Oilfield Chemicals Market Size, Growth Analysis Report, 2026-2034

REPORT DETAILS

Oilfield Chemicals Market Summary

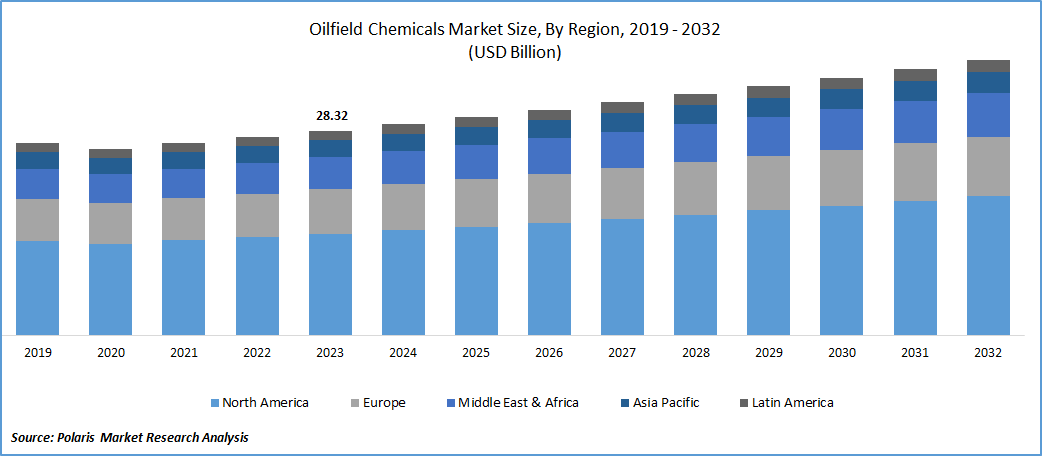

The global oilfield chemicals market size was valued at USD 25.66 billion in 2025 and is projected to grow at a CAGR of 4.9% from 2026 to 2034. This growth is driven by the resurgence in oil exploration and production activities, particularly in mature and aging wells, and technological advancements in drilling operations.

Market Statistics

Key Takeaways

- In oilfield chemicals by application, the workover & completion segment is expected to record a significant CAGR during the forecast period. The rising focus on extending well life and improving recovery rates from mature assets propels the completion and workover chemicals market growth.

- By product, the rheology modifiers segment dominated in 2025. The dominance is attributed to their major role in managing crucial characteristics such as yield, stress, viscosity, responsiveness to change, and the time taken for relaxation of oil wells. Rheology modifiers enable superior fluid stability, efficient cuttings transport, and optimized pumping performance. Thus, rheology modifiers oilfield chemicals are increasingly favored in complex drilling environments. These factors are reinforcing their dominance within the oilfield chemicals market by product.

- In 2025, North America dominated the market. Canada, ranking as the world's fourth-largest producer of crude oil, makes a significant contribution to its growth.

- The oilfield chemicals industry in Asia Pacific is expected to record the highest CAGR during the forecast period, driven by ramped-up exploration and production activities in offshore and onshore oil and gas fields.

Industry Dynamics

- Rising investments in offshore drilling propel the offshore drilling chemicals demand. Offshore drilling serves as a means to access untapped reserves, particularly in deepwater areas, amid soaring global energy demands.

- Technological advancements in offshore drilling equipment and subsea operations boost the consumption of offshore drilling chemicals, particularly corrosion inhibitors, demulsifiers, and flow assurance additives. This factor is strengthening demand across offshore oilfield chemicals applications.

- Burgeoning energy usage in the transportation, manufacturing, and power generation sectors necessitates oil & gas players to ramp up their operations. It bolsters the demand for oilfield chemicals.

- Preference for the implementation of modern oil recovery techniques has led to an upsurge in onshore exploration activities, particularly in developing countries, which creates future growth opportunities for oilfield chemical businesses.

- Oilfield chemicals regulatory compliance with evolving environmental regulations adds financial pressure on manufacturers. Also, the rising oilfield chemicals manufacturing cost limits pricing flexibility and impact margins across the industry.

AI Impact on Oilfield Chemicals Market

- AI-based simulations facilitate real-time analysis of well conditions, reservoir behavior, and drilling parameters. AI in oilfield chemicals helps recommend optimal chemical formulations and dosages. Technology adoption reduces waste and lowers operational costs.

- AI tools can be deployed to predict equipment degradation by monitoring corrosion, scaling, or fouling, creating the scope for proactive chemical treatment strategies.

