Lead Acid Battery Recycling Market Business Growth, Development Factors, 2026-2034

REPORT DETAILS

What is the lead-acid battery recycling market size in 2025?

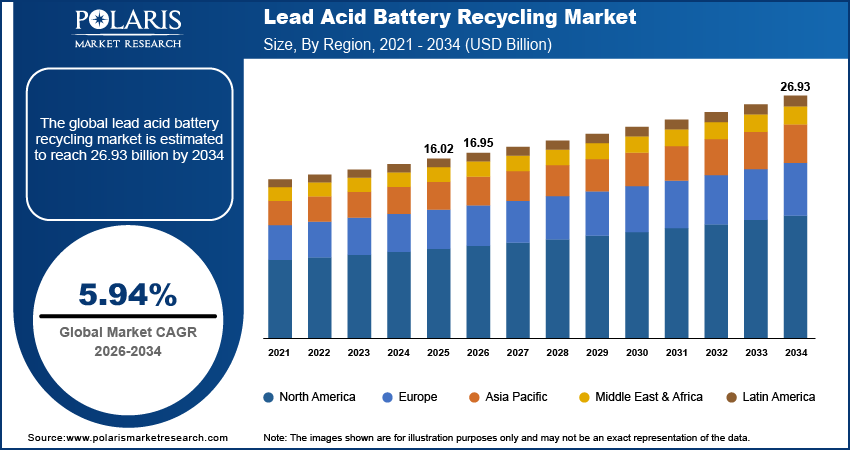

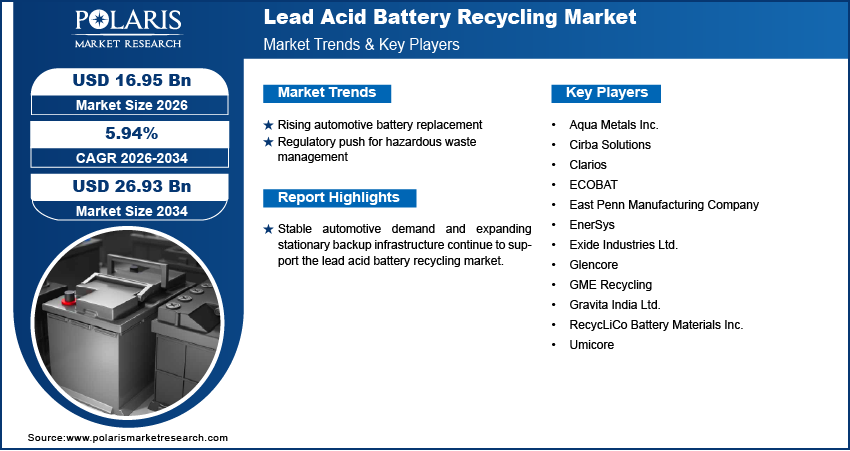

The global lead-acid battery recycling market is estimated around USD 16.02 billion in 2025,?with consistent growth anticipated during 2026–2034. Driven by rising battery replacement rates and stricter waste regulations worldwide. The market is projected to grow at a CAGR of 5.94% during the forecast period.

Market Statistics

Key Takeaways

-

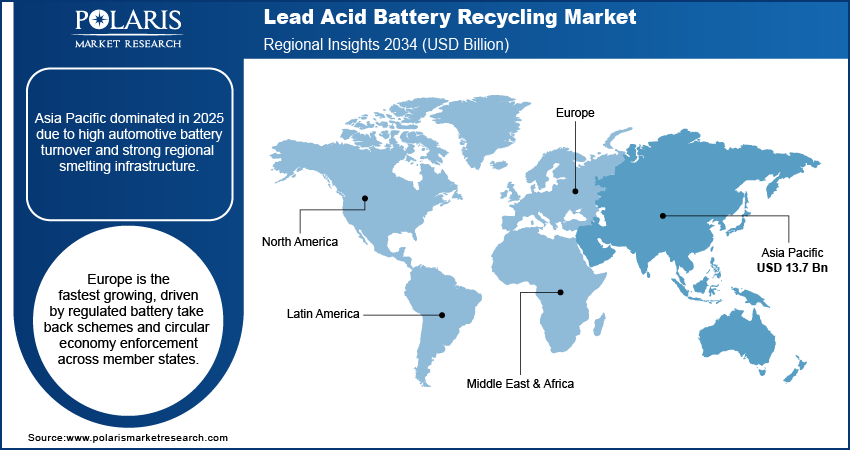

Asia Pacific dominated in 2025 with a 41.8% share, supported by strong vehicle production, industrial expansion, telecom growth, and established secondary lead smelting capacity ensuring regional supply stability.

