Robotic Radiotherapy Market Landscape, Company Dynamics, and Future Projections, 2025-2034

REPORT DETAILS

REPORT DETAILS

Robotic Radiotherapy Market Summary

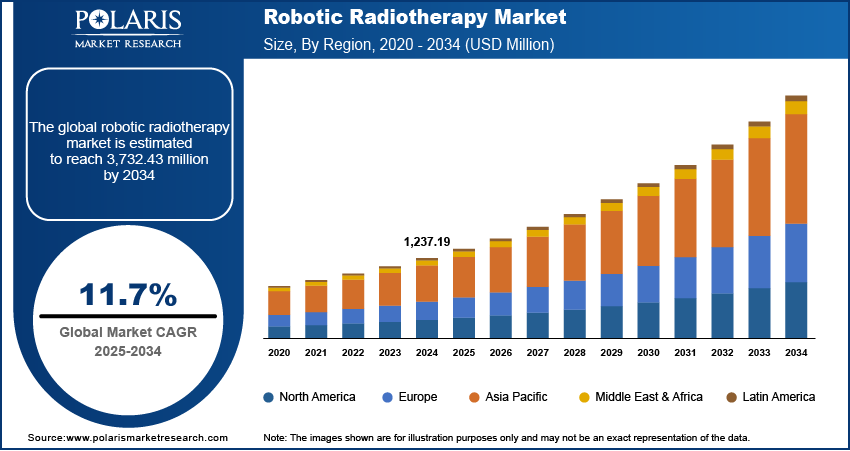

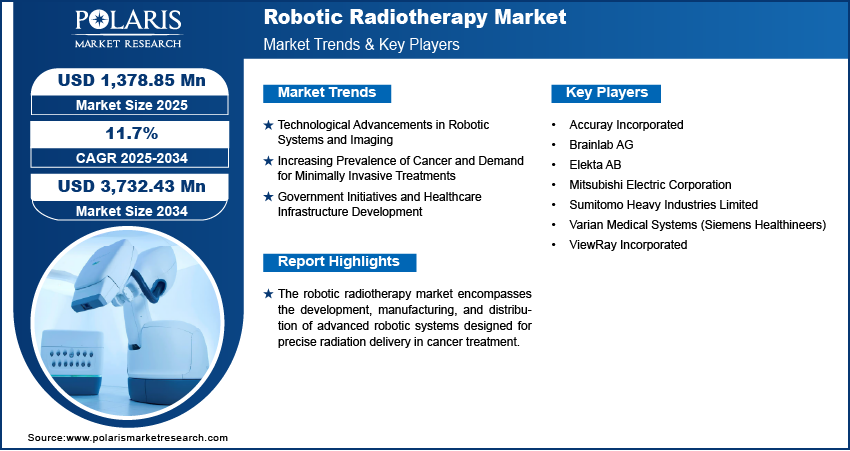

The robotic radiotherapy market size was valued at USD 1,237.19 million in 2024, exhibiting a CAGR of 11.7% during 2025–2034.

Market Statistics

Key Takeaways

- Radiotherapy systems hold the largest share due to their essential role in precise radiation delivery and treatment plan execution.

- Linear accelerators dominate the technology market, valued for versatility and precise radiation dose management.

- The prostate cancer segment grows as precision treatment advances improve patient outcomes and reduce side effects.

- Independent radiotherapy centers expand quickly, offering specialized, accessible, and cost-effective outpatient treatment options.

- North America leads regionally with advanced healthcare, high technology adoption, and strong research investments.

- Asia Pacific shows the highest growth, driven by rising cancer cases, improved healthcare access, and government investments.

Rising global cancer prevalence, continuous advancements in robotic and imaging technologies, increasing demand for minimally invasive treatments, and strong government initiatives are driving the market growth.

Industry Dynamics

- Increasing global cancer prevalence drives demand for precise, effective robotic radiotherapy treatments and expands the potential patient base rapidly.

- Advances in robotic technology and real-time imaging enhance treatment accuracy and reduce damage to healthy tissues, boosting adoption rates.

