August 2025: Rapid7 acquired a leading threat intelligence firm to strengthen its penetration testing services and expand its cybersecurity solutions, reflecting industry consolidation.

Penetration Testing Market Share, Size, Trends, Industry Analysis Report, 2026 - 2034

Penetration Testing Market Share, Size, Trends, Industry Analysis Report, 2026 - 2034

REPORT DETAILS

Report Code: PM2372

No. of Pages: 125

Format: PDF

Published Date:

Base Year: 2025

Author: Apurva Agarwal

Historical Data: 2021-2024

Reviewed By: Likhil Gajbhiye

Penetration Testing Market Summery

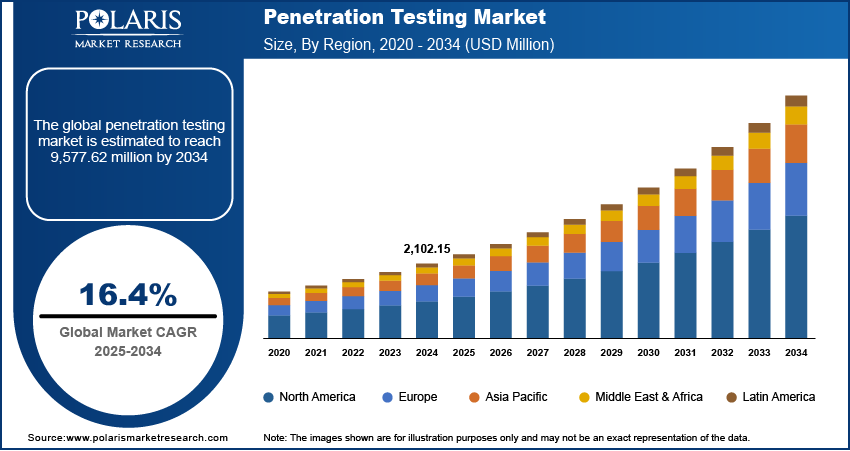

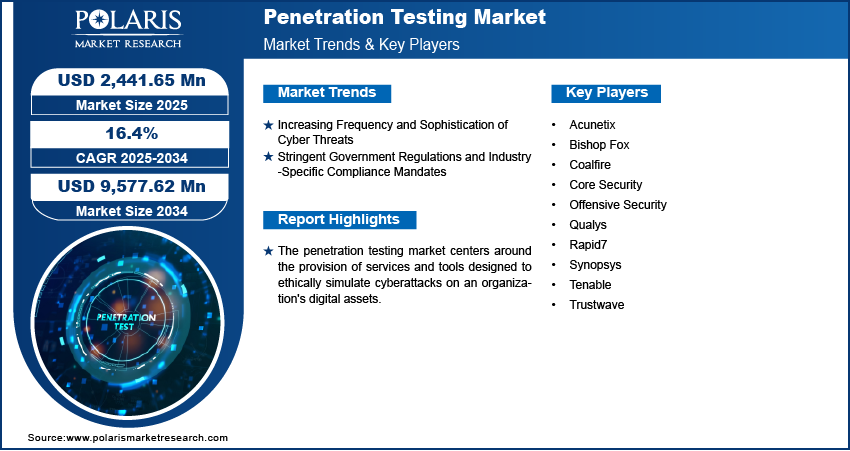

The penetration testing market size was valued at USD 2,441.65 million in 2025, growing at a CAGR of 16.4% during 2026–2034. The rising frequency and complexity of cyberattacks and the growing emphasis on regulatory compliance boost the market growth.

