes the requirement for costly rework, and enhances production efficiency.

- The technology enables predictive maintenance in injection molding. It is used to analyze data from sensors in equipment. Predicting possible equipment failures helps manufacturers schedule maintenance ahead of time. This reduces downtime and improves production schedules.

- The adoption of AI plays a key role in energy optimization. AI tools are used to reduce scrap and minimize machine downtime. This benefit contributes to achieving sustainability goals and results in significant cost savings.

- AI helps in defect reduction in injection molding. Practical AI use cases in plants include cycle-time optimization, defect detection, process window control, and scrap reduction. It supports smart manufacturing initiatives while improving consistency at scale.

What is Injection Molding Plastic?

Injection molded plastics is a manufacturing process. In the process, molten plastic is injected into molds to form specific shapes. It is largely used to produce complex and high-volume plastic parts with steady quality. This process supports mass production, reduces material waste, and is commonly applied across packaging, automotive, and electronics industries. The machine melts the plastic, injects it into the mold, cools it, and solidifies it into the final product. The injection molded plastic market is growing quickly because of lower labor costs, faster manufacturing, less waste, and better material flexibility. However, challenges such as increasing demand for bio-based polymers and concerns over environmental impact are hindering complete market expansion.

Plastic injection molding process is especially critical for high-volume manufacturing where repeatability and dimensional accuracy are required. However, tooling cost and design iterations can increase upfront investment and extend lead times for new programs. The transition toward bio-based and recycled plastics adds qualification complexity and may increase costs in applications that require strict performance and compliance validation.

The growing packaging industry propels the injection molded plastic market growth. Injection molded plastics offer strong protection for products. They improve shelf life and reduce damage during transport. The light weight of these plastics helps lower transportation costs. This makes them a cost-effective option for packaging companies. Further, innovation in plastic materials allows for the creation of sustainable and recyclable products. This fulfils the growing demand for biodegradable packaging. According to data from the Packaging Industry Association of India, the packaging sector in India was worth USD 50.5 billion in 2019. It is projected to reach USD 204.81 billion by 2025, with a CAGR of 26.7%. Injection molding is commonly used to make caps and closures, dispensers, rigid containers, and thin-wall packaging. It helps brands balance performance, speed, and cost and produce durable lightweight packaging. Therefore, the growing packaging industry globally is propelling the market revenue.

The demand for injection molded plastics is driven by the rising number of e-commerce platforms. E-commerce platforms prefer durable, lightweight, and affordable packaging materials. It helps them ship products safely and efficiently. Injection molded plastics offer the strength and precision needed for protective packaging components like trays, inserts, containers, and closures. These platforms also inspire new ideas in packaging design. It encourages businesses to develop custom, brand-specific packaging that improves customer experience. Injection molded plastics play a key role in this trend. It enables manufacturers to create complex shapes, textures, and colors with high accuracy. As a result, the growing number of e-commerce platforms drives the injection molded plastics market. Rising penetration of e-commerce propels the demand for standardized protective formats and high-throughput packaging components. It supports stable, repeatable injection molding programs at scale. This factor accelerates the demand for e-commerce protective packaging.

Material Classification Overview

| Category | Thermoplastics | Thermosets | Commodity Plastics | Engineering Plastics |

| Definition | Can be melted and remolded multiple times | Set permanently after heating, cannot be remolded | Low-cost, high-volume plastics | High-performance plastics with advanced properties |

| Structure | Linear or branched | Cross-linked | Simple polymer structure | Complex molecular structure |

| Processing | Easy, recyclable | Complex, non-recyclable | Easy processing | Requires controlled processing |

| Heat Resistance | Low to moderate | High | Low | High |

| Cost | Moderate | Moderate to High | Low | High |

| Applications | Packaging, consumer goods | Electrical, adhesives | Packaging, daily-use items | Automotive, electronics |

| Examples | PP, PE, ABS | Epoxy, phenolic | PE, PP, PS | ABS, polycarbonate, nylon |