- Growing integration of AI and ML enables adaptive, personalized treatment planning, improving therapy outcomes and operational efficiency.

- Rising geriatric population increases the need for minimally invasive, precise cancer treatments suitable for older patients with comorbidities.

- Expanding government funding and infrastructure development improve accessibility to advanced robotic radiotherapy in emerging and developed markets.

- Rising patient awareness of robotic radiotherapy benefits, such as fewer side effects and faster recovery, encourages wider acceptance and use.

- High costs and complexity of robotic radiotherapy systems limit accessibility and slow adoption in lower-income or resource-limited healthcare settings.

To Understand More About this Research: Download Sample Report

The robotic radiotherapy market encompasses the segment of healthcare technology focused on the application of robotic systems for the precise delivery of radiation oncology therapy to cancerous tumors. This specialized field aims to enhance treatment accuracy, minimize damage to surrounding healthy tissues, and improve patient outcomes through the integration of advanced robotics with radiation delivery platforms. Key market drivers include the increasing prevalence of cancer globally, which is escalating the overall market demand. Furthermore, advancements in robotic technology and the growing emphasis on minimally invasive surgery and treatment options are significantly impacting the market dynamics. The ability of robotic systems to offer superior precision and real-time imaging during treatment is a crucial market growth factor, driving adoption by healthcare providers seeking to improve patient care and treatment efficacy.

Analyzing the market outlook, the integration of Artificial Intelligence (AI) and Machine Learning (ML) into robotic radiotherapy systems presents a substantial market potential. These technologies enable adaptive treatment planning and real-time adjustments, further optimizing radiation delivery. The growing geriatric population, which is more susceptible to cancer, is also contributing to the expanding market size. Additionally, the rising awareness of the benefits associated with robotic radiotherapy, such as reduced side effects and shorter recovery times, is fostering increased market penetration. Understanding these market trends is crucial for stakeholders conducting market entry assessments and developing strategic plans to capitalize on the evolving healthcare landscape.

Market Dynamics:

Technological Advancements in Robotic Systems and Imaging

The continuous evolution of robotic systems and advanced imaging technologies is a paramount driver for the robotic radiotherapy market. Integrating high-precision robotic arms with real-time imaging capabilities, such as cone-beam computed tomography (CBCT), enhances the accuracy of radiation delivery. For instance, a study published on PubMed in 2022, "Advancements in Imaging and Robotic Precision for Radiotherapy," highlighted the significant improvement in tumor targeting accuracy achieved through the combination of robotic platforms with advanced imaging. The research further pointed to the ongoing development of adaptive radiotherapy techniques, where real-time imaging allows for adjustments in radiation delivery based on tumor changes during treatment. The focus on reducing side effects and increasing the effectiveness of radiation therapy through precise targeting is a powerful market drive. This continual innovation directly translates to increased adoption rates, thereby propelling the growth of the robotic radiotherapy market.

Increasing Prevalence of Cancer and Demand for Minimally Invasive Treatments

The escalating global incidence of cancer is a significant factor propelling the robotic radiotherapy market. As cancer cases rise, there is a growing demand for effective and less invasive treatment options. The International Agency for Research on Cancer (IARC) estimates that there were 19.3 million new cancer cases and nearly 10 million cancer deaths worldwide in 2020. This increasing prevalence drives the demand for effective cancer treatment modalities, including radiotherapy.

According to data published by the National Cancer Institute (NCI) in 2023, "Cancer Prevalence and Treatment Modalities," the number of cancer diagnoses worldwide continues to increase, creating a substantial need for advanced radiotherapy solutions. Additionally, patients are increasingly seeking treatments that minimize discomfort and recovery time. Robotic radiotherapy, with its precision and reduced impact on healthy tissues, aligns with this demand. The ability to deliver high doses of radiation to tumors while sparing surrounding organs is a key advantage, leading to higher patient satisfaction and treatment efficacy. This growing need for minimally invasive, effective cancer treatments is a substantial market demand trend, consequently fostering expansion within the robotic radiotherapy market.