Market Statistics

2026 Market Size USD 2,837.20 Million

2034 Projected Market Size USD 9,577.62 Million

CAGR (2026 - 2034) 16.40%

Largest Market in 2025 North America

Key Takeaways

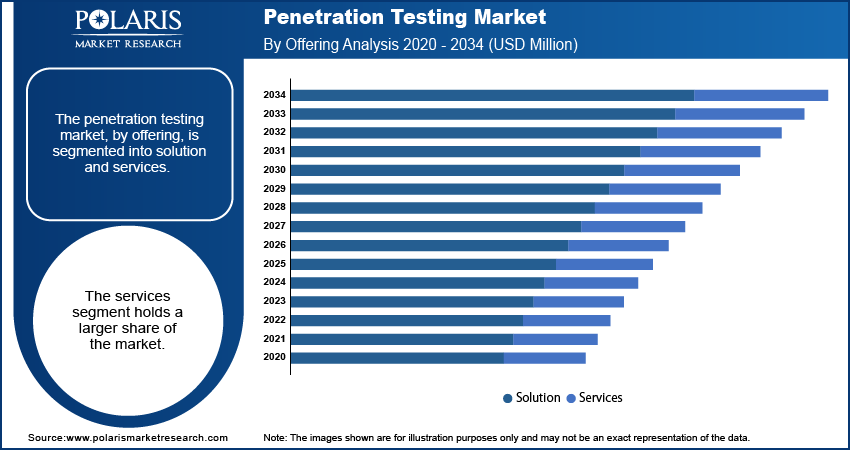

- The services segment accounts for a larger market share, primarily due to penetration testing fundamentally being a service-oriented engagement.

- The cloud segment is projected to register the highest growth rate during the projection period. Rapid adoption of cloud computing across various deployment models contributes to the segment’s growth.

- The cloud-based segment dominated the market, owing to the increasing preference of organizations for cloud-based solutions due to their inherent benefits.

- North America holds the largest market share. The robust presence of leading market participants and early adoption of cybersecurity-based practices contribute to the region’s leading market share.

- Asia Pacific is anticipated to register the highest growth rate during the projection period. The rapid expansion is primarily fueled by the rising digitalization across various nations in the region.

Industry Dynamics

- The growing complexity and frequency of cyberattacks create a need for comprehensive security assessments. It protects sensitive information and maintains operational integrity. Thus, the demand for penetration testing is growing.

- Regulatory bodies globally established stringent cybersecurity frameworks. This factor drives the need for penetration testing.

- The rapid expansion of cloud computing and widespread digital transformation initiatives across industries would create market opportunities.

- Shortage of skilled cybersecurity professionals restrains the market expansion

AI Impact on Penetration Testing Market

- Artificial intelligence is used to automate vulnerability scanning and threat detection. AI use helps reduce the time required to uncover security weaknesses.

- Machine learning adapts to evolving attack vectors. It improves the accuracy and depth of penetration testing.

- AI-powered tools simulate complex cyberattacks and provide a realistic assessment of system defenses.

- Continuous AI learning enhances testing strategies over time. As a result, it enables quicker remediation and stronger protection against emerging cybersecurity threats.

- AI-driven testing outcomes need expert validation. It is required to reduce false positives, confirm exploitability, and prioritize remediation based on business risk. Thus, there is a rising demand for hybrid models. These models combine automated penetration testing with human-led exploitation and reporting. It also supports the adoption of penetration testing as a service (PTaaS) and continuous penetration testing approaches aligned with DevSecOps.

Source: Polaris Market Research Analysis

To Understand More About this Research: Download Sample Report

Penetration testing is a controlled security assessment where approved testers simulate real-world attack techniques to identify exploitable weaknesses across networks, applications, cloud environments, and user workflows. In market sizing, penetration testing typically includes professional services and related platforms used to plan, execute, and report testing engagements; it generally excludes routine vulnerability scanning sold as standalone tools.

The penetration testing market offers services that assess the security of an organization's IT infrastructure by simulating cyberattacks. These tests identify weaknesses in networks, applications, and systems that attackers might exploit. The rise in both the number and complexity of cyber threats is pushing businesses to evaluate and improve their defenses. Additionally, stringent government regulations and industry-specific rules, like GDPR and HIPAA, require regular penetration testing to meet security standards. This growing focus on regulatory compliance propels the market growth. Vulnerability assessments list potential weaknesses. However, penetration testing assesses whether those weaknesses can be exploited in a controlled environment. It documents the real-world impact, along with remediation steps.

