Mining Equipment Market Size & Share Global Analysis Report, 2026-2034

REPORT DETAILS

Mining Equipment Market Summary

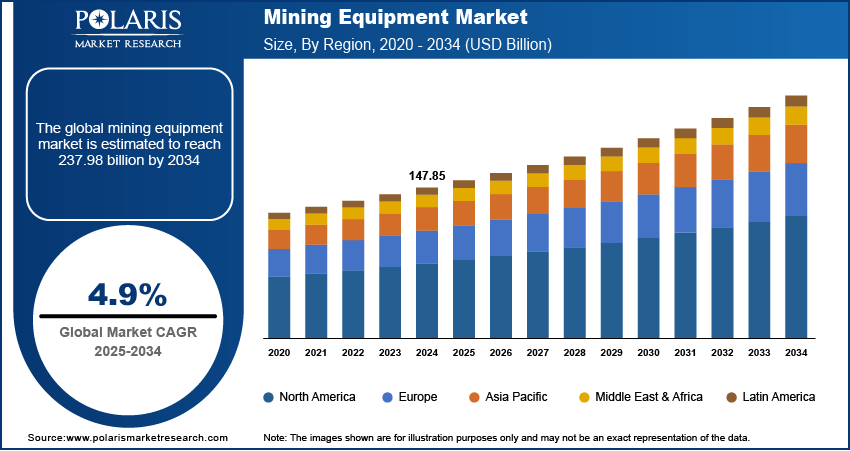

The global mining equipment market size was valued at USD 155.84 billion in 2025 and is projected to register a CAGR of 5.8% from 2026 to 2034. The market is driven by increasing demand for efficient mineral extraction and expanding mining activities in emerging economies.

Market Statistics

Key Takeaways

- Asia Pacific captured a major market share of 49.80% in 2025. The dominance is attributed to intensified mining activities across China, India, and Australia, driven by strong demand for minerals and favorable mining policies.

- The Latin America mining equipment market is projected to register a significant CAGR of 6.4% during the forecast period. It is fueled by increased investments in metal mining and exploration, supported by rich mineral reserves and growing interest from international stakeholders.

- The surface mining equipment segment led the market with 36.15% revenue share in 2025. It is driven by its widespread use in large-scale operations. Its ability to manage high-volume material extraction across diverse terrains efficiently also boosts its dominance.

- The drills and breakers segment is expected to show the highest CAGR of 11.3% during the forecast period. This growth comes from the rising need for high-precision tools that boost efficiency and safety in more complex mining environments.

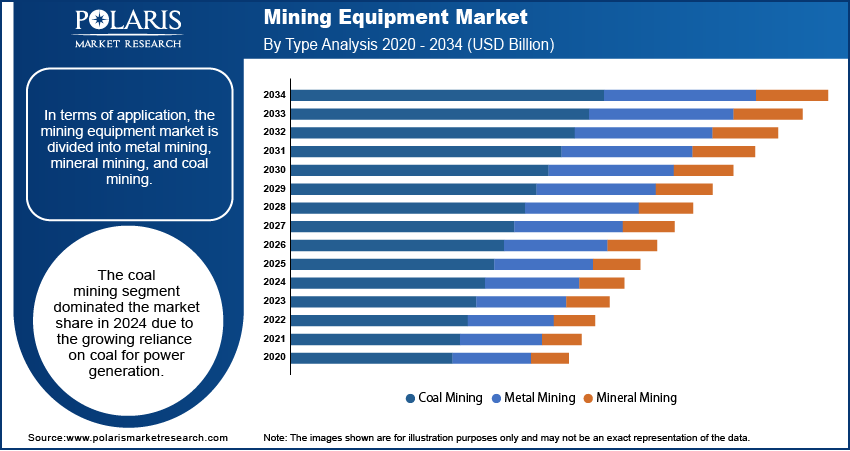

- The coal mining segment held the largest market share of 49.80% in 2025. This growth is due to an increasing dependence on coal as a main energy source, especially in areas where other fuels are not easily available.

Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations.

Industry Dynamics

- Growing demand for efficient material extraction, driven by large-scale mining projects, propels the market.

- Expanding applications across the construction, energy, and infrastructure sectors would create lucrative market opportunities.

- Regulatory challenges, environmental concerns, and high capital investment requirements hinder market growth.

- Technological advancements such as automation, electrification, and smart diagnostics in mining equipment will fuel the market expansion.

Source: Polaris Market Research Analysis

To Understand More About this Research:Download Sample Report

What is Mining Equipment?

