Structured Cabling Market Trends, Share, Growth Analysis Report, 2026-2034

REPORT DETAILS

REPORT DETAILS

Structured Cabling Market Summary

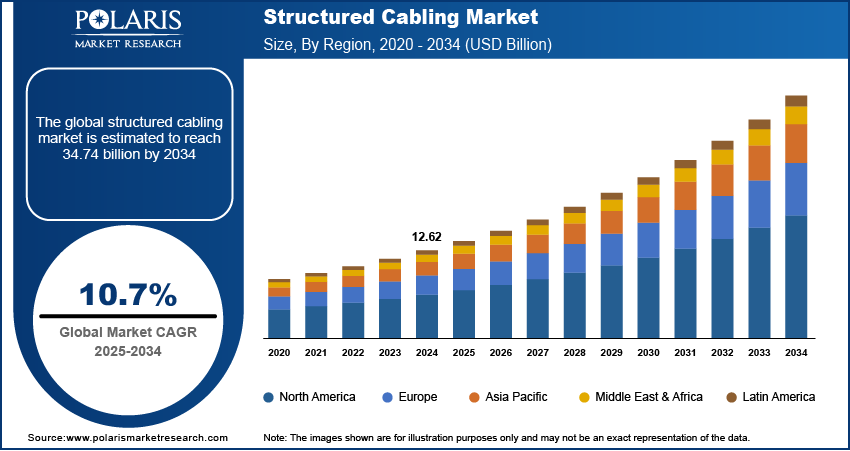

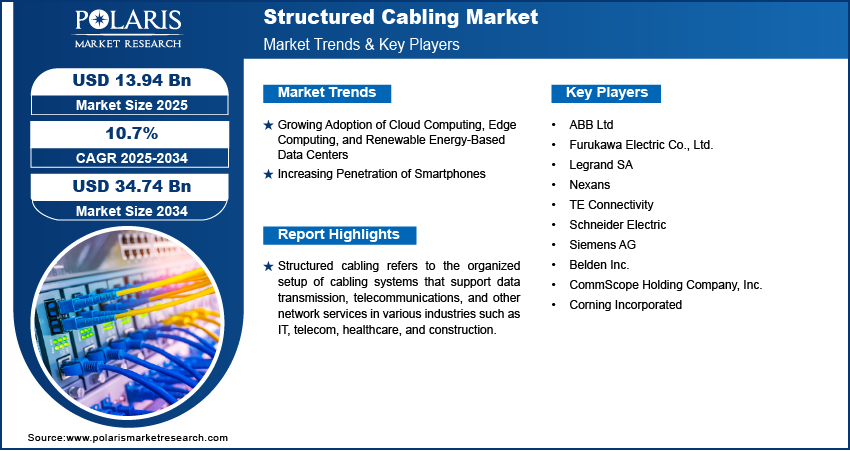

The global structured cabling market size was valued at USD 13.94 billion in 2025, growing at a CAGR of 9.5% from 2026 to 2034. Rising demand for high-speed data connectivity and growing digitization boost the market growth. Also, advancements in communication technology will drive the market expansion in the coming years.

Market Statistics

Key Takeaways

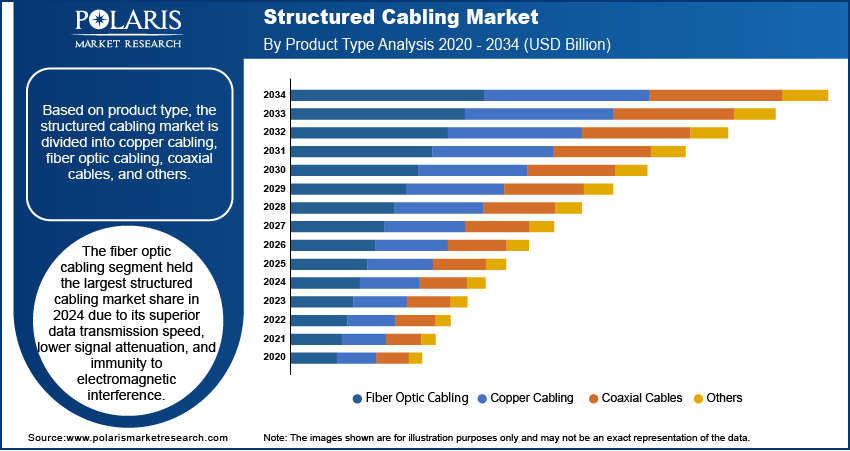

- The fiber optic structured cabling segment held the largest share of market revenue in 2025. Its superior data transmission speed and lower signal attenuation contributed to the dominance.

