U.S. Gastric Cancer Diagnostics Market Size Report 2026-2034

REPORT DETAILS

REPORT DETAILS

U.S. Gastric Cancer Diagnostics Market Summary

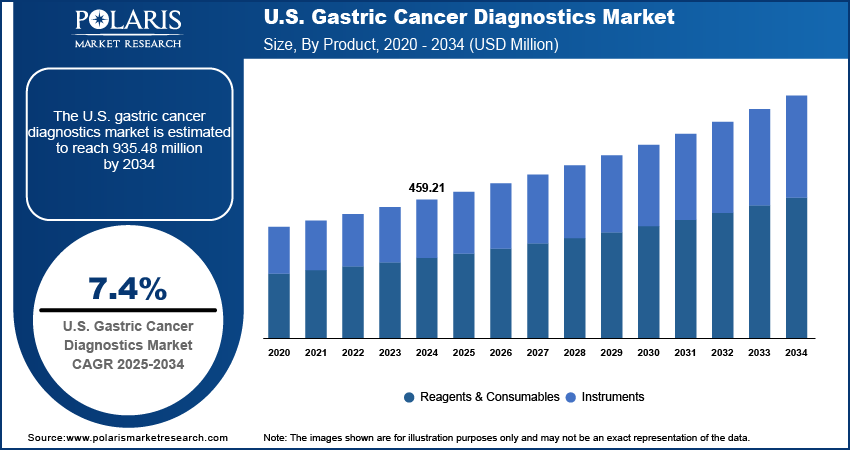

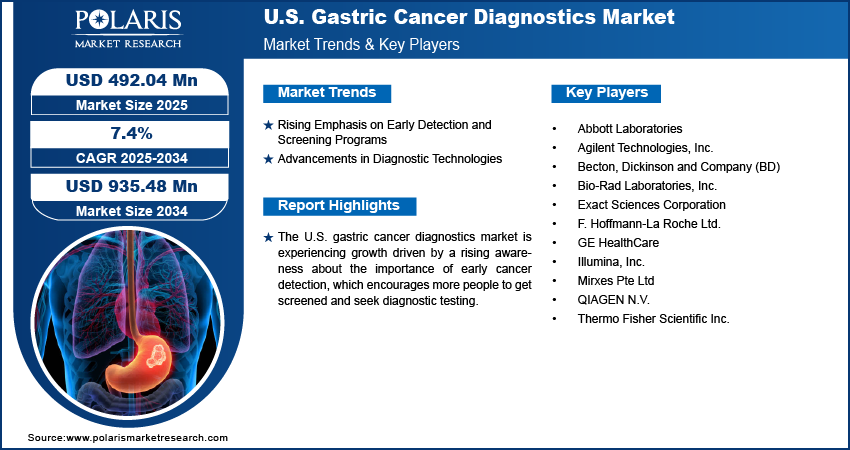

The U.S. gastric cancer diagnostics market size was valued at USD 492.83 million in 2025 and is anticipated to register a CAGR of 7.4% from 2026 to 2034. The market growth is largely driven by a growing awareness of early detection and screening programs, coupled with continued advancements in diagnostic technologies.

Market Statistics

Key Takeaways

- The reagents and consumables segment dominated the market in 2025 with a revenue share of 60.0%. The segment led due to the regular use of staining solutions, molecular testing kits, and other disposable diagnostic products.

- The instruments segment is expected to register the fastest CAGR of 6.7% during 2026–2034. Growth is driven by the increasing use of advanced endoscopy systems, liquid biopsy platforms, and next-generation sequencing (NGS) technologies.

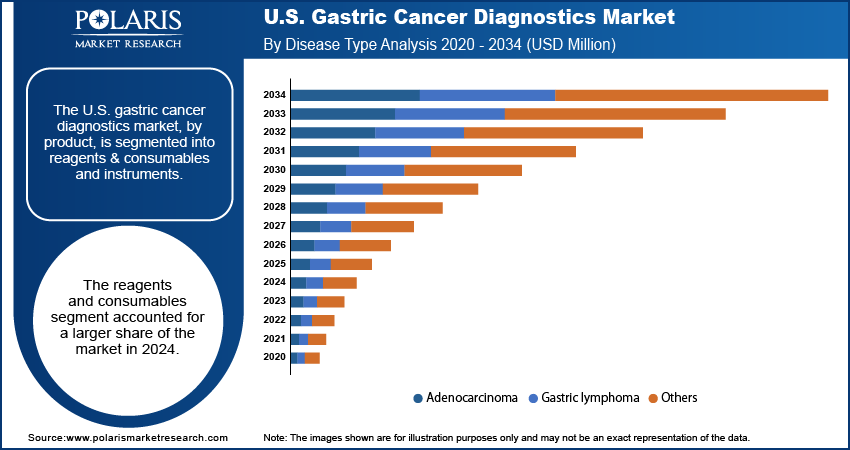

- By disease type, the adenocarcinoma segment accounted for the largest revenue share of 70.0% in 2025. The segment held the largest share as adenocarcinoma represents the majority of stomach cancer cases.

