Transcatheter Aortic Valve Replacement (TAVR) Market Research Report, Size & Forecast by 2026 - 2034

REPORT DETAILS

Transcatheter Aortic Valve Replacement (TAVR) Market Summary

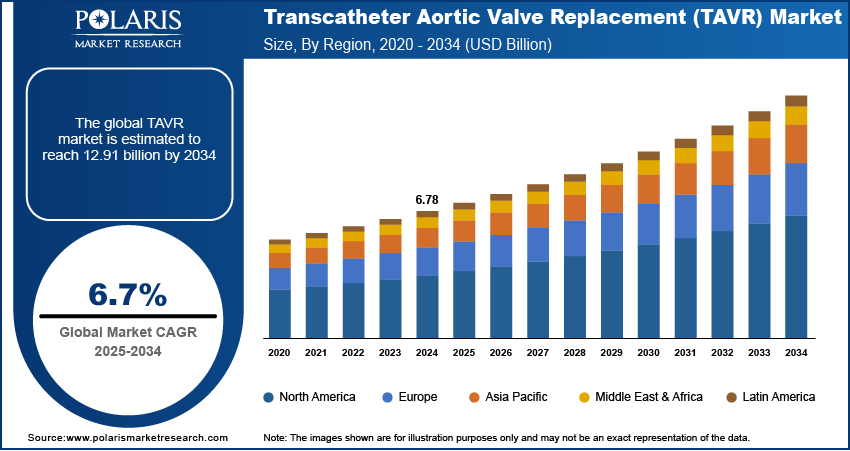

The global transcatheter aortic valve replacement (TAVR) market size was valued at USD 7.21 billion in 2025 and is projected to grow at a CAGR of 6.7% from 2026 to 2034. The growing cases of cardiac valve illnesses together with aging population is boosting the market growth.

Market Statistics

Key Takeaways

- The balloon-expandable segment held a 55.7% revenue share in 2025, driven by high deployment precision and controlled placement.

- The hospital segment held a 75.4% revenue share in 2025, due to the existence of commending compensation policies in both advanced and advancing nations, enhanced healthcare framework, and technological enhancements in TAVR gadgets and apparatus.

- In 2025, the Nitinol segment held a 51.2% revenue share, owing to its shape-memory and superelastic properties and high compatibility with self-expandable TAVR systems.

- North America transcatheter aortic valve replacement (TAVR) market dominated the market with 43.6% market share due to its progressive healthcare system, and surging cases of illnesses such as aortic stenosis, together with evolved healthcare framework that reinforces the acquisition of progressive medical device technologies.

- Europe is projected to grow at a 7.1% CAGR, fueled by speedy economic development, the existence of strict directives, and an escalation in cardiovascular disease cases.

Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations.

Industry Dynamics

- TAVR is less intrusive option to conventional surgical aortic valve replacement (SAVR). Due to this, they are more alluring to both patients and healthcare experts as they cause interim hospital stays, speedier recuperation times, and handful of post operative issues which is propelling the market expansion.

- Inventions such as next-generation valve designs, conveyance systems, and imaging technologies, have rendered TAVR functions secure and more productive thereby fueling the market growth.

- The geriatric population is more susceptible to aortic valve diseases, which pushes the demand for more contemporary cures like TAVR.

- The high cost of transcatheter aortic valve replacement gadgets places a prominent provocation for the market growth.

Source: Polaris Market Research Analysis

What is Transcatheter Aortic Valve Replacement (TAVR)?

Transcatheter aortic valve replacement (TAVR) is a minimally invasive surgical treatment that involves replacing a sick or malfunctioning aortic valve with an artificial valve. TAVR is used to treat aortic stenosis, which occurs when the aortic valve narrows, making it difficult for the heart to pump blood throughout the body. Transcatheter procedures often utilize microcatheters, small flexible catheters for precise navigation and delivery of devices or therapeutics within narrow or tortuous vascular pathways.