- The data center structured cabling systems segment dominated the market share in 2025. It is driven by the increasing demand for cloud storage, big data analytics, and edge computing solutions.

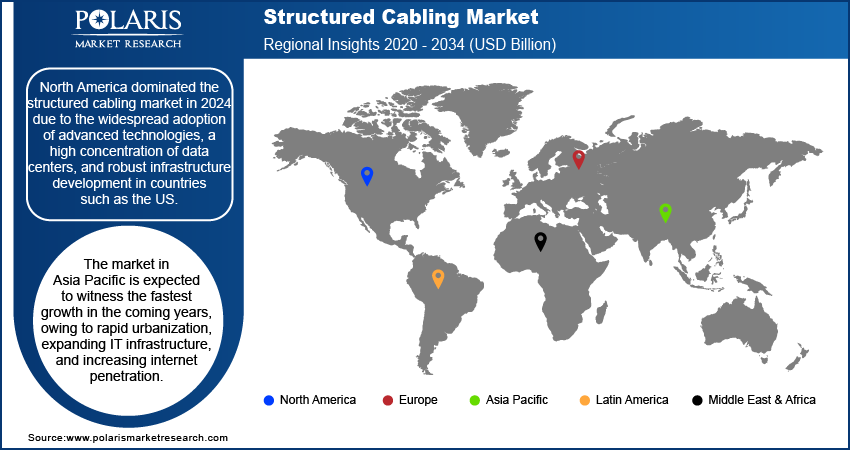

- North America held the largest revenue share in 2025. The widespread adoption of advanced technologies and a high concentration of data centers boost the dominance. Also, robust infrastructure development in countries such as the U.S.

- The Asia Pacific market is expected to witness the fastest growth in the coming years. Rapid urbanization, expanding IT infrastructure, and increasing internet penetration boost the regional market growth.

Industry Dynamics

- The rising adoption of cloud computing, edge computing, and renewable energy-based data centers propels the demand for structured cabling across the world.

- Growing use of smartphones across the globe is propelling the market growth.

- High cost of setup hinders the growth of the market.

- Innovations in installation techniques and increasing emphasis of automation will create lucrative opportunities in the market.

AI Impact on Structured Cabling Market

- Expansion of AI-driven data centers will propel the requirement for high-speed fiber and high-density structured cabling systems.

- Enterprises are upgrading cabling to support low-latency AI, cloud, and edge computing environments.

- AI-based network analytics allows for predictive maintenance. It helps reduce downtime and service costs for B2B operators.

- Smart infrastructure planning tools optimize cable design. This lowers installation time and project risks.

- OEMs and system integrators adopt AI for automated testing, fault detection, and quality assurance.

- AI-enabled capacity forecasting assists vendors in aligning production, inventory, and contract-based deployments.

To Understand More About this Research: Download Sample Report

Structured cabling refers to the organized arrangement of cabling systems that support data transmission, telecommunications, and other network services in different industries like IT, telecom, healthcare, and construction. The structured cabling market development is driven by the increasing demand for high-speed data connectivity, digitization, and advancements in communication technology. In addition, structured cabling has emerged as a foundational element of modern network infrastructure. It provides scalable, standardized, and future-ready connectivity across data centers, smart buildings, and industrial environments. Organizations are increasingly using cloud-based platforms, IoT systems, and AI-driven workloads. Thus, demand for reliable data center cabling infrastructure and enterprise network connectivity is growing.

Structured cabling is now essential for modern communication systems due to the rapid adoption of smart systems, IoT technology, and cloud-based setups. The increase in data center deployments and the growing need for better network scalability and efficiency are driving the demand for structured cabling. According to data published by the United States International Trade Commission, there are over 2,600 data centers spread across the U.S.

Market Drivers

Growing Adoption of Cloud Computing, Edge Computing, and Renewable Energy-Based Data Centers

Cloud and edge computing depend on smooth data transmission and quick connectivity. Structured cabling meets this need with its organized and flexible design. Renewable energy data centers need reliable cabling systems to support energy-efficient operations and sustainable practices. The rapid growth of hyperscale data centers and distributed edge facilities has resulted in higher cabling density and complexity. This is especially true as AI workloads demand more power and bandwidth. Structured cabling systems play a critical role in supporting high-performance computing environments by enabling efficient airflow, simplified maintenance, and future scalability. Therefore, the growing adoption of cloud computing, edge computing, and renewable energy-based data centers propels the structured cabling market expansion.