-

Europe is projected to grow at a CAGR of 6.3%, driven by strict battery take-back regulations, circular economy initiatives, a strong automotive manufacturing base, and advanced waste management compliance frameworks.

-

North America held around a 27.3% share in 2025, supported by high vehicle ownership, structured collection systems, deposit return mechanisms, and stringent environmental regulations strengthening recycling infrastructure.

-

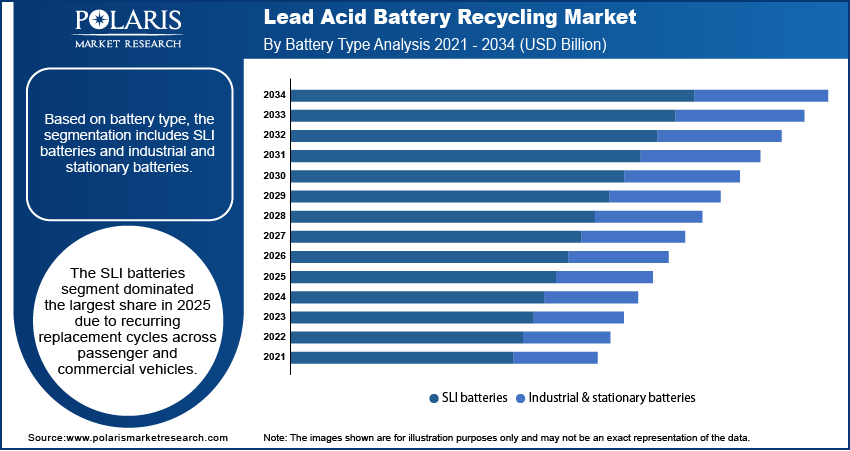

By battery type, SLI batteries accounted for nearly a 64.5% share in 2025, driven by frequent starter battery replacements across passenger and commercial vehicles, ensuring continuous scrap generation and stable recycling volumes globally.

-

By recycling process, pyrometallurgical processes held around a 71.2% share in 2025, supported by established smelting infrastructure, high-volume processing capability, and cost-efficient bulk scrap handling across major recycling hubs.

-

By recycling processes, hydrometallurgical processes are growing at a CAGR of 6.5%, driven by lower emission intensity, controlled chemical extraction methods, and increasing environmental compliance encouraging adoption of cleaner recycling technologies.

-

By end user, automotive remained the leading end user with a 68.7% share in 2025, supported by structured collection networks, regular battery replacement cycles, and strong aftermarket demand ensuring consistent feedstock supply.

Industry Dynamics

- Rising automotive battery replacement cycles support steady scrap generation and stable secondary lead output.

- Stricter battery recycling environmental regulations strengthen formal collection and licensed processing systems.

- High compliance and emission control costs create margin pressure across recycling operations.

- Formalization of recycling ecosystems and expansion of stationary energy storage create long-term growth opportunities.

Why Lead-Acid Battery Recycling Matters in the Circular Economy

Lead acid battery recycling refers to the structured collection and reprocessing of used lead acid batteries to recover lead, plastic, and electrolyte for reuse. In this system, batteries are broken in controlled units where lead grids and paste are separated and refined. Plastic casings are cleaned and converted into pellets for new battery manufacturing. This closed-loop system establishes the lead acid battery recycling process, which has a high rate of recovery above 95 percent. This recycling process helps in the recycling of batteries in the circular economy.

The lead acid battery recycling process is governed by tough environmental and hazardous waste laws due to its risk associated with lead poisoning. For instance, in August 2024, the Government of UK announced that waste lead-acid batteries containing POPs are to be classified as hazardous waste and can only be sent to authorized treatment facilities for destruction. In addition, the governments in the U.S., Europe, and some Asian countries enforce collection rates and recycling facilities. The standards of compliance include the control of emissions, occupational health and safety, and the safe neutralization of acid. ESG analysis is now a key consideration in the global lead acid battery recycling industry, as formal recycling minimizes the reliance on primary lead mining.