Mining equipment means heavy machines and tools used to take minerals and ores from the earth. It includes excavators, drills, loaders, haul trucks, and crushers. These machines help in digging, breaking rocks, moving materials, and processing them. They are used in both surface mining and underground mining processes.

The growing demand for coal around the world, particularly in developing markets, is driving global market growth. According to data from the International Energy Agency, global coal consumption hit a record high in 2022, increasing by 4% compared to the previous year, reaching 8.42 billion tonnes (Bt). The continuous rise in electricity generation is causing higher coal use, which, in turn, boosts the demand for mining equipment.

Mining equipment is essential for the efficient extraction and processing of minerals from the earth. The equipment plays a crucial role in both surface and underground mining operations. It includes a variety of machines. Each machine is intended for specific tasks in the mining process. Excavators, dump trucks, and crawlers & dozers are commonly used for surface mining

The growing mining activities for the extraction of metals drive the market demand. Mining companies require specialized equipment to meet the challenges of accessing deeper deposits, processing complex ores, and adhering to stricter environmental regulations as metal extraction increases. Moreover, the rising global demand for metals such as copper, lithium, and rare earth elements by growing industries such as electronics, renewable energy, and electric vehicles intensifies mining activities, which boosts the demand for mining equipment such as drills, excavators, crushers, and material handling systems.

Mining Equipment Market Growth Drivers

Growing Urbanization Worldwide

The growing urbanization across the world is projected to propel the global mining equipment demand during the forecast period. According to the World Economic Forum, 55% of the world's population lives in urban areas. The population is expected to rise to 80% by 2050 . Urbanization fuels the demand for materials like concrete, steel, and aluminum. This leads to the extraction of key resources such as limestone, iron ore, and bauxite. Because of this, mining companies are expanding operations by using modern equipment like excavators, loaders, crushers, and conveyors to meet higher production targets. The focus on sustainable and efficient mining practices in urban areas is increasing. This trend promotes the use of modern, high-capacity, and eco-friendly mining equipment.

Incorporation of Advanced Technologies

The market is witnessing a rising integration of technologies like automation, artificial intelligence (AI), and the Internet of Things (IoT). Use of these technologies in mining equipment improves efficiency, safety, and productivity. This prompts mining companies to upgrade their equipment. Predictive maintenance tools and data-driven decision-making solutions also boost equipment reliability and reduce downtime. This makes advanced machinery a worthwhile investment and increases its use in deep and complex mining activities. Therefore, the incorporation of advanced technologies in mining equipment is estimated to fuel the global market development.

Market Restraints

High Capital Requirements and Used Equipment Competition

New mining equipment carries significant upfront capital requirements. A modern autonomous haul truck can cost more than USD 5 million per unit. In cost-constrained markets, particularly across sub-Saharan Africa and parts of Latin America, mine operators frequently turn to used and refurbished equipment. The global used mining equipment industry imposes a structural ceiling on new-unit demand in emerging economies, particularly for mid-tier equipment categories. OEMs have responded by expanding certified-used programs and bundling equipment with financing and maintenance contracts to reduce the effective price gap.

Environmental and Regulatory Complexity

Environmental compliance requirements have increased materially across all major mining jurisdictions. Stricter permitting timelines, emissions limits, and water management standards add cost and delay to project development schedules, which in turn defer equipment procurement. In ecologically sensitive geographies, such as the Amazon basin, high-altitude Andean watersheds, and Northern European peatlands, permitting delays of three to seven years are now common for new mine developments. This regulatory friction doesn't reduce long-term equipment demand. However, it creates significant variance between forecast and realized procurement timelines.

Geopolitical Supply Chain Risk

Mining equipment supply chains carry concentrated geopolitical risk in three areas.

- China produces ~85–90% of global rare earth elements. These elements are used in permanent magnets for electric motors, components central to battery-electric mining vehicles.

- Semiconductor chips for autonomous vehicle systems and onboard diagnostics have faced supply disruptions since 2020 that have extended equipment lead times by 18–24 months in some cases.

- Steel and structural components for heavy equipment are subject to ongoing trade policy shifts, including U.S. Section 232 tariffs and EU anti-dumping measures. Mine operators procuring large fleets should factor these supply chain variables into their lead time assumptions and contract structures.

