Next Generation Sequencing Market Growth, Size, Analysis Report, 2026 - 2034

REPORT DETAILS

Next Generation Sequencing Market Summary

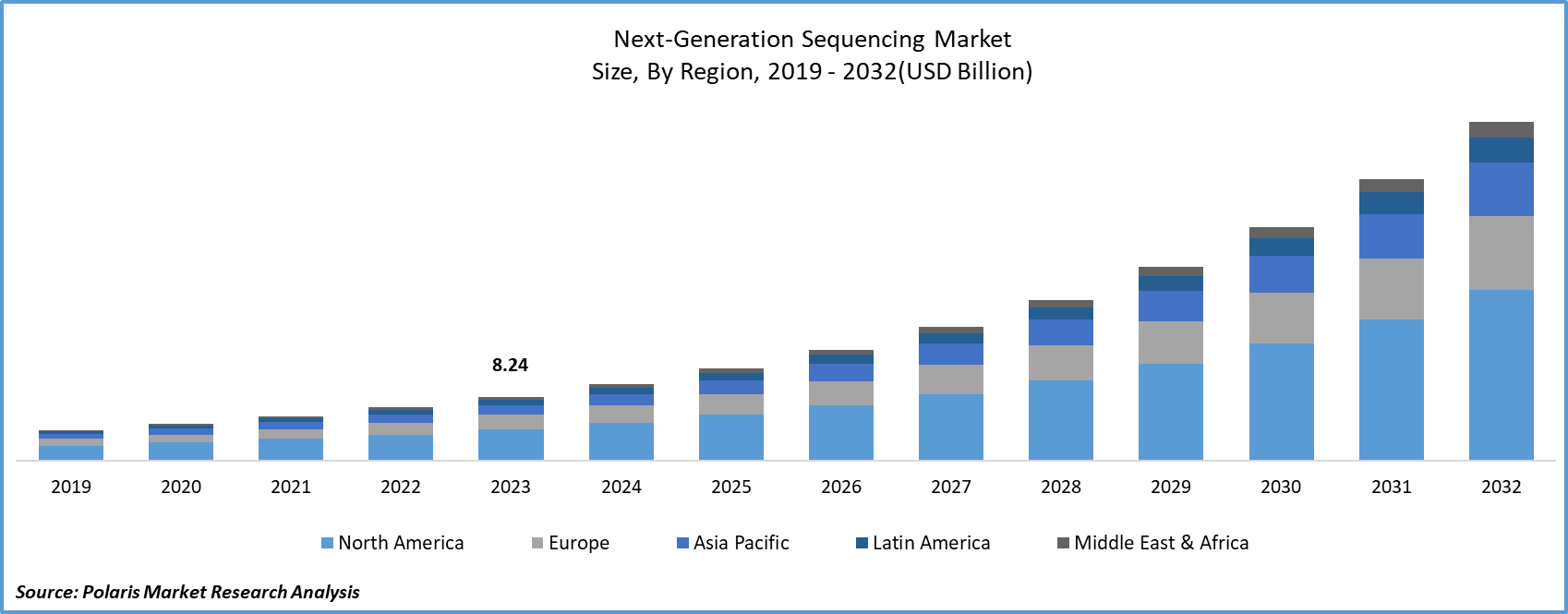

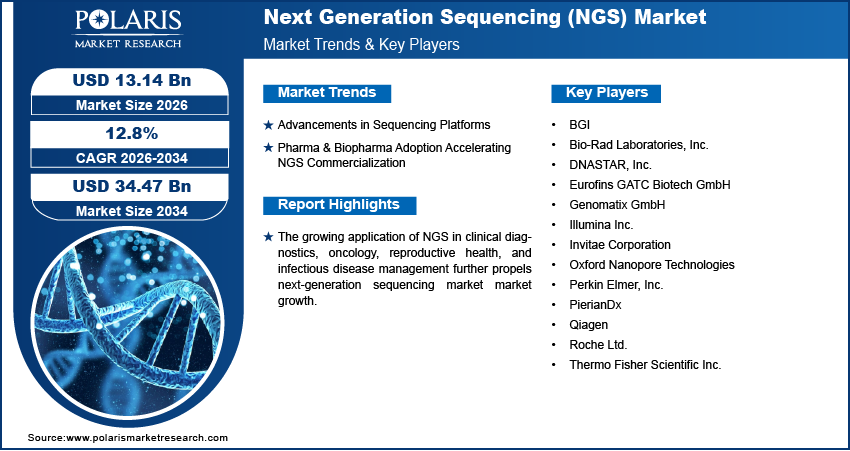

The global next-generation sequencing market size was valued at USD 11.74 billion in 2025. It is projected to register a CAGR of 12.8% from 2026 to 2034. Increasing demand for precision medicine and advancements in genomic technologies drive the market expansion. The rising prevalence of genetic disorders requires comprehensive sequencing solutions, which propels market growth.

