U.S. Automotive Market Size, Share Report 2026-2034

REPORT DETAILS

U.S. Automotive Market Summary

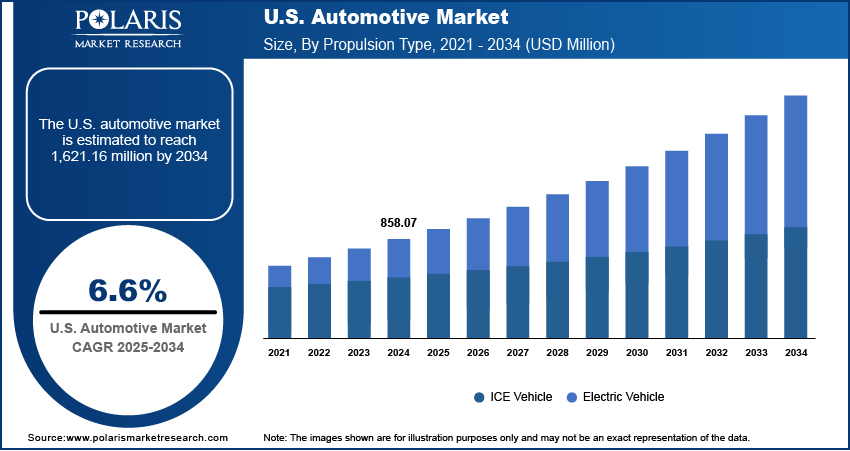

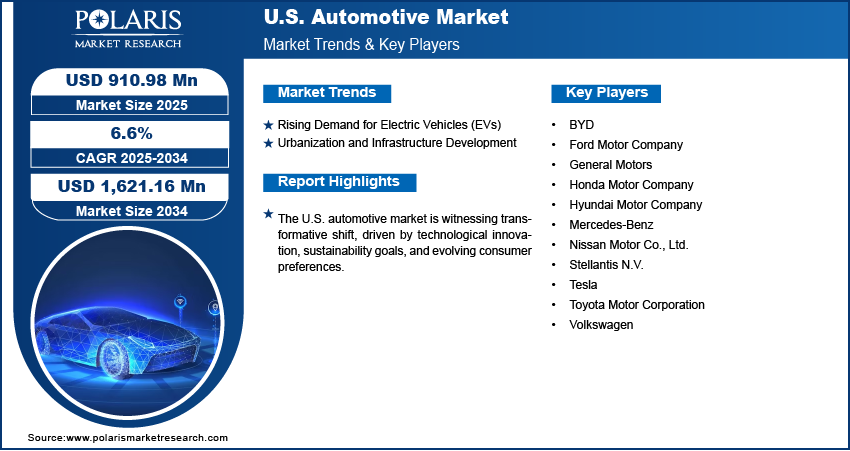

The U.S. automotive market size was valued at USD 914.30 million in 2025, growing at a CAGR of 6.6% from 2025 to 2034. The growth is being shaped by automaker investments in high-demand segments such as crossovers, SUVs, and pickups, alongside advancements in software-defined vehicles and smart manufacturing. Rising demand for electric vehicles (EVs) is further transforming the industry, supported by improving affordability and expanded credit availability.

Market Statistics

Key Takeaways

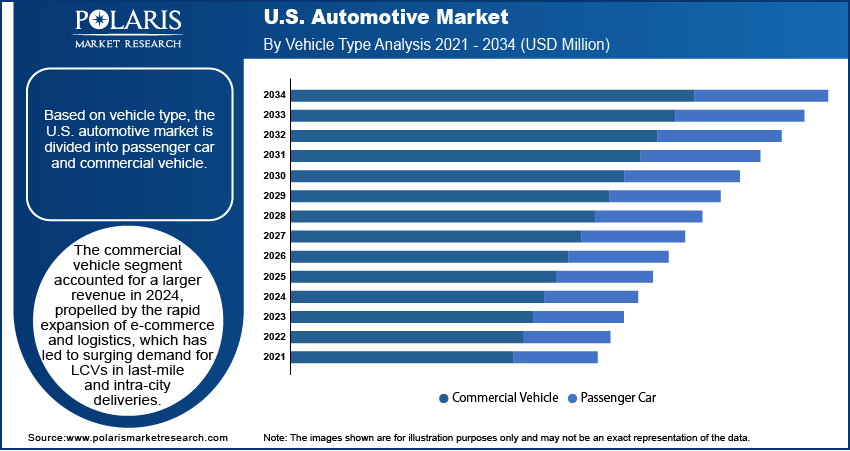

- The commercial vehicle segment is expected to grow fastest at a CAGR of 7.1%. This is due to rising demand from e-commerce, logistics, and infrastructure development activities.

