Self-Hosted Cloud Platform Market Size, Trends, Industry Analysis Report, 2026 - 2034

REPORT DETAILS

Self-Hosted Cloud Platform Market Summery

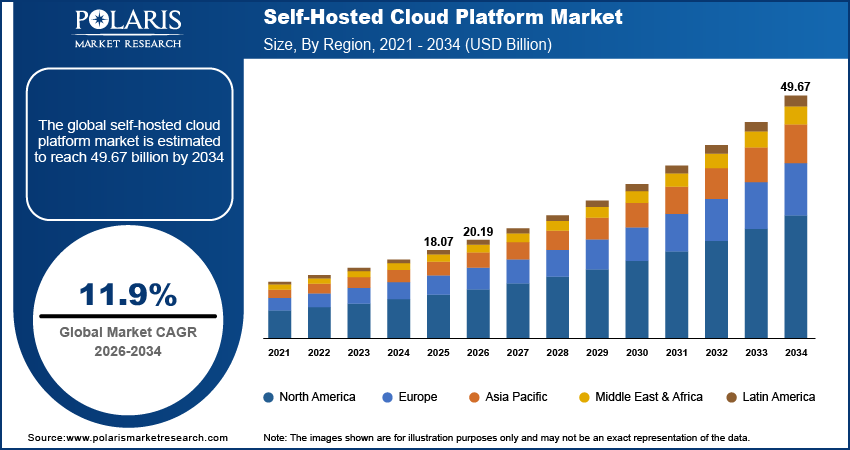

The global self-hosted cloud platform market is estimated around USD 18.07 billion in 2025,?with consistent growth anticipated during 2026–2034. Growth is supported by rising data sovereignty requirements, increasing regulatory compliance mandates, and enterprise investment in software-defined data centers. The market is projected to grow at a CAGR of 11.9% during the forecast period.

Market Statistics

Key Takeaways

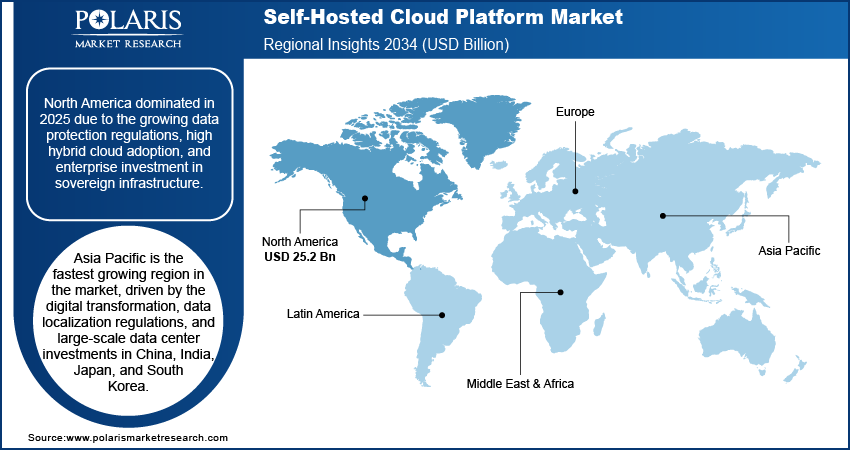

- North America accounted for the largest regional share of around 37.6% in 2025, driven by strong regulatory pressures, high enterprise cloud maturity, and increasing adoption across BFSI, healthcare, and government sectors.

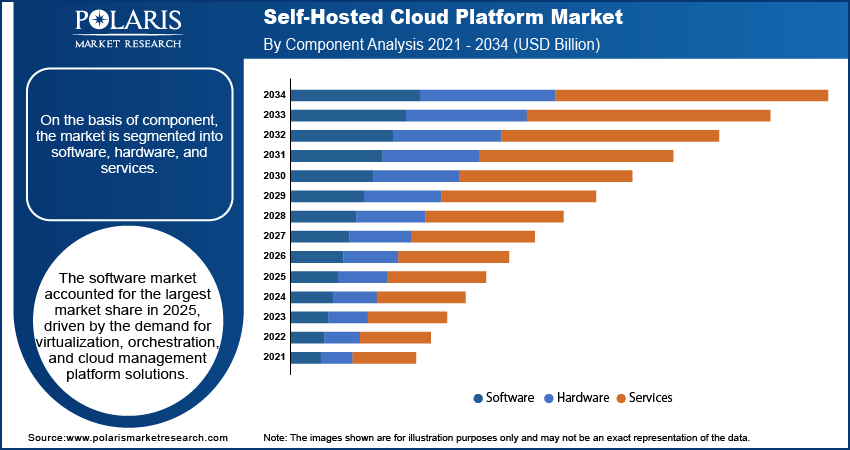

- By Component, Software segment accounted for the largest share of approximately 79.9% in 2025, supported by growing demand for cloud orchestration, automation, and enterprise-controlled infrastructure platforms.