Market Statistics

Key Takeaways

- North America led the revenue share in 2025 with an estimated 44.66% share. The leading position is driven by strong healthcare infrastructure and the increasing prevalence of chronic conditions.

- Asia Pacific is likely to grow at the highest rate of 16.76% CAGR, driven by rising R&D spending, the increasing prevalence of chronic diseases, and government incentives.

- In 2025, the diagnostics/infectious diseases segment dominated the next generation sequencing (NGS) market by an estimated 48.10% share. The dominance is driven by the advancement of liquid biopsies for cancer diagnosis and the global impact of the COVID-19 outbreak.

- The sequencing instruments segment dominated in 2025 with an estimated 38.21% share. High demand for advanced sequencing equipment in clinical diagnosis and treatment propelled the dominance

NGS Market Growth Drivers and Restraints

-

The growing use of technology in research and clinical settings for NGS data analysis fuels the market growth.

-

Advancements in sequencing technologies are whole-genome and targeted sequencing. Adoption of these technologies drives robust market growth.

- Artificial intelligence (AI) and machine learning (ML) are becoming common in next-generation sequencing workflows. This integration accelerates variant calling and improves mutation detection. It improves the interpretation of complex genomic datasets. AI-based bioinformatics services and platforms reduce manual intervention. This increases sequencing accuracy and lowers operational costs in research and clinical NGS applications.

- High sequencing technology costs and data management challenges restrain the NGS market size.

AI Impact on Next Generation Sequencing Market

- Beyond data interpretation, AI-powered sequencing platforms improve end-to-end workflow efficiency. It is adopted for various applications, from automated sample preparation to real-time quality control. These advancements are effective in large-scale population genomics projects and clinical diagnostics. In such applications, turnaround time and data accuracy are critical performance indicators.

- Machine learning genomics methods facilitate the detection of patterns and mutations in genomic information. Thus, ML adoption enhances disease diagnosis and personalized treatment design.

- AI tools help reduce errors and make sequencing processes faster and cheaper, making it easier to scale up.

- AI enables effective sequencing data management. It facilitates the efficient analysis of large-scale genomic datasets. Thus, AI adoption enhances research

Source: Polaris Market Research Analysis

Next-generation sequencing has evolved from a research-centric technology into a core pillar of modern clinical diagnostics, drug discovery, and population genomics. The expanding adoption of high-throughput genomic sequencing solutions across oncology, infectious disease testing, and reproductive health significantly reshaped the global next-generation sequencing market outlook. Healthcare systems transition toward data-driven precision medicine models accelerated the NGS demand.

The increasing prevalence of cancer and genetic disorders drives the next generation sequencing market growth. According to WHO, an estimated 20 million new cancer cases and 9.7 million cancer-related deaths were reported in 2022. It is estimated that 53.5 million people were living within five years of being diagnosed with cancer. Around 1 in 5 individuals will develop cancer at some point in their lives, with approximately 1 in 9 men and 1 in 12 women. Further, the rising use of the technology in research and clinical applications is also driving the future demand and outlook of the next-generation sequencing market. The increasing use of NGS in clinical diagnostics, oncology, reproductive health, and infectious disease management drives industry growth. In reproductive health, NGS is used for preimplantation genetic testing and prenatal screening. It offers valuable information about genetic conditions. Such conditions may impact embryos or fetuses. This information aids in making informed decisions about family planning and managing potential hereditary diseases.

Market Trends

Advancements in Sequencing Platforms

Companies in the industry focus on sequencing platform innovation. NGS includes techniques such as whole-genome sequencing, exome sequencing, and targeted sequencing. It facilitates rapid and cost-effective analysis of genetic material. In medicine, NGS helps identify genetic mutations associated with diseases. It plays key role in early diagnosis and personalized treatment plans. The technique is also important in cancer research. It helps clarify the genetic basis of various cancers. Increased use in cancer research boosts the development of targeted therapies and personalized drug development. Additionally, NGS is vital in identifying rare genetic disorders. It is used for prenatal screening and monitoring infectious disease outbreaks by analyzing pathogen genomes. Advancements in sequencing platforms promote market growth.