Market Dynamics

Rising Adoption of Electric Vehicles Globally

EV manufacturers focus on reducing weight to increase battery efficiency and vehicle range. Injection molded plastics offer a great solution by replacing heavier metal parts without losing structural strength or performance. Automakers use these plastics in interior panels, housings, brackets, battery casings, and various under-the-hood parts to improve energy efficiency. EVs also need effective thermal management and electrical insulation, which injection molded plastics offer. These vehicles feature modern and sleek interiors. Customizable and attractive plastic parts made through injection molding help shape this interior. According to the International Energy Agency, electric car sales reached 3.5 million in 2023, surpassing 2022 figures. This marked a 35% increase from the previous year. As a result, the growing popularity of electric vehicles worldwide is driving the expansion of the injection molded plastic market.

Growing Urbanization Worldwide

The construction of residential and commercial buildings is increasing with the growing urbanization. The World Economic Forum reported that the global urban population is expected to grow by 2.5 billion by 2050. Injection molded plastics provide a flexible solution for many construction components, such as pipes, fittings, and insulation materials. Owing to their lightweight and corrosion-resistant properties, these plastics have become ideal for modern urban infrastructure that requires efficient and sustainable building solutions. Urbanization drives the need for healthcare facilities and services. Increased focus on infrastructure development raises the demand for injection molded plastics. Connected medical devices, disposables, and packaging solutions often use these plastics as they are biocompatible, sterile, and made with precision. Also, urbanization drives the need for consumer goods and appliances, which rely heavily on injection molded plastic parts. Thus, the growing urbanization worldwide is driving the market expansion.

Segment Insights

Market Evaluation by Raw Material

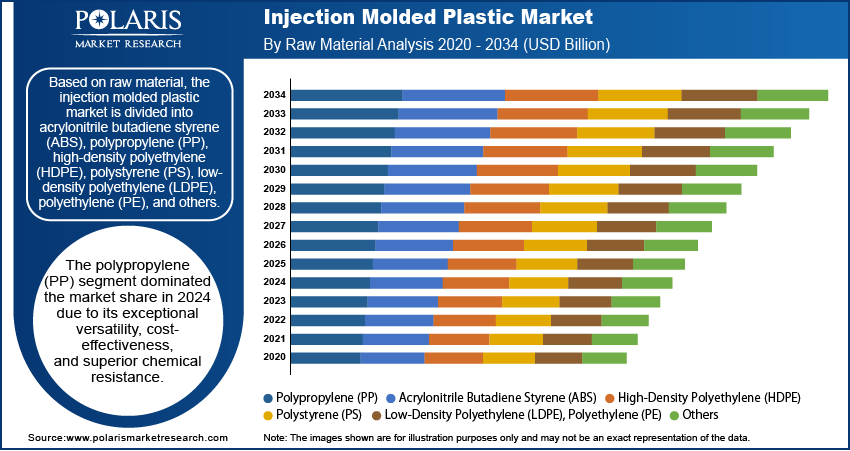

Based on raw material, the market is divided into acrylonitrile butadiene styrene (ABS), polypropylene (PP), high-density polyethylene (HDPE), polystyrene (PS), low-density polyethylene (LDPE), polyethylene (PE), and others. The polypropylene (PP) segment had the largest revenue share of 23.96% in 2025. Its versatility, low cost, and strong resistance to chemicals drive the demand for polypropylene injection molding. It is lightweight and has high impact strength. This is why PP injection molding is gaining popularity in the automotive, consumer goods, and packaging industries. This feature improved fuel efficiency in vehicles and lowered transportation costs in logistics. Its easy processing and recyclability also matched the growing demand for sustainable and affordable plastic solutions. These benefits made it the top choice for many applications. Material selection focuses more on performance and cost. PP remains a preferred choice for high-volume packaging and consumer applications. ABS demand rises where surface finish, rigidity, and dimensional stability are critical (notably electronics housings and automotive interiors).

