Lightweight Aggregates Market Demand Scenario and Growth Prospects 2025-2034

REPORT DETAILS

REPORT DETAILS

ABOUT THIS REPORT

Market Statistics

Market Overview

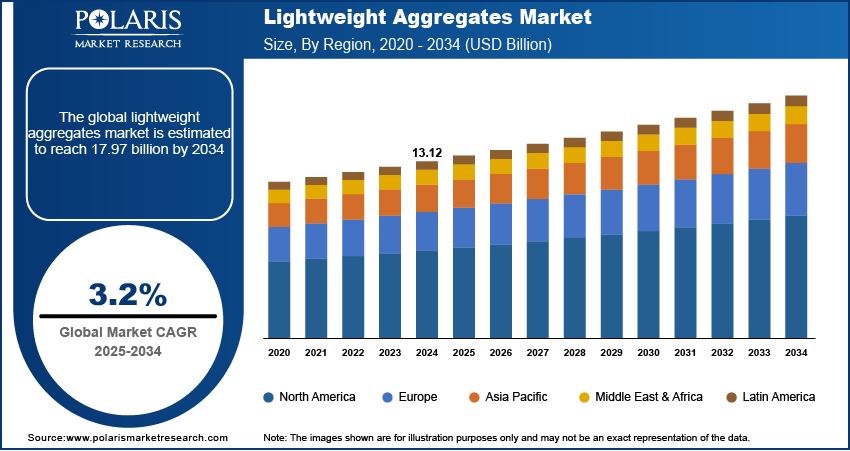

Lightweight aggregates market size was valued at USD 13.12 billion in 2024, exhibiting a CAGR of 3.2% during the forecast period. Rising demand for sustainable construction, urban infrastructure expansion, seismic-resilient buildings, and advanced aggregate technologies is driving market growth.

Key Insights

- Expanded clay led the market in 2024 due to its durability, thermal insulation, and suitability across diverse construction applications.

- Infrastructure was the largest end-user in 2024, driven by demand for lightweight materials in bridge decks, roads, and large public projects.

- Asia Pacific held the largest share in 2024 due to rapid urban growth, affordable housing demand, and infrastructure investments in emerging economies.

- North America is projected to grow fastest due to sustainable building trends, infrastructure rehabilitation, and supportive government funding.

Industry Dynamics

- Rapid urbanization and infrastructure investment in emerging markets is increasing demand for lighter, durable, and cost-effective building materials.

- Growing adoption of green buildings and seismic-resilient structures boosts the use of lightweight aggregates for structural and thermal efficiency.

- Rising use in modular and prefabricated construction enhances market demand due to reduced structural load and faster construction timelines.

- The high initial cost of processing and lack of awareness among small contractors limit widespread adoption in cost-sensitive markets.

Market Statistics

2024 Market Size: USD 13.12 billion

2034 Projected Market Size: USD 17.97 billion

CAGR (2025–2034): 3.2%

Asia Pacific: Largest market in 2024

To Understand More About this Research: Download Sample Report

The lightweight aggregates market refers to the industry focused on the production and distribution of aggregates that possess lower density compared to conventional aggregates. These are typically manufactured from natural materials such as pumice, volcanic rock, and expanded clay, or through industrial byproducts like fly ash and slag. Lightweight aggregates are primarily used in construction applications where weight reduction, insulation, and structural performance are critical, such as in lightweight concrete, precast concrete, bridge decks, geotechnical fills, and roof systems. Their unique properties, including building thermal insulation, low density, and fire resistance coating, make them essential for modern construction practices that emphasize sustainability and energy efficiency. Rising demand for sustainable construction materials that reduce the overall environmental impact of buildings and infrastructure projects.

Increased use of lightweight concrete in high-rise buildings and large-scale infrastructure due to the need for reduced dead load and improved seismic performance is further contributing to the market growth. Expansion of green building initiatives and regulatory emphasis on energy-efficient structures, which is further fueling demand for thermally insulating aggregates.

Market Dynamics

Surging Urbanization and Rapid Infrastructure Development

Surging urbanization and rapid infrastructure development in emerging economies are significantly contributing to the market growth. For instance, the India Brand Equity Foundation reports that India plans to invest around USD 1.723 trillion in infrastructure from FY24 to FY30, focusing on key sectors such as power, roads, and industries like renewable energy and electric vehicles. This initiative aims to drive economic growth and promote sustainability. Expanding residential, commercial, and transportation sectors are placing increased demand on the construction industry for materials that ensure durability while minimizing structural load. Lightweight aggregates have emerged as a viable solution, offering the ability to reduce dead load in multistory buildings, road embankments, and bridges without compromising structural performance. The growing need for seismic-resilient structures in densely populated regions has further strengthened the adoption of lightweight concrete materials. These dynamics are actively driving market expansion, as governments and private developers seek cost-effective, sustainable, and technically efficient materials to meet the rising urban infrastructure demands in high-growth geographies.