The growing incidence of cardiac valve diseases and the implementation of favorable government initiatives are a few of the key factors driving the demand for transcatheter heart valve replacement. The approval of new products by governments worldwide and the benefits of transcatheter technology over surgical valves are also contributing to the expansion of TAVR. TAVR is currently the recommended alternative to traditional open-heart surgery as it is less invasive, has quicker recovery times, and has lower death rates. In addition, the market is being positively impacted by the growing number of obese people and the frequency of congenital cardiac problems.

The rising aging population globally is driving the transcatheter heart valve replacement demand globally. The aging population is more susceptible to aortic valve diseases, which drives the demand for novel treatments like TAVR. Advances in catheter technology, imaging methods, and valve design have increased TAVR's accessibility, safety, and effectiveness. Cutting-edge imaging technologies, including CT scans and 3D echocardiography, allow for precise operation planning and execution, thereby reducing problems and supporting market growth.

TAVR Access Routes

In transcatheter aortic valve replacement (TAVR), different access routes such as transapical, transaortic, and transfemoral are used. The selection of types depends on patient anatomy, vascular condition, and surgical suitability. Transfemoral access is the most commonly preferred due to its minimally invasive nature and faster recovery. Transapical and transaortic approaches are generally more invasive and associated with longer recovery. They are used when femoral access is not feasible.

Comparison Table: Transapical vs Transaortic vs Transfemoral

| Parameter | Transapical (TA) | Transaortic (TAo) | Transfemoral (TF) |

| Access Site | Apex of the left ventricle through small chest incision | Direct access through ascending aorta via upper chest incision | Femoral artery through groin |

| Procedure Type | Surgical/minimally invasive hybrid | Surgical/minimally invasive hybrid | Percutaneous catheter-based |

| Invasiveness | High | Moderate to high | Lowest |

| Type of Anesthesia | General anesthesia | General anesthesia | Often local anesthesia + sedation |

| Hospital Stay | 4–7 days | 3–6 days | 1–3 days |

| Recovery Time | 2–4 weeks | 2–3 weeks | 1–2 weeks |

| Bleeding Risk | Higher | Moderate to high | Lower |

| Vascular Complications | Lower peripheral vascular issues | Moderate | Possible peripheral vascular complications |

| Procedural Risk | Higher | Moderate | Lowest overall |

| Suitable For | Patients unsuitable for peripheral access | Patients with poor femoral access but suitable aortic anatomy | Patients with good femoral artery anatomy |

| Clinical Preference | Declining usage | Selective use | Most preferred and standard approach |

| Postoperative Pain | Higher | Moderate | Lowest |

| Long-Term Outcomes | Less favorable compared to TF | Better than TA in some cases | Most favorable overall |

