Ostomy Care and Accessories Market Size, Report Overview, 2025-2034

REPORT DETAILS

Market Statistics

Overview

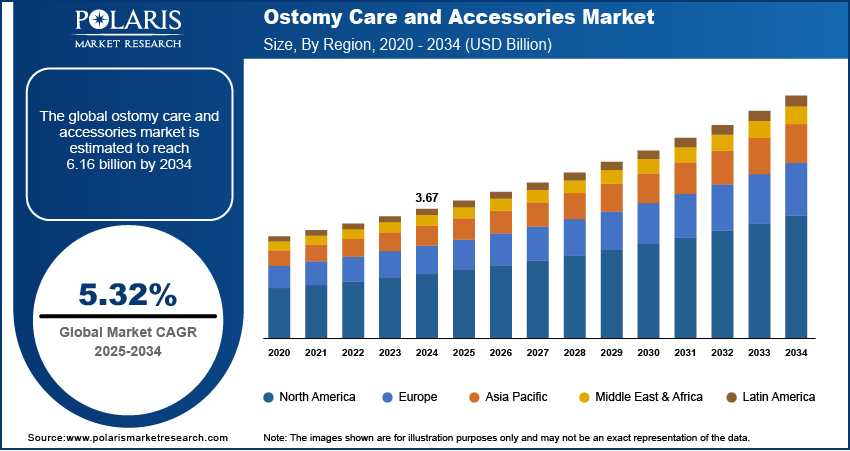

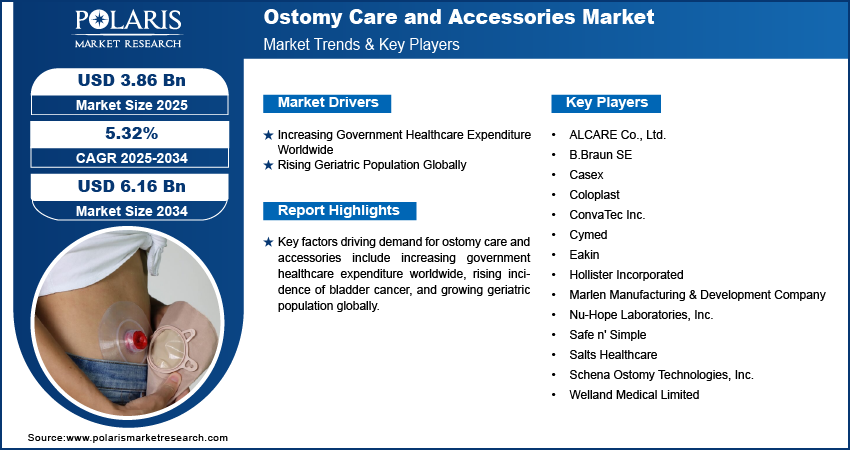

The global ostomy care and accessories market size was valued at USD 3.67 billion in 2024, growing at a CAGR of 5.32% from 2025 to 2034. Key factors driving demand for ostomy care and accessories include increasing government healthcare expenditure worldwide, rising incidence of bladder cancer, and growing geriatric population globally.

Key Insights

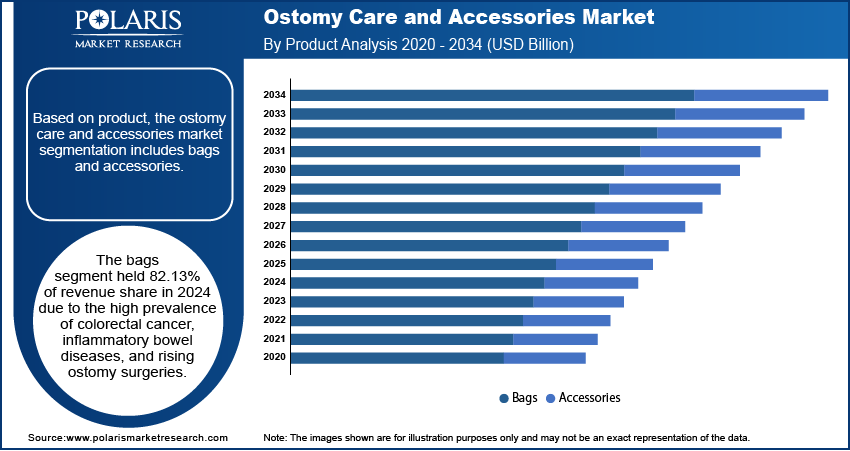

- The bags segment held 82.13% of revenue share in 2024 due to the high prevalence of inflammatory bowel diseases.