- In chemical manufacturing, AI simulations can assist in designing and optimizing polymers, surfactants, and other formulations.

- AI-aided R&D can lead to eco-friendly chemicals for oilfield applications through performance and environmental impact modelling. The use of chemicals is important for adherence to stricter regulatory and ESG requirements in oilfields.

- By integrating AI with IoT sensors in wells and pipelines, operators can automate chemical monitoring.

- The integration of AI and IoT-based monitoring systems transforms digital oilfield chemical management. The integration helps with predictive corrosion control and automated dosing. Using these technologies also improves performance. It supports sustainability and ESG goals by reducing chemical overuse.

Source: Polaris Market Research Analysis

Oilfield Chemicals Definition

Oilfield chemicals are a critical component of upstream oil and gas operations. The chemicals are crucial at multiple stages of crude oil production. They are used in various processes, including drilling, production, well stimulation, and reservoir recovery. The chemicals help with efficient drilling, improve production, and ensure flow assurance. They assist in preventing corrosion and meeting environmental standards. The chemicals boost efficiency and ensure safety in oil field operations. The oilfield chemicals market analysis encompasses chemicals used across oilfield lifecycle, from drilling and cementing to production, workover, and enhanced oil recovery. It makes them essential to sustain output from conventional and unconventional reserves.

Oilfield chemicals are essential throughout the oilfield chemicals value chain. The chemicals address issues related to scale formation, corrosion, and emulsion stability. They also help maintain reservoir performance in onshore and offshore oilfield operations. Increasing oil exploration propels the demand for these chemicals. The growth is also driven by rising production activities, boosted by the shale gas boom and technological advancements that enable the extraction of oil and gas from older wells.

Rising integration of advanced technologies and the growing adoption of enhanced oil recovery techniques accelerated onshore exploration activities, particularly in developing economies. Also, a growing global demand for oil products propelled the exploration. The Oil and Gas Producers Association in Brazil (ABPIP) notes that small and medium-sized oil companies in Brazil are projected to invest approximately USD 7.74 billion in onshore fields by 2029. This reflects a trend in which industry players significantly invest in onshore exploration. It helps them meet the rising demand for oil and capitalize on technological advancements in the sector.

Oilfield Chemicals Comparison: Onshore Shale vs Offshore Deepwater

| Parameter | Onshore Shale Operations | Offshore Deepwater Operations |

| Chemical Intensity | High volume, lower unit value chemicals such as friction reducers, biocides, scale inhibitors, and surfactants used in frequent stimulation and flowback cycles. | Lower volume but highly specialized, high-performance chemicals such as corrosion inhibitors, demulsifiers, hydrate inhibitors, and high-temperature scale control products. |

| Qualification Timelines | Shorter (3–9 months) due to standardized well designs, faster trial approvals, and competitive vendor onboarding processes. | Longer (12–24 months) because of strict operator approvals, safety audits, and multi-stage offshore qualification programs. |

| Logistics Constraints | Road transport, regional storage yards, rapid delivery cycles, and high inventory turnover near basins. | Complex marine logistics, helicopter/vessel transport, offshore storage limits, weather dependency, and higher supply chain risk. |

| Typical Chemical Spend Drivers | Well count, lateral length, frac stages, water reuse rates, and stimulation frequency. | Flow assurance requirements, corrosion control, asset integrity, production uptime, regulatory compliance, and offshore safety standards. |

Source: Polaris Market Research Analysis

Oilfield Chemicals Market Drivers

Rising Investment in Offshore Drilling

The oilfield gas market is growing due to rising investments in offshore drilling. For instance, USD 75 million was invested in the offshore segment through the Emissions Reduction Fund (ERF) in Canada. Offshore drilling provides access to untapped reserves, particularly in deepwater areas, as global energy demand increases. Technological advancements in drilling and mining equipment and techniques have made offshore operations more efficient and cost-effective. It attracts more investments in offshore operations. Declining onshore reserves have made offshore fields a key source for new gas production. Governments of various countries announced incentives and supportive policies for offshore operations. Such government support encourages investments in offshore drilling. Increasing oil prices make these costly projects financially feasible. Thus, increasing investments in offshore drilling drive growth in the oilfield chemical market.