Source: Polaris Market Research Analysis

In addition, the lead acid battery recycling industry is still a structured market owing to its consistent generation of scrap materials from the replacement of lead acid batteries in the automotive and industrial sectors. The lead acid battery recycling industry is also supported by the predictable availability of feedstock and the established smelting capacity. The secondary lead supply also helps to stabilize the price of raw materials for battery producers. Unlike other battery types, the lead-acid battery recycling industry is already a mature market.

Key Growth Drivers

Rising automotive battery replacement: The increasing number of vehicles on the road and the average age of vehicles are driving the replacement of batteries in passenger and commercial vehicles. The Battery Council International statistics indicated that the battery replacement industry represents 77% of the SLI battery market, ensuring sustained demand from existing ICE vehicles. The consistent generation of scrap materials remains one of the major driving forces behind the lead acid battery recycling market. Automotive starter batteries have a limited life span, ensuring consistent generation of collection volumes on an annual basis.

Regulatory push for hazardous waste management: The danger of lead and sulfuric acid waste management has resulted in the imposition of more stringent recycling policies for lead batteries in the leading economies of the world. The government ensures the implementation of appropriate waste management channels to prevent lead from contaminating the soil and groundwater. The need to comply with these regulations is a major driver of the lead acid battery recycling market.

Restraints & Challenges

Environmental compliance costs: The high costs of environmental monitoring and emission control are significant factors that restrict the lead acid battery recycling market. Lead acid battery recycling units have to invest in air filtration systems, wastewater treatment plants, and employee safety equipment to comply with regulations. Regular auditing and reporting requirements further increase costs. Such pressures impact the bottom line of the lead acid battery recycling market, especially for smaller and medium-scale recycling units.

Market Opportunities

Formalization of recycling ecosystems: An increasing shift from informal scrap handling to licensed recycling facilities creates clear lead acid battery recycling market opportunities. Emerging countries governments are enhancing their collection networks and tracing mechanisms. This transition improves material recovery efficiency and supports organized secondary lead production. Formal ecosystems also attract institutional investments in the lead acid battery recycling industry.

Rise in stationary energy storage: The rising adoption of backup power systems and grid support services is leading to an increase in the number of lead acid batteries in use. Telecom towers, data centers, and industrial facilities remain reliant on this technology. Growth in these installations creates future scrap volumes, supporting secondary lead production. Battery Council International stated that the global BESS market is projected to more than double by 2030, with installed capacity rising from 200 GWh to 1,200 GWh, supported by rising power demand as a single hyperscale data center may require up to 1 GW of electricity. This trend opens long-term lead-acid battery recycling market opportunities tied to stationary energy infrastructure.

Lead Acid Battery Recycling Process, Technology & Value Chain

The lead acid battery recycling process begins with the collection of the batteries from the automotive, industrial, and telecom sectors. The batteries are then transported to the recycling centers to ensure that they are recycled properly.

The batteries are then disassembled in a controlled environment where the lead paste, grids, plastics, and electrolytes are removed. This process of mechanical separation helps to ensure a constant feed of lead for recycling from batteries.

The separated lead fractions are then subjected to high-temperature smelting and refining to obtain battery-grade lead. This step is the heart of the secondary lead recycling process and ensures that the lead is supplied to the manufacturers.

The polypropylene is washed and reprocessed into pellets, which can be used to make new casings, while the electrolyte is purified or neutralized for use in industry. This marks the end of the lead acid battery recycling process.

Recycling Technologies Used

Pyrometallurgical battery recycling leads in the recycling of lead from batteries. The process requires the use of high-temperature smelting furnaces to separate the lead from other materials. The process is suitable for large-scale processing. Emission control systems are critical to manage air pollutants generated during combustion.

Hydrometallurgical lead acid battery recycling requires the use of aqueous chemical solutions to extract lead compounds at low temperatures. This method is environmentally friendly since it does not emit air pollutants. Although not widely practiced on a large scale, it is slowly gaining popularity due to controlled processing and environmental concerns.

Value Chain Analysis

Collection channels represent the first stage of the value chain and consist of retailers, automotive service centers, bulk consumers, and scrap aggregators. Closed-loop schemes and buy-back options enhance recycling rates. Efficient logistics ensure steady input for recycling facilities.

The capital outlay on furnaces, filtration systems, and waste treatment systems is a measure of operating capacity. Environmental regulations have a direct effect on the continuity of operations. Adherence to environmental regulations has a direct effect on the continuity of operations.