- The passenger car segment dominated the revenue share of 60.6% in 2025. Growth is driven by rising personal mobility demand and increasing adoption of advanced vehicle features.

- By propulsion type, the ICE vehicle segment accounted for the largest revenue share of 54.0% in 2025. The segment held the dominant share due to established fuel infrastructure and high adoption of conventional vehicles.

- The electric vehicle segment is expected to witness the fastest CAGR of 12.7% during 2026–2034. The growth is supported by government incentives, battery advancements, and expanding charging infrastructure.

*Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations.

Industry Dynamics

- Rising demand for electric vehicles (EVs) is supporting U.S. automotive market growth. Increasing environmental awareness and government support are accelerating EV adoption.

- Advancements in battery technologies such as solid-state batteries and lithium-sulfur chemistries are improving EV efficiency and performance. These developments are supporting wider EV adoption.

- Improving vehicle affordability is increasing access to vehicle ownership across a broader consumer base. Competitive pricing and government incentives are supporting demand growth.

- Expanding credit availability through flexible financing options and low-interest loans is supporting vehicle sales. Easier financing is helping consumers manage vehicle purchases more effectively.

AI Impact on U.S. Automotive Market

- AI-powered driver assistance systems are improving vehicle safety, navigation, and driving efficiency.

- AI integration is supporting predictive maintenance and reducing unexpected vehicle breakdowns and repair costs.

- Automakers are using AI to improve manufacturing efficiency, quality control, and production scalability.

- AI-enabled autonomous driving technologies are accelerating innovation in connected and self-driving vehicles.

U.S. Automotive Market Definition

The automotive sector refers to the industry involved in the design, development, manufacturing, and sale of motor vehicles. In the U.S., the market is experiencing momentum, driven by automaker investments in high-demand vehicle segments, including crossovers, SUVs, and pickup trucks. These vehicle types continue to align with consumer preferences for performance, space, and versatility, driving consistent demand. Manufacturers are strategically expanding model offerings in these categories, balancing utility with enhanced comfort and advanced in-vehicle features. This targeted investment approach supports sales volume and also strengthens brand loyalty and market competitiveness.

Source: Polaris Market Research Analysis

Advancements in automotive manufacturing are reshaping the industry’s operational framework. Automation, digitized production lines, and the emergence of software-defined vehicles are revolutionizing the engineering and assembly of vehicles. Automakers are increasingly adopting integrated software platforms that enable real-time updates and enhanced vehicle functionality post-sale, thereby creating new value streams. For instance, in April 2025, Nissan announced that it will introduce next-gen ProPILOT in FY2027, combining its Ground Truth Perception Lidar with Wayve's AI Driver software. The system enhances collision avoidance and adapts to complex driving scenarios using AI learning, advancing autonomous capabilities. These innovations optimize production efficiency, reduce complexity, and enable more agile responses to market changes. Therefore, as the industry moves toward more connected and intelligent vehicles, advanced manufacturing technologies serve as a major enabler of long-term growth and competitiveness in the U.S. market.

Rise of Electric Vehicles in the U.S.

Electric vehicle adoption is increasing across the U.S. due to growing sustainability goals and supportive government policies. Automakers are expanding EV production and investing in battery technologies and charging infrastructure. Rising consumer awareness about carbon emissions and fuel efficiency is also supporting the shift toward electric mobility in passenger and commercial vehicles.