Increasing Penetration of Smartphones

The use of smartphones is rising across the world. According to the State of Mobile Internet Connectivity Report 2023, over half (54%) of the global population owns a smartphone. The rise in smartphone use has led to a significant increase in mobile data traffic. Telecom providers emphasize handling higher traffic levels. They also focus on ensuring low latency since more people rely on smartphones for streaming, gaming, communication, and business applications. Structured cabling provides the scalability and reliability needed to support these high-speed networks. It enables seamless data transfer and consistent service. This situation prompts telecom operators to upgrade their 5G backhaul networks and expand fiber-based infrastructure. Structured cabling systems make these upgrades easier. They support high-capacity, low-latency data transmission throughout telecom central offices and network hubs. Moreover, the growth of private 5G networks, driven by smartphone adoption, increases demand for effective cabling systems. These systems can manage the higher bandwidth and connectivity demands.

Segmentation Insights

By Product Type

Based on type of product, the market segmentation includes copper cabling, fiber optic cabling, coaxial cables, and others. The fiber optic cabling segment led revenue share in 2025. Its higher data transmission speed and lower signal loss propel the dominance. Also, resistance to electromagnetic interference supports its leading position. The rapid expansion of 5G networks and the increasing penetration of high-speed internet services propel the demand for fiber optic cabling. In data centers and telecom networks, long-distance transmission, immunity to electromagnetic interference, and high bandwidth are crucial. Data-heavy environments prefer fiber optic cabling over copper cabling. Copper structured cabling offers various benefits like affordability and easy installation. Thus, it is commonly used in short-range enterprise LAN applications.

Copper vs Fiber Structured Cabling Decision Framework

| Decision Factor | Copper Cabling | Fiber Optic Cabling |

| Bandwidth Capacity | Moderate; suitable for standard enterprise networks | Very high; supports data centers, AI, and high-speed backbones |

| Transmission Distance | Limited (up to ~100 m) | Long-distance support (kilometers) |

| Latency Performance | Higher latency than fiber | Ultra-low latency for real-time applications |

| EMI Resistance | Susceptible to electromagnetic interference | Immune to EMI and electrical noise |

| Installation Cost | Lower upfront cost | Higher initial investment |

| Maintenance Needs | Higher due to signal loss and interference | Lower; stable and durable performance |

| Scalability | Limited future upgrade potential | Highly scalable for future bandwidth demands |

| Use Case Fit | Office LANs, small enterprises | Data centers, smart buildings, industrial networks |

By Application

By application, the segmentation includes data centers, local area networks (LAN), and telecommunication. The data centers segment dominated revenue share in 2025. The rising demand for cloud storage, big data analytics, and edge computing solutions boosts domination. The increasing deployment of hyperscale and colocation data centers globally has driven investments in structured cabling infrastructure. Investments in hyperscale, colocation, and enterprise data centers propelled the demand for high-density structured cabling architectures. This cabling supports east-west traffic and virtualization-heavy workloads. Structured cabling ensures scalability, operational efficiency, and simplified network management across these facilities.

Regional Analysis

By region, the report gives insights into the structured cabling market in North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa. North America led the global structured cabling market in 2025. The segment dominance is attributed to the widespread use of new technologies and rising number of data centers. Strong infrastructure development in countries like the U.S. contributed to the regional market growth. The U.S. had the largest share of the North America structured cabling market. Major investments in IT infrastructure, 5G rollout, and cloud computing projects boost the U.S. market expansion. In addition, the presence of key market players like Belden Inc. and Nexans helped North America maintain its lead.

The Asia Pacific structured cabling market is expected to witness the fastest growth in the coming years. Rapid urbanization and expanding IT infrastructure drive the regional market growth. Also, increasing internet access contributes to the growth. A report from Google states that 440 million people (i.e., 75% of the population) are online in Southeast Asia. The active rollout of 5G and large smart city projects propel the market expansion. Also, significant investments in data center construction in India and China are fueling the structured cabling industry in the region. Furthermore, the increasing emphasis on digital transformation raise the demand for structure cabling systems. The growth is also attributed to government efforts to improve broadband connectivity.