- By Deployment Model, On-Premise segment accounted for the largest share of around 58.4% in 2025, driven by rising data sovereignty requirements, regulatory compliance needs, and enterprise preference for full infrastructure control.

- By Enterprise Size, Large Enterprises segment accounted for the largest share of nearly 67.2% in 2025, supported by large-scale IT environments, high data security requirements, and extensive adoption of private cloud infrastructure.

- By Industry Vertical, BFSI segment accounted for the largest share of around 29.5% in 2025, driven by strict regulatory compliance, data protection requirements, and increasing adoption of secure cloud environments for financial operations.

Industry Dynamics

- Rising data privacy regulations and cross-border data transfer restrictions are accelerating adoption of enterprise-controlled cloud infrastructure.

- Expansion of virtualization, containerization, and software-defined data centers is strengthening demand for self-managed cloud platforms.

- High upfront capital expenditure and ongoing infrastructure maintenance costs create financial barriers for smaller enterprises.

- Integration with edge computing and hybrid cloud orchestration frameworks is unlocking long-term growth opportunities across regulated and latency-sensitive sectors.

What is a Self-Hosted Cloud Platform?

The self-hosted cloud platform market refers to cloud environments deployed and operated within an organization’s own data center or dedicated facilities, using on-premise cloud platform architectures built on virtualization, containerization, and software-defined data centers. Unlike public cloud consumption models, enterprise self-hosted cloud infrastructure is owned, configured, and governed directly by internal IT teams, enabling full control over compute, storage, networking, security policies, and data residency.

Source: Polaris Market Research Analysis

To Understand More About this Research:Download Sample Report

Drivers & Opportunities

Increasing Data Privacy and Regulatory Compliance Pressures: Rising need for data sovereignty, privacy, and breach accountability is pushing companies to retain control over the infrastructure by using self-hosted cloud solutions. Enterprises in regulated industries are more likely to operate in environments where governance, access, and audit trails are maintained in-house. In September 2025, Stratbeans announced the launch of a comprehensive compliance platform that is compliant with Digital Personal Data Protection (DPDP) regulations, covering data governance, consent management, and automated breach response. The Self-Hosted Cloud Platform Market is directly affected as organizations prefer the certainty of compliance over shared infrastructure.

Growing Investment in Software-Defined Data Centers (SDDCs): The adoption of virtualization and management of the infrastructure as a centralized function is boosting the use of self-hosted cloud solutions. Businesses are adopting AI and high-density applications that require dynamic computing infrastructure with automated orchestration and scalable control planes. In June 2025, Schneider Electric launched AI-ready modular pod and rack offerings that combine liquid cooling and scalable infrastructure design. Such developments help in supporting SDDC capabilities by offering flexible deployment options, which are most suited to applications that demand high performance. Therefore, the increasing investments in virtualization, automation, and management infrastructure are boosting demand for self-hosted cloud solutions.

Restraints & Challenges

High Capital Expenditure Requirements: The self-hosted cloud model requires high capital expenditure requirements in terms of servers, storage, network infrastructure, cooling infrastructure, and security infrastructure. Maintenance, upgrade, and talent-related expenses further escalate financial outlays. Such financial hurdles hinder adoption in smaller businesses and postpone large-scale adoption in financially conservative sectors of the Self-Hosted Cloud Platform Market.

Opportunity

Integration with Edge Computing Architectures: The rise in edge computing are projected to create opportunities for deployment. The self-hosted cloud platform are extended to a distributed edge architecture while retaining centralized management and control. This is made possible through the hybridized model, which enables real-time analytics, industrial automation, and AI inference at the edge while retaining control of the infrastructure. Thus, the rise in edge computing deployments in manufacturing, telecom, and smart infrastructure domains, are fueling the growth of the self-hosted cloud platform market.

Source: Polaris Market Research Analysis

Segmental Insights

This report offers detailed coverage of the self-hosted cloud platform market by component, deployment model, enterprise size, and industry vertical to help readers identify the fastest expanding and most attractive demand segments.

By Component

-

Software

Software represents the largest share within the self-hosted cloud platform market by component. Private cloud infrastructure software market demand is driven by virtualization layers, orchestration engines, and cloud management platform tools that support workload provisioning, access control, and policy enforcement.

