U.S. Ostomy Care and Accessories Market Size & Growth, 2025-2034

REPORT DETAILS

Market Statistics

Overview

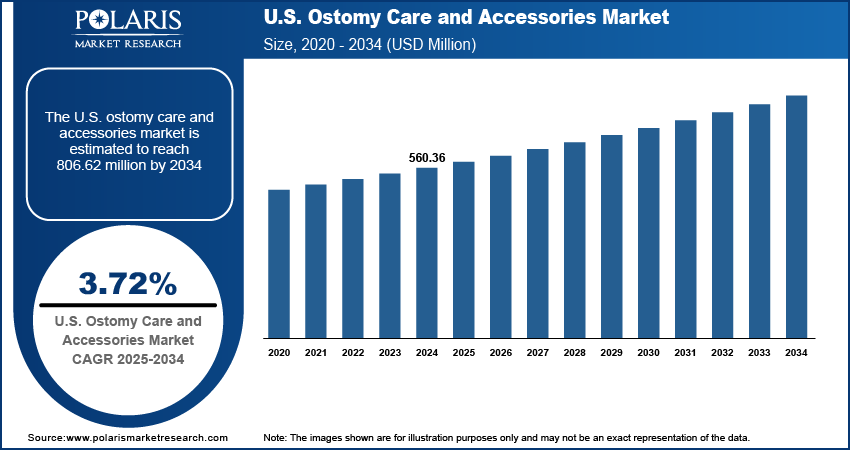

The U.S. ostomy care and accessories market size was valued at USD 560.36 million in 2024, growing at a CAGR of 3.72% from 2025 to 2034. Key factors driving demand for ostomy care and accessories in the U.S. include the expanding geriatric population, increasing incidence of bladder cancer, and the expanding healthcare spending.

Key Insight

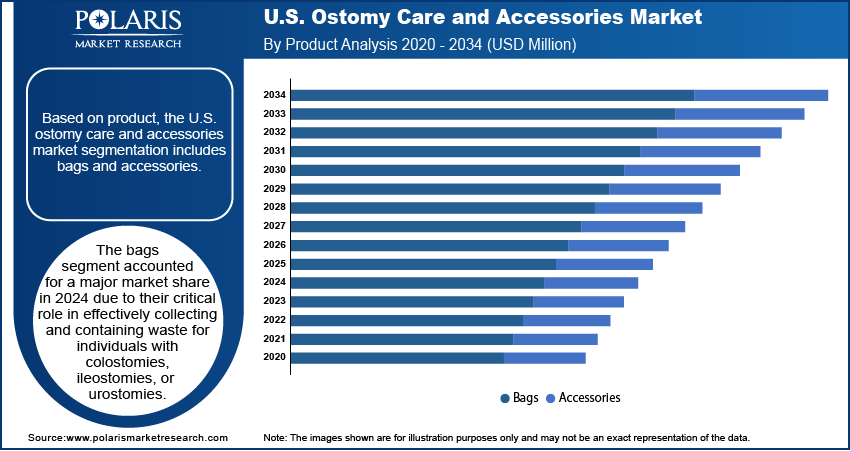

- The bags segment accounted for a major U.S. ostomy care and accessories market share in 2024 due to the growing number of colostomies, ileostomies, or urostomies surgeries.

- The colostomy segment held the largest revenue share in 2024 due to the high prevalence of bowel obstruction cases in the U.S.

- The home care settings segment dominated the revenue share in 2024 due to the convenience of receiving treatment outside hospital environments.

Industry Dynamics

- Bladder cancer patients rely on ostomy care to manage post-surgery urinary diversion, ensure hygiene and comfort, and enhance quality of life. Therefore, the increasing incidence of bladder cancer is fueling the demand for ostomy care and accessories.

- Older adults face higher risks of conditions such as colorectal cancer that require ostomy surgeries and their related accessories. Hence, the expanding geriatric population is driving the U.S. ostomy care and accessories market.

- The increasing investments in cancer research in the country are expected to create a lucrative market opportunity during the forecast period.

- High cost of ostomy care and accessories may hamper the market growth.

Artificial Intelligence (AI) Impact on U.S. Ostomy Care and Accessories Market

- AI is transforming the U.S. ostomy care and accessories market by enhancing product innovation, such as smart pouches with leak-detection sensors.

- It improves patient care through AI-driven apps that monitor stoma health and offer personalized recommendations.

- Automation in manufacturing boosts efficiency, reducing costs and improving supply chain reliability.

- AI-powered telehealth platforms provide remote consultations, improving accessibility for rural patients.

