Point of Care Diagnostics Market Overview, Global Size | 2026-2034

REPORT DETAILS

Point of Care (PoC) Diagnostics Market Summary

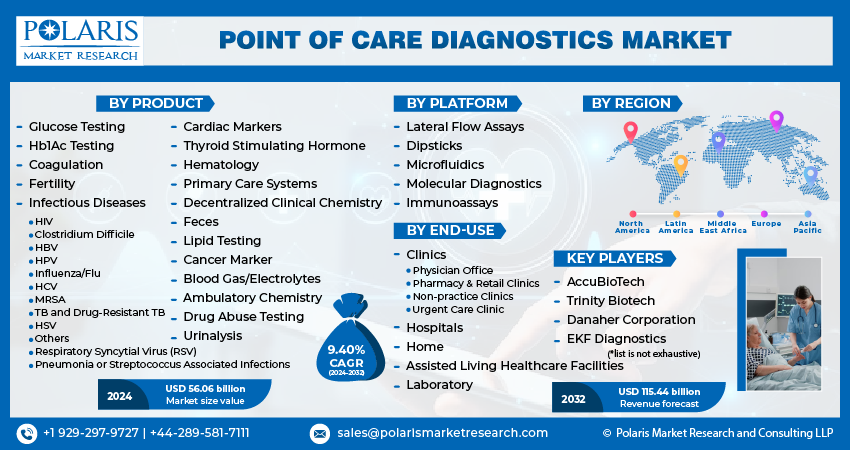

The global point of care (PoC) diagnostics market size was valued at USD 60.99 billion in 2025, growing at a CAGR of 9.40% from 2026–2034. Key factors driving demand include rising demand for rapid and accurate testing solutions, government and institutional investments, growing prevalence of chronic and infectious diseases, and rising advancement in PoC technology.

Market Statistics

Key Takeaways

- North America dominated with 42.6% share of the global market in 2025, owing to its technologically advanced healthcare infrastructure and extensive availability of devices.

- Asia Pacific is estimated to experience a 10.1% CAGR, boosted by improvements in health care facilities and the growing need for cost-effective testing products.

- The infectious disease segment held a share of 33.3% of revenue in 2025. It is due to the urgent need for rapid detection of infectious agents.

- OTC is expected to be the fastest-growing segment with 9.9% CAGR in the coming years. The segment is driven by increasing consumer preference for home-use tests for parameters like glucose and pregnancy.

- Clinics held a 35.9% share of the market in 2025. Clinics play an important role in offering quick access to diagnosis to the patient.

Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations

Industry Dynamics

- The growing global incidence of disease is driving demand for timely, accessible diagnostics that enable treatment decisions at the point-of-care.

- Ongoing advances in technology are improving the accuracy, usability, and efficiency of point-of-care diagnostic devices for an expanding range of applications.

- Government regulations present significant obstacles that delay product approval and market access, increasing overall development costs and delaying the launch of new tests.

- The growth opportunity in decentralized environments, such as pharmacies and homes, is driven by patient demand for accessible, patient-managed care.

AI Impact on Point of Care (PoC) Diagnostics Market

- AI algorithms are able to analyze complex data patterns, improving accuracy and reducing the potential for human error, and supporting reliable and accurate test results.

- AI discover trends in patients’ longitudinal data to facilitate earlier identification of disease and to shift the paradigm of care away from treatment and towards prevention and monitoring that is personalized to patients.

- AI also enables the automation of data entry, inventory management of devices, and streamlined integration of results into electronic health records, freeing up important clinical workflows and reducing administrative burden.

- AI is able to power decision support tools that guide non-specialists through testing and diagnosis in remote, or typically underserved, areas to allow for equitable access to quality high-level patient care.

What Does the Current Market Landscape Look for Point of Care Diagnostics?