Pharma & Biopharma Adoption Accelerating NGS Commercialization

Pharmaceutical and biopharmaceutical companies use NGS for various applications. These include identifying genetic mutations, understanding disease mechanisms, and developing targeted therapies. NGS provides a clear view of the genetic causes of diseases. This helps create effective and personalized treatment plans. For example, in cancer research, NGS detects specific genetic changes in tumors. This allows for the development of targeted therapies suited to the genetic profiles of individual patients. Recent advancements in NGS technology have led to wider use due to better accuracy, faster turnaround times, and lower costs across different applications. Additionally, the integration of AI and ML with NGS improves data analysis and interpretation. This results in stronger findings that boost industry revenue.

Source: Polaris Market Research Analysis

Segment Insights

By Workflow Insights

The NGS workflow market segmentation includes pre-sequencing, sequencing, and post-sequencing data analysis. The sequencing segment led the market in 2025 and is expected to register the fastest growth during the projection period. NGS sequencing is an important step in the workflow. Sequencing systems provide accurate liquid amounts, which are essential for NGS. Functions such as micro-liter plates and changing tubes are also done by these systems, helping streamline workflow.

The post-sequencing data analysis segment is projected to witness significant growth. NGS data analysis software platforms are being increasingly used for clinical diagnosis due to reduced installation costs. In addition, the easy availability of proteomic and genomic data is projected to provide several opportunities for the segment’s growth.

Application Insights

The global Next-Generation Sequencing Market segmentation, based on application, includes drug discovery/personalized medicine, genetic screening, diagnostics/infectious diseases, agricultural & animal research, and others. In 2025, the diagnostics/infectious diseases segment dominated the market, owing to an advancement in liquid biopsies in the diagnosis of cancer and the rise of COVID-19 disease across the world. The liquid biopsy utilizes circulating tumor DNA as a cancer biomarker for a real-time diagnosis of cancer.

Furthermore, it provides exceptional sensitivity with low error rates when diagnosing low-level circulating tumor DNA (ctDNA) in the bloodstream. For instance, Fulgent Genetics, Inc., a company specializing in these services based in the United States, unveiled a COVID-19 test based on next-generation sequencing technology in March 2020.

Product Insights

The global market segmentation, based on product, includes instruments, reagents & consumables, and services. The global market segmentation, based on product, includes Instruments, reagents & consumables, and services. The NGS instruments market accounted for the largest revenue share in 2025. NGS instruments provide reliable genetic information in clinical diagnosis and illness treatment. This factor highlights a significant demand for advanced sequencing equipment. Rising technological advancements propel the development of high-throughput sequencing tools. It is allowing for faster and more efficient DNA and RNA sequencing. Rising demand for high-throughput and automated sequencing systems in clinical diagnostics propels the dominance.

The services segment is anticipated to witness the fastest growth throughout the forecast period. As the demand for data analysis and interpretation services grows, these services are becoming more crucial for understanding complex genetic information. The ability of researchers and healthcare professionals to access and analyze vast amounts of genetic data, facilitated by the availability of cloud-based computing systems, is attributed to the segment growth. Also, rising preference for genomic testing services boosts the segment expansion. The sequencing services market is expected to witness the fastest growth as healthcare institutions increasingly outsource data analysis, interpretation, and bioinformatics services to specialized providers.

Comparison of Targeted Sequencing, Whole Genome Sequencing, and Whole Exome Sequencing

| Parameter | Targeted Sequencing | Whole Genome Sequencing (WGS) | Whole Exome Sequencing (WES) |

| Scope | Focuses on specific genes or genomic regions of interest | Sequences the entire genome, including coding and non-coding regions | Sequences only the exome (protein-coding regions) |

| Coverage Depth | High depth for selected targets | Moderate depth across the full genome | High depth for coding regions |

| Cost | Lower cost | Highest cost | Moderate cost |

| Data Volume | Low | Very high | Medium |

| Turnaround Time | Faster | Longer | Moderate |

| Clinical Use | Cancer panels, inherited disease testing, pathogen detection | Rare disease research, comprehensive genomic studies | Genetic disorder diagnosis, rare disease identification |

| Advantages | Cost-effective, highly sensitive, focused results | Most comprehensive genomic information | Balances cost and broad genetic insight |

| Limitations | Limited to predefined targets | Expensive, complex data analysis | Misses non-coding region mutations |

Source: Polaris Market Research Analysis

Source: Polaris Market Research Analysis

Regional Insights

By region, the study provides market insights into North America, Europe, Asia-Pacific, and the Rest of the World. North America held the largest market share in 2025. Well-established healthcare infrastructure and an increasing prevalence of chronic diseases boost the regional market. Government funding for genomics research propels the growth of the regional genomics market, which drives the next generation sequencing market expansion. Also, the presence of key market players in the region and easy access to advanced genomic research technology will drive the North America next-generation sequencing market.

