Medical Plastics Market Size, Share & Growth analysis, 2026 - 2034

REPORT DETAILS

Medical Plastics Market Summary

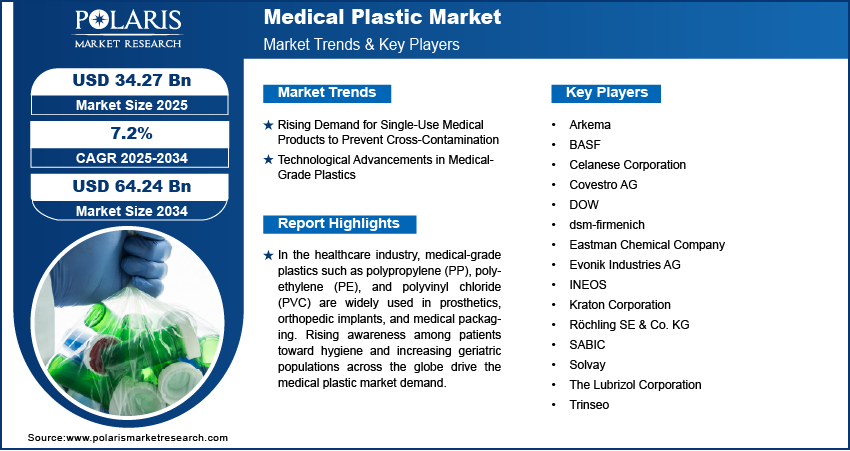

The global medical plastics market size was valued at USD 33.68 billion in 2025, growing at a CAGR of 5.6% from 2026 to 2034. Key factors driving demand for medical plastics include increasing healthcare spending, growing demand for minimally invasive surgeries, and an expanding geriatric population globally.

Market Statistics

Key Takeaways

- The thermoplastics segment accounted for 68.51% of the revenue share in 2025 due to its widespread use in medical device manufacturing.

- The medical instruments & devices segment held 55.30% of total medical plastics demand in 2025 due to growing demand for minimally invasive equipment.

- North America accounted for 42.21% revenue share in 2025, owing to the growing aging population requiring medical devices and implants.

- The U.S. held 87.20% of North America’s medical plastics consumption in 2025, due to widespread adoption of advanced medical technologies.

- The Asia Pacific medical plastic market is projected to register a CAGR of 8.9% during 2026–2034. Increasing government healthcare spending propelled the medical plastics growth.

Industry Dynamics

- The increasing healthcare spending fuels the medical plastics demand by allowing healthcare providers to stock up on plastic-based supplies such as IV bags, tubing, and syringes.

- The growing demand for minimally invasive surgeries is increasing the adoption of medical plastics, as these surgeries require biocompatible materials.

- The expanding clinical trials for cancer research are expected to create lucrative opportunities for the market during the forecast period.

- The stringent regulatory compliance and approval processes regarding plastics used in healthcare applications restrain the market expansion.

Source: Polaris Market Research Analysis

To Understand More About this Research: Download Sample Report

The medical plastics industry encompasses medical-grade polymer materials used in the manufacturing of medical devices, medical disposables, pharmaceutical packaging, and diagnostic equipment. These materials are designed to meet biocompatibility, sterilization, and regulatory standards. Such compliance ensures safety in medical environments. This sets medical plastics apart from regular industrial plastics.

A few types of medical plastics include polyvinyl chloride (PVC), polyethylene (PE), polypropylene (PP), polystyrene (PS), and advanced engineering plastics such as polycarbonate (PC) and polyetheretherketone (PEEK). Medical plastics are widely used in devices, packaging, and equipment. Disposable items such as syringes, IV tubes, and catheters are often made of PVC or PP due to their cost-effectiveness and sterility. High-performance plastics, such as PEEK, are strong and biocompatible. They are used in surgical implants and orthopedic devices. Transparent plastics like PC and polymethyl methacrylate (PMMA) offer clarity and impact resistance. They are ideal for lenses, surgical instruments, and labware. Additionally, medical-grade silicones are flexible and hypoallergenic. Hence, they are used in prosthetics and wound care.