Point-of-Care (PoC) diagnostics are defined as medical testing conducted at or near the site of patient care, allowing immediate availability of results to support timely clinical decision making. There is an increasing demand for rapid and accurate testing solutions, which is driving the growth opportunities. Traditional lab testing has long processing times, which delay timely diagnosis and treatment. At the same time, PoC enables healthcare providers to get reliable results within minutes, thereby facilitating faster clinical decisions and producing better patient outcomes. For instance, in May 2024, Roche received an FDA clearance for the US-authorized HPV self-collection tests. This test's screening will benefit from an increase in early detection of cervical cancer risk by improving access for more patients. Time to receipt of results is required in the emergency and primary care environments, as immediate intervention is essential. PoC testing also helps decentralize test capacity and minimize delayed analytical lab results for the centralized laboratories.

Core Point of Care Diagnostic Technologies

Rapid Test Kits: Easy-to-use disposable kits that enable rapid testing. These kits find extensive application in pregnancy tests, infection detection, and routine medical checkups.

Molecular Point-of-Care Diagnostics: Point-of-care devices that enable the identification and measurement of genetic materials of pathogens. Such devices are used to detect bacteria and viruses and provide faster results than conventional methods.

Biosensors: Devices that utilize sensors to analyze biomolecules such as glucose or oxygen levels or the presence of certain proteins in the body. They enable instant or continuous monitoring.

Home Healthcare Testing: Convenient and user-friendly devices that enable patient monitoring from home locations. Such devices enable chronic disease management, increase convenience, and decrease hospitalization rates.

AI-Based Diagnostics: Use of artificial intelligence technology enables quick analysis of results, reduces the margin for errors, and improves diagnosis speed. It also assists in recognizing the criticality of the issue and its priority

Source: Polaris Market Research Analysis Diagnostics Market.png)

The increase in government and institutional investment in healthcare infrastructure and access is also contributing to the growth of the market. Health care agencies and healthcare institutions are encouraging the use of PoC technologies to reach more individuals for diagnostic purposes, especially in underserved or remote areas where full-scale laboratory facilities do not exist. For example, in February 2024, HemoCue collaborated with Novo Nordisk to deploy more than 400 HbA1c point-of-care systems across 30 low- and middle-income country clinics to enhance type 1 diabetes testing for children. This type of adoption further integrates refined diagnostic products into day-to-day routine care. Additionally, it assists in research to innovate different PoC technologies to improve their accuracy, portability, and affordability. Therefore, by providing support, funding, and methods to facilitate authorization, governments and institutions boost the expanded adoption of PoC diagnostics across various healthcare settings.

Drivers & Opportunities

What are the Factors Driving the Industry?

Growing Prevalence of Chronic and Infectious Diseases: The increased incidence of chronic and infectious diseases is driving growth opportunities as it coordinates with the growing need for timely, reliable, and reachable testing. According to CDC data from December 2024, there were 10.2 million physician office visits in the U.S. for various infectious and parasitic diseases. Chronic diseases, such as diabetes, cardiovascular disease, and respiratory infections, require continuous monitoring and early diagnosis in order to prevent complications and provide effective treatment. PoC diagnostics enable tests to be conducted at the patient's location, reducing the need for centralized laboratories and decreasing the time needed to initiate therapy. The speed of the PoC results allows for better disease management, encourages preventative measures, and provides positive patient outcomes, which is why there is an increased focus on PoC solutions in many modern healthcare systems.

Rising Advancement in PoC Technology: Continuous advancements in PoC technology support the market by enhancing accuracy, efficiency, and increasing user-friendliness across different diagnostic applications. Advances such as miniaturized biosensors, microfluidics, and digital connectivity have turned PoC devices into robust solutions for complicated diagnostic needs. For example, in June 2025, NOUL, a leader in blood testing technology, partnered with Nihon Kohden, a manufacturer of medical devices, to distribute the miLab BCM automated blood testing system in Mexico, with the goal of increasing diagnostic efficiency in the healthcare system. These advancements provide speed and precision to test outcomes and allow for integration with electronic health record and telehealth platforms, creating valuable components in both commercial, clinical, and remote care options. Furthermore, the intersection of novel technology and patient-focused simplicity allows point-of-care diagnostics to emerge as important instruments for empowering personalized healthcare and improve diagnostic capacity globally.