Secondary lead buyers mainly include battery manufacturers who use refined lead to produce new grids and paste material. The stable demand from the above manufacturers is supportive of the economics of the secondary lead production process. The integration between recyclers and battery producers strengthens circular material flows.

Recovered Materials & Applications

| Recovered Material | Recovery Stage | Application |

| Refined Lead | Smelting & Refining | New battery grids and lead paste |

| Lead Alloys | Refining | Industrial battery components |

| Polypropylene Plastic | Plastic Recovery | Battery casings and containers |

| Sodium Sulfate (from electrolyte) | Electrolyte Treatment | Detergent and glass manufacturing |

| Purified Sulfuric Acid | Electrolyte Treatment | Industrial acid reuse |

Source: Polaris Market Research Analysis

Source: Polaris Market Research Analysis

Segmental Insights

This report offers detailed coverage of the lead acid battery recycling market by battery type, by recycling process and end user to help readers identify the fastest expanding and most attractive demand segments.

By Battery Type

-

SLI batteries

SLI batteries represented the highest share in 2025 in the automotive lead acid battery recycling market, driven by regular starter battery replacement in passenger and commercial transportation. According to EUROBAT, the global 12V SLI battery market exceeds 300 GWh in 2024 and is projected to grow at 1–2% annually to surpass 340 GWh by 2030. High vehicle parc ensures continuous scrap generation. Organized dealer networks support efficient returns. This structure sustains volume stability across the forecast period.

-

Industrial & stationary batteries

Industrial and stationary batteries are expanding steadily within the industrial battery recycling market. The growth of backup power systems and infrastructure projects leads to an increase in installed capacity. The larger battery units lead to an increase in the amount of recoverable lead per cycle.

By Recycling Process

-

Pyrometallurgical

Pyrometallurgical represented the largest share in lead acid battery recycling in 2025. Well-established smelting capacity enables the processing of mixed battery scrap in bulk. High processing capacity supports cost-effective operations in bulk. Well-established infrastructure sustains its leading position in the market.

-

Hydrometallurgical

Hydrometallurgical processes are experiencing a gradual adoption rate in the recycling of lead acid batteries by process because of the lower emission intensity. Chemical extraction processes enable a controlled lead extraction process under controlled environments. Environmental compliance requirements support technology evaluation. Process optimization improves operational feasibility over time.

End User

-

Automotive

Automotive accounted for the maximum share in lead acid battery recycling by application in 2025. Continuous battery replacement cycles generate steady scrap volumes. Lead acid battery recycling for the automotive sector has a structured collection system through service centers and distributors. The aftermarket demand provides a guaranteed supply of feedstock.

-

Telecom

Telecom shows steady growth within lead acid battery recycling by application due to expansion of communication towers and rural connectivity networks. Backup power dependence increases battery installations at base stations. Growing installed base strengthens stationary battery recycling volumes. Infrastructure expansion supports sustained recovery growth.

Source: Polaris Market Research Analysis

Regional Insights & Dominant Markets

Asia Pacific Market Assessment

Asia Pacific lead acid battery recycling market dominated in 2025, driven by high vehicle production and replacement demand across China, India, Japan, South Korea, and ASEAN countries. Based on the ASEAN Automotive Federation statistics, the production of motor vehicles in ASEAN has grown from 2.99 million units in 2011 to 3.75 million units in 2024, registering a growth of about 25.5%. Moreover, expanding industrial activity and telecom infrastructure further increase stationary battery disposal volumes. Additionalaly, well established smelting capacity and secondary lead production facilities strengthen regional supply stability.

Europe Lead Acid Battery Recycling Market Insights

Europe lead acid battery recycling market shows highest growth due to regulated battery take-back schemes and circular economy policies. European Commission said that the EU aims to increase its circularity rate from about 12% to 24% by 2030. The automotive manufacturing sector in Germany, France, and Central Europe provides a constant source of scrap materials. The backup power sector for industry and telecom infrastructure also contributes to the recycling of stationary batteries. The strict regulations on waste management practices ensure a high recycling rate and proper processing of the material in all member countries.

North America Lead Acid Battery Recycling Market Overview

North America held the second largest share in lead acid battery recycling market, owing to its structured collection systems and strict environmental compliance norms. The U.S. maintains high vehicle ownership rates, which sustain recurring starter battery replacements. The U.S. Census Bureau data shows that 91.5% of U.S. households owned at least one vehicle in 2024, up from 90.9% in 2015. Formal recycling channels and deposit return systems improve recovery efficiency. Strong regulatory enforcement supports organized secondary lead production across the region.