Source: Polaris Market Research Analysis

Market Dynamics

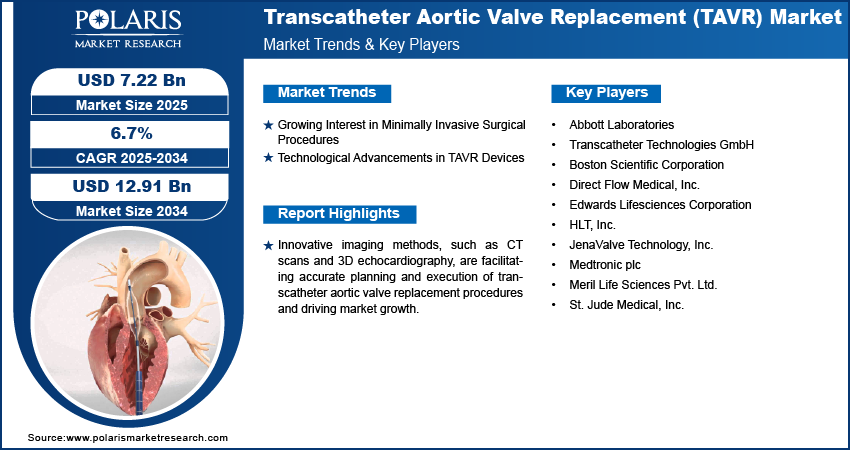

Growing Interest in Minimally Invasive Surgical Procedures

TAVR is a less invasive alternative to traditional surgical aortic valve replacement (SAVR). The less invasive nature of TAVR procedures makes them appealing to both patients and healthcare professionals, as they result in shorter hospital stays, faster recovery times, and fewer post-operative problems. These procedures are highly beneficial for elderly patients and those with several comorbidities. With healthcare systems placing a higher priority on patient-centered and cost-effective methods, there is a growing shift toward minimally invasive procedures like TAVR. Thus, the growing need for minimally invasive surgeries is driving the expansion of TAVR.

Technological Advancements in TAVR Devices

Innovations like next-generation valve designs, delivery systems, and imaging techniques have made TAVR operations safer and more efficient. These developments also help in addressing limitations like durability, convenience of implantation, and anatomical variances among patients. This, in turn, has increased the number of patients who can benefit from TAVR, improved procedural outcomes, and lowered the risk of complications. Thus, technological advancements in TAVR devices are propelling the TAVR revenue.

Source: Polaris Market Research Analysis

Segment Insights

Transcatheter Aortic Valve Replacement Market Evaluation by Mechanism Insights

The market segmentation, based on mechanism, includes self-expandable and balloon-expandable. The balloon-expandable segment led the share with a 57.4% market share in 2025. The non-repositionable, intra-annular architecture and reduced stent frame profile of balloon-expandable TAVR provide easy coronary access. In addition, ballon-expandable TAVR has a more steerable delivery mechanism as opposed to self-expanding devices, making it highly beneficial for patients with complicated vascular anatomy, such as a horizontal aorta. The introduction of several innovative ballon-expandable TAVR products by key compnies also contributes to the segment’s leading position.

The self-expandable segment is projected to witness significant growth during the forecast period. Most self-expanding valves are supra-annular, which reduces the rate of severe prosthesis-patient mismatch (PPM), lowers gradients, and increases the effective orifice area. Major manufacturers are also focusing on advanced product development, which contributes to the growth of the segment.

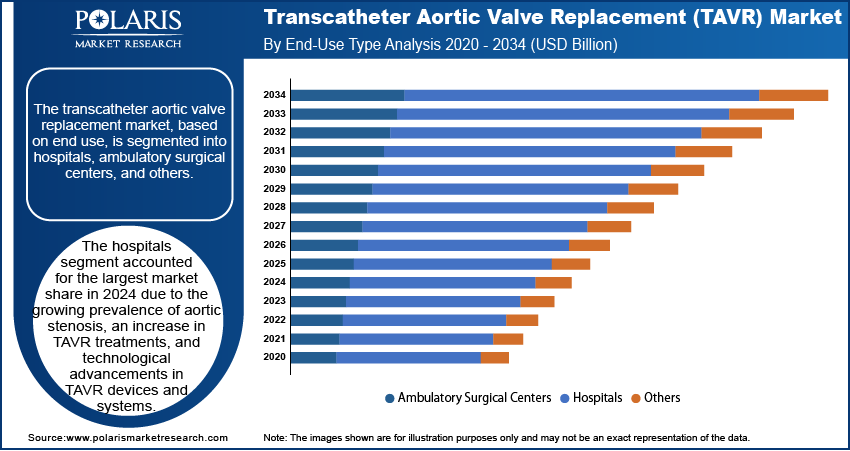

Assessment by End Use Insights

Based on end use, the market is segmented into ambulatory surgical centers, hospitals, and others. The hospitals segment dominated the market with the largest revenue share of 89.4% in 2025. The segment’s dominance is largely attributed to the presence of favorable reimbursement policies in both developed and developing nations, improved healthcare infrastructure, and technological improvements in TAVR devices and systems.