Rising Energy Demand

Population growth and rapid industrialization and urbanization lead to a rise in energy consumption. This trend is increasing the demand for oil and gas production. According to the Indian Ministry of Power, energy demand in India increased from 10,15,908 MU in 2022 to 11,02,887 MU in 2023, representing an 8.6% rise. This increase needs efficient and effective oilfield chemicals to support exploration, drilling, production, and refining processes. Chemicals are vital for keeping wells secure, improving extraction methods, and increasing the overall efficiency of oilfield operations. The rising energy demands in transportation, manufacturing, and power generation propels the oil and gas industry growth. Thus, increasing energy consumption fuels the demand for oilfield chemicals.

Source: Polaris Market Research Analysis

Segment Analysis

Market Assessment by Application

The oilfield chemicals market segmentation, based on application, includes drilling, production, cementing, and workover & completion. The workover & completion segment is expected to witness significant growth during the forecast period. Workover is the process of maintaining, repairing, or improving a well after its initial drilling. Completion is about getting the well ready for production. Both stages need specific chemicals to improve well performance, prevent corrosion, boost production efficiency, and manage reservoir conditions. The demand for chemicals used in workover and completion will rise as global oil and gas production increases and operators aim to maximize well output, driving growth in this segment.

Market Evaluation by Product

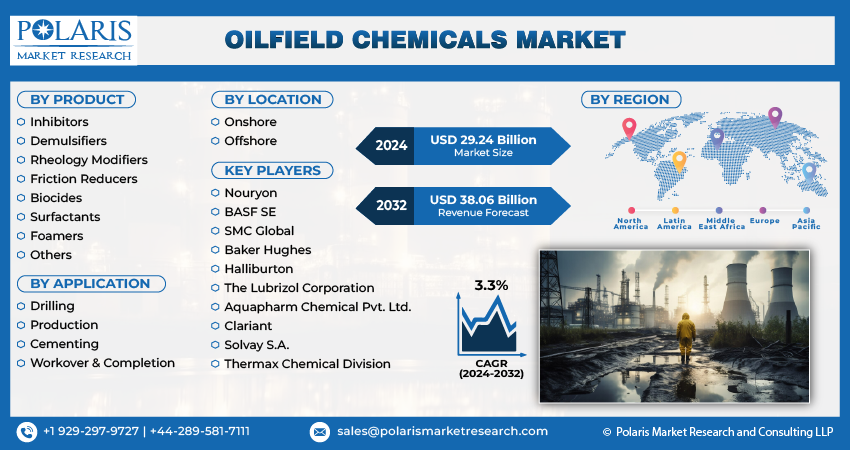

The oilfield chemicals market segmentation, based on product, includes inhibitors, demulsifiers, rheology modifiers, friction reducers, biocides, surfactants, foamers, and others. The rheology modifiers segment dominated the market in 2025 due to the major role of rheology modifiers in modifying the rheological properties of oil wells. They serve as additives in synthetic-based drilling fluids, as well as in water and oil emulsions. Rheology is the study of how materials deform and flow when stress or force is applied. In an oil well, rheological properties include crucial characteristics like yield, stress, viscosity, responsiveness to change, and relaxation time. Also, micro-fibrillated cellulose (MFC) is a key rheological modifier in oilfield operations. It offers stabilization under low shear rates while maintaining ease of pumping compared to alternatives such as xanthan gum, due to its high viscosity.