- The colostomy segment accounted for 42.34% of revenue share in 2024 due to growing aging population globally.

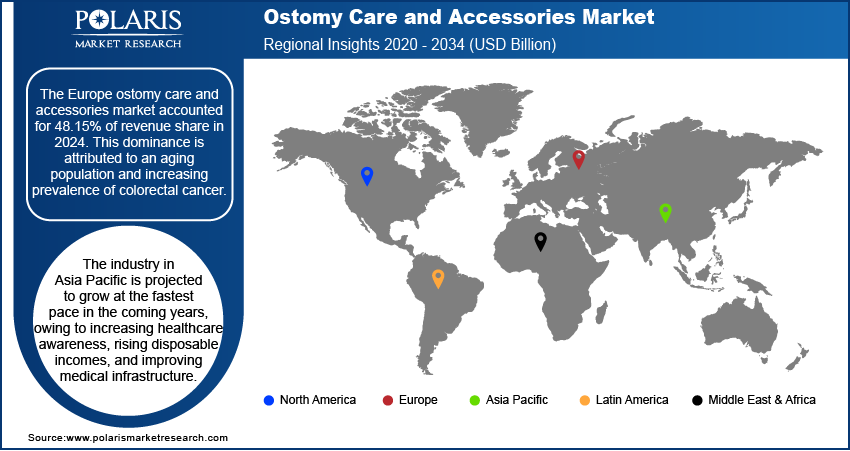

- The Europe ostomy care and accessories market accounted for 48.15% of global revenue share in 2024, owing to the increasing prevalence of colorectal cancer and other conditions requiring ostomy surgeries.

- Germany held the largest revenue share in the European ostomy care and accessories landscape in 2024, due to the high incidence of colorectal diseases.

- The industry in Asia Pacific is projected to grow at the fastest pace in the coming years, owing to rising disposable incomes.

Industry Dynamics

- The increasing government healthcare expenditure worldwide is driving the demand for ostomy care and accessories by reducing costs for ostomy patients who require supplies such as pouches, barriers, and skin care products frequently.

- The rising geriatric population globally is creating the need for ostomy care and accessories, as older adults usually face higher risks of conditions such as colorectal cancer, inflammatory bowel disease, and bladder dysfunction.

- Expanding focus on the home healthcare setting is projected to create a lucrative market opportunity during the forecast period.

- Skin irritation around the stoma hinders the market growth.

AI Impact on Ostomy Care and Accessories Market

- AI-driven analytics personalize products to individual needs, improving comfort and reducing complications.

- AI-powered ostomy bags monitor output and skin health, alerting users to potential issues.

- Predictive analytics streamlines inventory management, ensuring timely access to essentials.

- Automation lowers production costs, making advanced care more affordable.

- AI’s integration boosts accessibility, innovation, and quality in ostomy care.

Market Statistics

- 2024 Market Size: USD 3.67 Billion

- 2034 Projected Market Size: USD 6.16 Billion

- CAGR (2025–2034): 5.32%

- Europe: Largest Market Share

Source: Polaris Market Research Analysis

Ostomy care and accessories refer to the specialized products and practices used to manage an ostomy, a surgical opening created to divert waste from the body. This includes pouching systems, skin barriers, medical adhesives, and cleaning & hygiene products designed to ensure hygiene, comfort, and security. Accessories such as belts, perfumes & deodorants, and protective creams are used to enhance care. Proper ostomy management helps maintain skin health, prevent leaks, and improve the quality of life for individuals with stomas.

Ostomy care products provide security, comfort, and confidence by preventing leaks and skin irritation. They enable active lifestyles, reduce odors, and promote hygiene. High-quality accessories ensure discreet wear, ease of use, and better adhesion, enhancing emotional well-being and independence for ostomates. Proper care minimizes complications, allowing individuals to focus on daily activities without discomfort or anxiety.