-

Hardware

Hardware is the foundation, including compute servers, storage systems, and networking infrastructure. Moreover, hardware market growth is relatively more incremental, as enterprises are increasingly adopting software-defined solutions that decouple from physical infrastructure..

-

Services

Services market is the fastest-growing segment, driven by complexity and talent shortages. Enterprises adopting private clouds need architecture design, integration, and optimization services.

By Deployment Model

-

On-Premise

The on-premise cloud infrastructure market is the largest segment in the market. Enterprises in regulated industries require end-to-end control over data, network, and physical security. On-premise cloud infrastructure ensures predictable latency and control, especially for financial and military applications.

-

Dedicated Hosted

Dedicated hosted clouds offer isolated infrastructure hosted in third-party facilities. The adoption level is stable for organizations that need physical isolation without needing internal capital expenditures.

-

Hybrid

The adoption rate of hybrid private clouds is increasing as organizations extend their workloads across self-hosted infrastructure and public cloud models. Hybrid models strike a balance between autonomy and flexibility, allowing for scaling and disaster recovery capabilities. Adoption is fueled by digital transformation projects that require flexibility without compromising control.

By Enterprise Size

-

Large Enterprises

Large enterprise private cloud adoption led the market due to its sheer size, vulnerability to compliance risks, and data management issues. The self-hosted cloud platform for enterprises provides customizable security options, resource allocation, and connectivity with enterprise risk management systems.

-

SMEs

SME cloud infrastructure market is growing at a rapid pace as small businesses demand more predictable expense structures and enhanced cybersecurity. SMEs are increasingly adopting modular private cloud stacks to protect their intellectual properties and remain flexible.

By Industry Vertical

-

BFSI

BFSI private cloud market held the largest market share. The BFSI industry requires effective management of encryption, transaction-level auditing, and compliance. Private cloud deployment provides controlled access and latency-sensitive processing.

-

Healthcare

The self-hosted cloud market in the healthcare industry is expanding due to the increasing need for patient data protection regulations and the rapidly expanding electronic health record system market. The healthcare industry and hospitals require highly controlled environments for managing protected health information, medical imaging archives, and networked medical devices.

-

Government

The sovereign cloud infrastructure market is gaining momentum due to national cybersecurity strategies and data sovereignty requirements. Government agencies stress localized data presence, encrypted communication infrastructure, and business continuity for critical infrastructure services.

-

IT & Telecom

IT & Telecom providers deploy self-hosted cloud platforms to support network function virtualization, edge orchestration, and service lifecycle automation. As 5G rollout expands and distributed network architectures grow more complex, operators require internal cloud control to maintain performance consistency and minimize latency.

-

Manufacturing

Regulated industries private cloud deployment in manufacturing centers on intellectual property protection and secure industrial IoT integration. Production facilities yields sensitive design information, process analytics, and machine data that need to be protected by segmented access controls.

-

Defense

Defense industry is the fastest-growing market segment due to their classified workload needs and sovereign infrastructure needs. The self-hosted cloud environment offers isolated, encrypted communication channels and protection for national security frameworks.

Source: Polaris Market Research Analysis

Technology & Architecture Trends in the Self-Hosted Cloud Platform Market

The modernization of enterprise IT is driving the evolution of self-hosted cloud infrastructure architecture into programmable, policy-based, and security-compliant systems. Rather than functioning solely as virtualized data centers, modern private cloud deployments are engineered for workload portability, governance control, and automation at scale. Orchestration, containerization, identity-aware security, and software-defined infrastructure now define competitive differentiation within the market.

Self-Hosted Cloud Architecture Framework

A well-structured private cloud infrastructure architecture is a seamless stack of integrated architectural layers:

-

Orchestration Layer:

It is the control plane, which allows automated provisioning, policy management, and execution of Infrastructure-as-Code. The growing market for cloud orchestration tools reflects the need for API-managed workload orchestration and CI/CD pipelines.

-

Virtualization Layer:

Hypervisors abstract compute resources, while container runtimes coexist to support hybrid VM–container stacks. Organizations are moving towards container-based approaches to enhance scalability and resource utilization.

-

Storage Stack:

Software-defined storage offers a single platform for object, block, and file storage with global policy management. Encryption at rest, geo-redundancy, and auto-replication are essential capabilities to enable data sovereignty in cloud infrastructure.

-

IAM & Security Controls:

RBAC, federated identity, and MFA provide least-privilege access. Zero-trust security in private cloud infrastructure shifts perimeter security from continuous identity verification to micro-segmentation and dynamic policy enforcement.

-

Monitoring & Observability:

Compute, storage, and networking telemetry data is fed into SIEM and analytics systems. Observability tools support compliance reporting, performance optimization, and swift incident response.