Source: Polaris Market Research Analysis

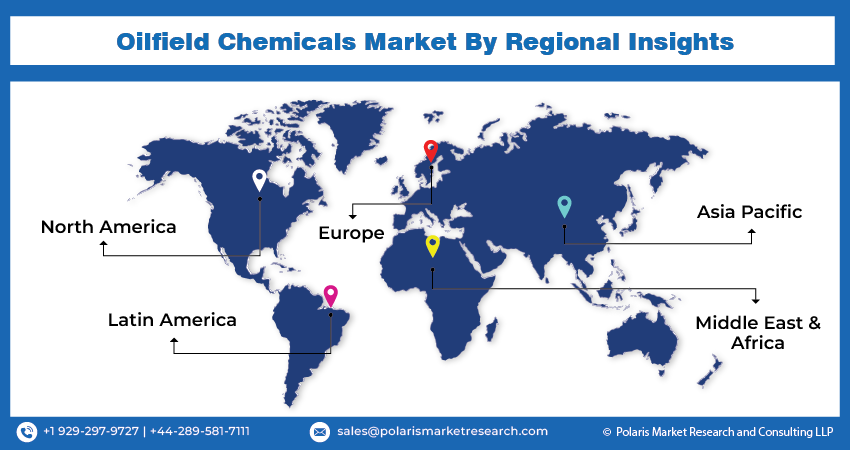

Regional Insights

By region, the study provides the oilfield chemicals market insights into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. In 2025, North America dominated the market. Canada boasts a robust offshore oil and gas industry. The country hosts significant oil-producing facilities, particularly in the provinces of Alberta, where the oil reserves amount to approximately 161.7 billion barrels, and British Columbia, with a crude oil production of around 12,000 barrels per day in 2021. The primary locations for offshore oil exploration in Canada are concentrated in the regions of Labrador & Newfoundland, hosting six major exploration sites. About 30% of the total crude oil produced in Canada undergoes domestic processing, while the remaining portion is refined & purified at the U.S. refineries. All these factors contribute to the growth of the Canadian oilfield chemicals market. Canada’s position as one of the world’s largest crude oil producers and its sustained investments in offshore exploration strengthen the North America oilfield chemicals market, particularly for production and flow assurance chemicals.

The oilfield chemicals industry in Asia Pacific is expected to record the highest CAGR during the forecast period. The Asia Pacific oilfield chemicals market growth is driven by increasing exploration and production activities in offshore and onshore oil and gas fields. Countries such as China, India, Australia, and Indonesia are major contributors to the market. These countries reported growing investments and technological advancements in energy infrastructure. Expanding industrialization and rising energy demand drive the need for efficient oilfield chemicals. In the region, stringent environmental regulations and the increasing need for enhanced oil recovery (EOR) boost the use of these chemicals in oilfield operations. Growth in offshore developments also supports the Asia Pacific oilfield chemicals growth.

India is emerging as a high-potential market supported by government initiatives and upstream investments. The oilfield chemicals market India is growing rapidly, due to its growing oil and gas exploration activities and rising energy demand. The country's growing offshore exploration in the Krishna-Godavari Basin and the rising number of onshore fields require effective oilfield chemicals. Chemicals are necessary to improve drilling and production processes. Rapid industrialization and population growth are driving up energy demand in India. This increases the need for oil and gas. Also, government initiatives like "Make in India" are attracting foreign investments in the oil and gas sector. All these factors are propelling the market in India.

Source: Polaris Market Research Analysis

Key Players and Competitive Analysis

The oilfield chemicals industry is always changing. Market players work hard to innovate and stand out. Top players rely on thorough research and development. They use different techniques. These companies seek strategic initiatives like mergers and acquisitions, partnerships, and collaborations. These strategies help them improve their products and enter new markets.

Oilfield chemicals competitive landscape is characterized by the presence of leading oilfield chemical manufacturers. The manufacturers offer integrated portfolios across drilling, production, and enhanced oil recovery. These aspects enable them to secure long-term contracts with major oil and gas operators.

New oilfield chemicals companies are impacting the oilfield chemical industry by introducing innovative products to meet the demand of specific sectors. The competitive trend is amplified by continuous progress in product offerings. A few major players in the market include Nouryon, BASF SE, SMC Global, Baker Hughes, Halliburton, The Lubrizol Corporation, Aquapharm Chemical Pvt. Ltd., Clariant, Solvay S.A., and Thermax Chemical Division.

Buyers’ Checklist (Procurement-Ready) for Oilfield Chemicals

| Category | Key Evaluation Criteria (B2B Focus) |

| Supplier Qualification | Verify ISO/API certifications, local regulatory approvals, production capacity, supply reliability, and past oilfield references across upstream, midstream, or EOR projects. |

| Technical Compatibility | Assess chemical compatibility with formation fluids, drilling mud systems, water salinity, temperature/pressure conditions, metallurgy, and existing treatment chemistries to avoid scaling, corrosion, or emulsion failure. |

| HSE Documentation | Require Safety Data Sheets (SDS), REACH/GHS compliance, toxicity and biodegradability profiles, spill response plans, transport safety certifications, and site-specific risk assessments. |

| Performance Benchmarks | Define measurable KPIs such as corrosion inhibition %, scale control efficiency, demulsification speed, injectivity improvement, and production uplift under real reservoir conditions. |

| Field Trial Validation | Approve suppliers based on pilot results, operational stability, chemical dosage optimization, cost-per-barrel impact, and ability to meet asset lifecycle performance targets. |

| Commercial & Supply Assurance | Evaluate long-term pricing stability, logistics footprint, inventory availability, local technical support, and digital performance monitoring capabilities. |

Source: Polaris Market Research Analysis

List of Key Companies in Oilfield Chemicals Market

- Aquapharm Chemical Pvt. Ltd.