The global demand for ostomy care and accessories is driven by the rising incidence of bladder cancer. Worldwide, the number of new bladder cancer cases was estimated to increase by approximately 72.8%, from 573,000 in 2020 to 991,000 by 2040. This is driving the need for urinary diversion procedures, such as urostomies, which create an artificial opening for urine excretion, leading to high demand for ostomy care and accessories. Healthcare providers and manufacturers are also responding to this rising incidence by ensuring product availability, innovation, and patient education to meet the needs of a larger ostomy-dependent population. Therefore, as more people suffer from bladder cancer, the demand for ostomy care and accessories increases.

Drivers & Opportunities

Increasing Government Healthcare Expenditure Worldwide: Governments worldwide are investing more in healthcare through expanding insurance coverage, which is reducing costs for ostomy patients who require ongoing supplies such as pouches, barriers, and skin care products. The share of Indian government health expenditure in the total health expenditure has increased from 29.0% to 48.0% between FY15 and FY22. Additionally, higher healthcare spending is supporting research and innovation, leading to advanced ostomy products that attract more users. Therefore, greater government investments in healthcare is creating a larger and sustainable demand for ostomy care solutions, leading to market growth.

Rising Geriatric Population Globally: Older adults usually face higher risks of conditions such as colorectal cancer, inflammatory bowel disease, and bladder dysfunction, which require ostomy surgeries and accessories. The World Health Organization, in its report, stated that by 2030, 1 in 6 people in the world will be aged 60 years or over. Aging also weakens the body’s natural healing processes. Thus, the geriatric population needs reliable ostomy products, such as pouches, barriers, and skin care solutions, to manage their stomas effectively and prevent complications. The growing elderly demographic is further driving healthcare providers and manufacturers to expand product availability and innovate more comfortable, user-friendly ostomy accessories tailored to seniors’ needs, contributing to industry expansion.

Source: Polaris Market Research Analysis

Segmental Insights

Product Analysis

Based on product, the segmentation includes bags and accessories. The bags segment held 82.13% of revenue share in 2024 due to the high prevalence of colorectal cancer, inflammatory bowel diseases, and rising ostomy surgeries. Manufacturers focused on innovations such as lightweight materials, odor-control technology, and skin-friendly adhesives to improve patient comfort. Additionally, increasing awareness about advanced ostomy products and strong reimbursement policies in developed regions further contributed to the segment's dominant position.

The accessories segment is estimated to grow at a robust pace in the coming years. Patients increasingly seek add-ons for better pouch security, leak prevention, and improved mobility, especially during physical activities. The aging population, which prioritizes ease of use and stability, further propels demand. Additionally, expanding e-commerce platforms are making these products more accessible, leading to segment growth.

Application Analysis

In terms of application, the segmentation includes colostomy, ileostomy, and urostomy. The colostomy segment accounted for 42.34% of revenue share in 2024 due to inflammatory bowel diseases requiring surgical interventions. The increasing adoption of colostomy bags with advanced features such as enhanced leak protection, odor control, and skin-friendly adhesives contributed significantly to the segment dominance. Additionally, improved healthcare infrastructure in developing regions and greater awareness of post-operative care solutions further strengthened the segment's position. The growing geriatric population, which is more susceptible to colorectal conditions, is driving the segment growth.

End Use Analysis

In terms of end use, the segmentation includes home care settings, hospitals, and others. The home care settings segment held 47.69% of revenue share in 2024 due to increasing preference for at-home patient care and the rising adoption of cost-effective, user-friendly ostomy care products. The growing geriatric population, coupled with a higher incidence of colorectal cancer and inflammatory bowel diseases, significantly contributed to the dominance. Patients increasingly favored home care due to its convenience, privacy, and reduced hospitalization costs. Manufacturers also focused on developing advanced, easy-to-use products such as skin-friendly adhesives and odor-control pouches, further boosting demand in this segment. Additionally, the expansion of home healthcare services and improved reimbursement policies in key regions such as North America and Europe strengthened the segment value.