Market Statistics

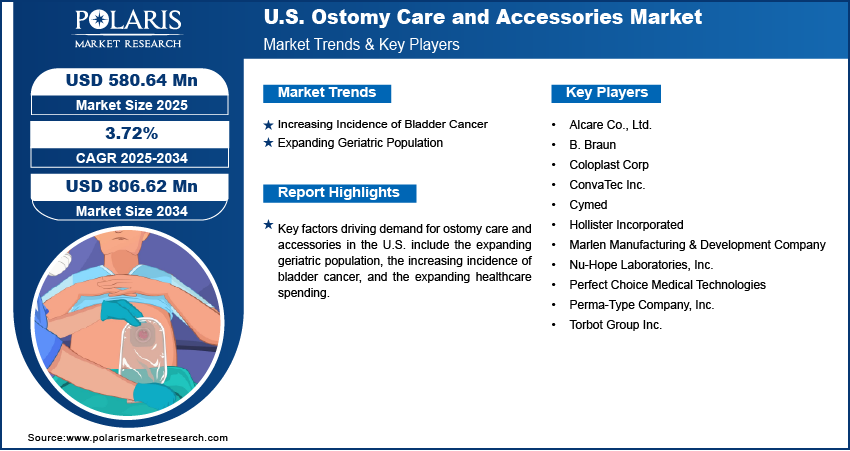

- 2024 Market Size: USD 560.36 Million

- 2034 Projected Market Size: USD 806.62 Million

- CAGR (2025-2034): 3.72%

Source: Polaris Market Research Analysis

Ostomy care and accessories refer to the products and supplies designed to support individuals living with a surgically created ostomy for waste elimination. These include ostomy pouches, skin barriers, medical adhesives, deodorants, and cleansing products. They help maintain hygiene, prevent leakage, protect the skin, and improve the comfort, confidence, and quality of life of ostomy patients.

The U.S. ostomy care and accessories market serves a growing patient base driven by rising colorectal cancer cases, inflammatory bowel diseases, and increasing awareness of post-surgical care. High healthcare expenditure, advanced product innovations like skin-friendly adhesives, and strong distribution networks support market growth. The country’s aging population further fuels demand, while personalized care products and telehealth guidance improve patient outcomes, convenience, and long-term ostomy management efficiency.

The U.S. ostomy care and accessories market demand is driven by the expanding healthcare spending. American Medical Association, in its article, stated that health spending in the U.S. increased by 7.5% in 2023 to $4.9 trillion from 2022. This drove hospitals and clinics in the country to perform more ostomy surgeries, creating a larger patient base needing post-operative care products such as bags. Rising healthcare budgets are also supporting education campaigns, helping patients understand the importance of high-quality ostomy supplies for their well-being. Additionally, expanded insurance coverage or subsidies are reducing costs, encouraging patients to purchase specialized accessories. Therefore, as healthcare spending rises, healthcare providers recommend advanced ostomy products, further driving demand in the market.

Drivers & Opportunities

Increasing Incidence of Bladder Cancer: Bladder cancer patients rely on ostomy care and accessories to manage post-surgery urinary diversion, ensure hygiene, comfort, and quality of life. The American Cancer Society estimates about 84,870 new cases of bladder cancer in the U.S. in 2025. Healthcare providers and manufacturers are also responding to this increasing incidence of bladder cancer by expanding product availability and innovation. Therefore, the rising bladder cancer prevalence is creating the need for specialized medical supplies such as ostomy pouches, skin barriers, medical adhesives, deodorants, and cleansing products.

Expanding Geriatric Population: Older adults are facing higher risks of conditions such as colorectal cancer, inflammatory bowel disease, and other gastrointestinal disorders that require ostomy surgeries and their related accessories. According to the Population Reference Bureau, the number of Americans ages 65 and older is projected to increase from 58 million in 2022 to 82 million by 2050. Additionally, elderly individuals often require specialized care and durable, easy-to-use accessories to manage their stomas effectively, further boosting market demand. Hence, the rising geriatric demographic, coupled with increasing awareness of advanced ostomy solutions, is ensuring sustained market growth.

Source: Polaris Market Research Analysis

Segmental Insights

Product Analysis

Based on product, the segmentation includes bags and accessories. The bags segment accounted for a major U.S. ostomy care and accessories market share in 2024. The dominance is attributed to their critical role in effectively collecting and containing waste for individuals with colostomies, ileostomies, or urostomies. The demand for these products grew as patients prioritized convenience, comfort, and discretion in their daily lives. Manufacturers introduced advanced features such as odor-proof materials, skin-friendly adhesives, and improved wear time, which enhanced user confidence and quality of life. The rising number of ostomy surgeries driven by colorectal cancer, inflammatory bowel disease, and trauma cases further fueled the segment’s dominance. Additionally, an increasing geriatric population, who are more prone to conditions requiring ostomies, boosted demand.

Application Analysis

In terms of application, the segmentation includes colostomy, ileostomy, and urostomy. The colostomy segment held the largest revenue share in 2024 due to the high prevalence of colorectal cancer, diverticulitis, and bowel obstruction cases in the country. A significant portion of the aging population in the country required colostomy procedures due to degenerative bowel diseases, increasing long-term product usage. The segment benefited from advances in colostomy pouch designs, including skin-friendly barriers and odor control technology, that improved patient comfort and confidence. The growing emphasis on patient education and post-surgery support programs further encouraged the consistent adoption of colostomy-related products. Rising healthcare accessibility and insurance coverage for ostomy supplies also played a crucial role in strengthening the segment’s dominant position.