Plastic is increasingly used in packaging applications to ensure sterility and extend shelf life. Blister packs, clamshells, and vacuum-sealed pouches made from PP or PE protect pharmaceuticals and surgical tools from contamination. Antimicrobial plastics infused with additives lower the risk of infections on high-touch surfaces, like hospital beds and equipment housings. Innovations in medical plastics include biodegradable polymers for temporary implants and 3D-printed custom prosthetics. Such advancements improve patient-specific care.

The global medical plastics market demand is driven by the expanding geriatric population globally. According to the United Nations, the global population aged 65 and above will surpass the number of children aged below 18 by 2070. Geriatric population is prone to various diseases. Thus. an increase in this population drives the need for syringes, catheters, wound care materials, orthopedic implants, and other medical supplies. All these products are made from medical-grade plastics. The rise in surgical procedures and the long-term care needs of the elderly increase the demand for sterile, durable, and lightweight plastic medical supplies. Thus, the growing population of older people around the world drives the demand for medical plastics.

Market Dynamics

Drivers

Increasing Healthcare Spending: Increasing Healthcare Spending: Higher budgets allow healthcare providers to use disposable plastic products for hygiene and to expand surgical and diagnostic equipment. They stock up on plastic supplies like IV bags, tubing, and syringes. More funding accelerates medical research and biotechnology. The industry relies on medical plastics for lab equipment, drug delivery systems, and prosthetics, which drives market growth. According to the UK Census Data 2021, total healthcare spending increased by 5.6% in nominal terms in 2023. Governments and the private sector invest higher amounts in healthcare. Thus, manufacturers are increasing production of medical-grade plastics. It helps them fulfil the growing demand for safer, more efficient, and cost-effective solutions.

Growing Demand for Minimally Invasive Surgeries: Minimally invasive surgeries need lightweight, flexible, and biocompatible materials. These materials ensure precision, lower infection risks, and improve patient recovery. Medical plastics meet these needs and drive their demand. Advances in robotic-assisted surgeries and smart medical devices also raise the need for durable, high-precision plastic parts. This expands the market for medical grade polymers. As more hospitals and clinics adopt minimally invasive surgeries to reduce hospital stays and improve results, manufacturers must create more high-performance plastics for single-use surgical tools, implantable devices, and sterile packaging.

Opportunities

Rising Demand for Biodegradable Medical Plastics

Key players and healthcare specialists are focusing on biodegradable medical plastics due to rising sustainability concerns, infection control needs, and advanced manufacturing trends. They focus on the development of antimicrobial medical plastics. Bio-based antimicrobial materials are being developed to lower the risk of hospital-acquired infections (HAIs). Advancements in 3D-printed medical plastics enable patient-specific biodegradable implants, scaffolds, and drug-delivery systems. This supports personalized care while also addressing sustainability and infection control needs. The increasing demand for eco-friendly, high-performance plastics meets strict environmental regulations. It also supports healthcare sustainability efforts globally.

Restraints

Stringent Regulatory Compliance and Approval Processes

Medical plastics regulations demand extensive biocompatibility testing, toxicological assessments, and long-term safety validation, particularly for implantable and patient-contact applications. Regulatory compliance requirements set by FDA, EMA, ISO, and other organizations will increase development timelines and approval costs for manufacturers. Frequent updates to material safety standards, chemical restrictions, and sustainability-related regulations lead to compliance complexity. Limited regulatory expertise and financial resources create entry barriers to small and mid-sized players. Further, global manufacturers need to manage fragmented regulatory frameworks across regions. It is increasing documentation, audits, and post-market surveillance obligations. These factors slow product commercialization, constrain innovation cycles, and increase overall cost structures within the medical plastics industry. Thus, stringent medical plastics regulations and approval processes hinder the market growth.