Government Initiatives and Healthcare Infrastructure Development

Government initiatives and investments in healthcare infrastructure are vital catalysts for the robotic radiotherapy market. Many countries are implementing programs to improve cancer care, which includes the adoption of advanced radiotherapy technologies. For example, a report from the National Institutes of Health (NIH) in 2021, "Strategic Investments in Advanced Radiotherapy Technologies," detailed government funding for the development and implementation of robotic radiotherapy systems in clinical settings. This support often involves subsidies, research grants, and the establishment of specialized cancer centers equipped with state-of-the-art technology. Moreover, improvements in healthcare infrastructure, particularly in developing regions, are facilitating the accessibility of advanced treatments. Governmental support and infrastructure development are key market growth factors, which in turn significantly stimulates the robotic radiotherapy market.

Segment Insights:

Market Assessment – By Product

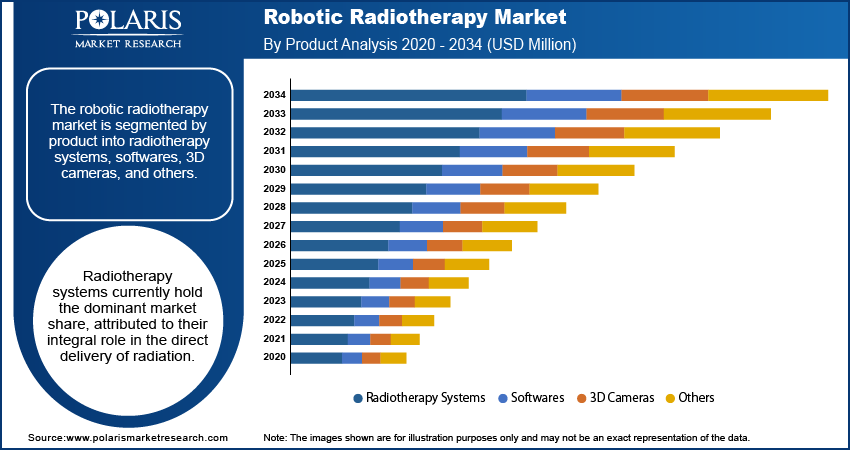

The robotic radiotherapy market is segmented by product into radiotherapy systems, softwares, 3D cameras, and others. Radiotherapy systems currently hold the dominant market share, attributed to their integral role in direct radiation delivery. These advanced systems, which combine robotic precision with radiation emission, are essential for executing complex treatment plans. The continued development of integrated platforms that enhance accuracy and efficiency is a significant factor in maintaining this sub-segment's leading position. This segment reflects the core technology driving the overall market's expansion and adoption.

The softwares sub-segment is demonstrating the highest growth rate within the robotic radiotherapy market. The increasing complexity of treatment planning and delivery necessitates sophisticated software solutions for data processing, image analysis, and treatment optimization. The demand for advanced algorithms that enable real-time adjustments and personalized treatment protocols is driving rapid innovation in this area. As healthcare providers seek to maximize the benefits of robotic radiotherapy, the need for robust and adaptable software solutions continues to expand, reflecting a strong upward trajectory for this subsegment.

Market Evaluation– By Technology

The robotic radiotherapy market is segmented by technology into linear accelerators, conventional linear accelerators, MRI-linear accelerators, stereotactic radiation therapy systems, cyberknife, gamma knife, particle therapy, proton beam therapy, and heavy ion beam therapy. Linear accelerators represent the largest market share within this segmentation. These systems, known for their versatility and established clinical efficacy, form the backbone of many radiotherapy treatments. The widespread adoption of linear accelerator technology, driven by its ability to deliver precise radiation dose management, contributes significantly to its dominant position in the market. The consistent refinement of linear accelerator capabilities, including integration with advanced imaging, ensures its continued relevance and broad applicability.