The ileostomy segment is estimated to grow at a rapid pace in the coming years, owing to the rising incidence of inflammatory bowel diseases such as Crohn’s disease and ulcerative colitis. Patients undergoing ileostomy procedures often require high-performance pouches that manage liquid stool output effectively. Increasing adoption of minimally invasive surgeries and growing awareness of ostomy care products among younger patients would accelerate the growth of the ileostomy segment during the forecast period.

End Use Analysis

In terms of end use, the segmentation includes home care settings, hospitals, and others. The home care settings segment dominated the revenue share in 2024 due to growing preference for self-managed ostomy care and the convenience of receiving treatment outside hospital environments. Many patients choose home-based care to reduce hospital visits, minimize costs, and maintain comfort in a familiar environment. Advancements in user-friendly ostomy products, such as pre-cut barriers, easy-drain pouches, and secure adhesives, have empowered patients to manage their conditions independently. Increased availability of e-commerce platforms for purchasing ostomy supplies and expanded reimbursement coverage further encouraged adoption in home care settings.

The hospitals segment is projected to grow at a robust pace during the assessment period, owing to the rising volume of ostomy surgeries performed in hospitals. Hospitals serve as the primary point of care for patients undergoing initial pouch fittings, receiving wound care, and managing complications. Growing investments in advanced ostomy care equipment and staff training programs ensure high-quality treatment and patient education during recovery. The increasing number of complex surgical cases, along with a focus on reducing post-surgical complications through professional care, is expected to continue to drive demand for hospital-based ostomy products and accessories.

Source: Polaris Market Research Analysis

Key Players & Competitive Analysis

The U.S. ostomy care and accessories market is highly competitive, dominated by key players such as Coloplast Corp, ConvaTec Inc., and Hollister Incorporated, which leverage strong brand recognition, extensive R&D, and advanced product portfolios. These companies focus on innovation in skin-friendly adhesives, odor-control technologies, and discreet designs to enhance patient comfort. B. Braun and Marlen Manufacturing & Development Company emphasize cost-effective solutions, while niche players like Nu-Hope Laboratories and Perfect Choice Medical Technologies cater to specialized needs. Smaller firms, including Perma-Type Company and Torbot Group, compete through customization and superior customer service. The market is further driven by mergers, acquisitions, and strategic partnerships to expand distribution networks. Rising demand for home care solutions and increasing ostomy awareness programs intensify competition, pushing manufacturers to differentiate through sustainability, digital health integration, and patient-centric innovations.

A few major companies operating in the U.S. ostomy care and accessories industry include Alcare Co., Ltd.; B. Braun; Coloplast Corp; ConvaTec Inc.; Cymed; Hollister Incorporated; Marlen Manufacturing & Development Company; Nu-Hope Laboratories, Inc.; Perfect Choice Medical Technologies; Perma-Type Company, Inc.; and Torbot Group Inc.

Key Companies

- Alcare Co., Ltd.

- B. Braun

- Coloplast Corp

- ConvaTec Inc.

- Cymed

- Hollister Incorporated

- Marlen Manufacturing & Development Company

- Nu-Hope Laboratories, Inc.

- Perfect Choice Medical Technologies

- Perma-Type Company, Inc.

- Torbot Group Inc.

U.S. Ostomy Care and Accessories Industry Developments

In February 2024, Convatec, a medical products and technologies company, launched Esteem Body with Leak Defense in Italy and announced its launch in the U.S. in April 2024.

U.S. Ostomy Care and Accessories Market Segmentation

By Product Outlook (Revenue, USD Million, 2020–2034)

- Bags

- One Piece

- Two Piece

- Accessories

- Seals/Barrier Rings

- Pouch Cover

- Pouch Closures

- Stoma Caps/Hat

- Others

By Application Outlook (Revenue, USD Million, 2020–2034)

- Colostomy

- Ileostomy

- Urostomy

By End Use Outlook (Revenue, USD Million, 2020–2034)

- Home Care Settings

- Hospitals

- Others

U.S. Ostomy Care and Accessories Market Report Scope

| Report Attributes | Details |

| Market Size in 2024 | USD 560.36 Million |

| Market Size in 2025 | USD 580.64 Million |

| Revenue Forecast by 2034 | USD 806.62 Million |

| CAGR | 3.72% from 2025 to 2034 |

| Base Year | 2024 |

| Historical Data | 2021–2023 |

| Forecast Period | 2025–2034 |

| Quantitative Units | Revenue in USD Million and CAGR from 2025 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

FAQ's

The market size was valued at USD 560.36 million in 2024 and is projected to grow to USD 806.62 million by 2034.

The market is projected to register a CAGR of 3.72% during the forecast period.

A few of the key players in the market are Alcare Co., Ltd.; B. Braun; Coloplast Corp; ConvaTec Inc.; Cymed; Hollister Incorporated; Marlen Manufacturing & Development Company; Nu-Hope Laboratories, Inc.; Perfect Choice Medical Technologies; Perma-Type Company, Inc.; and Torbot Group Inc.

The bags segment dominated the market share in 2024.

The hospitals segment is expected to witness the fastest growth during the forecast period.

Download Sample Report of U.S. Ostomy Care and Accessories Market

Please fill out the form to request a customized copy of the research report.