Source: Polaris Market Research Analysis

Segmental Insights

Polymer Type Analysis

Based on polymer type, the segmentation includes thermoplastics, elastomers, biodegradable polymers, and others. The thermoplastics segment accounted for 68.51% of revenue share in 2025 due to its exceptional versatility, cost-efficiency, and widespread use in medical device manufacturing. Thermoplastics types include polyethylene (PE), polypropylene (PP), and polyvinyl chloride (PVC). Their increasing preference is attributed to their easy processing and chemical resistance. Also, their ability to be sterilized propels thermoplastics demand. Thermoplastics are used in medical devices to meet stringent medical standards. It supports various applications, including tubing, syringes, catheters, and diagnostic equipment housings. These materials support large-scale, hygienic production. It maintains performance and regulatory compliance. The growing demand for disposable devices and single-use components contributed to thermoplastics' dominance. The dominance is also attributed to their cost-effectiveness and suitability for high-volume disposable medical products. Thus, thermoplastics are preferred in the manufacturing of syringes, tubing, and diagnostic housings.

The biodegradable polymers segment is expected to grow at a rate of 9.0% from 2026 to 2034. Growing environmental concerns and stringent rules on medical waste disposal drive the demand for biodegradable medical plastics. Polylactic acid (PLA) and polycaprolactone (PCL) are increasingly used in drug delivery systems, surgical implants, and tissue engineering. Their popularity is rising due to their biocompatibility and biodegradability. The focus on eco-friendly practices in healthcare is driving growth in this area. Developments in bioresorbable polymer technology will also support the use of these materials in different applications. Additionally, healthcare providers and regulators are becoming more aware of the importance of sustainable medical plastics. As a result, biodegradable polymers are becoming more popular.

Application Analysis

In terms of application, the segmentation includes medical instruments & devices, medical disposables, diagnostic instruments & tools, and others. The medical instruments & devices segment held 55.30% of revenue share in 2025. Rising preference for plastics used in medical devices is driven by increasing demand for advanced and minimally invasive equipment. The segment growth is driven by the increasing prevalence of chronic diseases and growing surgical volumes. The rising elderly population requires long-term care solutions, which contributes to the segment dominance. High-performance plastics are used to make parts for surgical instruments, imaging systems, and implantable devices. Superior strength-to-weight ratio, chemical resistance, and biocompatibility drive the segment growth. Innovations in design and material science also helped develop durable, lightweight, and sterilizable products. Due to these advantages, plastics are preferred for many medical devices and instruments.

The medical disposables segment is expected to record a CAGR of 8.2% from 2026 to 2034. The leading position is attributed to rising emphasis on infection control and cost containment. Also, the increasing usage of single-use products in hospitals and clinics boosts the segment growth. High patient turnover, especially in post-pandemic healthcare environments, prompts institutions to adopt disposable products such zas gloves, masks, IV bags, and syringes. The adoption helps institutions reduce cross-contamination risks. Moreover, there is an expansion of outpatient care services and home healthcare settings. Thus, demand for convenient, ready-to-use medical disposable products is rising.

Medical plastics play a critical role in pharmaceutical and medical plastic packaging. It ensures sterility, extended shelf life, and contamination prevention for drugs, implants, and diagnostic tools.

Manufacturing Analysis

Medical plastics manufacturing processes are extrusion tubing, injection molding, compression molding, and others. The extrusion tubing segment was valued at USD 15.10 billion in 2025. The dominance comes from the growing need for high-performance medical tubing in areas like catheters, IV lines, dialysis equipment, and drug delivery systems. Hospitals and outpatient care centers are relying more on polymer-based tubing because of its flexibility, clarity, and resistance to chemicals. The increase in chronic illnesses and minimally invasive procedures has also boosted demand for extrusion tubing. Advancements in co-extrusion and materials engineering enhanced the performance. It allows manufacturers to fulfil evolving clinical requirements and support the segment’s dominance.

The injection molding segment is estimated to record a CAGR of 7.5% from 2026 to 2034. Injection molding can produce complex and high-precision components at scale. It contributes to the dominance of the injection molding medical plastics segment. The process has benefits such as repeatability and design flexibility. It is compatible with various medical-grade polymers. As a result, manufacturers prefer it to produce surgical instruments, parts for diagnostic devices, and implantable components. This technique allows for efficient mass production. It also keeps high tolerances, which are crucial for patient safety and meeting regulations. These features are leading to segment growth.