MRI-linear accelerators are exhibiting the highest growth rate in the robotic radiotherapy market. The integration of magnetic resonance imaging (MRI) with linear accelerators enables real-time visualization of tumors and surrounding tissues during treatment. This capability allows for adaptive radiotherapy, where treatment plans are dynamically adjusted based on tumor movement and changes. The increasing demand for personalized and highly precise radiotherapy solutions is fueling the rapid adoption of MRI-linear accelerators. This technological advancement addresses the need for enhanced accuracy and reduced side effects, driving its accelerated growth trajectory within the market.

Market Assessment – By Application

The robotic radiotherapy market is segmented by application into prostate cancer, breast cancer, lung cancer, head & neck cancer, colorectal cancer, and other cancers. Lung cancer applications currently hold the most significant market share within this segmentation. This prominence stems from the rising global incidence of lung cancer and the complexity of its treatment, which often necessitates precise and targeted radiotherapy. The advantages provided by robotic radiotherapy systems, such as enhanced accuracy in delivering radiation to lung tumors while minimizing damage to surrounding healthy lung tissue, drive its widespread adoption in these clinical settings.

The prostate cancer application segment is demonstrating notable growth within the robotic radiotherapy market. The rising prevalence of prostate cancer, coupled with the increasing adoption of advanced radiotherapy techniques for localized prostate tumors, is fueling this expansion. The increasing availability of robotic radiotherapy technologies, that can enable high level of precision for that specific type of cancer, is a driver of the growth. Furthermore, the focus on minimizing side effects and improving patient outcomes in prostate cancer treatment is driving the demand for advanced robotic radiotherapy solutions.

Robotic Radiotherapy Market Assessment – By End-User

The robotic radiotherapy market is segmented by end user into hospitals and independent radiotherapy centers. Hospitals currently holds the largest market share within this segmentation. This dominance is attributed to the comprehensive infrastructure and multidisciplinary care teams available in hospital settings, which are essential for implementing and managing complex robotic radiotherapy treatments. The established patient base and the ability to integrate robotic radiotherapy with other hospital services further solidify the hospital's leading role in market adoption.

Independent radiotherapy centers are demonstrating a notable growth rate. The increasing specialization and focus on outpatient care are driving the expansion of these centers. These facilities offer streamlined services and often provide a more accessible and cost-effective alternative to hospital-based treatments. The increasing demand for specialized, patient-centric radiotherapy services outside of traditional hospital settings is contributing to the rapid growth of independent radiotherapy centers within the market.

Regional Footprint

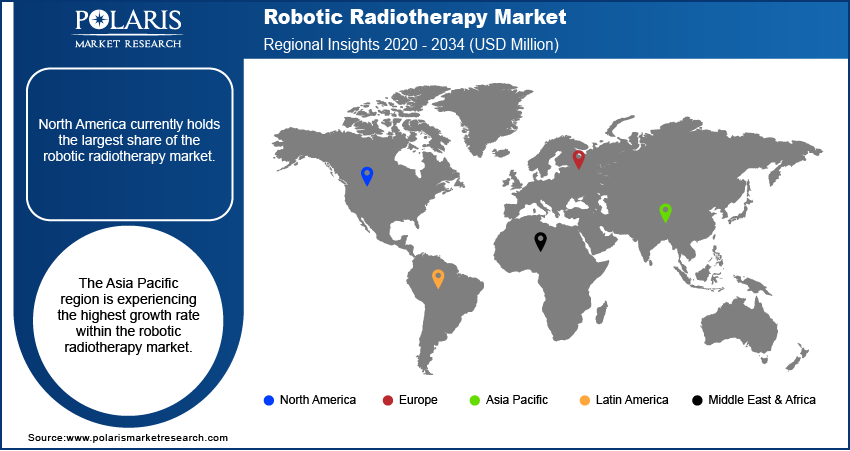

The robotic radiotherapy market demonstrates varying regional dynamics, influenced by healthcare infrastructure, technological adoption, and cancer prevalence. North America and Europe have established strong market positions, driven by advanced healthcare systems and significant investments in innovative technologies. Asia Pacific is emerging as a high-growth region, fueled by expanding healthcare access and increasing cancer incidence. Latin America and the Middle East & Africa are also witnessing market expansion, albeit at a relatively slower pace, due to ongoing healthcare infrastructure development and rising awareness of advanced treatment options.