- The hospitals segment held the dominant revenue share of 46.2% in 2025. Hospitals led the market due to the availability of imaging, biopsies, pathology testing, and specialist consultations in one place.

- The diagnostic laboratories segment is anticipated to witness the fastest CAGR of 7.7% during 2026–2034. The growth is supported by increasing demand for biomarker testing, molecular diagnostics, and genomic profiling services.

*Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations.

Industry Dynamics

- Rising focus on early detection is increasing demand for gastric cancer diagnostic tests. Early diagnosis improves treatment outcomes and survival rates.

- Advancements in technologies such as liquid biopsy, advanced imaging, and NGS are improving cancer detection accuracy. These technologies are also supporting faster diagnosis.

- Growing awareness about stomach cancer risk factors is increasing the number of screening and diagnostic procedures. More patients are undergoing regular testing.

- High costs of advanced diagnostic technologies are limiting adoption in some healthcare settings. Smaller facilities may face budget-related challenges.

AI Impact on U.S. Gastric Cancer Diagnostics Market

- AI tools are helping doctors find stomach cancer faster during endoscopy tests.

- AI systems can detect small abnormal tissue changes that may be missed manually.

- AI-based data analysis is helping improve biomarker testing and patient treatment planning.

- AI integration in labs is reducing manual work and helping speed up diagnostic testing.

What is U.S. Gastric Cancer Diagnostics Market?

The U.S. gastric cancer diagnostics market involves various medical procedures, tests, and evaluations used to identify and confirm the presence of stomach cancer. Its goal is to detect the disease early, understand how far it has spread, and guide treatment decisions.

The prevalence of Helicobacter pylori (H. pylori) infection remains a significant driver for the U.S. gastric cancer diagnostics market expansion. This bacterium is a primary risk factor for gastric cancer, and its persistent presence in the stomach can lead to chronic inflammation and cellular changes that may eventually become cancerous. Diagnosing and eradicating H. pylori is a crucial step in preventing gastric cancer development, thereby fueling the demand for specific diagnostic tests. For example, the National Cancer Institute (NCI) provides a fact sheet titled "Helicobacter pylori (H. pylori) and Cancer" which states that chronic H. pylori infections significantly increase the risk of developing non-cardia gastric adenocarcinoma and gastric MALT lymphoma. The fact sheet further emphasizes that treating H. pylori infection can reduce the risk of gastric cancer in at-risk individuals. This strong link between H. pylori and gastric cancer directly drives the need for diagnostic methods to detect the infection and monitor its impact.

Source: Polaris Market Research Analysis

The aging population in the U.S. is another major factor driving the U.S. gastric cancer diagnostics market growth. Gastric cancer disproportionately affects older individuals, with the average age of diagnosis being relatively high. As the number of elderly people in the U.S. continues to grow, there will be an increased number of individuals at higher risk for developing gastric cancer, leading to a greater need for diagnostic services. The American Cancer Society's "Key Statistics About Stomach Cancer" of January 2025 highlights this trend, noting that stomach cancer mostly affects older people, with about 6 out of every 10 people diagnosed each year being 65 or above. This demographic shift directly translates into an expanded pool of individuals requiring screening, early detection, and ongoing diagnostic monitoring for gastric cancer, thereby boosting the industry's growth.

Advancements in Cancer Diagnostic Technologies

Technologies such as liquid biopsy, next-generation sequencing (NGS), and AI-based diagnostics are improving gastric cancer testing and detection. These technologies help doctors identify cancer earlier, improve testing accuracy, and support treatment planning. Increasing use of advanced diagnostic systems is also supporting market growth.

Industry Dynamics

Rising Emphasis on Early Detection and Screening Programs

Early diagnosis of gastric cancer helps improve patient survival rates. When detected at an early stage, treatment options are more effective, and the chances of a successful recovery are significantly higher. This increased awareness among both the public and healthcare professionals is leading to a greater push for systematic screening and diagnostic efforts.

