Japan Printing Inks Market Demand, Growth Opportunity, 2025-2034

REPORT DETAILS

Market Statistics

Overview

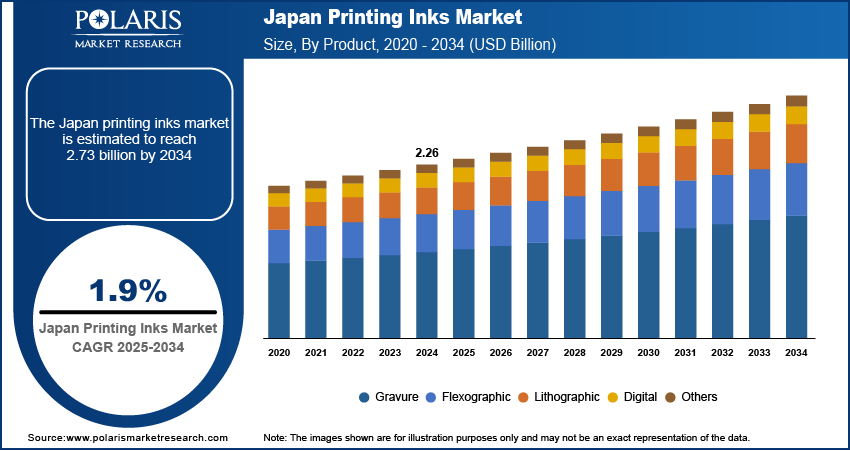

The Japan printing inks market size was valued at USD 2.26 billion in 2024, growing at a CAGR of 1.9% from 2025 to 2034. Growing environmental awareness among consumers is prompting packaging converters to adopt eco-friendly inks, such as water-based and soy-based formulations. This shift is driving increased demand for sustainable printing inks in various packaging applications across the market.

Key Insights

- The lithographic segment held ~42% of the market share in 2024, driven by its extensive use in high-volume commercial and publishing applications.

- The publication & commercial printing segment is projected to register the highest CAGR from 2025 to 2034. The growth is fueled by growing demand for premium print materials and branded business collateral.

Industry Dynamics

- High demand for precision printing in electronics, semiconductors, and industrial applications drives the adoption of advanced functional and conductive inks.

- Strong focus on automation and smart manufacturing boosts integration of high-performance inks in labels, packaging, and product identification.

- Expansion of inkjet and digital printing in industrial settings supports efficient, low-waste production with real-time variable data printing.

- Aging workforce and declining domestic print volume limit market expansion despite technological leadership in specialty ink development.

Market Statistics

- 2024 Market Size: USD 2.26 billion

- 2034 Projected Market Size: USD 2.73 billion

- CAGR (2025–2034): 1.9%

Source: Polaris Market Research Analysis

AI Impact on Japan Printing Inks Market

- AI enhances performance optimization in Japan’s printing inks market by analyzing detailed print parameters, substrate compatibility, and environmental factors to ensure precise and high-quality output tailored to local industry standards.

- Integration of AI enables adaptive ink formulation, automatically adjusting viscosity, pigment dispersion, and drying characteristics in response to varying job requirements, seasonal humidity, and equipment configurations.

- AI-powered monitoring systems support early detection of formulation inconsistencies, ink system blockages, or thermal deviations, facilitating predictive maintenance and reducing operational downtime in Japan’s precision-driven printing sector.

- AI improves operator efficiency by enabling smart automation of ink adjustments, real-time defect detection, and process feedback, enhancing accuracy, reducing material waste, and supporting the high-efficiency production demands of Japan’s commercial and industrial printing environments.

The printing inks market comprises the production and supply of colored fluids used in printing applications across packaging, publishing, commercial, and industrial sectors. These inks, based on various formulations such as solvent-based, water-based, and UV-curable, are essential for delivering text, images, and graphics onto diverse substrates such as paper, plastics, and metals. The expansion of digital printing in commercial and industrial applications is accelerating ink consumption, particularly in short-run and customized jobs. Enhanced print quality, fast turnaround times, and reduced waste are boosting digital ink adoption across printing operations.