Source: Polaris Market Research Analysis

Segment Analysis

Market Assessment by Type

Based on type, the market is categorized into underground mining equipment; surface mining equipment; crushing, pulverizing, & screening equipment; drills & breakers; and others. The surface mining equipment segment held the largest market share of 36.15% in 2025. This is due to its widespread application in large-scale operations and its ability to handle extensive material extraction efficiently. Industries such as construction, infrastructure development, and energy production heavily rely on resources such as coal, iron ore, and bauxite, which surface mining effectively extracts. The cost efficiency, ease of use, and ability to handle large amounts of minerals make equipment like draglines, power shovels, and large trucks essential. Technology improvements, such as automation and fleet management systems, contributed to the dominance. They enable companies to boost productivity and lower operational costs. The constant demand for resources, driven by rapid urbanization and industrialization in emerging economies, propelled the segment growth.

The drills and breakers segment is expected to exhibit a CAGR of 11.3% during the forecast period. Increasing need for precision and efficiency in mining operations propel the growth. Tools like mining drill bits are essential for breaking down tough rock formations and providing access to deeper mineral deposits. Investments in infrastructure projects and renewable energy initiatives are rising. These projects create requirement for materials such as lithium and rare earth elements. This trend would drive the demand for specialized drilling and breaking equipment. Additionally, the use of technologies, including hydraulic systems, real-time monitoring, and energy-efficient designs, improves their operational capabilities. This development matches the industry’s focus on reducing costs

Surface vs Underground Mining

| Factor | Surface Mining | Underground Mining |

| Definition | Mining done on the earth surface | Mining done below the earth surface |

| Depth | Used for shallow deposits | Used for deep deposits |

| Cost | Lower cost operations | Higher cost due to complexity |

| Productivity | High output, large volume extraction | Lower output compared to surface |

| Equipment Used | Large machines like excavators, haul trucks, draglines | Drills, loaders, underground trucks |

| Safety | Safer, open environment | Higher risk due to confined space |

| Environmental Impact | More land disturbance | Less surface damage but internal impact |

| Maintenance | Easier maintenance of equipment | Difficult maintenance underground |

| Automation Scope | High (autonomous trucks, fleet systems) | Growing but more complex |

| Use Cases | Coal, iron ore, bauxite | Gold, copper, deep minerals |

Source: Polaris Market Research Analysis

Real-World Examples of Mining Equipment

Coal mining operations

Coal is extracted mainly using surface mining. It is used for power generation. It supports large-scale energy needs.

Metal extraction (iron, copper, gold)

Metals are taken from the earth using surface or underground mining. Surface mining is used when deposits are near the ground. Underground mining is used for deeper deposits.

Quarrying (limestone, granite, sand)

Quarrying is done on the surface. It supplies materials for cement and construction work. The process is simple and low cost.

Mineral processing plants

After mining, ores are crushed and separated. This improves the quality of the material. It makes them ready for further use.

Infrastructure-related mining

Mining supplies sand, gravel, and stone. These materials are used in roads and buildings. Demand increases with development.

Market Evaluation by Application

In terms of application, the market is divided into metal mining, mineral mining, and coal mining. The coal mining segment dominated with 49.80% share in 2025. Growing dependence on coal for power generation drives its dominance. Surface mining equipment plays a key role in coal extraction. It provides cost-effective solutions for large operations. This also simplifies access to coal deposits close to the surface. Automation in large excavators and haul trucks boosts productivity and operational efficiency. Such technological improvements reinforce the segment's dominance. Local governments are investing in coal production to ensure energy security. It has increased the demand for machinery and equipment used in coal mining.

Technology Landscape

Automation and Autonomy Levels in Mining Equipment

Automation in mining equipment spans a spectrum from simple telematics and remote monitoring (Level 1–2) through to fully autonomous operation without on-board operator (Level 4–5). The current state of commercial deployment is as follows:

| Autonomy Level | Status in Mining Operations |

| Level 1: Assisted | Collision avoidance alerts, automatic braking, and tire pressure monitoring. Standard on most new trucks and loaders from major OEMs since 2018. |

| Level 2: Partial Automation | Automated speed control on haul routes, auto-levelling on graders, and remote-assist drilling. Widespread in Tier 1 open-cut mines. |

| Level 3: Conditional Automation | Fleet dispatch automation with minimal human intervention |

| Level 4: High Automation | Fully autonomous surface haul trucks operating on defined routes. BHP Jimblebar, Rio Tinto's Pilbara operations, and Fortescue's FMG network operate Level 4 fleets. Currently feasible only on large, well-defined surface operations. |

| Level 5: Full Autonomy | No human operator required in any condition. Not yet commercially deployed in mining; active R&D at Caterpillar, Komatsu, and multiple startups. Likely first commercial deployment 2028–2032. |