Source: Polaris Market Research Analysis

Segmental Insights

Product Analysis

Which Segment by Product Held the Largest Share?

Based on product, the segmentation includes glucose testing, Hb1Ac testing, coagulation, fertility, infectious diseases, cardiac markers, thyroid stimulating hormone, hematology, primary care systems, decentralized clinical chemistry, feces, lipid testing, cancer marker, blood gas/electrolytes, ambulatory chemistry, drug abuse testing, and urinalysis. The infectious diseases segment accounted largest revenue share in 2025 primarily due to the need to quickly and accurately identify communicable diseases. Its dominant share is driven by the ability to receive timely results necessary to control disease spread and initiate immediate treatment. The increase in need for point-of-care infectious disease testing is further supported by the growth in demand for decentralized testing approaches, especially in settings such as primary care and in emergencies.

The ambulatory chemistry segment is expected to witness robust growth during the forecast period driven by the growing demand for portable and operator-friendly diagnostic devices that will drive future growth in the market. This growth is further driven by the focus on patient experience and improved patient care with frequent monitoring of chronic disease utilized as point-of-care diagnostics in outpatient and non-hospital environments.

Glucose Monitoring vs Infectious Disease vs Cardiometabolic vs Pregnancy Tests

| Test Type | Principal Application | Common Setting | Main Advantage |

| Glucose Monitoring | Diabetes testing | Homes, hospitals | Constant monitoring |

| Infectious Disease Testing | Diagnosis of infection | Hospitals, drugstores, homes | Rapid detection |

| Cardiometabolic Testing | Markers related to heart | Emergency rooms, clinics | Rapid response |

| Pregnancy Tests | Testing for pregnancy hormones | Homesteads, clinics | Rapid detection |

Source: Polaris Market Research Analysis

Mode of Prescription Analysis

Why OTC Segment is Expected to Witness the Fastest Growth?

In terms of mode of prescription, the segmentation includes OTC and prescription-based. The OTC segment is expected to witness fastest growth at a CAGR of 9.9% during the forecast period as the consumer demand for self-test kits continues to grow for glucose monitoring, pregnancy testing, and infectious disease diagnostics. The rise in OTC diagnostics is a direct result of the rising focus on personal health management, convenience, privacy, and advancements in technology, leading to increased reliability and accuracy of OTC diagnostics. Moreover, patients can easily purchase these diagnostics without a physician's prescription, which allows OTC diagnostics to grow at a rapid pace across a wide range of consumer samples.

End Use Analysis

Which Segment by End Use Contributed to the Growth Opportunities?

Based on end use, the segmentation includes, clinics, hospitals, home, assisted living healthcare facilities, and laboratory. The clinics segment held 35.9% share of the market in 2025 as they have contributed to access and timeliness of patient care. Clinics often act as the first access point for the patient, and the integration of PoC testing at the staff level within a clinic enables more efficient diagnosis and clinical decision-making at the time of the appointment. The growing focus on outpatient care and alleviating healthcare from the overburden of hospitals has contributed to the adoption of PoC in clinics. Furthermore, the extensive application of PoC diagnostics, enabling tests for several health conditions, facilitates improved turnaround times and overall treatment efficiency for patients in clinics.

Source: Polaris Market Research Analysis Diagnostics Market Seg.png)

Regional Analysis

What are the Factors for Regional Expansion?

North America point of care (PoC) diagnostics market accounted for 42.6% of global market share in 2025. This dominance is attributed to the advanced healthcare system focused on technology adoption, advantageous accessibility of diagnostic devices in hospitals, clinics, and home care environments for early disease detection and patient management. High levels of awareness on the benefits of rapid testing amongst patients and health care providers, as well as a track record of substantial investment in research, innovation, and integration of digital health solutions, are contributing to substantial growth in PoC diagnostics in North America.