The growing use of cloud computing solutions and services has expanded the attack surface. It created new opportunities for exploitation. This rise in threats has increased the need for specialized cloud security and penetration testing. The high adoption of connected devices and the Bring Your Own Device (BYOD) trend in organizations increases security concerns. It boosts the demand for thorough penetration testing across different endpoints. Additionally, the rising use of technologies like artificial intelligence (AI) and deep learning in cyberattacks requires advanced penetration testing techniques to identify and address these changing threats, influencing future market trends.

Market Dynamics

Increasing Frequency and Sophistication of Cyber Threats

Organizations report a steady stream of ransomware incidents, data breaches, advanced persistent threats (APTs), and other harmful activities. These threats lead to major financial losses and damage reputations. The changing tactics of cybercriminals need proactive security measures to find and fix weaknesses before they can be exploited. For instance, a publication on the National Institutes of Health (NIH) website in 2023 highlighted the increasing complexity of cyber threats targeting healthcare systems. It stressed the need for thorough security assessments to protect sensitive patient information and ensure operational integrity. Thus, the increasing frequency and complexity of cyber threats fuel the penetration testing market. There is a rising demand for web application penetration testing and network penetration testing as organizations expand digital services, remote access, and third-party integrations.

Stringent Government Regulations and Industry-Specific Compliance Mandates

Regulatory bodies globally are creating strict cybersecurity frameworks and data protection laws. Examples include the European Union's General Data Protection Regulation (GDPR) and the United States' Health Insurance Portability and Accountability Act (HIPAA). These regulations often require or strongly suggest that organizations perform regular security assessments, including penetration testing, to show compliance and protect sensitive data. For instance, the Cybersecurity and Infrastructure Security Agency (CISA) issued guidelines in 2024. These guidelines highlight the importance of proactive testing and vulnerability assessments for critical infrastructure to ensure resilience against cyber threats. Hence, the implementation and enforcement of stringent government regulations and industry-specific compliance mandates propel the penetration testing market demand. In practice, compliance-driven testing is frequently tied to audit readiness and control validation, especially in regulated verticals such as BFSI and healthcare, where periodic penetration testing supports evidence requirements and reduces breach exposure.

Expansion of Cloud Computing and Digital Transformation Initiatives

As organizations increasingly migrate their operations, data, and applications to the cloud, the attack surface expands, introducing new and complex security challenges. Ensuring the security of cloud environments is crucial. Therefore, the need for specialized cloud penetration testing services is rising. Additionally, broader efforts in digital transformation require thorough security assessments. They help identify and address potential weaknesses introduced by the transformation. A research article published on PubMed in 2022 discussed the security issues of cloud adoption in healthcare and emphasized the vital role of penetration testing in finding cloud-specific vulnerabilities. Cloud-native architectures increase reliance on APIs, identity systems, and misconfiguration controls. It raises the demand for cloud security testing and API penetration testing. The testing is used to identify various issues such as privilege escalation, data exposure, and lateral movement pathways. Thus, the rapid growth of cloud computing and widespread digital transformation initiatives across various industries would create significant market opportunities during the forecast period.

Source: Polaris Market Research Analysis

Segment Insights

Market Assessment – By Offering

The market, by offering, is bifurcated into solution and services. The services segment holds a larger share. Penetration testing is fundamentally a service-oriented engagement. Organizations rely on specialized expertise to conduct complex security assessments. The testing requires skilled professionals to simulate attacks, analyze findings, and provide actionable recommendations for remediation. Tailored testing methodologies are based on specific infrastructure and application environments. The rising shift toward customized services reinforces the preference for penetration testing as a service over standalone solutions. This reliance on expert-driven engagements ensures comprehensive vulnerability identification. It contributes to the dominant share of the services segment. Service engagements are often purchased with defined deliverables such as executive summary, technical findings, proof-of-concept exploits where permitted, prioritized remediation guidance, and optional retesting. It further reinforces the service-led nature of the market.

The solution segment is anticipated to exhibit a higher growth rate during the forecast period. Increasing development and adoption of automated penetration testing tools and platforms drive the growth. These solutions provide benefits like scalability and efficiency. They can also conduct more frequent assessments. While they do not completely replace human expertise, these tools are getting better at identifying common vulnerabilities and simplifying the early stages of testing. The ongoing improvements in AI and machine learning boost the abilities of these solutions. These technologies facilitate more thorough and smart vulnerability scanning. The increasing use of automated tools and platforms is expected to drive the highest growth rate in this solution segment.

