U.S. Cardiovascular Device Market Opportunity, Demand, Report, 2026-2034

REPORT DETAILS

U.S. Cardiovascular Devices Market Summary and Key Insights

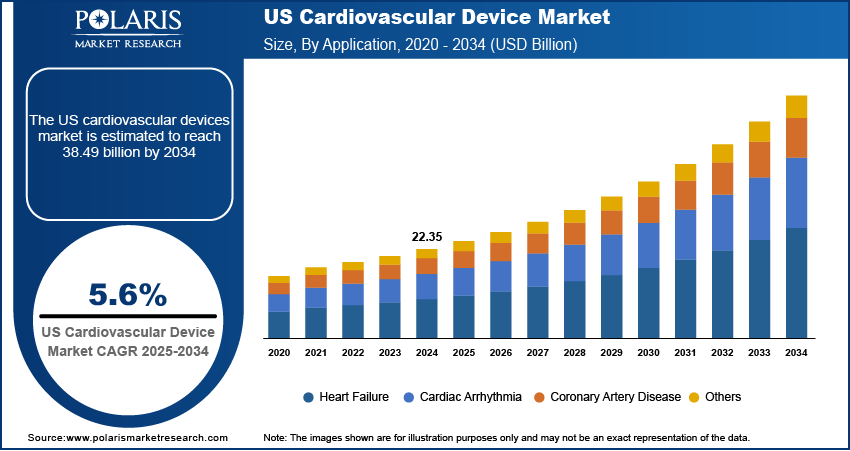

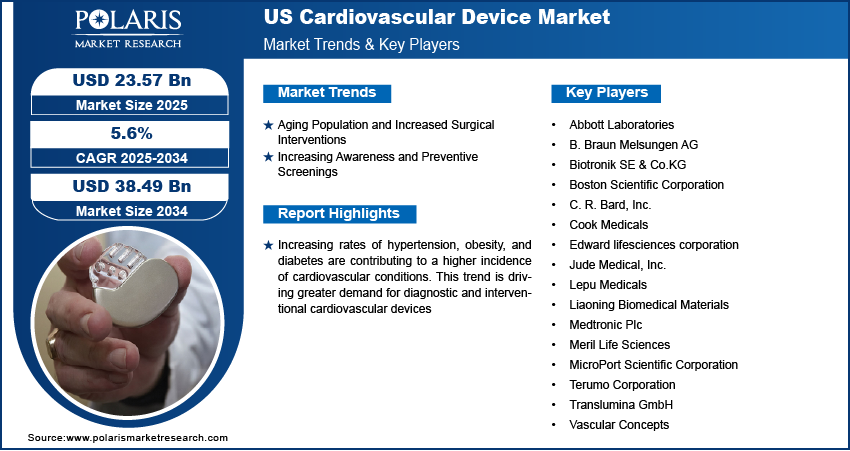

The U.S. cardiovascular device market size was valued at USD 23.57 billion in 2025 and is projected to register a CAGR of 5.60% from 2026 to 2034.

Market Statistics

U.S. Cardiovascular Devices Market Key Takeaways

- The Therapeutic & Surgical Devices segment accounted for a 61.40% revenue share in 2025. This is due to the rising number of interventional cardiology procedures and increasing adoption of minimally invasive cardiovascular treatments.

- The Diagnostics & Monitoring Devices segment is expected to register the highest CAGR of 8.80% during the forecast period. The segment’s growth is driven by the increasing emphasis on early disease detection, continuous patient monitoring, and AI-enabled diagnostic technologies.

- The Coronary Artery Disease segment accounted for the largest revenue share of 36.90% in 2025. This is owing to its widespread prevalence across the adult population and growing demand for coronary intervention devices.

- The Cardiac Arrhythmia segment is expected to witness the fastest growth at a CAGR of 9.60%. The segment’s growth is driven by the increasing incidence of atrial fibrillation and ventricular tachycardia among both older and younger populations.

- The Hospitals segment accounted for a 68.30% market share in 2025. The comprehensive infrastructure of hospitals, availability of advanced cardiac care facilities, and higher procedural volumes contribute to the segment’s leading position.

Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations.

Industry Dynamics

- A rising aging population susceptible to cardiovascular conditions drives the need for cardiovascular devices in the US.

- Efforts to raise awareness about cardiovascular health through public health campaigns and wellness programs are driving the US cardiac devices market growth.