The hospitals segment is expected to grow at a rapid pace in the coming years, owing to the rising number of surgical procedures, including ostomy surgeries, and the need for professional post-operative care. Hospitals offer specialized care, ensuring proper stoma management and reducing complications, which makes them a preferred choice for patients undergoing complex surgeries. The increasing prevalence of chronic diseases requiring surgical interventions, along with advancements in hospital infrastructure in emerging economies, is further projected to propel the segment growth. Additionally, hospitals are adopting innovative ostomy products, such as convex barriers and drainable pouches, to enhance patient outcomes, contributing to their leading position.

Source: Polaris Market Research Analysis

Regional Analysis

The Europe ostomy care and accessories market accounted for 48.15% of global revenue share in 2024. This dominance is attributed to an aging population, increasing prevalence of colorectal cancer, inflammatory bowel diseases (IBD), and other conditions requiring ostomy surgeries. On January 1st, 2024, the EU population was estimated at 449.3 million people, and more than one-fifth (21.6%) of it was aged 65 years and over. Improved healthcare infrastructure and reimbursement policies in countries such as the UK, France, and Italy supported patient access to advanced ostomy products. Additionally, rising awareness about ostomy care and the availability of innovative, skin-friendly, and discreet products boosted market growth. Patient support groups and government initiatives further contributed to the adoption of high-quality ostomy solutions in Europe.

Germany Ostomy Care and Accessories Market Insights

Germany held the largest revenue share in the Europe ostomy care and accessories landscape in 2024. The dominance is attributed to its established medical system and high incidence of colorectal diseases. The country’s aging population and increasing surgical procedures for cancer and IBD drove the need for reliable ostomy products. German patients benefited from favorable insurance coverage, encouraging the use of premium ostomy accessories. Additionally, a strong focus on R&D and the presence of major medical device companies ensured continuous innovation in ostomy care, enhancing comfort and convenience for users.

North America Ostomy Care and Accessories Market Analysis

The market in North America is projected to hold a substantial revenue share by 2034. The growth is driven by the high prevalence of colorectal cancer, Crohn’s disease, and ulcerative colitis, along with a growing geriatric population. The U.S. and Canada have developed healthcare systems that facilitate access to advanced ostomy products. Increasing awareness about ostomy care management, coupled with the availability of customizable and leak-proof solutions, supports market expansion. Additionally, favorable insurance policies and strong patient advocacy groups are playing a crucial role in driving demand for high-quality ostomy accessories.

U.S. Ostomy Care and Accessories Market Overview

The demand for ostomy care and accessories in the U.S is being driven by its high healthcare expenditure and large patient pool requiring ostomy procedures. American Medical Association, in its article, stated that health spending in the U.S. increased by 7.5% in 2023 to $4.9 trillion from 2022. Rising colorectal cancer cases, obesity-related surgeries, and IBD contribute to the growing demand. The presence of key players is ensuring a steady supply of innovative products such as odor-control bags, adhesive barriers, and wearable sensors. Furthermore, Medicare and private insurance coverage for ostomy supplies are enhancing affordability, while patient education programs and digital health tools are improving adherence to ostomy care.

Asia Pacific Ostomy Care and Accessories Market Trends

The industry in Asia Pacific is projected to grow at the fastest pace in the coming years. The expansion is fueled by increasing healthcare awareness, rising disposable incomes, and improving medical infrastructure. Countries such as Japan, China, and India are witnessing a surge in colorectal diseases and cancer cases, driving demand for ostomy products. Government initiatives to enhance surgical care and the growing adoption of Western medical practices are contributing to market growth. However, cost sensitivity and limited reimbursement policies in some regions are posing challenges. Despite this, manufacturers are introducing affordable and advanced ostomy solutions to cater to this rapidly growing region.