Market Evaluation– By Application

The market, by application, is segmented into web applications, mobile applications, network infrastructure, social engineering, cloud, and others. The web applications segment held the largest share in 2025. The ubiquitous nature of web applications in modern business operations propels the segment dominance. Companies in all sectors rely on web applications for customer interaction, internal processes, and essential functions. Protecting these applications from potential threats is a major concern. This has increased the demand for web application penetration testing services and solutions. The ongoing development of web technologies, along with the growing complexity of web applications, reinforces the segment's dominance. APIs power web and mobile experiences and often result in authorization and data leakage issues. Thus, Companies are also increasing their investments in API penetration testing.

The cloud segment is projected to experience the highest growth rate during the forecast period. The growing use of cloud computing in public, private, and hybrid models is driving fast growth. Organizations are shifting their data, applications, and infrastructure to the cloud. It is crucial to ensure the security of these environments. The security challenges related to cloud environments, along with the larger attack surface, increase the need for specialized cloud penetration testing services and solutions. This growing concern for protecting cloud assets fuels growth in the cloud segment. Other applications increasingly include OT/IoT environments, where testing is performed under strict safety constraints and change-control requirements.

Market Assessment – By Deployment Mode

By deployment mode, the penetration testing market is segmented into cloud-based and on-premises. The cloud-based segment holds a larger share. This rising preference for cloud-based solutions is attributed to their advantages such as scalability, flexibility, and cost-effectiveness. The simplicity of using and overseeing cloud-based penetration testing services and platforms aligns with the evolving IT infrastructure. Many organizations are either moving to or have already adopted cloud environments. This widespread acceptance, along with the benefits of cloud deployments, plays a significant role in the segment's dominance. Cloud-based delivery also supports managed penetration testing services, which simplify scheduling, evidence capture, reporting workflows, and retest cycles. This makes it easier for organizations to treat testing as an ongoing program instead of a one-time project.

The cloud-based deployment mode is also anticipated to experience a higher growth rate during the forecast period. Ongoing migration of businesses toward cloud infrastructures and the increasing demand for security solutions tailored to these environments fuel the segment growth. Organizations use cloud services for many important operations. Therefore, the demand for penetration testing solutions will increase because these solutions can effectively evaluate the security of their cloud assets. The flexibility and scalability of cloud-based penetration testing solutions make them an appealing choice for organizations that want to protect their changing cloud environments. Due to these factors, the segment is expected to witness the highest growth.

Market Assessment – By Vertical

The market, by vertical, is segmented into banking & financial services & insurance, healthcare, IT and ITes, telecom, retail & ecommerce, manufacturing, education, and others. The banking & financial services & insurance (BFSI) segment holds the largest share. This significant share comes from the strict rules in the BFSI sector. It also relies on the sensitive financial and personal data it manages. The strict compliance rules and serious consequences of security breaches require regular and thorough penetration testing. The testing helps protect important assets and maintain customer trust. This ongoing need for security evaluations makes the BFSI sector the leading industry. Regulatory scrutiny, digital banking growth, and third-party integration risk boost the BFSI segment growth. It increases the demand for network penetration testing and application penetration testing.

The healthcare segment is anticipated to experience the highest growth rate during the forecast period. The digitalization of healthcare records and the rise of connected medical devices boost the segment growth. Also, the growing threat of cyberattacks on patient data is driving growth. Owing to the sensitive nature of healthcare information and strict regulations, including laws like HIPAA, organizations emphasize healthcare cybersecurity. This rising emphasis on protecting patient data and securing healthcare systems propel the demand for penetration testing. These factors contribute to the segment growth.

Source: Polaris Market Research Analysis

Regional Analysis

North America holds the largest share of the penetration testing market. The early adoption of cybersecurity practices and the presence of leading companies support this dominance. Strict regulations in different industries also play a role. High awareness of potential cyber threats and significant investments in cybersecurity infrastructure boost the demand for penetration testing services and solutions. The existence of a developed and competitive market with numerous service providers and solution vendors strengthens North America's leading position. In the U.S. and Canada, penetration testing adoption is supported by mature enterprise security programs and a strong ecosystem of specialized service providers and tool vendors.