Increasing online shopping activities are driving the need for high-quality printed packaging and labels. This surge in e-commerce is supporting the consumption of printing inks for corrugated boxes, flexible packaging, and branded labeling solutions. Moreover, advancements in UV-curable inks are creating new opportunities for high-speed printing and specialty applications. These inks offer fast curing, durability, and low emissions, making them attractive for a variety of commercial and industrial print jobs.

Drivers & Opportunities

Increased Demand in Industrial Printing: Increased demand in industrial printing is creating a strong growth avenue for the Japan printing inks market. According to Japan’s Ministry of Economy, Trade and Industry (METI), in April 2024, industrial printing applications, including electronics, semiconductors, and functional materials, reported a 12.5% year-on-year increase in ink demand. The high demand is driven by growth in printed electronics and smart manufacturing. Industries such as electronics, textiles, and automotive are integrating advanced printing applications into their manufacturing processes. Printed electronics, including conductive inks, are enabling the development of flexible circuits, sensors, and display components. In textile manufacturing, specialized inks are being used for digital fabric printing to support mass customization and fast fashion trends. Automotive interiors and parts are also utilizing decorative and functional inks for enhanced aesthetics and component identification. These industrial sectors require high-performance inks that deliver durability, precision, and application-specific properties, which is boosting innovation in ink formulations and driving steady demand.

Shift Toward Low-VOC and Water-Based Inks: Shift toward low-VOC and water-based inks is accelerating due to rising environmental regulations and heightened focus on sustainable manufacturing practices. Regulatory pressure from environmental agencies and consumer demand for eco-friendly products are pushing manufacturers to reformulate inks with fewer volatile organic compounds. Water-based inks offer reduced emissions, safer handling, and easier cleanup without compromising print quality or compatibility across substrates. Printing firms are investing in new press technologies that support these ink systems, aligning production processes with green standards.

Source: Polaris Market Research Analysis

Segmental Insights

Product Analysis

Based on product, the Japan printing inks market segmentation includes gravure, flexographic, lithographic, digital, and others. The lithographic segment accounted for the largest revenue share of ~42% in 2024 due to its widespread use in high-volume commercial printing. This method allows sharp image reproduction and consistent print quality at lower costs per unit, especially for longer runs. Consumer goods manufacturers, publishing houses, and advertising agencies continue to rely on lithography for brochures, magazines, posters, and packaging inserts. The ability to handle diverse substrates and the maturity of the technology make it an efficient solution. Strong domestic demand for high-quality printed materials sustains its dominance over other printing processes.