Open-Source & Kubernetes Impact

The usage of open-source self-hosted cloud infrastructure is on the rise due to the increasing demand for interoperability and vendor-agnostic solutions.

- Kubernetes in Private Cloud: Kubernetes is a major contributor to the adoption of Kubernetes private cloud, offering container orchestration, auto-scaling, and workload mobility. It further aligns DevOps and offers cloud-native application modernization capabilities within sovereign infrastructure domains.

- OpenStack Relevance: OpenStack continues to be relevant in regulated and complex environments where customized APIs and multi-tenant infrastructure are needed. Its architecture facilitates the orchestration of compute, storage, and networking resources in enterprise-managed environments.

Security & Compliance Mapping

Security architecture is becoming more compliance-focused.

- Zero Trust: Access decisions are periodically validated based on identity, device health, and workload context.

- Data Encryption & Sovereignty: End-to-end encryption, key management solutions, and geographic data controls ensure alignment with regulatory requirements and private cloud compliance solutions.

- Compliance Readiness: Audit logging, configuration baselines, and regulatory mapping dashboards integrate governance directly into platform operations.

Regional Analysis

North America Self-Hosted Cloud Platform Market Assessment

North America witnessed a robust adoption growth in the self-hosted cloud platform market propelled by the rising regulatory pressures in the BFSI, healthcare, and government sectors. The growing data protection regulations raised concerns about data residency, consent, and international transfer, forcing organizations to maintain control over the infrastructure stack. In December 2025, close to 20 comprehensive state privacy laws had been enforced or passed in the US, making way for more stringent consent regimes and improved consumer rights. The growing complexity of compliance, therefore, reinforced the need in the U.S. private cloud infrastructure market and contributed to the North America self-hosted cloud market size. The adoption of hybrid models, comprising on-premise cloud infrastructure and public cloud infrastructure, are increasing as organizations pursued flexibility in operations without sacrificing control.

Asia Pacific Self-Hosted Cloud Platform Market Insight

Asia Pacific self-hosted cloud platform market is growing at a rapid pace driven by rising digital modernization initiatives across China, India, Japan, and South Korea. Rising cybersecurity risks and data governance requirements increased demand for secure on-premise cloud platforms, strengthening the Asia Pacific self-hosted cloud growth rate. In India, a massive investment of close to USD 70 billion in data centers is in progress, along with another USD 90 billion in announced investments, symbolizing the massive infrastructure development taking place to support AI and business workloads. Government-backed data localization initiatives are strengthening the mandate for storing data within the country, promoting the adoption of private and self-managed cloud infrastructure.

Europe Self-Hosted Cloud Platform Market Overview

The self-hosted cloud platform market is growing in Europe due to robust data protection regulations such as GDPR, which further strengthened the enterprise mandate for storing and processing data. Enterprises focused on localized infrastructure to ensure regulatory compliance and reduced exposure to regulations, thus expanding the Europe private cloud platform market. The concept of digital sovereignty further fueled the preference for self-managed cloud infrastructure over third-party hosting.

Middle East Self-Hosted Cloud Platform Market Assessment

Middle East market progressed through government-led digital transformation strategies and smart city development programs. The growing importance of cybersecurity in the financial sector and public administration led to an increase in the procurement of sovereign and self-controlled cloud infrastructure. The sovereign cloud market in the Middle East grew due to the rising focus on data governance by governments in the region. The demand for cloud infrastructure in the government sector led to the adoption of self-hosted cloud platforms in strategic sectors for improved security and control.

Heat Map Analysis

| Region | Market Position | Growth Momentum | Regulatory Strength | Recycling Infrastructure | Secondary Lead Production Base |

| North America | Leading | High | Very High | Low | Low |

| Asia Pacific | High | Very High | High | Low | Low |

| Europe | High | Medium–High | Very High | Low | Low |

| Middle East | Emerging | High | Medium–High | Low | Low |

Source: Polaris Market Research Analysis

Source: Polaris Market Research Analysis

Key Players & Competitive Analysis Report

The self-hosted cloud platform market reflects a moderately consolidated structure, with key players including global enterprise infrastructure companies and open-source-led platform suppliers operating in hybrid and private cloud models. The degree of competitiveness is driven by control of the underlying virtualization stacks, storage orchestration layers, and enterprise security integration, rather than raw storage capacity. Companies are competing on flexibility of deployment, support for data sovereignty on-premises, and integration with existing enterprise IT infrastructure. The level of differentiation in platforms is propelled by container orchestration, Kubernetes-native, identity integration, and automation.