The acrylonitrile butadiene styrene (ABS) segment is expected to grow at a robust pace with a CAGR of 2.85% in the coming years, owing to its rising adoption in the automotive and electronics sectors. ABS injection molding combines strength, rigidity, and aesthetic appeal, making it ideal for interior car components, dashboards, and consumer electronic housings. Furthermore, the rapid expansion of the electric vehicle fuels the segment dominance. Also, increased consumer demand for high-performance electronics boosts the dominance. These factors also have amplified the need for materials that offer superior dimensional stability and heat resistance, qualities inherent in ABS. These trends position ABS as a key raw material segment.

Market Insight by Application

In terms of application, the market is divided into packaging, automotive and transportation, building and construction, consumables and electronics, medical injection molded plastics, and others. The packaging segment led the market with 34.0% share in 2025 because of the growing demand for lightweight, durable, and affordable packaging solutions across various industries. Food and beverage companies, in particular, increasingly depend on plastic packaging. The packaging ensures product safety, extend shelf life, and lower transportation costs. The growing e-commerce sector drives the need for packaging that is strong yet uses less material. In addition, new developments in sustainable, recyclable plastics provide packaging manufacturers with lucrative opportunities to satisfy increasing consumer and regulatory demands for eco-friendly solutions. This factor is strengthening the segment’s dominance.

Regional Outlook

By region, the injection molded plastic market report provides insight into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. Asia Pacific accounted for the largest market share of 34.98% in 2025. Its robust manufacturing base and rising urbanization drive the dominance. Increasing consumer demand in key industries such as automotive, packaging, and electronics is driving growth in the regional market. China leads the market. Its extensive industrial infrastructure and low production costs drive the China's market growth. Also, high domestic consumption fuels the expansion. The Chinese government has invested in expanding manufacturing capacity. It also promotes industrial automation. This factor further boosts growth. Additionally, rapid economic development in India and Southeast Asia contributed to a surge in demand for affordable, high-performance plastic components. It is consolidating Asia Pacific injection molded plastic market growth. A dense ecosystem of tooling suppliers, contract manufacturers, and electronics production improves speed and cost competitiveness for injection molded plastic parts.

The North America injection molded plastic market is expected to grow quickly with a CAGR of 2.70% in the coming years. This growth is attributed to advances in precision molding technology and an increasing use of high-performance polymers in the automotive and healthcare industries. Rising investments in sustainable material development propel the growth. Companies in the U.S. continually test the boundaries of lightweight vehicle design and medical device development. This need creates a demand for complex, durable plastic parts. Strict environmental rules are driving the shift toward recyclable and bio-based materials. This supports the increasing sustainability goals of consumers and industries. Meeting medical-grade production standards, using automation, and improving recycled resin help achieve compliance and sustainability goals. These factors make North America an important player in the market.

Key Players and Competitive Analysis

The injection molded plastic market is highly competitive. Key players pursue mergers and acquisitions (M&A), collaborations, and strategic partnerships. Such strategies improve their product offerings and expand market reach. Major injection molded plastic manufacturers have actively sought mergers and acquisitions to strengthen their positions. Partnerships between industry leaders and research institutions also influence the market. Strategic partnerships are further driving innovation and commercialization. To expand and survive in a competitive and rising market climate, the injection molded plastic industry must offer cost-effective products. Competitive positioning varies across the value chain. Resin producers and compounders influence material availability and pricing. Converters and molders compete on quality systems, automation, cycle-time efficiency, and sustainable resin portfolios [post-consumer recycled (PCR)/PIR].

The market is fragmented, with the presence of numerous global and regional market players. A few major players in the market are ALPLA; AptarGroup, Inc.; BASF SE; Berry Global, Inc.; Dow, Inc.; DuPont de Nemours, Inc.; Eastman Chemical Company; ExxonMobil Corporation; Heppner Molds; HTI Plastics Inc.; Huntsman International LLC.; IAC Group; INEOS Group; LACKS ENTERPRISES, INC.; LyondellBasell Industries Holdings B.V.; Magna International, Inc.; Master Molded Products Corporation; Rutland Plastics; SABIC; and The Rodon Group.