Source: Polaris Market Research Analysis

Regional Analysis

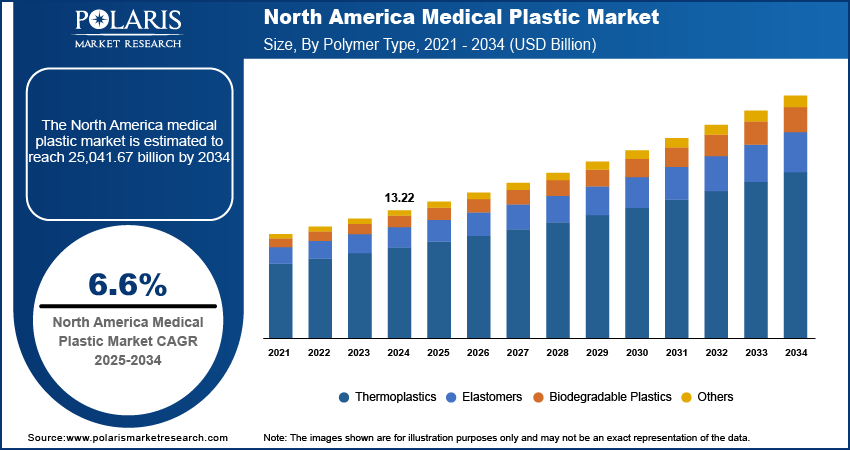

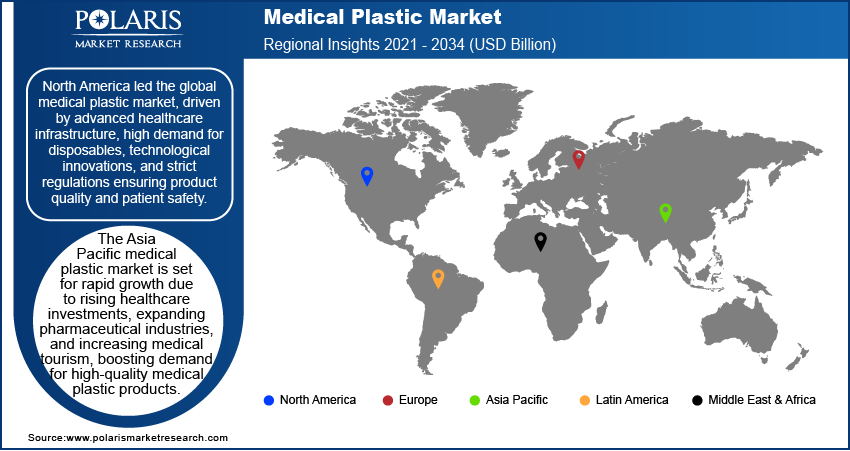

The North America medical plastics market accounted for a 42.21% global revenue share in 2025. This dominance is attributed to advanced healthcare infrastructure and increasing surgical procedures. Also, a growing aging population requiring medical devices and implants contributed to the leading position. According to the Population Reference Bureau, the number of Americans aged 65 and above will increase from 58 million in 2022 to 82 million by 2050. The FDA and Health Canada set strict regulatory standards. These standards ensure high-quality polymer use in medical devices, drug delivery systems, disposable healthcare products, and packaging. The increasing prevalence of chronic conditions, like cardiovascular disorders and diabetes, in the region propelled the demand for polymer-based medical solutions. Furthermore, advancements in biocompatible and biodegradable polymers for minimally invasive surgeries and wearable medical devices push market leadership.

U.S. Medical Plastics Industry Insights

The U.S. held 88.10% of the revenue share in the North America medical plastics landscape in 2025, due to its strong healthcare sector, high R&D investments, and widespread adoption of advanced medical technologies. The increasing prevalence of chronic illnesses and the need for infection-resistant materials in hospitals led market growth in the region. There is a rising shift toward disposable medical devices to prevent cross-contamination. This transition toward single-use devices fueled medical polymer consumption in the U.S. Furthermore, the FDA established supportive policies for innovative polymer-based medical products, such as bioresorbable stents and 3D-printed implants. Such initiatives propelled the U.S. medical plastics market expansion.