- The robust healthcare spending in the US creates several market opportunities.

- High cost of advanced devices and procedures may present market challenges.

AI Impact on U.S. Cardiovascular Device Market

- AI assists in improving equipment from the cardiovascular medical devices market by allowing real-time monitoring of heart health and patients’ general well-being.

- This technology helps in early detection of any heart diseases through analysis of information from diagnostic and implantable devices.

- AI assists in making faster treatment decisions using predictive analytics and information analysis techniques.

- AI enables better patient monitoring, device performance, and preventive care through continuous information analysis.

Source: Polaris Market Research Analysis

To Understand More About this Research: Download Sample Report

Cardiovascular Devices in Simple Terms

Cardiovascular devices are tools that are used by medical professionals for the detection, treatment, and management of illnesses relating to the heart and the blood vessels. Some of these devices include pacemakers, stents, heart monitors, defibrillators, and imaging systems used for diagnosing heart-related illnesses.

How Cardiovascular Devices Support Patient Care?

Patient Evaluation and Diagnosis: Patients receive physical exams, imaging, and heart monitoring in order to detect cardiovascular diseases such as coronary artery disease, arrhythmias, or heart failure.

Evaluation of the Cardiac Condition: Practitioners assess the severity of the disease and choose the best course of action, considering the symptoms and medical history of the patient as well as the results of the diagnosis.

Device Selection: The most suitable cardiovascular device is selected. It can include stents, pacemakers, defibrillators, heart valves, and monitoring devices, among other options.

Placement of Device or Procedure: The selected device is implanted surgically or used in a minimally invasive procedure for achieving restoration of normal heart function and improving blood flow and/or heart monitoring continuously.

Monitoring After Procedure: Patients are monitored after the procedure through check-ups, imaging, and remote heart monitoring to ensure that everything is working fine.

Disease Management Over Long Periods: Most cardiovascular devices continue assisting patients suffering from different heart diseases for a long period because of the capability of monitoring the heart, reducing risks, and managing the disease.

Increasing rates of hypertension, obesity, and diabetes are contributing to a higher incidence of cardiovascular conditions. This trend is driving greater demand for diagnostic and interventional cardiovascular devices across hospitals, clinics, and ambulatory centers to improve treatment outcomes and reduce mortality.

A cardiovascular device is a medical instrument or implant used to diagnose, treat, or manage heart and blood vessel-related conditions. These devices include pacemakers, stents, heart valves, and defibrillators, all designed to improve heart function and prevent or manage cardiovascular diseases. Various cardiovascular devices such as pacemakers, vascular stents, and heart valves are essential for treating and managing conditions such as heart failure, arrhythmias, and coronary artery disease. Innovations such as AI-based diagnostic tools, next-gen stents, leadless pacemakers, and wearable cardiac monitors are transforming disease management. These advancements are improving early detection, patient monitoring, and treatment precision, making newer devices more appealing to both providers and patients. In June 2024, AliveCor launched the Kardia 12L ECG System, featuring AI-powered technology, which detects 35 cardiac conditions using a reduced lead, revolutionizing cardiac care. These developments make devices more effective, safer, and user-friendly, boosting demand for advanced cardiovascular technologies and thereby driving the U.S. cardiovascular device market growth

Supportive reimbursement frameworks from Medicare and Medicaid for cardiovascular procedures and devices are enhancing affordability and access. Regulatory pathways encouraging faster approval of innovative cardiac technologies also promote faster adoption across healthcare systems. Additionally, sedentary lifestyles, poor diets, and stress are contributing to a surge in heart conditions among younger demographics. This shift is prompting early interventions using wearable heart monitors, smart diagnostic systems, and implantable devices to manage long-term risk.