Heat Map Analysis

| Region | Market Position | Growth Momentum | Regulatory Strength | Recycling Infrastructure | Secondary Lead Production Base |

| Asia Pacific | High | Moderate to High | Moderate | High | High |

| Europe | Moderate | High | High | High | Moderate |

| North America | High | Moderate | High | High | High |

| Latin America | Moderate | Moderate | Moderate | Developing to Moderate | Moderate |

| Middle East & Africa | Low to Moderate | Moderate | Low to Moderate | Developing | Low to Moderate |

Source: Polaris Market Research Analysis

Source: Polaris Market Research Analysis

Key Players & Competitive Analysis Report

The lead acid battery recycling industry has a moderately consolidated global market, with large integrated smelters and local recycling units functioning within a licensed framework. Industry rivalry is determined by the availability of a constant source of scrap material and dominance of the secondary lead production process. Firms continue to enhance furnace efficiency, emission control systems, and recovery rates to ensure cost discipline. They also improve collection infrastructure and regulatory practices to secure long-term contracts with automotive and industrial battery producers.

Key players in the lead acid battery recycling industry include Aqua Metals Inc., Cirba Solutions, Clarios, ECOBAT, East Penn Manufacturing Company, EnerSys, Exide Industries Ltd., Glencore, GME Recycling, Gravita India Ltd., RecycLiCo Battery Materials Inc., Umicore, and others.

Key Players

- Aqua Metals Inc.

- Cirba Solutions

- Clarios

- ECOBAT

- East Penn Manufacturing Company

- EnerSys

- Exide Industries Ltd.

- Glencore

- GME Recycling

- Gravita India Ltd.

- RecycLiCo Battery Materials Inc.

- Umicore

Industry Developments

November 2025: Ecobat secured a renewed permit to continue operations at its lead-acid battery recycling facility in California, strengthening regional recycling infrastructure and regulatory compliance. (source: Recycling Product News)

November 2025: Clarios is expanding battery recycling and critical mineral processing capacity in the US by restarting facilities, upgrading operations, and planning a new plant to strengthen domestic supply chains.

October 2025: Cirba Solutions is boosting national battery recycling access by launching an interactive map with nearly 750 U.S. recycling locations for end-of-life batteries to help consumers find nearby drop-off points and cut barriers to proper recycling.

July 2024: The European Union adopted the new Battery Regulation, establishing stringent targets for the collection, treatment, and recycling of batteries, along with mandatory recycling quotas. The regulation requires a minimum recycling rate of 45% for lead-acid batteries by 2030, as outlined by the European Parliament and Council of the European Union. This initiative is expected to significantly boost growth in the lead-acid battery recycling market.

Lead Acid Battery Recycling Market Segmentation

By Battery Type Outlook (Revenue, USD Billion, 2021-2034)

- SLI batteries

- Industrial & stationary batteries

By Recycling Process Outlook (Revenue, USD Billion, 2021-2034)

- Pyrometallurgical

- Hydrometallurgical

By End User Outlook (Revenue, USD Billion, 2021-2034)

- Automotive

- Industrial

- Telecom

- UPS & backup power

By Regional Outlook (Revenue, USD Billion, 2021-2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Lead Acid Battery Recycling Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 16.02 Billion |

| Market Size in 2026 | USD 16.95 Billion |

| Revenue Forecast by 2034 | USD 26.93 Billion |

| CAGR | 5.94% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2022–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

FAQ's

• The global market size was valued at USD 16.02 billion in 2025 and is projected to grow to USD 26.93 billion by 2034.

• Asia Pacific dominates due to high vehicle production, large replacement battery volumes, and established secondary lead smelting capacity.

• Recycled lead is primarily used in manufacturing automotive starter batteries, industrial power storage systems, telecom backup units, and UPS installations.

• A few of the key players in the market are Aqua Metals Inc., Cirba Solutions, Clarios, ECOBAT, East Penn Manufacturing Company, EnerSys, Exide Industries Ltd., Glencore, GME Recycling, Gravita India Ltd., RecycLiCo Battery Materials Inc., Umicore, and others.

• Growth is driven by rising automotive battery replacement rates and stricter hazardous waste regulations across the world.

Download Sample Report of Lead Acid Battery Recycling Market

Please fill out the form to request a customized copy of the research report.