In North America next-gen sequencing market, the U.S. dominated the market in 2025. The dominance is propelled by advancements in genomic research and decreasing costs of sequencing technologies. The increasing application of NGS in personalized medicine propels the U.S. market growth. NGS provides comprehensive insights into genetic variations and mutations. This benefit revolutionizes diagnostics, especially in oncology. In oncology, it allows for accurate tumor profiling and targeted therapies. Additionally, the rise in research activities related to genetic disorders, infectious diseases, and pharmacogenomics fuels the U.S. next generation sequencing market outlook.

Source: Polaris Market Research Analysis

The Asia Pacific next-gen sequencing market is expected to witness the fastest growth in the next-generation sequencing market during anticipated years due to increased investments in research and development activities and the surging prevalence of chronic diseases. Also, government funding for genomics research boosts the Asia Pacific genomics growth. The availability of advanced genomics technologies and the presence of key players in the region are also expected to drive the growth of the next-generation sequencing market regional revenue forecast.

Regulatory Framework Governing the Global Next-Generation Sequencing Market

| Region | Regulatory Authority/Framework | Key Requirements & Focus |

| U.S. | FDA (Food and Drug Administration) | NGS-based in vitro diagnostics (IVDs) are regulated with requirements for analytical and clinical validation; tests may require 510(k), PMA or De Novo pathways. Flexible oversight adapts to novel genomic technology. |

| European Union | In Vitro Diagnostic Regulation (EU IVDR 2017/746) | Stricter IVD oversight than previous directives; risk-based classification, notified body assessment, clinical evidence and post-market surveillance required. |

| Asia-Pacific | NMPA (China), PMDA (Japan), other national regulators | Varying national guidelines; China’s NMPA may require local clinical data; Japan’s PMDA often aligns with global standards but demands additional validation. |

| International Standards | ISO & Global Guidelines | Standards such as ISO laboratory quality (e.g., ISO 15189) and harmonization efforts support consistent NGS quality and data integrity. |

Source: Polaris Market Research Analysis

Key Market Players & Competitive Insights

Leading market players are investing heavily in research and development in order to expand their product lines, which will help the Next-Generation Sequencing Market, grow even more. Market participants undertake various strategic activities to expand their global footprint. Key market developments include new product launches, contractual agreements, mergers and acquisitions, higher investments, and collaborations with other organizations. Industry players must offer cost-effective products to expand and survive in highly competitive and rising market climate.

The next-gen sequencing market presents significant investment opportunities. These are driven by expanding clinical adoption and technological advancements. Favorable government genomics initiatives also boost the investments in the industry. Stakeholders across diagnostics, pharmaceuticals, and healthcare infrastructure increasingly leverage NGS insights to gain competitive and clinical advantages.

Manufacturing locally to minimize operational costs is one of the key business tactics used by manufacturers in the global Next-Generation Sequencing industry to benefit clients and increase the market sector. In recent years, the industry has offered some technological advancements. Major players in the Market, including BGI, Bio-Rad Laboratories, Inc., DNASTAR, Inc., Eurofins GATC Biotech GmbH, Genomatix GmbH, Oxford Nanopore Technologies, Perkin Elmer, Inc., PierianDx, Qiagen, Invitae Corporation, Roche Ltd., Thermo Fisher Scientific Inc., and Illumina Inc.

Why Invest in the Next Generation Sequencing (NGS) Market?

- Strong Revenue Visibility: Clinical diagnostics, pharmaceutical R&D, CROs, and population genomics programs consistently require NGS solutions. This factor wil drive NGS market investments.

- Rising Enterprise Use Cases: There is an increasing focus on oncology, rare disease screening, agrigenomics, and infectious disease surveillance. It will create genomic research opportunities.

- Technology-Led Cost Efficiency: Rising adoption of technological advancements lowers sequencing costs. It also leads to higher throughput platforms. Solution providers and service vendors report improved margins with technology integration.