Technological Advancements in Aggregate Processing Techniques

Technological advancements in aggregate processing techniques are reshaping the competitive landscape and contributing to the market dynamics. For instance, in November 2024, Neustark and Aggregate Industries are introducing onshore carbon removal technology to the United Kingdom, leveraging innovative methods for capturing and sequestering atmospheric CO2. Innovations in kiln operations, rotary expansion, and cold bonding palletization have enabled the production of aggregates with highly tailored physical and mechanical properties. These improvements are allowing manufacturers to offer materials with specific compressive strength, porosity, and density profiles suited for advanced construction applications. The integration of recycled raw materials such as fly ash and blast furnace slag further supports performance and sustainability goals, attracting investment from environmentally focused developers. Continuous innovation in material engineering is boosting market expansion, creating new opportunities for application across prefabricated structures, geotechnical fill, and thermal insulation layers. These advancements are positioning lightweight aggregates as a critical component in the evolution of modern construction methodologies.

Segment Insights

Lightweight Aggregates Market Assessment by Type Outlook

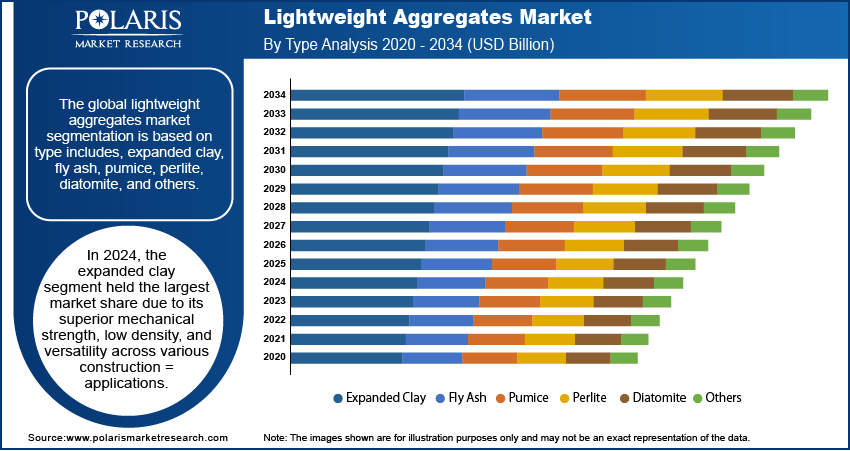

The segmentation based on type includes, expanded clay, fly ash, pumice, perlite, diatomite, and others. In 2024, the expanded clay segment held the largest market share due to its superior mechanical strength, low density, and versatility across various construction applications. Its inert nature, fire resistance, and exceptional thermal insulation properties make it highly suitable for lightweight concrete blocks, floor screeds, and geotechnical fill. The expanded clay segment continues to benefit from increasing preference among developers and engineers seeking long-lasting and sustainable materials. Expanded clay consistent particle shape and low water absorption rate enhance concrete workability and durability.

The pumice segment is expected to record the fastest CAGR over the forecast period, driven by its natural abundance, chemical inertness, and eco-friendly profile. High porosity and low density make pumice highly effective in lightweight concrete applications, especially in regions prone to seismic activity. Increasing demand for environmentally sustainable construction materials is accelerating adoption in both residential and infrastructure projects. The ability of pumice to enhance insulation and acoustic performance further boosts its value proposition. Rising awareness about natural pozzolans and their benefits is significantly contributing to the market growth, particularly in sustainable design and green certification-driven construction frameworks.

Lightweight Aggregates Market Evaluation by End User Outlook

The segmentation based on end user includes, building and construction, industrial, infrastructure, and others. The infrastructure segment accounted for the largest market share in 2024 due to the escalating demand for lightweight materials in bridge decks, precast components, and road substructures. Heavy infrastructure projects often require reduction of dead load to improve stability and lifespan, especially in regions with complex soil conditions. Lightweight aggregates play a crucial role in slope stabilization, embankment fill, and drainage layers, making them integral to infrastructure resilience. Government investments in large-scale public works and transportation networks are further driving demand. These developments are actively contributing to market growth, where performance reliability and cost-efficiency remain key considerations for large engineering contractors.