Europe Medical Plastics Market Trends

The market in Europe is projected to hold 30.02% of revenue share by 2034 due to stringent EU regulations promoting biocompatibility and sustainability in medical devices. The region reports rising aging population. The geriatric populations is highly prone to various health conditions. Thus, rise in this population drives the need for orthopedic implants, catheters, and prosthetics made from high-performance plastics. Germany, France, and the UK have strong healthcare systems. These countries emphasize on advanced wound care and drug delivery systems. Thus, they are leading in medical polymer adoption. Additionally, the push for eco-friendly medical packaging and recyclable polymers is aligning with Europe’s sustainability goals. Thus, rising adoption of sustainable alternatives is further driving market growth.

Germany Medical Plastics Industry Overview

The Germany medical plastics market demand is being driven by the rising need for precision-engineered implants, surgical instruments, and diagnostic equipment. The country strongly focuses on research and innovation in polymer science. Government of the Germany supports healthcare technology. These factors are sustaining market growth. The increasing use of polymers in minimally invasive surgeries and smart drug delivery systems propels demand for medical plastics. Additionally, Germany’s strict sterilization and hygiene standards in hospitals boost the requirement for high-quality plastic disposable medical products.

Asia Pacific Medical Plastics Market Outlook

The Asia Pacific medical plastic market is projected to register a CAGR of 8.9% from 2026 to 2034. The growth is attributed to expanding healthcare access and rising medical tourism. Increasing government healthcare spending also boosts the growth. Countries such as China, India, and Japan are major contributors. They experience high demand for medical plastics due to growing populations and rising chronic disease prevalence. The growing need for affordable medical devices drives market growth in these countries. The move from traditional materials to polymers in syringes, IV tubes, and surgical gloves creates market opportunities. Furthermore, the booming pharmaceutical industry in India and China increases demand for polymer-based drug packaging. Investments in local polymer manufacturing and partnerships with global medical device companies speed up the China medical plastics market expansion.

Regulatory Compliance Map for Medical Plastics Materials

| Regulatory Body/Standard | Region | Focus Area | Information |

| FDA Biocompatibility Guidance (ISO 10993-1 use) | U.S. | Device material safety | FDA recommends ISO 10993-1 for biocompatibility evaluation based on type and duration of patient contact. |

| ISO 10993-1 | Global | Biological evaluation | Provides a risk-based framework for biological safety testing of medical plastics used worldwide. |

| EU MDR / IVDR | Europe | Device safety & performance | Requires ISO 10993-aligned biological evaluation with enhanced clinical evidence and post-market surveillance. |

| USP <661> | Global | Plastic packaging systems | Defines material quality, extractables, and chemical safety requirements for plastic pharmaceutical packaging. |

| PMDA / NMPA / CDSCO (ISO-aligned) | Asia Pacific | Device approval & safety | Major APAC regulators adopt ISO 10993-based biocompatibility and material safety standards for medical plastics. |

Source: Polaris Market Research Analysis

Source: Polaris Market Research Analysis

Key Players & Competitive Analysis

The medical plastic industry witnesses intense competition. The competition driven by the presence of major players such as DOW, Covestro AG, Celanese Corporation, Eastman Chemical Company, Evonik Industries AG, SABIC, and others. Medical plastics market players emphasize innovative materials science and strategic collaborations. They also focus on global business expansion to maintain their dominance. Innovation in biocompatible polymers, sterilizable plastics, and sustainable solutions is a key focus. It meets regulatory demands and industry trends. Many medical plastics manufacturers invest in research and development. This helps them create high-performance medical polymers for uses such as implants, drug delivery systems, and diagnostic devices. At the same time, new companies and tech-driven disruptors challenge established firms with unique formulations, 3D printing capabilities, and eco-friendly options. Leading firms focus on cost efficiency, regulatory compliance, and developing new materials. This allows them to stand out and maintain their leadership in the changing medical plastics competitive landscape. Leading companies differentiate through regulatory expertise and sterilizable material innovation. These strategies position themselves as long-term partners for medical device OEMs rather than commodity suppliers.