The Asia Pacific market is anticipated to exhibit the highest growth rate during the forecast period. The growth is driven by the accelerating pace of digitalization across various economies in the region. Also, growing awareness of the escalating cyber threat landscape fuel the expansion. Increasing investments in IT services and the proliferation of online businesses are a few growth drivers. Supportive government initiatives toward cybersecurity fuels the demand for penetration testing services and solutions across the region. Businesses in this region increasingly recognize the importance of proactive security measures. Thus, the Asia Pacific market is poised to become a major contributor to the global market.

.webp)

Source: Polaris Market Research Analysis

Key Players and Competitive Insights

A few of the major market players include Acunetix (Invicti Security), Rapid7, Qualys, Tenable, Core Security (HelpSystems), Synopsys, Trustwave (Singtel), Coalfire, Bishop Fox, and Offensive Security. These organizations offer a range of services and solutions designed to identify and mitigate security vulnerabilities in IT infrastructures, web applications, mobile applications, and cloud environments. They cater to the growing demand for proactive cybersecurity measures across various industries.

The competitive landscape is characterized by a mix of established cybersecurity vendors and specialized penetration testing service providers. Competition is driven by factors such as the breadth and depth of service offerings, technological innovation in testing methodologies and tools, the expertise of security professionals, and the ability to address evolving security threats and compliance requirements. Market insights reveal a trend toward the integration of penetration testing with other security assessment tools and the increasing adoption of continuous testing approaches. Organizations are also seeking providers with specific industry expertise and the ability to deliver actionable remediation guidance, fostering a dynamic and competitive environment within the market.

Competitively, providers are increasingly differentiating as (1) tool-led platforms (automation and workflow), (2) service-led specialists (deep exploitation expertise), and (3) PTaaS models combining both. Buyers are prioritizing vendors that can demonstrate industry-specific expertise, clear rules-of-engagement, high-quality reporting, and structured retesting.

Buyer Checklist

| Buyer Dimension | Key Focus | What Buyers Must Evaluate? |

| Lifecycle | Adoption & usage journey | Risk assessment → scope definition → vendor RFP → pilot → testing → remediation → retesting → continuous security cycle |

| Vendor Checklist | Capability & delivery quality | Certifications (OSCP, CEH, CREST), standards alignment (OWASP, PTES, NIST), domain expertise, reporting quality, post-test support, data protection |

| Pricing Drivers | Cost influencers | Number of assets, test type (black/gray/white box), complexity, depth of exploitation, tester skill, retesting needs, reporting detail |

| Compliance Mapping | Regulatory alignment | PCI DSS (annual tests), ISO 27001 (risk controls), HIPAA (technical safeguards), GDPR (DPIA support), NIST 800-53/171, local cybersecurity mandates |

| Metrics & KPIs | Performance tracking | Mean time to remediate, critical findings count, coverage % vs scope, false positives, repeat vulnerabilities, risk reduction per cycle |

Source: Polaris Market Research Analysis

List of Key Companies

- Acunetix

- Bishop Fox

- Coalfire

- Core Security

- Offensive Security

- Qualys

- Rapid7

- Synopsys

- Tenable

- Trustwave

Industry Developments

February 2026: Palo Alto Networks completed the CyberArk deal to improve identity checks in zero-trust projects.

February 2026: Bishop Fox launched Cosmos AI, an AI-based app testing tool that reduces assessment time by 40%.

July 2025: Trustwave introduced its advanced Operational Technology (OT) services portfolio. The company stated that the portfolio will enable companies in defending industrial operations and critical infrastructure against cyber threats. OT Security & Architecture Design, Penetration Testing an OT Environment, and Threat Intelligence Integration are key services in the portfolio.

April 2025: RySec LLC officially launched its cybersecurity consulting division. It will provide enterprise-level penetration testing at transparent and competitive rates.