Cardiovascular Devices vs Traditional Cardiac Treatment

| Factor | Conventional Cardiac Treatment | Advanced Cardiovascular Devices |

| Method of Treatment | Mostly medication and conventional surgical approach | Diagnostic, monitoring and intervention through devices |

| Patient Monitoring | Regular visits to hospital or clinics | Constant monitoring using implanted and portable devices |

| Type of Procedure | Frequently includes more invasive procedures | Tends to use minimally invasive approaches |

| Duration of Recovery | Includes lengthy hospital stay and recuperation | Tends to enable quicker recovery and shorter stay in hospital |

| Level of Accuracy | Depends mostly on clinical judgment | Improved with the help of advanced diagnostics and monitoring |

Source: Polaris Market Research Analysis

Market Dynamics

Rising Aging Population Susceptible to Cardiovascular Conditions

The rising proportion of older adults in the U.S. is leading to a growing number of patients affected by cardiovascular conditions such as arrhythmias, aortic stenosis, and coronary artery disease. According to the Population Reference Bureau, the U.S. demographic of individuals aged 65 and above is anticipated to grow significantly from 58 million in 2022 to 82 million by 2050, reflecting a 47% increase. Older individuals often require surgical procedures, including pacemaker implantation, angioplasty, and valve replacement, to manage these conditions effectively. This demographic shift is creating sustained demand for high-performance cardiovascular devices that are durable and also compatible with minimally invasive techniques. Manufacturers are focusing on developing compact and precise devices that reduce surgical risks and improve recovery times for elderly patients. Hospitals and cardiac centers are also increasing investments in advanced technologies to cater to the specific needs of geriatric populations, further fueling U.S. cardiovascular device market expansion.

Increasing Awareness and Preventive Screenings

Efforts to raise awareness about cardiovascular health through public health campaigns and wellness programs are encouraging more people to undergo regular heart screenings. Early testing for blood pressure, cholesterol, and ECG abnormalities is becoming common, prompting earlier detection of potential issues before they become severe. Patients are also becoming more proactive in managing their heart health, leading to a rise in the use of noninvasive diagnostic tools and wearable medical devices. Healthcare providers are expanding preventive care services and using data-driven insights to tailor treatment strategies. The importance of prevention is reducing hospital admissions for advanced conditions while driving demand for precise, easy-to-use diagnostic cardiovascular devices.

Integration of Advanced Technologies in Cardiovascular Devices

Modern technological innovations have helped in making heart disease diagnosis and treatment more accurate. AI-driven diagnostic tools make it easier for physicians to diagnose heart-related illnesses, whereas wearable cardiac monitors help track heart health outside the hospital. Robotic surgical procedures enhance precision in cardiovascular surgery, and modern imaging techniques help develop an appropriate treatment strategy for the illness.

Sustainability Trends in Cardiovascular Devices

Sustainability is gaining prominence in the market for cardiovascular devices as companies seek means to become more environmentally friendly. Manufacturers have improved processes to cut waste and use resources more efficiently. The use of implants that last longer reduces the need for patient replacements. Similarly, digital monitoring tools are helping to cut down on unnecessary trips to the hospital. Moreover, improved device life cycle management and recycling practices are making cardiovascular medicine more sustainable.