The ambulatory surgical centers segment is projected to witness the fastest growth during the forecast period. These facilities have reduced overhead, fixed costs, and shorter stays than hospitals, which makes them more affordable and drives the segment’s growth.

Source: Polaris Market Research Analysis

Transcatheter Aortic Valve Replacement Market Regional Analysis

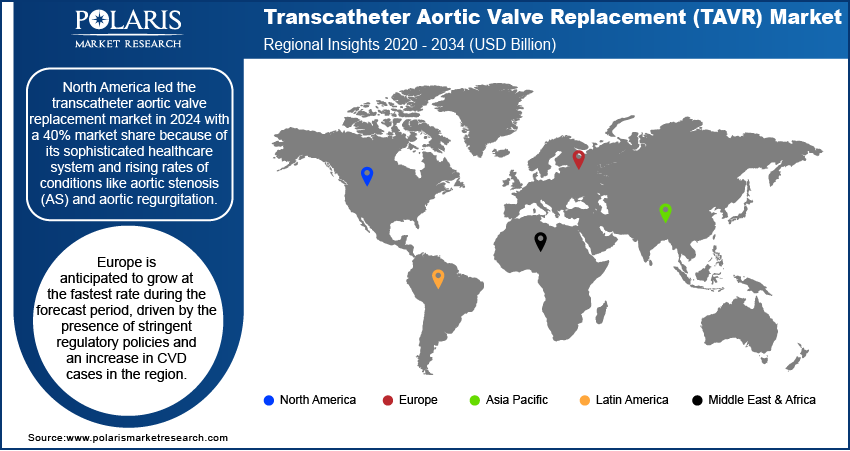

By region, the report provides the market insights into North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa. North America led the global market with a 40% revenue share in 2025, driven by its advanced healthcare system and rising incidence of diseases like aortic stenosis, coupled with a well-developed healthcare infrastructure that supports the adoption of advanced medical device technologies.

The Europe transcatheter aortic valve replacement market is expected to witness the fastest growth during the forecast period. The region’s robust growth is driven by several factors, including rapid economic development, the presence of stringent regulations, and an increase in cardiovascular disease (CVD) cases. For instance, a May 2024 article from the World Health Organization highlighted that CVD accounts for over 42.5% of all yearly deaths in Europe, or around 10,000 deaths every day, making it the primary cause of disability and premature death. Besides, the introduction of new, innovative products in the EU has made TAVR more accessible, thereby contributing to the regional development.

The Asia Pacific region is experiencing strong growth in the transcatheter aortic valve replacement (TAVR) market, driven by an aging population and rising cases of aortic stenosis. Countries such as China, India, and South Korea are expanding access to advanced heart procedures. Although Japan is often viewed separately, its influence on the regional market is notable through the demand and innovation surrounding Japan’s transcatheter heart valve products, thereby driving the growth of TAVR in Asia Pacific.

Japan's transcatheter heart valve replacement market is experiencing significant growth due to its advanced healthcare system and rapidly aging population. The high rate of aortic valve disease among elderly patients has significantly increased demand for transcatheter heart valve replacement, including transcatheter aortic valves. Hospitals across the country have quickly adopted TAVR procedures, making Japan transcatheter heart valves a standard in minimally invasive heart treatments. Strong insurance coverage, well-trained specialists, and a focus on innovation continue to drive growth.

Source: Polaris Market Research Analysis

Key Players and Competitive Insights

Leading market players are investing heavily in research and development to expand their offerings, which will help the market grow even more. These participants are also undertaking a variety of strategic activities, such as innovative product launches, international collaborations, higher investments, and mergers and acquisitions to expand their global footprint. To expand and survive in a more competitive climate, companies must offer cost-effective solutions.