Application Analysis

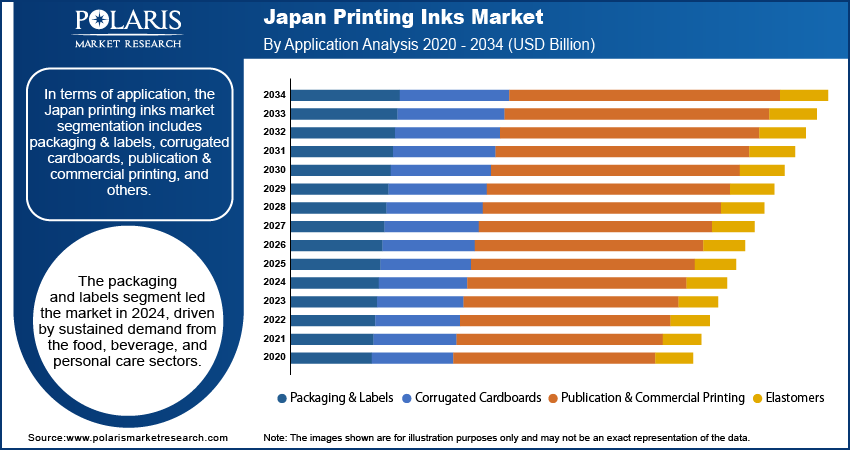

In terms of application, the Japan printing inks market segmentation includes packaging & labels, corrugated cardboards, publication & commercial printing, and others. The publication & commercial printing segment is expected to register the highest CAGR from 2025 to 2034. The growth is attributed to a renewed focus on premium-quality print media and business collateral. High-end publishing, art books, educational content, and professional marketing materials are witnessing stable demand despite digital alternatives. Businesses value printed materials for their tangible engagement and branding impact. Government campaigns and local content publishing are also contributing to print volume growth. Investments in offset and digital presses optimized for this segment are rising. Ink manufacturers benefit from consistent requirements for color accuracy, fast drying, and substrate versatility, supporting the expansion of commercial and publication printing services.

Source: Polaris Market Research Analysis

Key Players & Competitive Analysis

The competitive landscape of the Japan printing inks market is shaped by a combination of strategic alliances, market expansion strategies, and technology advancements. Industry players are focusing on developing sustainable ink formulations to align with shifting regulatory and environmental demands. Companies are increasingly engaging in joint ventures and mergers and acquisitions to strengthen their domestic manufacturing and R&D capabilities. Post-merger integration has become a crucial area of focus, particularly to streamline operations, unify supply chains, and consolidate product portfolios.

Market participants are investing in technology advancements to offer inks compatible with advanced printing equipment and specialized substrates, particularly for applications in electronics and packaging. Strategic alliances between ink producers and end-user industries are also contributing to product innovation and customized solutions. These collaborative efforts are enhancing competitiveness and enabling quicker market response times. The market is witnessing intensifying competition, driven by rapid innovation cycles and evolving customer expectations in both quality and environmental compliance.

Key Players

- Ashland Inc.

- DIC Corporation

- DuPont

- Flint Group

- Huber Group

- Royal Dutch Printing Ink Factories Van Son

- Siegwerk Druckfarben AG & Co. KGaA

- Sun Chemical

- TOKYO PRINTING INK MFG Co. Ltd

- Zeller+Gmelin GmbH & Co. KG

Japan Printing Inks Industry Developments

September 2024: DuPont launched Advanced Artistri Digital Printing Ink Technology at PRINTING United 2024.

Japan Printing Inks Market Segmentation

By Product Outlook (Revenue, USD Billion, 2020–2034)

- Gravure

- Flexographic

- Lithographic

- Digital

- Others

By Resin Outlook (Revenue, USD Billion, 2020–2034)

- Modified Rosin

- Modified Cellulose

- Acrylic

- Polyurethane

- Others

By Application Outlook (Revenue, USD Billion, 2020–2034)

- Packaging & Labels

- Corrugated Cardboards

- Publication & Commercial Printing

- Others

Japan Printing Inks Market Report Scope

| Report Attributes | Details |

| Market Size in 2024 | USD 2.26 billion |

| Market Size in 2025 | USD 2.30 billion |

| Revenue Forecast by 2034 | USD 2.73 billion |

| CAGR | 1.9% from 2025 to 2034 |

| Base Year | 2024 |

| Historical Data | 2020–2023 |

| Forecast Period | 2025–2034 |

| Quantitative Units | Revenue in USD billion and CAGR from 2025 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

FAQ's

The Japan market size was valued at USD 2.26 billion in 2024 and is projected to grow to USD 2.73 billion by 2034.

The Japan market is projected to register a CAGR of 1.9% during the forecast period.

A few of the key players in the market are Ashland Inc., DIC Corporation, DuPont, Flint Group, Huber Group, Royal Dutch Printing Ink Factories Van Son, Siegwerk Druckfarben AG & Co. KGaA, Sun Chemical, TOKYO PRINTING INK MFG Co. Ltd, and Zeller+Gmelin GmbH & Co. KG.

The lithographic segment accounted for the largest revenue share of ~42% in 2024 due to its widespread use in high-volume commercial printing.

The publication & commercial printing segment is expected to register the highest CAGR from 2025 to 2034, due to a renewed focus on premium-quality print media and business collateral.

Download Sample Report of Japan Printing Inks Market

Please fill out the form to request a customized copy of the research report.