North America currently holds the largest share of the robotic radiotherapy market. This region's dominance is attributed to its robust healthcare infrastructure, high adoption rates of advanced medical technologies, and substantial investments in research and development. The presence of leading healthcare institutions and a strong reimbursement framework further facilitates the widespread implementation of robotic radiotherapy systems. The established healthcare ecosystem and a focus on cutting-edge cancer treatment contribute significantly to North America's leading market position.

The Asia Pacific region is experiencing the highest growth rate within the robotic radiotherapy market. This rapid expansion is driven by a confluence of factors, including increasing cancer prevalence, improving healthcare access, and rising disposable incomes. Governments in several countries within the region are investing heavily in upgrading healthcare infrastructure and promoting the adoption of advanced radiotherapy technologies. Furthermore, the growing awareness of minimally invasive treatment options and the increasing availability of skilled healthcare professionals are accelerating the market's growth trajectory in Asia Pacific.

Key Players and Competitive Insights

The robotic radiotherapy market features a landscape of established and innovative players, including Accuray Incorporated, Elekta AB, Varian Medical Systems (Siemens Healthineers), Brainlab AG, ViewRay Incorporated, Mitsubishi Electric Corporation, and Sumitomo Heavy Industries Limited. These companies are actively involved in developing and providing advanced robotic radiotherapy systems, software, and related technologies, contributing significantly to the market's evolution.

Competitive analysis of the robotic radiotherapy market reveals a dynamic environment characterized by continuous technological advancements and strategic collaborations. Companies are focused on enhancing treatment precision, improving patient outcomes, and expanding their product portfolios. Innovation in areas such as real-time imaging, adaptive radiotherapy, and software integration is crucial for maintaining a competitive edge. The market also sees strategic partnerships and acquisitions aimed at strengthening product offerings and expanding market reach, with companies striving to provide comprehensive solutions that meet the evolving needs of healthcare providers.

Accuray Incorporated, headquartered in Sunnyvale, California, offers the CyberKnife and TomoTherapy systems, which integrate robotic precision with radiation delivery. These systems are designed to deliver highly accurate radiation therapy, minimizing damage to healthy tissues. The company’s focus on innovative technology and patient-centric solutions makes it a key player in the robotic radiotherapy space.

Elekta AB, based in Stockholm, Sweden, provides a range of radiotherapy solutions, including the Versa HD and Elekta Unity systems. These systems combine linear accelerators with advanced imaging and software, enabling precise and adaptive radiation therapy. Elekta’s comprehensive portfolio and commitment to research and development position it as a significant contributor to the advancement of robotic radiotherapy technologies.

List of Key Companies

- Accuray Incorporated

- Brainlab AG

- Elekta AB

- Mitsubishi Electric Corporation

- Sumitomo Heavy Industries Limited

- Varian Medical Systems (Siemens Healthineers)

- ViewRay Incorporated

Industry Developments

- January 2025: Accuray reported that its Radixact SynC System and CyberKnife S7 System received approval from China’s National Medical Products Administration (NMPA). This regulatory clearance enhanced Accuray’s access to the Chinese market and created additional opportunities for revenue expansion.

- April 2024: Elekta AB and Microsoft announced a partnership to utilize Microsoft's Azure cloud computing platform for enhanced radiation oncology treatment planning and data management. This collaboration aims to improve the efficiency and precision of radiotherapy treatments by leveraging the power of cloud-based solutions. This kind of collaboration is aimed at improving the software side of robotic radiotherapy.

- May 2024: Varian Medical Systems (Siemens Healthineers) announced that their Ethos radiation system, a next-generation platform designed for highly precise and adaptable cancer treatment, has received FDA 510(k) clearance. This approval signifies a significant advancement in radiation therapy technology, enabling more personalized and effective cancer treatments. This represents a product approval that is very important to the market.