The transcatheter aortic valve replacement market faces competition from major global players. These players dominate with their extensive production capacities and advanced technologies. Competition is further heightened by fluctuating raw material prices, stringent environmental regulations, and the necessity for technological advancements to improve device efficiency. A few major players are Boston Scientific Corporation; Direct Flow Medical, Inc.; Edwards Lifesciences Corporation; HLT, Inc.; Abbott Laboratories; JenaValve Technology, Inc.; Medtronic plc; Meril Life Sciences Pvt. Ltd.; St. Jude Medical, Inc.; Medtronic; and Transcatheter Technologies GmbH.

Abbott Laboratories, established in 1888 and based in Abbott Park, Illinois, is a multinational healthcare company operating in more than 160 countries with about 114,000 employees as of 2024. The company develops and manufactures a variety of healthcare products, including medical devices, diagnostics, branded generic pharmaceuticals, and nutritional products. In 2013, Abbott separated its research-based pharmaceuticals division into a new company, AbbVie, but continues to produce branded generics primarily in emerging regions. Abbott’s operations are divided into four main segments. The Pharmaceuticals segment provides prescription medications for cardiovascular diseases, metabolic disorders, infectious diseases, immunology, and neurology. This segment includes lipid management therapies developed with AstraZeneca, diabetes care products, and biosimilars. The Diagnostics segment offers in-vitro diagnostic systems and tests used for disease detection and monitoring. Its products include immunoassay systems like ARCHITECT and AxSYM, molecular diagnostics under the Vysis brand, point-of-care testing devices such as the i-STAT system, and diabetes monitoring tools branded FreeStyle. The Nutritional Products segment supplies nutrition for infants, adults, and individuals with special dietary needs, with brands such as Similac, Ensure, and Glucerna. The Medical Devices segment produces cardiovascular care devices, including coronary stents (Xience V), carotid stents (Acculink, Accunet), vessel closure devices (StarClose), and balloon dilation products (Voyager), as well as devices related to heart failure, electrophysiology, neuromodulation, and diabetes management. Abbott’s global presence spans North America, Latin America, Europe, the Middle East, Asia Pacific, and Africa. The company maintains manufacturing and research facilities in countries including the United States, Colombia, India, Singapore, Spain, and the United Kingdom. Key regions for Abbott include Germany, China, India, Switzerland, Japan, and the Netherlands.

Medtronic plc is a developer, manufacturer, and seller of device-based medical therapies. The company's business operations are divided into the Cardiovascular Portfolio, Medical Surgical Portfolio, Neuroscience Portfolio, and Diabetes Operating Unit. Medtronic's cardiovascular portfolio segment specializes in implantable cardiac devices such as defibrillators, pacemakers, and resynchronization therapy devices. Additionally, it offers insertable cardiac monitor systems, cardiac ablation products, TYRX products, and remote patient-centered and monitoring software. The Medical Surgical Portfolio segment provides a range of surgical products, including vessel sealing instruments, surgical stapling devices, wound closure and electrosurgery products, hernia mechanical devices, surgical artificial intelligence and robotic-assisted surgery products, mesh implants, lung products, gynecology, and various therapies to treat diseases. It also offers products in the fields of minimally invasive gastrointestinal and hepatologic diagnostics and therapies. The Neuroscience Portfolio segment offers products for various medical professionals, including neurosurgeons, spinal surgeons, neurologists, anesthesiologists, pain management specialists, orthopedic surgeons, urologists, interventional radiologists, urogynecologists, and throat specialists. The segment also provides intra-operative imaging systems, image-guided surgery systems, and robotic guidance systems used in robot-assisted spine procedures. The Diabetes Operating Unit segment specializes in continuous glucose monitoring systems, insulin pumps, and consumables, smart insulin pen systems, and consumables and supplies.

List of Key Companies

- Abbott Laboratories

- Boston Scientific Corporation

- Direct Flow Medical, Inc.