List of Key Companies

- ALPLA

- AptarGroup, Inc.

- BASF SE

- Berry Global, Inc.

- Dow, Inc.

- DuPont de Nemours, Inc.

- Eastman Chemical Company

- ExxonMobil Corporation

- Heppner Molds

- HTI Plastics Inc.

- Huntsman International LLC.

- IAC Group

- INEOS Group

- LACKS ENTERPRISES, INC.

- LyondellBasell Industries Holdings B.V.

- Magna International, Inc.

- Master Molded Products Corporation

- Rutland Plastics

- SABIC

- The Rodon Group

Injection Molded Plastic Industry Developments

- January 2026: ENGEL unveiled a 1,000 kN fully electric machine at Plastindia 2026 for medical and packaging, and its compact victory 50 machine for high-precision, small-part production. (Source: engelglobal.com)

- January 2026: BASF introduced Ultramid TG3, a high-performance polyamide grade for automotive use. It supports sustainability while maintaining strong mechanical performance and durability. (Source: basf.com)

- May 2024: ALPLA, a global leader in the development and production of plastic packaging solutions, announced that it had strengthened its injection molding business with the new ALPLAinject division. (Source: alpla.com)

- February 2024: Kreate acquired an injection-molded plastics supplier in Georgetown, TX, a move expected to boost its production capacity and strengthen its logistics network. (Source: businesswire.com)

Injection Molded Plastic Market Segmentation

By Raw Material Outlook (Revenue, USD Billion, 2021–2034)

- Acrylonitrile Butadiene Styrene (ABS)

- Polypropylene (PP)

- High-Density Polyethylene (HDPE)

- Polystyrene (PS)

- Low-Density Polyethylene (LDPE)

- Polyethylene (PE)

- Others

By Application Outlook (Revenue, USD Billion, 2021–2034)

- Packaging

- Automotive & Transportation

- Building & Construction

- Consumables & Electronics

- Medical

- Others

By Regional Outlook (Revenue, USD Billion, 2021–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Future Outlook

Market will move more toward sustainable plastics with higher use of recycled and bio-based materials. Recycling and circular economy focus will increase in coming years. Automation and AI will improve production efficiency and reduce waste. Demand for lightweight plastics will rise in automotive and packaging, helping market growth.

Injection Molded Plastic Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 349.47 billion |

| Market Size in 2026 | USD 360.73 billion |

| Revenue Forecast in 2034 | USD 471.35 billion |

| CAGR | 3.0% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD billion, 2021–2034 and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

The global market size was valued at USD 349.47 billion in 2025 and is projected to grow to USD 471.35 billion by 2034.

The global market is projected to register a CAGR of 3.0% during the forecast period.

Asia Pacific holds the largest share of the global market. It is led by China, India, Japan, and South Korea. Manufacturing expansion and e-commerce penetration fuel the regional market growth. Also, the automotive industry growth boosts growth.

The packaging segment dominated the revenue share in 2025. The segment dominance is attributed to rising demand for lightweight, durable, and cost-efficient packaging solutions across industries.

A few of the key players in the market are ALPLA; AptarGroup, Inc.; BASF SE; Berry Global, Inc.; Dow, Inc.; DuPont de Nemours, Inc.; Eastman Chemical Company; ExxonMobil Corporation; Heppner Molds; HTI Plastics Inc.; Huntsman International LLC.; IAC Group; INEOS Group; LACKS ENTERPRISES, INC.; LyondellBasell Industries Holdings B.V.; Magna International, Inc.; Master Molded Products Corporation; Rutland Plastics; SABIC; and The Rodon Group.

Common materials include polypropylene (PP), polyethylene (PE), ABS, polystyrene (PS), and nylon.

Used in packaging, automotive parts, electronics, medical devices, and consumer goods.

High production efficiency, low waste, repeatability, and ability to produce complex shapes.

Download Sample Report of Injection Molded Plastic Market

Please fill out the form to request a customized copy of the research report.