U.S. Point of Care (PoC) Diagnostics Market Insight

U.S. held 81.15% market share in North America point of care (PoC) diagnostics landscape in 2025 as a result of its developed healthcare system and capitalizing on the adoption of innovative diagnostic technologies. The integration of PoC devices into various hospitals and home care environments for preventive healthcare has made these devices popular. Furthermore, the commitment to research and development with the expansion of digital health platforms has strengthened the U.S. PoC diagnostics market.

Asia Pacific Point of Care (PoC) Diagnostics Market

The market in Asia Pacific is projected to grow fastest from 2026-2034, as healthcare access improves, and the demand for cheap testing options rises. The rising burden of chronic and communicable diseases boosts the demand for quick and innovative diagnostic opportunities, as many places in Asia lack the healthcare delivery mechanisms for treatment in both urban and rural areas. According to a June 2025 Asian Development Bank (ADB) report, over 20 countries in Asia face a 20% or greater risk of premature death from chronic diseases. The increasing shift towards portable diagnostic testing and technologies that are optimized for resource-limited environments will expand the diagnostic sector. Moreover, the growth in healthcare awareness and improvements in healthcare investments point to the fact that the region will continue to increase its PoC options to deliver effective, quick healthcare responses.

Japan Point of Care (PoC) Diagnostics Market Overview

The market in Japan is expanding due to managing the healthcare needs of its aging population and the increasing rate of chronic disease. The country has witnessed the rapid adoption of PoC testing devices that support patient management and prevent unnecessary hospital visits. Additionally, Japan's focus on innovation and the production of quality diagnostic solutions drives the consistent growth of the PoC diagnostics market.

Europe Point of Care (PoC) Diagnostics Market

The point of care (PoC) diagnostics landscape in Europe is projected to hold a substantial share in 2034 due to its established health care systems and focus on quality patient outcomes. The rising focus on decentralizing service delivery and reducing burdens on hospitals has supported the rapid growth of PoC diagnostic testing in clinical locations and in the community environment. Regulatory frameworks in Europe favour innovation for PoC diagnostic solutions, along with the development of new diagnostics to manage the growing burden of chronic disease. Additionally, the rise in access to health care services, combined with the support of technological innovation, will continue to affect the advantage of having a strong PoC diagnostics market in Europe.

UK Point of Care (PoC) Diagnostics Market

The UK market is driven by a continuing shift toward decentralized healthcare delivery and the need to reduce the burden on centralized laboratories. Point-of-care testing solutions are being widely integrated to support primary care practices, community clinics, and home care to create faster pathways to diagnosis and treatment. In addition, supportive healthcare policies and the adoption of advanced diagnostic technologies further improve the role of PoC diagnostics as a mode to improve accessibility and efficiency in the UK's overall healthcare system.

Source: Polaris Market Research Analysis Diagnostics Market Reg.png)

Key Players & Competitive Analysis Report

The point of care (PoC) diagnostics market is competitive and changing quickly. This change comes from advancements in technology and actions by both established companies and new players. Vendors are investing in research and development (R&D) to create fast, connected devices, which offers a good chance for revenue. A major trend is the shift toward decentralized testing, which is growing in emerging markets and new areas, like home-based care. Competitor intelligence has shown that success relies on sourcing, economic influences, supply disruptions, and geopolitical changes that affect production and access to markets. The future of industry ecosystems would be differentiated by partnerships that support sustainable value chains and capitalize on growth opportunities in untapped regions.

Major companies operating in the point of care (PoC) diagnostics industry include Abbott, BD, bioMérieux, Danaher Corporation, EKF Diagnostics Holdings plc, F. Hoffmann-La Roche Ltd, Quest Diagnostics Incorporated, QuidelOrtho Corporation, Siemens Healthcare Private Limited, and Thermo Fisher Scientific Inc.