Data from the National Cancer Institute's Surveillance, Epidemiology, and End Results (SEER) program, as highlighted in the American Cancer Society's "Stomach (Gastric) Cancer Survival Rates", shows a stark difference in 5-year relative survival rates. The survival rate for localized stomach cancer is 75%, while for distant stage cancer, it drops to 7%. This significant difference underscores the critical importance of early diagnosis. This strong correlation between early detection and improved outcomes is a major force driving the growth of the U.S. gastric cancer diagnostics market.

Advancements in Diagnostic Technologies

The field of gastric cancer diagnostics is constantly evolving with new and improved technologies. These advancements offer more accurate, less invasive, and more efficient ways to detect and characterize gastric cancer. From enhanced imaging techniques to sophisticated molecular tests, these innovations are making it easier for doctors to diagnose the disease.

A review article published in PubMed Central titled "Advancements in non-invasive diagnosis of gastric cancer" discusses how methods such as advanced imaging, liquid biopsy, and breath tests are set to transform gastric cancer diagnosis, making it more accessible and efficient. The article also states that early diagnosis is crucial for improving patient outcomes, with 5-year survival rates approaching 90% when gastric cancer is curable through surgical resection. These ongoing technological developments improve the capabilities of diagnostic tools, thereby driving their adoption and use in the U.S. gastric cancer diagnostics market.

Source: Polaris Market Research Analysis

Segmental Insights

Product Analysis

The reagents and consumables segment held 60.0% share in 2025, due to the constant and high demand for these products in routine diagnostic tests, including histopathology, immunohistochemistry, and molecular testing. Every cancer biopsy, blood test, or imaging procedure requires a range of specialized reagents, kits, and other single-use items, leading to their continuous consumption. The ongoing need for specific dyes and chemical solutions for tissue staining in pathological examinations or the demand for test kits used in identifying Helicobacter pylori infection, a known risk factor for gastric cancer, contributes significantly to this segment's leading position.

The instruments segment is anticipated to register the highest growth at a CAGR of 6.7%, during the forecast period. This growth is largely fueled by rapid technological advancements and the increasing integration of innovative solutions. New generations of endoscopic instruments with enhanced imaging capabilities, such as high-definition endoscopes with virtual chromoendoscopy, are improving the visualization of subtle lesions and aiding in earlier detection. Moreover, the emergence of advanced molecular diagnostic platforms, including next-generation sequencing (NGS) and liquid biopsy technologies, requires sophisticated instruments for analysis.

Disease Type Analysis

The adenocarcinoma segment held the largest share valued at 70.0% in 2025. This is because adenocarcinoma accounts for the vast majority of stomach cancer cases, making it the most frequently diagnosed type. Diagnostic efforts and research are heavily concentrated on this specific form of cancer due to its prevalence and the significant impact on public health. A review in PubMed Central titled "Incidence trends of gastric cancer in the United States over 2000–2020: A population-based analysis" indicates that adenocarcinoma was the most common subtype in both older and younger adult populations during the study period, highlighting its widespread occurrence.

The others segment, which includes rarer types of gastric cancers, is anticipated to register the highest growth rate at a CAGR of 6.1% in the U.S. gastric cancer diagnostics market during the forecast period. While less common, conditions such as neuroendocrine tumors, gastrointestinal stromal tumors (GISTs), and squamous cell carcinomas are gaining more attention due to improved diagnostic techniques and increased research into their specific characteristics. As diagnostic tools become more sophisticated, the ability to accurately identify these less common, yet distinct, cancer types is improving.

End Use Analysis

The hospitals segment held the largest share accounting for 46.2% in 2025. Hospitals are often the first point of contact for patients experiencing symptoms, and they offer a comprehensive range of diagnostic services under one roof, from initial consultations and endoscopies to advanced imaging and biopsies. The integrated nature of care within hospitals, including the immediate availability of pathology labs and specialists for multidisciplinary team discussions, makes them central to the diagnostic pathway. For example, Memorial Sloan Kettering Cancer Center, as noted in their "Stomach Cancer Treatment" information, emphasizes their comprehensive approach, seeing a high volume of patients and performing numerous diagnostic procedures, which underscores the significant role hospitals play.

The diagnostic laboratories segment is anticipated to register the highest growth rate during the forecast period. This growth is driven by the increasing demand for specialized and high-volume testing, including molecular diagnostics, cancer biomarker testing, and advanced pathology services. While hospitals perform some tests in-house, complex or high-throughput analyses are often outsourced to dedicated diagnostic laboratories that possess specialized equipment and expertise. These labs are crucial for confirming diagnoses and cancer stages, and guiding personalized treatment plans through detailed molecular profiling. The growing adoption of liquid biopsies and next-generation sequencing (NGS) for detecting circulating tumor DNA and other biomarkers often requires the advanced capabilities found in specialized diagnostic laboratories.