Structured Cabling Cost & ROI Analysis

Cable type, network size, installation complexity, and the performance requirement influence the structured cabling cost. Fiber optic cabling has higher initial costs than copper cabling. The cabling offers lower maintenance, greater bandwidth capacity, and scalability for the future. Thus, it provides better long-term returns. Businesses are now focusing more on the total cost of ownership (TCO) when looking at investments in structured cabling, rather than just the upfront installation cost.

| Factor | Cost & ROI Impact |

| Initial Investment | Includes cabling materials, network design, labor, and testing during installation. |

| Maintenance Savings | Standardized structure reduces troubleshooting time and ongoing IT support costs. |

| Downtime Reduction | Reliable cabling improves network uptime, preventing business and revenue losses. |

| Scalability Value | Supports future upgrades without full rewiring, lowering long-term expansion costs. |

| Operational Efficiency | Simplifies moves, adds, and changes, reducing reconfiguration expenses. |

| Long-Term ROI | Delivers lower total cost of ownership and higher performance over the network lifecycle. |

Key Players and Competitive Analysis

Major market players invest heavily in research and development. It helps them expand their offerings. These market participants undertake various strategic activities such as innovative launches and higher investments. They also emphasize international collaborations, and mergers and acquisitions between organizations. These activities assist them in expanding their global footprint.

List of Key Companies

- ABB Ltd

- Belden Inc.

- CommScope Holding Company, Inc.

- Corning Incorporated

- Furukawa Electric Co., Ltd.

- Legrand SA

- Nexans

- Schneider Electric

- Siemens AG

- TE Connectivity

Structured Cabling Industry Developments

- March 2025: Corning advanced its Springboard strategy to drive USD 4 billion in yearly sales by 2026 as generative-AI demand climbs.

- March 2025: Schneider Electric committed USD 700 million to expand US plants and labs through 2027, generating around 1,000 new jobs.

- March 2025: Prysmian Group finalized its USD 950 million takeover of Channell Commercial Corporation, widening its reach in digital-connectivity systems.

- November 2024: Nexans partnered with Sweden-based BIMobject to integrate its products into Building Information Modeling (BIM). It will enable early inclusion in construction designs. The collaboration supports Nexans’ digital transformation strategy.

Analyst Predictions on Structured Cabling Market Future

- Artificial intelligence workloads are expected to accelerate demand for ultra-high-density fiber cabling in hyperscale and enterprise data centers.

- Rising integration of edge computing will drive localized, low-latency cabling deployments across smart factories, hospitals, and retail.

- Increasing adoption of 800G and beyond network architectures will require next-generation cabling systems and connectivity standards.

- Smart buildings and IoT expansion will increase installation of structured cabling across commercial infrastructure.

- Growing emphasis on sustainability goals will propel the demand for energy-efficient, low-loss cabling systems.

- Modular, pre-terminated cabling will gain traction to reduce deployment time and minimize labor costs.

Structured Cabling Market Segmentation

By Product Type Outlook (Revenue, USD Billion, 2021–2034)

- Copper Cabling

- Fiber Optic Cabling

- Coaxial Cables

- Others

By Application Outlook (Revenue, USD Billion, 2021–2034)

- Data Centers

- Local Area Networks (LAN)

- Telecommunication

By Industry Vertical Outlook (Revenue, USD Billion, 2021–2034)

- IT and Telecom

- Healthcare

- Industrial Manufacturing

- Others

By Regional Outlook (Revenue, USD Billion, 2021–2034)

- North America

- U.S.

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Structured Cabling Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 13.94 billion |

| Market Size in 2026 | USD 15.41 billion |

| Revenue Forecast in 2034 | USD 34.74 billion |

| CAGR | 9.5% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2022–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD billion, 2021–2034 and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

The market is expected to register a CAGR of 9.5% during 2026–2034. The market is projected to reach USD 34.74 billion by 2034.

North America led the market in 2025. Rising deployment of 5G, expansion of data centers, and increasing investments in smart infrastructure drove the dominance.

The fiber optic cabling segment held the largest share in 2025. The segment dominance is attributed to its superior data transmission speed and lower signal attenuation.

IT and telecommunications sector leads demand. Cloud computing expansion and 5G rollouts propel the structured cabling installation in the sector.

Fiber optic cables support higher bandwidth and long-distance transmission. It offers low latency and superior data transmission. Due to these advantages, their demand is higher than copper cabling.

Download Sample Report of Structured Cabling Market

Please fill out the form to request a customized copy of the research report.