DOW, Covestro AG, Celanese Corporation, Eastman Chemical Company, Evonik Industries AG, SABIC, BASF, Arkema, dsm-firmenich, Kraton Corporation, INEOS, Solvay, The Lubrizol Corporation, Trinseo, and Röchling SE & Co. KG. are among the major companies operating in the medical plastics industry.

Key Players

- Arkema

- BASF

- Celanese Corporation

- Covestro AG

- DOW

- dsm-firmenich

- Eastman Chemical Company

- Evonik Industries AG

- INEOS

- Kraton Corporation

- Röchling SE & Co. KG

- SABIC

- Solvay

- The Lubrizol Corporation

- Trinseo

Medical Plastics Industry Developments

- In June 2025, BASF introduced Ultramid Advanced N3U42G6. It is a new PPA grade for safer, more durable high-voltage EV connectors. KOSTAL Kontakt Systeme is already adopting the material for high-current modules.

- In July 2025, Dow launched INNATE TF 220, an HDPE resin for recyclable, high-performance BOPE films in flexible packaging. Dow also partnered with detergent brand Liby to incorporate 10% REVOLOOP PCR resin into Liby’s new “Floral Era” packaging, advancing scalable mono-material and PCR solutions

- In September 2024, Americhem Healthcare introduced the ColorRx medical grade polymers product line in Europe. With the launch, the company aims to help molders and OEMs start their device development.

- In March 2024, Covestro inaugurated a new polycarbonate copolymer plant in Antwerp. The plant is expected to produce high-quality plastics on an industrial scale, using its technology based on a solvent-free melt process with a new reactor concept.

- In April 2022, Solvay introduced Ixef GS-5022, a lubricated medical-grade polymer for single-use surgical instruments and biopharma components.

Medical Plastics Market Segmentation

By Polymer Type Outlook (Revenue, USD Billion, 2021–2034)

- Thermoplastics

- Polypropylene (PP)

- Polyvinyl Chloride (PVC)

- Polyethylene (PE)

- Polycarbonate (PC)

- Polyurethane

- Acrylonitrile Butadiene Styrene (ABS)

- Others

- Elastomers

- Biodegradable Polymers

- Others

By Application Outlook (Revenue, USD Billion, 2021–2034)

- Medical Instruments & Devices

- Medical Disposables

- Diagnostic Instruments & Tools

- Others

By Manufacturing Outlook (Revenue, USD Billion, 2021–2034)

- Extrusion Tubing

- Injection Molding

- Compression Molding

- Others

By Regional Outlook (Revenue, USD Billion, 2021–2034)

- North America

- U.S.

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Medical Plastics Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 33.68 billion |

| Market Size in 2026 | USD 35.50 billion |

| Revenue Forecast in 2034 | USD 54.86 billion |

| CAGR | 5.6% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2022–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD billion, 2021–2034 and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Medical Plastics Market FAQ's

The global medical plastics market was valued USD 33.68 billion in 2025 and is projected to reach USD 54.86 billion by 2034, with steady growth rates.

The medical instruments & devices segment held 55.30% of revenue share in 2025 due to rising demand for advanced and minimally invasive equipment.

Polypropylene, polyethylene, polycarbonate, and engineering plastics like PPSU dominate. It is due to biocompatibility, sterilization capability, durability, and chemical resistance for medical applications.

North America and Asia Pacific lead the market. Rising aging populations, healthcare investments, and technological advancements boost the dominance.

SABIC, BASF, Celanese, Evonik, Solvay, and Covestro are among the key players. They focus on innovation, acquisition, and R&D investments. The players emphasize expanding production capacity globally.

Download Sample Report of Medical Plastics Market

Please fill out the form to request a customized copy of the research report.