Source: Polaris Market Research Analysis

U.S. Cardiovascular Devices Market Segment Analysis

U.S. Cardiovascular Devices Market, by Device Type

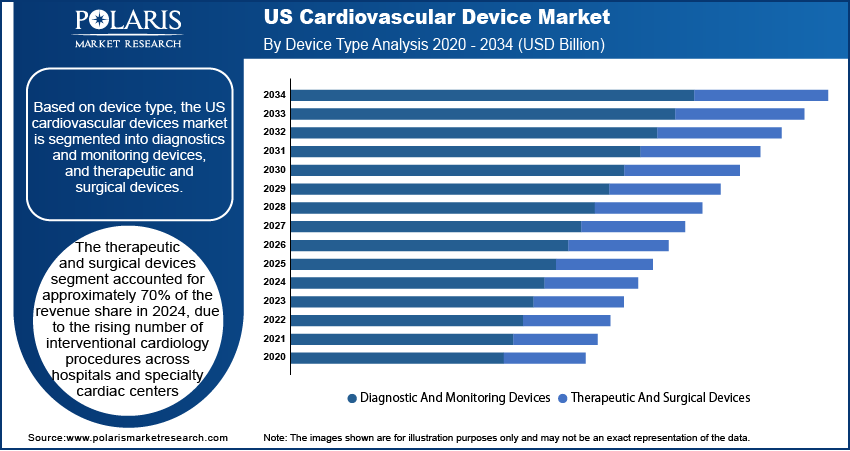

Based on device type, the U.S. cardiovascular device market is segmented into diagnostics and monitoring devices, and therapeutic and surgical devices. The therapeutic and surgical devices segment accounted for approximately 70% of the revenue share in 2024 due to the rising number of interventional cardiology procedures across hospitals and specialty cardiac centers. The growing prevalence of complex heart conditions such as coronary artery disease, valve disorders, and arrhythmias is leading to increased use of stents, pacemakers, implantable defibrillators, and valve repair devices. According to the National Library of Medicine, Coronary artery disease (CAD) is responsible for an estimated 610,000 fatalities each year, representing roughly 25% of all deaths in the U.S. Physicians are relying more on minimally invasive procedures that use next-generation surgical tools, reducing patient recovery time and improving procedural outcomes. Strong demand from high-risk cardiac patients and growing adoption of advanced surgical techniques across major healthcare networks are further contributing to the expansion of this segment. In addition, continuous product upgrades in terms of device compatibility, wireless connectivity, and battery life are making these tools more attractive to both clinicians and patients.

The diagnostics and monitoring devices segment is expected to register the highest CAGR during the forecast period due to increasing emphasis on early detection and real-time monitoring of cardiac conditions. The growing popularity of wearable ECG monitors, remote telemetry, and AI-integrated diagnostic tools is transforming how physicians track heart health and respond to abnormalities. Patients having chronic conditions are turning to portable monitoring systems for continuous assessment, especially outside of clinical environments. Innovations in compact diagnostic imaging and noninvasive tools are expanding usage in outpatient and home care settings. Increasing awareness of preventive cardiac care is driving uptake among younger and health-conscious individuals, accelerating market penetration. In addition, the demand for integrated diagnostic platforms that deliver accurate, fast, and user-friendly cardiac assessments is gaining momentum across both primary care and specialized settings.

Application Outlook

Based on application, the U.S. cardiovascular device market is segmented into heart failure, cardiac arrhythmia, coronary artery disease, and others. The coronary artery disease segment accounted for the largest revenue share in 2024 due to its widespread prevalence across the adult population and high incidence among aging individuals. For instance, according to the U.S. Centers for Disease Control and Prevention, coronary heart disease (CHD) is the leading type of heart disease, causing 371,506 deaths in 2022. It affects approximately 5% of adults aged 20 and older, or 1 in 20 individuals. Lifestyle factors such as poor diet, physical inactivity, and smoking are contributing to arterial plaque buildup, making coronary blockages one of the most treated cardiovascular conditions. This rising burden is driving consistent demand for stents, angioplasty catheters, and drug-eluting balloons across the U.S. health system. Increasing preference for minimally invasive revascularization techniques is also influencing procedure volume. Hospitals and heart centers are continuously adopting advanced interventional cardiology systems to address these cases efficiently. Availability of high-end surgical equipment and growing coverage under insurance plans are allowing wider access to treatment. Strong investments in research and development for novel stent materials and bioresorbable scaffolds further strengthen the segment’s market position.

The cardiac arrhythmia segment is expected to witness the fastest growth rate during the forecast period, due to the increasing incidence of atrial fibrillation, bradycardia, and ventricular tachycardia among both older and younger populations. The rise in wearable monitoring technologies and early diagnostic tools is allowing for faster and more accurate detection of rhythm irregularities. Demand for implantable cardioverter defibrillators (ICDs), cardiac resynchronization therapy (CRT) devices, and catheter ablation systems is steadily increasing in response to clinical guidelines recommending early intervention. Healthcare providers are also expanding electrophysiology labs and offering specialized care pathways to manage arrhythmic conditions more effectively. Technological improvements in leadless pacemakers and wireless cardiac monitors are enhancing patient comfort and procedural success. The growing focus on rhythm management through personalized therapy and smart monitoring tools is expected to drive adoption across clinical and home-based care environments.

Use Cases of Cardiovascular Devices

| Use Case | How Cardiovascular Devices Are Used |

| Placement of Coronary Stent | Implantation of stents helps in opening up blocked or narrowed arteries to ensure smooth circulation of blood into the heart and prevent heart attacks. |

| Monitoring and Management of Heart Rhythm | Cardiac monitors help in tracking the heart rhythms of a patient to monitor arrhythmias. |

| Implantation of Pacemaker and Defibrillator | The use of an equipment from the cardiac implantable devices market helps in managing the arrhythmias in a patient’s heart. |

| Cardiac Imaging and Diagnosis | Modern imaging technology helps doctors in diagnosing various heart diseases and managing them. |

| Heart Valve Replacement Procedures | Heart valve replacement procedures involve the use of special cardiovascular devices to perform surgery or a transcatheter procedure on heart valves. |

| Treatment of Peripheral Vascular Diseases | Vascular devices such as balloons and stents are used in the treatment of peripheral vascular diseases. |

| Remote Cardiac Patient Monitoring | Use of wearable and implantable monitoring devices to monitor heart condition remotely. |