The building and construction segment is poised to grow at the fastest CAGR over the forecast period, due to rising demand for sustainable building materials in both residential and commercial developments. Lightweight aggregates are gaining traction in the production of lightweight concrete panels, and roofing solutions, all of which benefit from improved thermal efficiency and reduced structural stress. Increasing emphasis on green building certifications and energy-efficient architecture is accelerating adoption across urban housing, schools, and office complexes. Lightweight materials also improve construction logistics by reducing handling and transportation costs. These advantages are fueling expansion across evolving construction practices focused on both performance and sustainability.

Regional Analysis

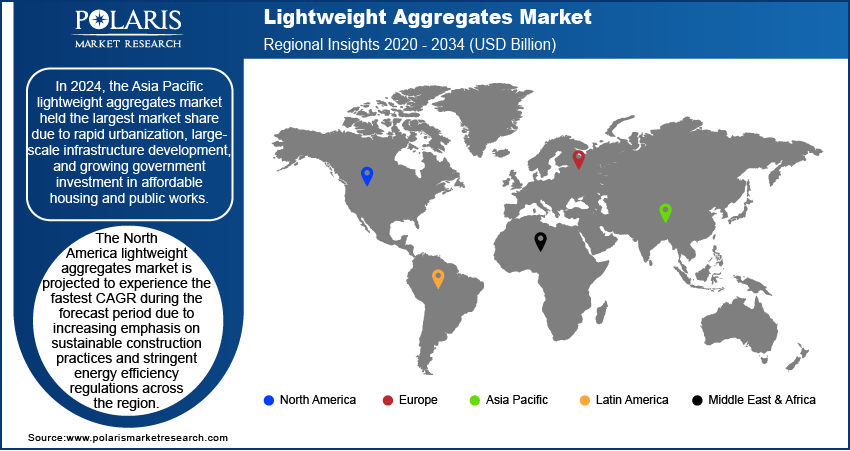

By region, the study provides market insights into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. In 2024, the Asia Pacific held the largest revenue share due to rapid urbanization, large-scale infrastructure development, and growing government investment in affordable housing and public works. For instance, according to the India Brand Equity Foundation by 2030, it is projected that urban areas in India will house approximately 40% of the nation's population, while simultaneously contributing around 75% to the country's Gross Domestic Product (GDP). Incraesing construction sector across emerging economies is creating substantial demand for high-performance, cost-effective, and energy-efficient materials. Lightweight aggregates are increasingly favored in the region for their ability to reduce structural load, improve thermal insulation, and support faster construction timelines. Strong demand from both residential and non-residential sectors, combined with rising adoption of green building practices and advancements in local manufacturing capabilities, is significantly contributing market expansion across the Asia Pacific.

The North America is projected to experience the fastest CAGR during the forecast period due to increasing emphasis on sustainable construction practices and stringent energy efficiency regulations across the region. Strong demand for eco-friendly and lightweight building materials is driven by the need to reduce structural load, improve insulation performance, and enhance seismic resilience. Continued investment in infrastructure rehabilitation particularly in transportation, commercial buildings, and urban housing is accelerating the adoption of advanced construction materials such as lightweight aggregates. For instance, in 2023, the federal government allocated approximately USD 44.8 billion for infrastructure projects and additionally distributed USD 81.5 billion to state governments to support their infrastructure initiatives. Moreover, technological innovations in aggregate production and the region’s proactive approach to green building certifications are contributing to expansion. Rising environmental awareness and policy support for low-carbon construction further strengthen market dynamics.

Lightweight Aggregates Key Market Players & Competitive Analysis Report

The competitive landscape is shaped by a combination of strategic initiatives, product innovation, and capacity expansion efforts aimed at meeting the evolving demands of the construction and infrastructure sectors. Industry analysis highlights a growing focus on expansion strategies, particularly in emerging economies where demand for lightweight, sustainable, and high-strength building materials is intensifying. Key players are actively engaging in joint ventures and strategic alliances to enhance regional presence and optimize supply chains. Product launches featuring aggregates engineered for specific structural, thermal, or acoustic performance are reinforcing differentiation in a highly competitive environment. Technology advancements in manufacturing processes are driving the development of tailored lightweight aggregates with enhanced mechanical properties, contributing to improved application performance across diverse end-use segments. Sustainability mandates and carbon footprint reduction goals are accelerating investments in alternative raw materials and circular economy models.