- Growing Pharmaceutical and Biotechnology Applications: Drug developers are highly reliant on NGS. They use this technique for biomarker discovery, companion diagnostics, and precision medicine pipelines.

- Data & Analytics Upside: Growth in bioinformatics, cloud-based analysis, and AI-enabled interpretation contributes to high-value B2B software revenues.

- Positive Long-Term Outlook: Government genomics initiatives, regulatory approvals, and global healthcare digitization will support favorable sequencing market forecast.

Key Companies

- BGI

- Bio-Rad Laboratories, Inc.

- DNASTAR, Inc.

- Eurofins GATC Biotech GmbH

- Genomatix GmbH

- Illumina Inc.

- Invitae Corporation

- Oxford Nanopore Technologies

- Perkin Elmer, Inc.

- PierianDx

- Qiagen

- Roche Ltd.

- Thermo Fisher Scientific Inc.

Industry Developments

-

April 2026: ACT Genomics announced an upgrade to the ACTDrug® series. It is its next-generation sequencing (NGS) genomic profiling service. The updated panel covers 101 clinically relevant genes. It offers a seven-working-day turnaround time. The series provide comprehensive genomic information to support physicians to make effective treatment decisions for newly diagnosed patients having advanced or metastatic cancer. (Source: actgenomics.com)

-

July 2025: QIAGEN announced the expansion of its NGS Portfolio with the introduction of QIAseq xHYB Long Read Panels. According to QIAGEN, the panels support NGS platforms like PacBio for applications that include structural variants, repeat expansions, and HLA typing. (Source: corporate.qiagen.com)

Future of Next-Generation Sequencing (NGS) Market

The future of the NGS market is fueled by rapid advancements in AI-powered genomics. NGS enables faster data analysis and improves accuracy in disease detection. Growing adoption of personalized medicine is expected to increase demand for precise genetic profiling and targeted therapies. Large-scale population sequencing projects and national genome initiatives are expected to offer lucrative opportunities in the coming years. There is a continuous reduction in sequencing costs, and it has faster turnaround times. These features will make NGS more accessible across clinical diagnostics, research, and drug discovery applications

Market Segmentation

Workflow Outlook

- Pre-Sequencing

- Nucleic Acid Extraction

- Library Preparation

- Sequencing

- Instruments

- Run Data

- Post-Sequencing Data Analysis

- Primary

- Secondary

- Tertiary

- Bioinformatics

Application Outlook

- Drug Discovery/Personalized Medicine

- Genetic Screening

- Diagnostics/Infectious Diseases

- Agricultural & Animal Research

- Others

Technology Outlook

- Whole Genome Sequencing

- Targeted Sequencing & Re-sequencing

- Whole Exome Sequencing

- RNA Sequencing

- Chip Sequencing

- De Novo Sequencing

- Methyl Sequencing

Product Outlook

- Instruments

- Reagents & Consumables

- Services

End-Use Outlook

- Healthcare Institutions

- Academics

- Biotech & Pharma Firms

- Others

Regional Outlook

- North America

- U.S.

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia-Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Next Generation Sequencing Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 11.74 billion |

| Market Size in 2026 | USD 13.14 billion |

| Revenue Forecast in 2034 | USD 34.47 billion |

| CAGR | 12.8% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2022–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD billion, 2021–2034 and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Next Generation Sequencing Market FAQ's

The NGS market was valued at USD 11.74 billion in 2025 and is projected to reach USD 34.47 billion by 2034.

North America leads the NGS market, driven by advanced infrastructure, the presence of major players, and robust research funding initiatives.

Drug discovery/personalized medicine, genetic screening, diagnostics/infectious diseases, and agricultural & animal research are primary applications of NGS.

Leading players include BGI, Bio-Rad Laboratories, Inc., DNASTAR, Inc., Eurofins GATC Biotech GmbH, Genomatix GmbH, Illumina Inc., Invitae Corporation, Oxford Nanopore Technologies, Perkin Elmer, Inc., PierianDx, Qiagen, Roche Ltd., and Thermo Fisher Scientific Inc.

The NGS market is projected to register a CAGR of 12.8% from 2026 to 2034. It is driven by declining sequencing costs and technological advancements.

The market is divided into instruments, reagents & consumables, and services. Among these, sequencing instruments hold the largest share. This is mainly because they are widely used in clinical diagnostics and research labs.

Download Sample Report of Next Generation Sequencing Market

Please fill out the form to request a customized copy of the research report.