Source: Polaris Market Research Analysis

End User Outlook

Based on end user, the segmentation includes hospitals, ambulatory surgical centers, and specialty clinics. The hospitals segment accounted for approximately 60% of the revenue share in 2024 due to their comprehensive infrastructure for handling complex cardiovascular interventions and emergency cardiac care. Large multispecialty hospitals have well-equipped catheterization labs, cardiac surgical theaters, and intensive care units that support high volumes of both elective and urgent procedures. Access to skilled cardiologists, multidisciplinary teams, and post-operative care facilities makes hospitals the preferred choice for critical interventions such as bypass surgeries, valve replacements, and stent placements. Advanced procurement capabilities allow hospitals to adopt the latest generation of cardiovascular devices quickly. In addition, favorable reimbursement models and integration with insurance providers support higher patient throughput and revenue. Hospitals also lead in clinical trials and adoption of newly approved technologies, giving them an edge in delivering innovative cardiac care.

The ambulatory surgical centers (ASCs) segment is expected to witness the fastest growth rate during the forecast period, due to a growing shift toward cost-efficient, same-day cardiovascular procedures. Patients increasingly prefer outpatient settings that offer shorter wait times, lower procedural costs, and quicker recovery. Advances in catheter-based and minimally invasive cardiac technologies are enabling safe and effective treatments in ASCs without the need for overnight hospital stays. These centers are rapidly upgrading facilities to meet accreditation standards for cardiovascular procedures, attracting both patients and physicians. Expansion of value-based care models and insurer preference for outpatient treatment paths are boosting ASC procedure volumes. Investments in compact diagnostic tools and portable interventional systems are supporting the trend, making ASCs a high-growth channel for cardiovascular device usage in the US.

Source: Polaris Market Research Analysis

Cost and Adoption Factors

The use of cardiovascular devices in the US is influenced by both cost and efficacy. Advanced devices usually entail huge costs during their development, and cost thus becomes a critical consideration for the hospital/healthcare provider. Insurance reimbursement programs from public and private insurance companies become other factors influencing the accessibility of the technology to the patient. Adoption of the technology is influenced by the ability of the technology to enhance the well-being of patients, the efficiency of the procedure, and reduced healthcare costs.

Key Players and Competitive Analysis

The competitive landscape of the U.S. cardiovascular device market is shaped by continuous innovation, strategic partnerships, and aggressive market expansion strategies aimed at addressing the rising burden of heart-related conditions. Industry analysis highlights a clear focus on enhancing product portfolios through mergers and acquisitions, enabling established players to integrate advanced technologies such as AI-powered diagnostics, next-generation stents, and wireless implantable devices into their offerings. Strategic alliances between device manufacturers and healthcare providers are fostering the co-development of value-based solutions that improve patient outcomes while reducing procedural costs.

Post-merger integration efforts have led to streamlined R&D pipelines and expanded distribution capabilities across hospitals and ambulatory centers. Technology advancements remain a key competitive lever, particularly in minimally invasive surgical tools, wearable cardiac monitors, and remote patient management platforms. Joint ventures are also accelerating innovation in digital cardiology and interventional systems. Companies are targeting niche markets such as transcatheter valve therapies, structural heart interventions, and arrhythmia management to differentiate their positioning.

Rising demand for data-integrated, user-friendly devices is driving investments in interoperability and software-driven monitoring systems. The competitive intensity is expected to increase in the future as regulatory agencies promote faster approvals and value-based reimbursement models continue to gain traction.

List of Key Companies in U.S. Cardiovascular Device Market

- Abbott Laboratories

- B. Braun Melsungen AG

- Biotronik SE & Co.KG

- Boston Scientific Corporation

- C. R. Bard, Inc.

- Cook Medicals

- Edward lifesciences corporation

- Jude Medical, Inc.