Key Players

- Abbott

- BD

- bioMérieux

- Danaher Corporation

- EKF Diagnostics Holdings plc

- F. Hoffmann-La Roche Ltd

- Quest Diagnostics Incorporated

- QuidelOrtho Corporation

- Siemens Healthcare Private Limited

- Thermo Fisher Scientific Inc

Industry Developments

- March 2026: Abbott announced the completion of the acquisition of Exact Sciences. The company stated that the acquisition will help establish it as a leader in the cancer screening and diagnostics segment. It will also enable Abbott to serve millions of additional people. (source: abbott.com)

- November 2025: Sapphiros revealed a strategic agreement with Roche. According to Sapphiros, the agreement will provide Roche with access to 1 billion lateral flow tests and future molecular POC platforms. (source: sapphiros.com)

- June 2025: Philips launched the portable Flash Ultrasound System 5100 POC. Designed for ER and ICU use, it offers high-quality imaging and automated workflows to support rapid decision-making for clinicians across anesthesia, critical care, and emergency medicine. (Source: philips.com)

- August 2024: AcouSort and Werfen collaborated to integrate acoustofluidics technology into Werfen's GEM Premier 7000 system, enabling hemolysis detection for point-of-care blood gas analysis. (Source: acousort.com)

Future of POC Diagnostics Market

The market for point of care diagnostics has been forecast to experience growth owing to the incorporation of artificial intelligence (AI), wearable diagnostic devices, and increased need for self-testing at home. There will be more deployment of decentralized healthcare models in underdeveloped and distant regions. Improved technologies for biosensors, internet connectivity, and molecular tests have also been forecasted to spur growth in this market. Growing interest in preventive healthcare, along with real-time health monitoring, is expected to play an important role in driving market development.

Point of Care (PoC) Diagnostics Market Segmentation

By Product Outlook (Revenue, USD Billion, 2021–2034)

- Glucose Testing

- Hb1Ac Testing

- Coagulation

- Fertility

- Infectious Diseases

- HIV

- Clostridium Difficile

- HBV

- Pneumonia or Streptococcus Associated Infections

- Respiratory Syncytial Virus (RSV)

- HPV

- Influenza/Flu

- HCV

- MRSA

- TB and Drug-Resistant TB

- HSV

- Others

- Cardiac Markers

- Thyroid Stimulating Hormone

- Hematology

- Primary Care Systems

- Decentralized Clinical Chemistry

- Feces

- Lipid Testing

- Cancer Marker

- Blood Gas/Electrolytes

- Ambulatory Chemistry

- Drug Abuse Testing

- Urinalysis

By Mode of Prescription (Revenue, USD Billion, 2021–2034)

- OTC

- Prescription-based

By End Use Outlook (Revenue, USD Billion, 2021–2034)

- Clinics

- Physician Office

- Pharmacy & Retail Clinics

- Non-practice Clinics

- Urgent Care Clinic

- Hospitals

- Home

- Assisted Living Healthcare Facilities

- Laboratory

By Regional Outlook (Revenue, USD Billion, 2021–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Point of Care (PoC) Diagnostics Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 60.99 Billion |

| Market Size in 2026 | USD 66.50 Billion |

| Revenue Forecast by 2034 | USD 136.90 Billion |

| CAGR | 9.40% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Point of Care Diagnostics Market FAQ's

The global market size was valued at USD 60.99 billion in 2025 and is projected to grow to USD 136.90 billion by 2034.

The global market is projected to register a CAGR of 9.40% during the forecast period.

North America point of care (PoC) diagnostics market accounted for 42.60% of global market share in 2025.

A few of the key players in the market are Abbott, BD, bioMérieux, Danaher Corporation, EKF Diagnostics Holdings plc, F. Hoffmann-La Roche Ltd, Quest Diagnostics Incorporated, QuidelOrtho Corporation, Siemens Healthcare Private Limited, and Thermo Fisher Scientific Inc.

The infectious diseases segment accounted for 33.33% revenue share in 2025.

The OTC segment is expected to witness fastest growth at a CAGR of 9.9% during the forecast period.

Download Sample Report of Point of Care Diagnostics Market

Please fill out the form to request a customized copy of the research report.