Arcosa Inc. is engaged in the production and distribution of clay lightweight and rotary kiln-expanded shale aggregates, primarily serving the construction industry. The company specializes in manufacturing lightweight aggregates that enhance the structural integrity of concrete while reducing its overall weight. These products are widely used in applications such as highway and road surfaces, concrete bridge decks, high-rise buildings, geotechnical projects, and horticultural soil amendments. Arcosa operates multiple production facilities across the United States. Arcosas strategic location near America’s inland river system and national railroad network allows it to supply their products across most of the 48 contiguous states efficiently.

Holcim Group is engaged in the production of building materials, including lightweight aggregates for construction applications. The company specializes in innovative solutions for cement, concrete, and aggregates that cater to infrastructure development and industrial projects. Holcim provides services that include sustainable construction materials and advanced engineering solutions for building and construction needs. Holcim has a global presence across Europe, North America, Latin America, Asia Pacific, and Africa. The company's extensive network enables it to serve diverse markets with tailored solutions for urbanization and infrastructure challenges.

Key Companies in the Lightweight Aggregates Market

- Arcosa Inc.

- Argex

- Ashtech Pvt. Ltd.

- Boral Industries Inc.

- Buildex, LLC

- Cemex S.A.B. DE C.V.

- Heidelberg Materials

- Holcim Group

- Laterlite S.P.A.

- Leca International

- Litagg Industries Pvt Ltd

- Northeast Solite Corporation

- Rock Solid Processing Ltd

- Stalite Lightweight Aggregate

- Utelite Corporation

Lightweight Aggregates Market Developments

In July 2025, CRH acquired Eco Material Technologies for USD 2.1 billion, securing a long-term supply of fly ash and pozzolans for lightweight aggregate concrete production.

In September 2024, Rock Solid Processing Ltd launched the CarbonLite range of low carbon aggregates, providing an innovative, eco-friendly alternative to traditional aggregates. This material effectively reduces the carbon emissions linked to construction projects, advancing sustainability efforts in the industry.

In August 2024, Arcosa, Inc. acquired the construction materials division of Stavola Holding Corporation for approximately USD 1.2 billion. This transaction is part of a broader strategic initiative aimed at enhancing the portfolio and accelerating the company’s long-term growth objectives.

In April 2022, Holcim launched Aggneo, a fully natural secondary aggregate that provides a sustainable alternative with comparable quality and performance to virgin aggregates. It is applicable in various civil engineering and construction projects, including tunnels, roads, and precast concrete for landscaping.

Lightweight Aggregates Market Segmentation

By Type Outlook (Revenue USD Billion 2020 - 2034)

- Expanded Clay

- Fly Ash

- Pumice

- Perlite

- Diatomite

- Others

By Application Outlook (Revenue USD Billion 2020 - 2034)

- Walls

- Floors

- Roofs

- Bridges

- Tunnels

- Others

By End Use Outlook (Revenue USD Billion 2020 - 2034)

- Building and Construction

- Residential

- Commercial

- Industrial

- Infrastructure

- Others

By Regional Outlook (Revenue USD Billion 2020 - 2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Lightweight Aggregates Market Report Scope:

| Report Attributes | Details |

| Market Size Value in 2024 | USD 13.12 billion |

| Market Size Value in 2025 | USD 13.53 billion |

| Revenue Forecast in 2034 | USD 17.97 billion |

| CAGR | 3.2% from 2025 to 2034 |

| Base Year | 2024 |

| Historical Data | 2020– 2023 |

| Forecast Period | 2025 – 2034 |

| Quantitative Units | Revenue in USD million, and CAGR from 2025 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

The global lightweight aggregates market size was valued at USD 13.12 billion in 2024 and is projected to grow to USD 17.97 billion by 2034.

The global market is projected to grow at a CAGR of 3.2% during the forecast period.

In 2024, the Asia Pacific held the largest revenue share due to rapid urbanization, large-scale infrastructure development, and growing government investment in affordable housing and public works.

Some of the key players in the market are Arcosa Inc.; Argex; Ashtech Pvt. Ltd.; Boral Industries Inc.; Buildex, LLC; Cemex S.A.B. DE C.V.; Heidelberg Materials; Holcim Group; Laterlite S.P.A.; Leca International; Litagg Industries Pvt Ltd; Northeast Solite Corporation; Rock Solid Processing Ltd; Stalite Lightweight Aggregate; Utelite Corporation.

In 2024, the expanded clay segment held the largest market share due to its superior mechanical strength, low density, and versatility across various construction applications.

The infrastructure segment accounted for the largest market share in 2024 due to the escalating demand for lightweight materials in bridge decks, precast components, and road substructures.

Download Sample Report of Lightweight Aggregates Market

Please fill out the form to request a customized copy of the research report.