Source: Polaris Market Research Analysis

Electrification Technology: Surface and Underground

Electrification is advancing differently across surface and underground operations. Underground mines face the most compelling economics for electrification. They are replacing diesel engines, eliminating heat and exhaust in confined spaces. Electrification substantially reduces ventilation costs, which can represent 30–50% of underground operating energy costs. Epiroc and Sandvik have launched full battery-electric underground drill rig, loader, and haul truck product lines. Surface electrification faces a harder cost hurdle given the larger equipment sizes involved. Komatsu-Cummins and Caterpillar-ELRA are targeting commercial production of 150–300 tonne battery-electric haul trucks before 2027.

Source: Polaris Market Research Analysis

Regional Analysis

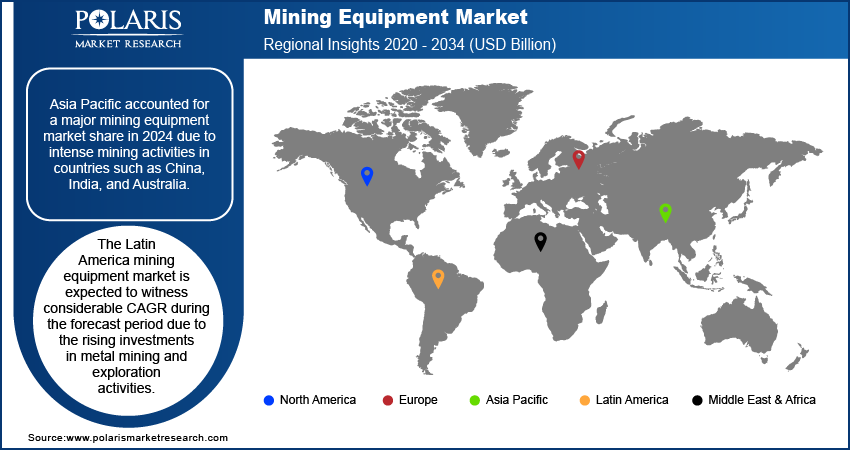

By region, the study provides the insights into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. Asia Pacific led the global market with a major share of 49.80% in 2025. Intense mining activities in China, India, and Australia drives the dominance. China dominated the regional market in 2025. Massive demand for coal, metal recycling, and minerals led to the dominance. India’s growing investments in infrastructure and power generation boost mining activities. This is creating a demand for mining equipment. There is an increasing adoption of surface mining techniques for efficient large-scale resource extraction. This boosts the industry growth. Also, the integration of automation and digitalization technologies fueled the dominance. Rapid urbanization, industrialization, and energy demands across emerging economies drive the need for advanced mining equipment.

The Latin America mining equipment market is expected to witness a significant CAGR of 6.4% during the forecast period. It is due to the growing investments in metal mining and exploration. Countries like Chile, Peru, and Brazil have large copper, lithium, and iron ore deposits. Thus, they attract significant foreign direct investment to improve their mining infrastructure. The shift toward renewable energy and electric vehicles propels the demand for key metals. It makes Latin America an important supplier across the world. Technological advancements are rising, especially in drills and breakers. This enables efficient extraction from the region's tough terrains. It supports the growth of the Latin American industry.

Source: Polaris Market Research Analysis

Key Players & Competitive Analysis Report

Major players are investing heavily in research and development to expand their offerings, which will drive the growth in the coming years. Players undertake a variety of strategic activities to expand their global footprint. They emphasize new product launches, international collaborations, higher investments, and mergers and acquisitions.

The industry is fragmented, with the presence of numerous global and regional players. Major players include Guangdong Leimeng Intelligent Equipment Group Co. Ltd; Henan Baichy Machinery Equipment Co. Ltd; Komatsu Ltd; Liebherr; Atlas Copco AB; Sandvik AB; Doosan Corporation; AB Volvo; Hitachi, Ltd; Deere & Company; Metso Qutotec; Epiroc; Boart Longyear Ltd; Caterpillar Inc.; and Vipeak Mining Machinery Co. Ltd.

List of Key Companies in Market

- AB Volvo

- Atlas Copco AB

- Boart Longyear Ltd

- Caterpillar Inc.