- Edwards Lifesciences Corporation

- HLT, Inc.

- JenaValve Technology, Inc.

- Medtronic plc

- Meril Life Sciences Pvt. Ltd.

- St. Jude Medical, Inc.

- Transcatheter Technologies GmbH

Transcatheter Aortic Valve Replacement Industry Developments

- March 2026: Emboline, Inc. announced positive results from its pivotal PROTECT H2H global clinical trial. The trial evaluated the Emboliner® Embolic Protection System in patients undergoing transcatheter aortic valve replacement (TAVR). The company presented these results as a Late-Breaking Clinical Trial at the American College of Cardiology's Annual Scientific Session & Expo (ACC 2026). These findings support the potential for a new standard of embolic protection in TAVR. (Source: PRNewswire)

- March 2026: Emboline, Inc. announced it had closed $20 Million in growth capital from Trinity Capital, a leading international alternative asset manager. Through this, Emboline plans to support the commercialization of the Emboliner® Embolic Protection System to Minimize Stroke Risk From TAVR. (Source: PRNewswire)

- November 2024: Abbott announced the first patient procedures with its investigational transcatheter aortic valve implantation (TAVI) balloon-expandable system. The company stated that the system is a first step toward creating a TAVI platform that is AI-integrated and software-guided. In addition to the commercially available Navitor TAVI system, this innovation will expand Abbott's structural heart portfolio and give doctors another treatment option. (Source: abbott.mediaroom.com)

- August 2024: Boston Scientific received CE Mark approval for their Acurate Prime TAVR system, which is intended for patients with severe aortic stenosis. It is based on the Acurate Neo2 platform and has a better valve frame, improved valve sizes for larger anatomies, and faster, controlled deployment. (Source: bostonscientific.com)

Future of TAVR Market

The transcatheter aortic valve replacement (TAVR) market is expected to grow significantly during the forecast period. Clinical indications expand beyond high-risk elderly patients to include intermediate- and low-risk populations. Increasing adoption among younger patients will drive demand for improved long-term valve durability and lifetime management strategies. Technological advancements in next-generation valves are enhancing precision. They help in reducing complications such as paravalvular leak and pacemaker implantation, and improving procedural outcomes. AI-assisted imaging, procedural planning, and robotic solutions are being adopted. They will transform TAVR selection, personalized treatment, and greater procedural efficiency.

Transcatheter Aortic Valve Replacement Market Segmentation

By Mechanism Outlook

- Self-Expandable

- Balloon-Expandable

By Material Outlook

- Stainless Steel

- Cobalt Chromium

- Nitinol

- Others

By Procedure Outlook

- Transapical

- Transaortic

- Transfemoral

By End Use Outlook

- Ambulatory Surgical Centers

- Hospitals

- Others

By Regional Outlook

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Transcatheter Aortic Valve Replacement Market Report Scope

| Report Attributes | Details |

| Market Size Value in 2025 | USD 7.21 billion |

| Market Size Value in 2026 | USD 7.67 billion |

| Revenue Forecast by 2034 | USD 12.92 billion |

| CAGR | 6.7% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Transcatheter Aortic Valve Replacement (TAVR) Market FAQ's

The transcatheter aortic valve replacement market was valued at USD .21 billion in 2025 and is projected to grow to USD 12.92 billion in 2034.

The market is projected to register a CAGR of 6.7% during the forecast period.

North America held the largest market share in 2025.

Boston Scientific Corporation; Direct Flow Medical, Inc.; Transcatheter Technologies GmbH; Edwards Lifesciences Corporation; HLT, Inc.; St. Jude Medical; Medtronic, and Abbott Laboratories are a few of the key players in the market.

The hospitals segment dominated the market in 2025.

The balloon-expandable segment held the largest market share in 2025.

Download Sample Report of Transcatheter Aortic Valve Replacement (TAVR) Market

Please fill out the form to request a customized copy of the research report.