Source: Polaris Market Research Analysis

Key Players & Competitive Analysis

The global ostomy care and accessories market is highly competitive, with key players such as Coloplast, ConvaTec Inc., and Hollister Incorporated leading the industry through innovation, product diversification, and strong brand recognition. These companies dominate the market with advanced skin-friendly adhesives, odor-control technologies, and user-friendly pouching systems. B. Braun SE and Welland Medical Limited focus on cost-effective solutions, catering to price-sensitive markets, while ALCARE Co., Ltd. and Schena Ostomy Technologies, Inc. emphasize niche products like convex barriers and specialty seals. Emerging players such as Safe n’ Simple and Nu-Hope Laboratories, Inc. compete by offering customizable accessories, including belts and support systems. Marlen Manufacturing & Development Company and Salts Healthcare differentiate themselves through high-quality manufacturing and patient-centric designs. Regional competition is intensifying, with companies expanding into developing markets through strategic partnerships and e-commerce distribution. Sustainability initiatives, such as biodegradable materials and reusable products, are becoming key differentiators.

A few major companies operating in the ostomy care and accessories industry include ALCARE Co., Ltd.; B.Braun SE; Casex; Coloplast; ConvaTec Inc.; Cymed; Eakin; Hollister Incorporated; Marlen Manufacturing & Development Company; Nu-Hope Laboratories, Inc.; Safe n' Simple; Salts Healthcare; Schena Ostomy Technologies, Inc.; and Welland Medical Limited.

Key Players

- ALCARE Co., Ltd.

- B.Braun SE

- Casex

- Coloplast

- ConvaTec Inc.

- Cymed

- Eakin

- Hollister Incorporated

- Marlen Manufacturing & Development Company

- Nu-Hope Laboratories, Inc.

- Safe n' Simple

- Salts Healthcare

- Schena Ostomy Technologies, Inc.

- Welland Medical Limited

Ostomy Care and Accessories Industry Developments

In September 2024, Convatec, a medical products and technologies company, acquired Livramedom, a home care service provider based in France, to expand its presence in Europe in the direct-to-consumer market.

In February 2024, Convatec announced the launch of Esteem Body with Leak Defense in Italy.

In September 2021, Coloplast opened its first factory in Central America to support the global growth of the company, which produces medical devices, including ostomy pouches and catheters.

Ostomy Care and Accessories Market Segmentation

By Product Outlook (Revenue, USD Billion, Volume Unit, 2020–2034)

- Bags

- One Piece

- Two Piece

- Accessories

- Seals/Barrier Rings

- Pouch Cover

- Pouch Closures

- Stoma Caps/Hat

- Others

By Application Outlook (Revenue, USD Billion, Volume Unit, 2020–2034)

- Colostomy

- Ileostomy

- Urostomy

By End Use Outlook (Revenue, USD Billion, Volume Unit, 2020–2034)

- Home Care Settings

- Hospitals

- Others

By Regional Outlook (Revenue, USD Billion, Volume, Unit, 2020–2034)

- North America

- U.S.

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Ostomy Care and Accessories Market Report Scope

| Report Attributes | Details |

| Market Size in 2024 | USD 3.67 Billion |

| Market Size in 2025 | USD 3.86 Billion |

| Revenue Forecast by 2034 | USD 6.16 Billion |

| CAGR | 5.32% from 2025 to 2034 |

| Base Year | 2024 |

| Historical Data | 2020–2023 |

| Forecast Period | 2025–2034 |

| Quantitative Units | Revenue in USD Billion, Volume in Units, and CAGR from 2025 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Ostomy Care and Accessories Market FAQ's

The global market size was valued at USD 3.67 billion in 2024 and is projected to grow to USD 6.16 billion by 2034.

The global market is projected to register a CAGR of 5.32% during the forecast period.

Europe dominated the market in 2024.

A few of the key players in the market are ALCARE Co., Ltd.; B.Braun SE; Casex; Coloplast; ConvaTec Inc.; Cymed; Eakin; Hollister Incorporated; Marlen Manufacturing & Development Company; Nu-Hope Laboratories, Inc.; Safe n' Simple; Salts Healthcare; Schena Ostomy Technologies, Inc.; and Welland Medical Limited.

The bags segment dominated the market revenue share in 2024.

The hospitals segment is projected to witness the fastest growth during the forecast period.

Download Sample Report of Ostomy Care and Accessories Market

Please fill out the form to request a customized copy of the research report.