- Lepu Medicals

- Liaoning Biomedical Materials

- Medtronic Plc

- Meril Life Sciences

- MicroPort Scientific Corporation

- Terumo Corporation

- Translumina GmbH

- Vascular Concepts

Future Outlook

The outlook for the U.S. cardiovascular devices market appears promising due to several factors, including the high incidence rate of heart diseases, the growing number of older adults, and technological progress in the field of medicine. The use of innovative techniques for diagnosis and treatment of cardiovascular diseases, such as minimally invasive operations, artificial intelligence applications for diagnosis, cardiac devices that can be worn by patients, and remote monitoring devices, is likely to increase in the near future. With an advanced healthcare system, appropriate reimbursement policies, and consistent investments in innovations, the market is projected to grow steadily in the future.

US Cardiovascular Devices Industry Developments

- May 2026: Royal Philips announced Philips SmartIQ, an innovative coronary imaging technology for its Azurion image-guided therapy. Royal Philips stated that the technology has been developed in collaboration with leading cardiovascular centers. It is designed to address the trade-off between image quality and radiation exposure in coronary procedures.(source: philips.com)

- March 2026: Medtronic plc (NYSE: MDT) announced receiving U.S. FDA approval for an expanded indication for the OmniaSecure defibrillation lead. The company stated that the lead has been approved for placement in the left bundle branch (LBB) area. It can be used for conduction system pacing (CSP), which closely mimics the natural physiology of the heart.(source: medtronic.com)

- In March 2025, Abbott obtained CE Mark certification for its Volt Pulsed Field Ablation System, designed specifically for the treatment of patients suffering from arrhythmias. This system utilizes advanced pulsed field ablation technology to selectively target and ablate cardiac tissue, offering a novel approach to managing abnormal heart rhythms.

U.S. Cardiovascular Device Market Segmentation

By Device Type Outlook (Revenue USD Billion, 2021–2034)

- Diagnostic and Monitoring Devices

- Electrocardiogram

- Remote Cardiac Monitoring

- MRI

- Others

- Therapeutic and Surgical Devices

- Ventricular Assist Devices

- Cardiac Rhythm Management Devices

- Catheter

- Stents

- Others

U.S. Cardiovascular Devices Market, by Application

- Heart Failure

- Cardiac Arrhythmia

- Coronary Artery Disease

- Others

U.S. Cardiovascular Devices Market, by End Use

- Hospitals

- Ambulatory Surgical Centers

- Specialty Clinics

U.S. Cardiovascular Device Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 22.57 billion |

| Market Size in 2026 | USD 24.87 billion |

| Revenue Forecast by 2034 | USD 38.55 billion |

| CAGR | 5.60% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

U.S. Cardiovascular Devices Market Frequently Asked Questions

The U.S. cardiovascular device market size was valued at USD 23.57 billion in 2025 and is projected to grow to USD 38.55 billion by 2034.

The US market is projected to register a CAGR of 5.60% during the forecast period.

A few key players in the market are Abbott Laboratories; B. Braun Melsungen AG; Biotronik SE & Co.KG; Boston Scientific Corporation; C. R. Bard, Inc.; Cook Medicals; Lepu Medicals; Liaoning Biomedical Materials; Medtronic Plc; Meril Life Sciences; MicroPort Scientific Corporation; Terumo Corporation; Translumina GmbH; Vascular Concepts; Jude Medical, Inc.; and Edward Lifesciences Corporation.

The therapeutic and surgical devices segment accounted for approximately 70% of the revenue share in 2024 due to the rising number of interventional cardiology procedures across hospitals and specialty cardiac centers.

The coronary artery disease segment accounted for the largest revenue share in 2024, due to its widespread prevalence of high incidence of cardiovascular disease among aging individuals.

Popular cardiovascular devices include stents, pacemakers, defibrillators, heart monitors, heart valves, and cardiac imaging equipment. These devices are used to diagnose, treat, and monitor heart and blood vessels.

AI and digital technology enable doctors to diagnose heart diseases and monitor their patients in a better way. The development of wearable devices and digital monitoring systems will help doctors monitor the state of the heart in a more efficient manner.

The US cardiovascular device market is expected to grow since there is an increased number of individuals requiring heart disease treatment. This is due to the availability of new technology, less invasive procedures, and improved monitoring devices.

Download Sample Report of U.S. Cardiovascular Device Market

Please fill out the form to request a customized copy of the research report.