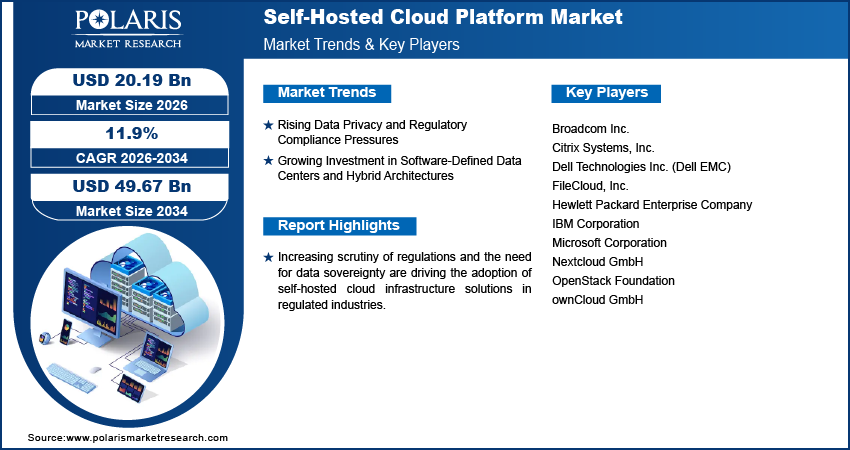

The major players in the global self-hosted cloud platform market are Broadcom Inc., Citrix Systems, Inc., Dell Technologies Inc. (Dell EMC), FileCloud, Inc., Hewlett Packard Enterprise Company, IBM Corporation, Microsoft Corporation, Nextcloud GmbH, OpenStack Foundation, and ownCloud GmbH.

Key Players

- Broadcom Inc.

- Citrix Systems, Inc.

- Dell Technologies Inc. (Dell EMC)

- FileCloud, Inc.

- Hewlett Packard Enterprise Company

- IBM Corporation

- Microsoft Corporation

- Nextcloud GmbH

- OpenStack Foundation

- ownCloud GmbH

Industry Developments

- June 2025: DoubleWord introduced a self-hosted inference platform on the Snowflake Marketplace, allowing enterprises to perform AI model inference on their own cloud infrastructure. This offering further expanded the capabilities of Self-Hosted Cloud Platforms with scalable AI processing for secure enterprise data resources.

- June 2025: Broadcom released VMware Cloud Foundation 9.0, a significant enhancement to its unified private cloud platform, making it easier to deploy, manage, and secure on-premises and hybrid cloud environments.

- May 2025: Synology unveiled the PAS7700, an active-active NVMe all-flash storage solution engineered for enterprise mission-critical workloads, delivering high performance, scalability, and continuous availability.

Self-Hosted Cloud Platform Market Segmentation

By Component Outlook (Revenue, USD Billion, 2021-2034)

- Software

- Hardware

- Services

By Deployment Model Outlook (Revenue, USD Billion, 2021-2034)

- On-premise

- Dedicated hosted

- Hybrid

By Enterprise Size Outlook (Revenue, USD Billion, 2021-2034)

- SMEs

- Large enterprises

By Industry Vertical Outlook (Revenue, USD Billion, 2021-2034)

- BFSI

- Healthcare

- Government

- IT & Telecom

- Manufacturing

- Defense

By Regional Outlook (Revenue, USD Billion, 2021-2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Self-Hosted Cloud Platform Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 18.07 Billion |

| Market Size in 2026 | USD 20.19 Billion |

| Revenue Forecast by 2034 | USD 49.67 Billion |

| CAGR | 11.9% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2022–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Self-Hosted Cloud Platform Market FAQ's

The global market size was valued at USD 18.07 billion in 2025 and is projected to grow to USD 49.67 billion by 2034.

North America leads the market due to strong regulatory enforcement, high enterprise cloud maturity, and rising adoption across BFSI, healthcare, and government sectors.

Large enterprises represent the dominant end users, particularly across BFSI, healthcare, government, IT & telecom, and defense sectors where data sovereignty and compliance control are critical.

A few of the key players in the market are Broadcom Inc., Citrix Systems, Inc., Dell Technologies Inc. (Dell EMC), FileCloud, Inc., Hewlett Packard Enterprise Company, IBM Corporation, Microsoft Corporation, Nextcloud GmbH, OpenStack Foundation, and ownCloud GmbH.

Growth is driven by rising data privacy regulations, increasing cybersecurity risks, expansion of software-defined data centers, edge computing integration, and enterprise demand for infrastructure sovereignty.

Download Sample Report of Self-Hosted Cloud Platform Market

Please fill out the form to request a customized copy of the research report.