Industry Dynamics

Rising Demand for Electric Vehicles (EVs)

Consumers and governments are prioritizing energy efficient transportation solutions, leading to a rise in EV adoption across the U.S. According to a 2024 IEA report, electric car registrations in the country reached 1.4 million units in 2023, reflecting a growth of over 40% year-over-year, highlighting accelerating consumer adoption of EVs. Automakers are investing heavily in battery technology, electric vehicle charging infrastructure, and production scalability to meet this growing demand driven by the shift toward sustainable mobility and the need to reduce carbon emissions. Additionally, advancements in battery efficiency, such as solid-state batteries, nickel-rich cathodes, lithium-sulfur chemistries, and composite materials, aim to improve energy storage efficiency in compact, lightweight designs for advanced applications. Also, cost reduction is making EVs more accessible to a broader market. This transition is reshaping vehicle design, supply chains, and manufacturing processes, positioning EVs as a central component of the industry's future. As environmental regulations become stricter, the automotive sector is accelerating its shift toward electrification to align with long-term sustainability goals. Thus, rising EV demand propels the U.S. automotive market expansion.

Improving Vehicle Affordability and Expanding Credit Availability

Improving vehicle affordability and expanding credit availability are driving growth opportunities, as they directly influence consumer purchasing power and access to credit. Vehicles become attainable to a broader demographic as manufacturers introduce more competitively priced models across various segments. At the same time, the availability of flexible financing options, low-interest loans, and extended repayment plans makes it easier for consumers to manage large-ticket purchases. For instance, the U.S. federal EV tax credit provides up to USD 7,500 for qualifying new plug-in electric vehicles through 2032. Eligibility depends on income ranging from USD 150,000 to USD 300,000 (based on filing status), vehicle price caps, and specific requirements for sourcing battery components and critical minerals. This combination enables first-time vehicle ownership and also boosts repeat purchases and upgrades. These factors help sustain consistent demand across both new and pre-owned vehicle segments by lowering financial barriers. Furthermore, they support stable production volumes and strengthen the overall resilience of the automotive ecosystem.

Source: Polaris Market Research Analysis

Changing Consumer Preferences

Consumer preference is shifting toward SUVs, pickup trucks, and hybrid vehicles across the U.S. market. Buyers are increasingly prioritizing larger vehicles with advanced safety, comfort, and connectivity features. Rising fuel efficiency awareness is also supporting demand for hybrid models. Automakers are expanding their SUV and hybrid portfolios to match changing consumer demand.

Segmental Insights

Vehicle Type Analysis

The segmentation, based on vehicle type, includes passenger car and commercial vehicle. The commercial vehicle segment is expected to witness fastest growth at a CAGR of 7.1%, propelled by the rapid expansion of e-commerce and logistics, which has led to surging demand for LCVs in last-mile and intra-city deliveries. E-retailers and logistics companies are continuously expanding their fleets to meet faster delivery timelines and service growing online consumer bases. Additionally, industrialization and infrastructure development, driven by rising government spending, are stimulating demand for medium- and heavy-duty vehicles. According to the Council on Foreign Relations, the IIJA in the U.S. included USD 550 billion in spending to upgrade physical infrastructure, such as roads, bridges, railways, airports, and water systems. These vehicles are crucial for transporting raw materials, machinery, and finished goods over long distances.

Propulsion Type Analysis

The segmentation, based on propulsion type, includes ICE vehicle and electric vehicle. The electric vehicle segment is expected to witness the fastest growth at a CAGR of 12.7% during the forecast period, driven by increasing environmental awareness and supportive regulatory policies promoting clean energy transportation. Advancement in battery technology, improved charging infrastructure, and cost reductions in EV components are making EVs more affordable and efficient. Automakers are accelerating their electrification strategies, expanding EV portfolios to meet rising consumer demand. Public investment in EV charging infrastructure is expanding rapidly, making EV ownership more feasible and attractive for consumers and fleet operators. Additionally, strict emissions regulations and incentives for EV adoption are boosting U.S. automotive market growth. Therefore, as global efforts to achieve carbon neutrality amplify, the transition to electric mobility is expected to gain effective momentum, driving the rapid expansion of the EV segment.