Market Segmentation

By Product Outlook (Revenue-USD Million, 2020–2034)

- Radiotherapy Systems

- Softwares

- 3D Cameras

- Others

By Technology Outlook (Revenue-USD Million, 2020–2034)

- Linear Accelerators

- Conventional Linear Accelerators

- MRI - Linear Accelerators

- Stereotactic Radiation Therapy Systems

- Cyberknife

- Gamma Knife

- Particle Therapy

- Proton Beam Therapy

- Heavy Ion beam Therapy

By Application Outlook (Revenue-USD Million, 2020–2034)

- Prostate Cancer

- Breast Cancer

- Lung Cancer

- Head & Neck Cancer

- Colorectal Cancer

- Other Cancers

By End User Outlook (Revenue-USD Million, 2020–2034)

- Hospitals

- Independent Radiotherapy Centers

By Regional Outlook (Revenue-USD Million, 2020–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Report Scope:

| Report Attributes | Details |

| Market Size Value in 2024 | USD 1,237.19 million |

| Market Size Value in 2025 | USD 1,378.85 million |

| Revenue Forecast by 2034 | USD 3,732.43 million |

| CAGR | 11.7% from 2025 to 2034 |

| Base Year | 2024 |

| Historical Data | 2020–2023 |

| Forecast Period | 2025–2034 |

| Quantitative Units | Revenue in USD million and CAGR from 2025 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Industry Insights |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

How is the report valuable for an organization?

Workflow/Innovation Strategy

The robotic radiotherapy market has been segmented into detailed segments of product, technology, application, and end user. Moreover, the study provides the reader with a detailed understanding of the different segments at both the global and regional levels.

Market Entry Strategies

Growth strategies within the robotic radiotherapy market center on technological innovation and strategic partnerships. Companies are focusing on enhancing system precision and integrating advanced imaging capabilities to improve treatment outcomes. Market penetration is being driven by expanding applications in diverse cancer treatments and increasing awareness of minimally invasive options. Collaborations with healthcare institutions and technology providers are crucial for developing comprehensive solutions. Furthermore, targeted marketing efforts, emphasizing the clinical benefits and cost-effectiveness of robotic radiotherapy, are essential for driving adoption and expanding market reach.

FAQ's

The robotic radiotherapy market size was valued at USD 1,237.19 million in 2024 and is projected to grow to USD 3,732.43 million by 2034.

The market is projected to register a CAGR of 11.7% during the forecast period, 2025-2034.

North America had the largest share of the market.

Key players in the robotic radiotherapy market include Accuray Incorporated, Elekta AB, Varian Medical Systems (Siemens Healthineers), Brainlab AG, ViewRay Incorporated, Mitsubishi Electric Corporation, and Sumitomo Heavy Industries Limited.

The radiotherapy systems segment accounted for the larger share of the market in 2024.

Following are some of the robotic radiotherapy market trends: ? Integration of AI and Machine Learning: There's a significant push to incorporate AI and machine learning into robotic radiotherapy systems. This aims to enhance treatment planning, improve precision, and enable real-time adjustments during therapy. ? Shift Towards Adaptive Radiotherapy: The focus is increasing on adaptive radiotherapy, where treatment plans are dynamically adjusted based on changes in the tumor's size, shape, or position during treatment. This requires advanced imaging and software capabilities. ? Emphasis on Patient-Centric Care: There's a growing emphasis on providing personalized and less invasive treatments to improve patient outcomes and quality of life. This drives the demand for precise robotic radiotherapy solutions.

Robotic radiotherapy represents a significant advancement in cancer treatment, leveraging robotic technology to enhance the precision and effectiveness of radiation therapy. At its core, it involves the use of sophisticated robotic arms and advanced imaging systems to deliver high doses of radiation directly to tumors while minimizing damage to surrounding healthy tissues. This approach allows for greater accuracy in targeting cancerous cells, even in complex or hard-to-reach areas of the body. The integration of real-time imaging, such as cone-beam computed tomography (CBCT) or magnetic resonance imaging (MRI), enables clinicians to monitor tumor movement and adjust radiation delivery dynamically, ensuring optimal treatment outcomes.

Download Sample Report of Robotic Radiotherapy Market

Please fill out the form to request a customized copy of the research report.