- Deere & Company

- Doosan Corporation

- Epiroc

- Guangdong Leimeng Intelligent Equipment Group Co. Ltd

- Henan Baichy Machinery Equipment Co. Ltd

- Hitachi, Ltd

- Komatsu Ltd

- Liebherr

- Metso Qutotec

- Sandvik AB

- Vipeak Mining Machinery Co. Ltd

Mining Equipment Industry Developments

-

January 2026: Caterpillar Inc. introduced the Cat AI Assistant to improve equipment interaction. It supports operators with real-time guidance and better decision-making. (Source: caterpillar.com)

-

December 2025: Sany Group launched electric excavators, loaders, and trucks at EXCON 2025. This helps the shift toward low-emission and energy-efficient mining operations. (Source: tractorjunction.com)

- September 2025: Cummins Inc. and Komatsu Ltd. signed a memorandum of understanding to co-develop hybrid powertrains for heavy surface mining equipment. The partnership merges Cummins’ long-standing diesel engine expertise with Komatsu’s leadership in mining machinery. Wabtec will supply the drive systems. (Source: cummins.com)

- June 2025: Komatsu bought six Core Machinery dealerships in Arizona and California, expanding its U.S. network to better serve southwest mining customers and improve equipment/service delivery. (Source: komatsu.com)

- May 2025: Epiroc launched the Diamec Automated Rod Magazine (ARM) for core drilling rigs. It allows 252 meters of automated drilling without manual input. The feature boosts safety and productivity. (Source: epiroc.com)

- September 2024: Komatsu, a global manufacturer of construction, mining, forestry, and industrial machinery, introduced the new Z3 series of medium-size class development jumbo drills and bolters to its lineup, further broadening Komatsu's selection of offerings for the underground mining industry. (Source: komatsu.com)

- September 2024: Sandvik, a global engineering company, showcased its latest surface drilling solutions at MINExpo INTERNATIONAL 2024. (Source: pitandquarry.com)

- May 2024: Komatsu introduced the second generation of the company’s Z2 product line of drilling and bolting rigs for mining applications. (Source: komatsu.com)

Mining Equipment Market Segmentation

By Type Outlook (Revenue, USD Billion, 2021–2034)

- Underground Mining Equipment

- Surface Mining Equipment

- Crushing, Pulverizing, & Screening Equipment

- Drills & Breakers

- Others

By Propulsion Outlook (Revenue, USD Billion, 2021–2034)

- Diesel

- CNG/LNG/RNG

By Power Output Outlook (Revenue, USD Billion, 2021–2034)

- < 500 HP

- 500–2,000 HP

- >2,000 HP

By Application Outlook (Revenue, USD Billion, 2021–2034)

- Metal Mining

- Mineral Mining

- Coal Mining

By Regional Outlook (Revenue, USD Billion, 2021–2034)

- North America

- U.S.

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Mining Equipment Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 155.84 Billion |

| Market Size by 2026 | USD 164.78 Billion |

| Revenue Forecast by 2034 | USD 259.94 Billion |

| CAGR | 5.8% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Mining Equipment Market FAQ's

The global market was valued at USD 155.84 billion in 2025. It is expected to reach USD 259.94 billion by 2034.

The market is projected to register a CAGR of 5.8% from 2026 to 2034. It is driven by rising mineral demand, fleet modernization, and expanding automation adoption globally.

Asia Pacific led the market with 49.80% revenue share in 2025. Coal mechanization, nickel expansion, and large iron-ore fleet investments boost the dominance.

Battery-electric vehicle adoption and autonomous haulage systems are key trends. Also, surging demand for critical battery minerals like lithium and cobalt would fuel the industry growth during the forecast period.

A few major players include Guangdong Leimeng Intelligent Equipment Group Co. Ltd; Henan Baichy Machinery Equipment Co. Ltd; Komatsu Ltd; Liebherr; Atlas Copco AB; Sandvik AB; Doosan Corporation; AB Volvo; Hitachi, Ltd; Deere & Company; Metso Qutotec; Epiroc; Boart Longyear Ltd; Caterpillar Inc.; and Vipeak Mining Machinery Co. Ltd. They compete through automation platforms, electrification, and bundled service contracts.

Surface equipment is large and used for open areas. Underground equipment is compact and used in tunnels. Surface is cheaper, underground is more complex

Used in coal mining, metal mining, quarrying, and construction-related mining. Also used in mineral processing plants

It increases production. Saves time and labor. Improves safety. Helps handle large volumes.

Automation means using machines with less human control. Includes autonomous trucks and smart systems. It improves efficiency and reduces errors.

More electric machines will be used. Automation and AI will grow. Focus will be on safety and low emissions.

Download Sample Report of Mining Equipment Market

Please fill out the form to request a customized copy of the research report.