Role of Hospitals & Diagnostic Laboratories

| Aspect | Hospitals | Diagnostic Laboratories |

| Main Role | First point of diagnosis and patient evaluation | Specialized testing and detailed analysis |

| Services Offered | Endoscopy, imaging, biopsy, pathology, consultations | Molecular testing, biomarker testing, genomic profiling |

| Testing Type | Routine and initial diagnostic procedures | Advanced and high-volume testing |

| Importance in Market | Supports early detection and treatment decisions | Supports accurate diagnosis and personalized treatment planning |

Source: Polaris Market Research Analysis

Source: Polaris Market Research Analysis

Key Players and Competitive Insights

The U.S. gastric cancer diagnostics market is competitive, with a mix of established global healthcare companies and specialized diagnostic firms. These companies focus on continuous innovation in product development, strategic partnerships, and expanding their reach to gain a stronger foothold. The competition is driven by the need for more accurate, less invasive, and earlier detection methods for gastric cancer.

A few prominent companies in the industry include Abbott Laboratories; Becton, Dickinson and Company (BD); Bio-Rad Laboratories, Inc.; F. Hoffmann-La Roche Ltd.; Thermo Fisher Scientific Inc.; Agilent Technologies, Inc.; Illumina, Inc.; QIAGEN N.V.; Exact Sciences Corporation; Mirxes Pte Ltd; and GE HealthCare.

Key Players

- Abbott Laboratories

- Agilent Technologies, Inc.

- Becton, Dickinson and Company (BD)

- Bio-Rad Laboratories, Inc.

- Exact Sciences Corporation

- F. Hoffmann-La Roche Ltd.

- GE HealthCare

- Illumina, Inc.

- Mirxes Pte Ltd

- QIAGEN N.V.

- Thermo Fisher Scientific Inc.

Industry Developments

- February 2026: Aiforia Technologies Plc launched the CE-IVD marked Aiforia Gastric Cancer AI application. The application helps pathologists detect cancerous regions in digitized tissue samples. (Source: aiforia.com)

- April 2025: Agilent Technologies Inc. announced that the PD-L1 IHC 22C3 pharmDx (Code SK006) assay achieved European IVDR certification, enabling its use as a Companion Diagnostic (CDx) to help identify patients affected by gastric or gastroesophageal junction adenocarcinoma. (Source: agilent.com)

Future Outlook

The U.S. gastric cancer diagnostics market is expected to grow steadily in the coming years. Rising gastric cancer cases and growing awareness about early diagnosis are supporting market growth. Increasing use of molecular testing, liquid biopsy, and AI-based diagnostics is improving cancer detection. Growing focus on precision medicine is also increasing demand for advanced diagnostic tests. Healthcare investments in oncology diagnostics are further supporting market expansion.

U.S. Gastric Cancer Diagnostics Market Segmentation

By Product Outlook (Revenue – USD Million, 2021–2034)

- Reagents & Consumables

- Instruments

By Disease Type Outlook (Revenue – USD Million, 2021–2034)

- Adenocarcinoma

- Gastric lymphoma

- Others

By End Use Outlook (Revenue – USD Million, 2021–2034)

- Hospitals

- Diagnostic Laboratories

- Diagnostic Imaging

U.S. Gastric Cancer Diagnostics Market Report Scope:

| Report Attributes | Details |

| Market Size in 2025 | USD 492.83 million |

| Market Size in 2026 | USD 529.00 million |

| Revenue Forecast by 2034 | USD 938.38 million |

| CAGR | 7.4% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD million and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Insights |

| Segments Covered |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

The global market size was valued at USD 492.83 million in 2025 and is projected to grow to USD 938.38 million by 2034.

The global market is projected to register a CAGR of 7.4% during the forecast period.

A few key players in the market include Abbott Laboratories; Becton, Dickinson and Company (BD); Bio-Rad Laboratories, Inc.; F. Hoffmann-La Roche Ltd.; Thermo Fisher Scientific Inc.; Agilent Technologies, Inc.; Illumina, Inc.; QIAGEN N.V.; Exact Sciences Corporation; Mirxes Pte Ltd; and GE HealthCare.

The reagents and consumables segment accounted for the largest share of the market in 2025 valued at 60.0%.

the adenocarcinoma segment accounted for the largest revenue share of 70.0% in 2025.

Download Sample Report of U.S. Gastric Cancer Diagnostics Market

Please fill out the form to request a customized copy of the research report.