Source: Polaris Market Research Analysis

Key Players and Competitive Analysis

The U.S. automotive sector is witnessing competition as traditional OEMs confront disruptions from electric vehicle pioneers and technology companies. Ford, General Motors, and others are making strategic investments in electrification and autonomous technologies to counter the dominance of emerging manufacturers. Revenue opportunities are shifting toward software-defined vehicles and subscription services, with competitive intelligence revealing that technology partnerships have become critical differentiators. Small and medium-sized businesses specializing in EV components and semiconductor solutions are capturing a significant share of the vendor market as supply chain disruptions force OEMs to diversify their supplier networks. Economic and geopolitical shifts, particularly trade tensions with China, are accelerating domestic manufacturing investments and reshoring initiatives. Sustainable value chains have emerged as competitive advantages, with companies such as GM and Ford investing heavily in circular economy practices. Industry trends show consolidation through joint ventures and mergers, particularly in autonomous driving capabilities.

A few key players are BYD; General Motors; Honda Motor Company; Hyundai Motor Company; Mercedes-Benz; Nissan Motor Co., Ltd.; Stellantis N.V.; Suzuki Motor Corporation; Tesla; Toyota Motor Corporation; and Volkswagen.

Key Players

- BYD

- Ford Motor Company

- General Motors

- Honda Motor Company

- Hyundai Motor Company

- Mercedes-Benz

- Nissan Motor Co., Ltd.

- Stellantis N.V.

- Tesla

- Toyota Motor Corporation

- Volkswagen

Industry Developments

- April 2026: Subaru unveiled the all-electric 2027 Subaru Getaway. The SUV offers 420 horsepower, over 300 miles of range, and standard all-wheel drive. (Source: prnewswire.com)

- April 2026: Kia showcased the all-new Seltos SUV, 2027 EV3, and PV5 WAV accessible mobility concept at the New York International Auto Show. (Source: worldwide.kia.com)

- June 2025: General Motors delivered the first hand-built Cadillac CELESTIQ to its owner in a private ceremony at the General Motors Global Technical Center. (Source: gm.com)

- March 2025: Hyundai Motor Group planned a USD 21 million investment in the U.S. through 2028, allocating USD 9 million for production expansion to 1.2 million annual units, USD 6 million for supply chain localization, and USD 6 million for future technologies and charging infrastructure development. (Source: hyundai.com)

Future Outlook

The U.S. automotive market is expected to grow steadily with rising vehicle electrification and connected vehicle technologies. Increasing demand for commercial fleets and logistics vehicles is supporting market expansion. Advancements in autonomous driving technologies are creating new growth opportunities. Automakers are also investing in smart manufacturing and digital mobility solutions to improve production efficiency and vehicle performance.

U.S. Automotive Market Segmentation

By Vehicle Type Outlook (Revenue, USD Million, 2021–2034)

- Passenger Car

- Hatchback

- Sedan

- SUV

- MUV

- Commercial Vehicle

- LCVs

- Heavy Trucks

- Buses & Coaches

By Propulsion Type Outlook (Revenue, USD Million, 2021–2034)

- ICE Vehicle

- Electric Vehicle

U.S. Automotive Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 914.30 million |

| Market Size in 2026 | USD 974.38 million |

| Revenue Forecast by 2034 | USD 1,630.86 million |

| CAGR | 6.6% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Million and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

FAQ's

The market size was valued at USD 914.30 million in 2025 and is projected to grow to USD 1,630.86 million by 2034.

The market is projected to register a CAGR of 6.6% during the forecast period.

A few of the key players in the market are BYD; General Motors; Honda Motor Company; Hyundai Motor Company; Mercedes-Benz; Nissan Motor Co., Ltd.; Stellantis N.V.; Suzuki Motor Corporation; Tesla; and Toyota Motor Corporation; and Volkswagen.

The passenger car segment dominated the revenue share of 60.6% in 2025.

The ICE vehicle segment accounted for the largest revenue share of 54.0% in 2025.

The U.S. automotive market includes the production, distribution, and sale of passenger and commercial vehicles across the country.

The U.S. auto industry is one of the largest automotive industries globally, supported by strong vehicle production, sales, and manufacturing activities.

Major vehicle segments include passenger cars, SUVs, pickup trucks, light commercial vehicles, and heavy commercial vehicles.

Download Sample Report of U.S. Automotive Market

Please fill out the form to request a customized copy of the research report.