- Baker Hughes

- BASF SE

- Clariant

- Halliburton

- Nouryon

- SMC Global

- Solvay S.A.

- The Lubrizol Corporation

- Thermax Chemical Division

Oilfield Chemicals Industry Developments

In January 2026, Syensqo completed the previously announced divestment of its Oil & Gas business unit, a global player in oilfield stimulation chemicals, to SNF Group. The unit generated net sales of approximately €400 million in 2024.

In July 2025, SLB secured approval from the UK's Competition and Markets Authority for its $8 billion acquisition of ChampionX. This strategic move strengthens SLB's production systems unit and broadens its expertise in chemicals and automation technologies for oil extraction.

In August 2025, Cathedral Holdings inaugurated a 5,000-square-foot technical lab and office facility in The Woodlands, Texas, providing advanced chemical solutions for oil and gas operations, with a focus on the Permian Basin and Midland regions.

In May 2024, BASF announced the expansion of its Basoflux paraffin inhibitor production capacity at its Tarragona, Spain site. The investment aimed to meet growing global demand, with the first deliveries expected in early 2025, supporting sustainable oilfield solutions.

In May 2024, BASF expanded the production capacity of its Basoflux line of paraffin inhibitors. This investment highlights BASF to advancing innovative and sustainable aqueous-based dispersions tailored for the oil & gas sector.

Oilfield Chemicals Market Segmentation

By Product Outlook (Revenue USD Billion, 2021–2034)

- Inhibitors

- Demulsifiers

- Rheology Modifiers

- Friction Reducers

- Biocides

- Surfactants

- Foamers

- Others

By Application Outlook (Revenue USD Billion, 2021–2034)

- Drilling

- Production

- Cementing

- Workover & Completion

By Location Outlook (Revenue USD Billion, 2021–2034)

- Onshore

- Offshore

By Regional Outlook (Revenue USD Billion, 2021–2034)

- North America

- U.S.

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Oilfield Chemicals Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 25.66 billion |

| Market Size in 2026 | USD 26.86 billion |

| Revenue Forecast in 2034 | USD 39.34 billion |

| CAGR | 4.9% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2022–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD billion, 2021–2034 and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Oilfield Chemicals Market FAQ's

The biocides segment will witness the fastest-growth in the coming years. The rheology segment dominates the market revenue share.

North America leads market revenue share. The dominance is driven by shale gas production and hydraulic fracturing activities. The Middle East & Africa also holds significant share due to extensive oil production.

The workover & completion segment is expected to witness significant demand during the forecast period. Rising oil and gas production worldwide and increasing focus on maximizing well output fuel the segment growth

The market size was valued at USD 32.07 billion in 2024 and is projected to grow to USD 49.77 billion by 2034.

The global market is projected to record a CAGR of 4.50% during the forecast period.

North America held the largest share in the global market in 2024.

A few key players are Nouryon, BASF SE, SMC Global, Baker Hughes, Halliburton, The Lubrizol Corporation, Aquapharm Chemical Pvt. Ltd., Clariant, Solvay S.A., and Thermax Chemical Division.

The rheology modifiers segment dominated the market in 2024, due to the major role of rheology modifiers in modifying the rheological properties of oil wells.

The oilfield chemicals market is expected to grow from USD 25.66 billion in 2025 to USD 39.34 billion by 2034. It is expected to register a CAGR of 4.9% during 2026–2034.

The workover & completion segment is expected to witness significant growth during the forecast period, attributed to the utilization of workover and completion chemicals by oil companies post-oil extraction from wells.

Production chemicals are specialized additives. These include corrosion inhibitors, scale inhibitors, demulsifiers, biocides, hydrate inhibitors, paraffin and asphaltene inhibitors, and surfactants. They help with flow, protect equipment, and maintain fluid quality in oil extraction.

Offshore demand is driven by complex flow assurance challenges (hydrates, wax, scaling) and asset integrity requirements. It is also fueled by long-distance subsea transport issues and stringent operational and regulatory environments.

Oilfield chemicals used in hydraulic fracturing include friction reducers, gelling agents, cross-linkers, breakers, clay control agents, corrosion/scale inhibitors, biocides, pH modifiers, and surfactants. Acids like hydrochloric prepare perforations, while proppants hold fractures open.

Increasing global oil-gas exploration and growing deepwater drilling activities boost the market growth. Also, enhanced oil recovery needs and rising shale gas production contribute to the industry expansion.

Download Sample Report of Oilfield Chemicals Market

Please fill out the form to request a customized copy of the research report.