Market Segmentation

By Offering Outlook (Revenue – USD Million, 2021–2034)

- Solution

- Services

By Application Outlook (Revenue – USD Million, 2021–2034)

- Web Applications

- Mobile Applications

- Network Infrastructure

- Social Engineering

- Cloud

- Others

By Deployment Mode Outlook (Revenue – USD Million, 2021–2034)

- Cloud-Based

- On-Premises

By Vertical Outlook (Revenue – USD Million, 2021–2034)

- Banking & Financial Services & Insurance

- Healthcare

- IT and ITeS

- Telecom

- Retail & Ecommerce

- Manufacturing

- Education

- Others

By Regional Outlook (Revenue – USD Million, 2021–2034)

- North America

- U.S.

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- Suth Korea

- Indnesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- Suth Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Penetration Testing Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 2,441.65 million |

| Market Size in 2026 | USD 2,837.20 million |

| Revenue Forecast in 2034 | USD 9,577.62 million |

| CAGR | 16.4% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2022–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD million, 2021–2034 and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Why Organizations Must Purchase the Report?

Workflow/Innovation Strategy: The penetration testing market has been segmented into detailed segments of offering, application, deployment mode, and vertical. Moreover, the study provides the reader with a detailed understanding of the different segments at both the global and regional levels.

Market Entry Strategies: Growth strategies increasingly focus on expanding service portfolios to tackle new security areas like cloud environments, IoT devices, and operational technology (OT). Providers stress the importance of integrating AI and automation. These technologies improve the efficiency and scalability of their testing services. Marketing efforts highlight the proactive risk reduction benefits of penetration testing. Companies also stress compliance and the prevention of expensive data breaches. Strategic partnerships with managed service providers and technology vendors are vital for growing market reach. Additionally, educating organizations about the changing threat landscape and the need for regular, thorough security assessments is a key marketing push to boost market demand.

Penetration Testing Market FAQ's

The market is projected to reach USD 9,577.62 million by 2034. It is expected to register a CAGR of 16.4% from 2026 to 2034.

North America dominated the market in 2025. Stringent regulations and high cybersecurity adoption rates among enterprises propelled the dominance.

Rising cyber threats and strict compliance regulations (GDPR, HIPAA, PCI DSS) drive the market growth. In addition, cloud computing expansion and increasing adoption of automated testing solutions fuel the growth.

The BFSI (Banking, Financial Services, and Insurance) segment leads penetration testing adoption. It is due to handling of highly sensitive financial data in the industry. Also, stringent regulatory compliance requirements boost the dominance.

Emerging trends are Penetration Testing as a Service (PTaaS), AI-powered automation, and cloud-native testing. DevSecOps integration and remote security assessments are also key trends.

Penetration testing actively exploits system vulnerabilities by simulating real cyberattacks. In contrast, vulnerability assessment identifies and lists security weaknesses without trying to exploit them or simulate a breach. Integration of Automation and AI: The market is witnessing a rise in the use of automated tools and AI to enhance the efficiency, speed, and coverage of penetration testing processes. ? Growing Importance of Continuous Testing: Organizations are moving toward more frequent or continuous penetration testing to keep pace with the evolving threat landscape and ensure the ongoing security posture.

Organizations should conduct penetration testing annually at minimum. It must be conducted quarterly for high-risk sectors. Penetration testing must be done after significant infrastructure changes, new deployments, or for regulatory requirements.

Penetration testing reports include identified vulnerabilities, exploited weaknesses, and risk severity ratings. Attack methodologies used, remediation recommendations, and detailed executive summaries for stakeholders are also included.

Testing scope, system complexity, infrastructure size, and testing type can affect the pricing. In addition, frequency, compliance requirements, and tester expertise also influence penetration testing costs.

PTaaS provides subscription-based, ongoing security testing with on-demand access. It also includes automated workflows and real-time reporting, unlike traditional one-time, project-based penetration testing.

PCI DSS, HIPAA, GDPR, SOC 2, ISO 27001, GLBA (Gramm-Leach-Bliley Act), and SOX (Sarbanes-Oxley) often mandate or suggest regular penetration testing.

Page last updated on:

Download Sample Report of Penetration Testing Market

Please fill out the form to request a customized copy of the research report.