U.S. Plant-Based Meat Market Demand, Growth Opportunity, 2026-2034

REPORT DETAILS

U.S. Plant-Based Meat Market Summary

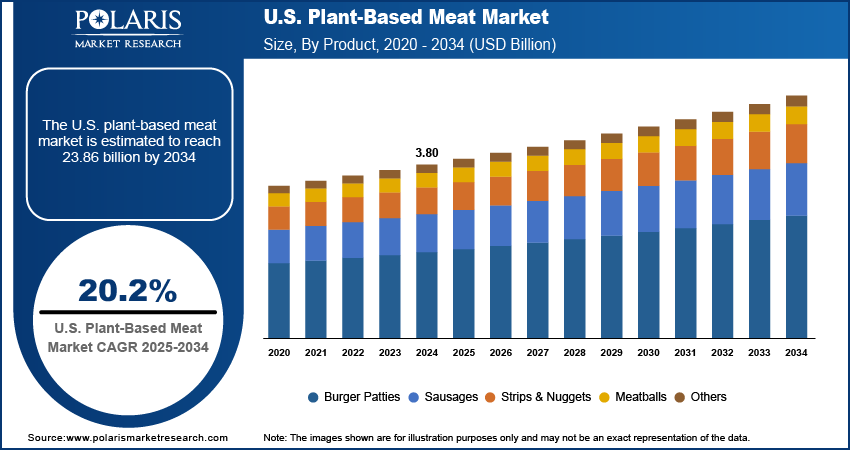

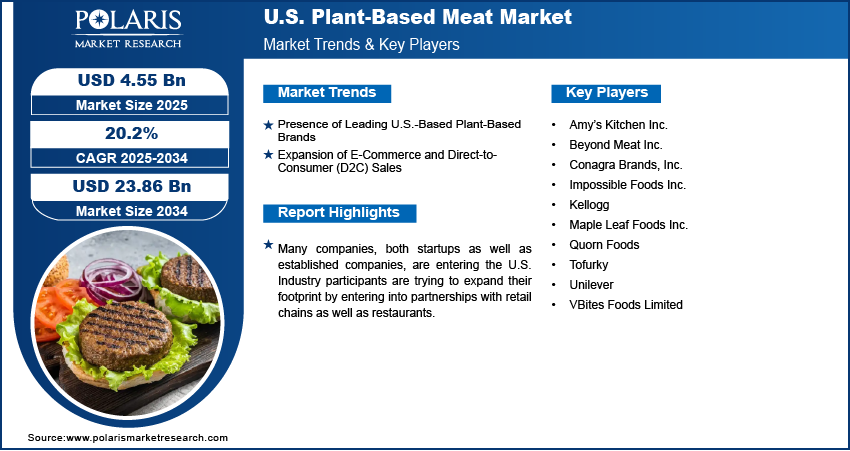

The U.S. plant-based meat market size was valued at USD 4.55 billion in 2025, growing at a CAGR of 20.2% from 2026 to 2034. Key factors driving demand are the presence of leading U.S.-based plant-based brands and the expansion of e-commerce and direct-to-consumer (D2C) sales.

Market Statistics

Key Takeaways

- The soy segment dominated the market with 40.0% share in 2025, driven by its high protein content and strong ability to mimic the texture of traditional meat.

- The wheat segment is expected to witness CAGR of 17.8% during the forecast period. Wheat-based ingredients, particularly wheat gluten (seitan), are becoming increasingly popular for delivering a chewy, meat-like texture.

- The burger patties segment accounted for 43.43% of the U.S. plant-based meat market revenue in 2025, with consumers readily embracing plant-based versions from well-known brands such as Beyond Meat and Impossible Foods.

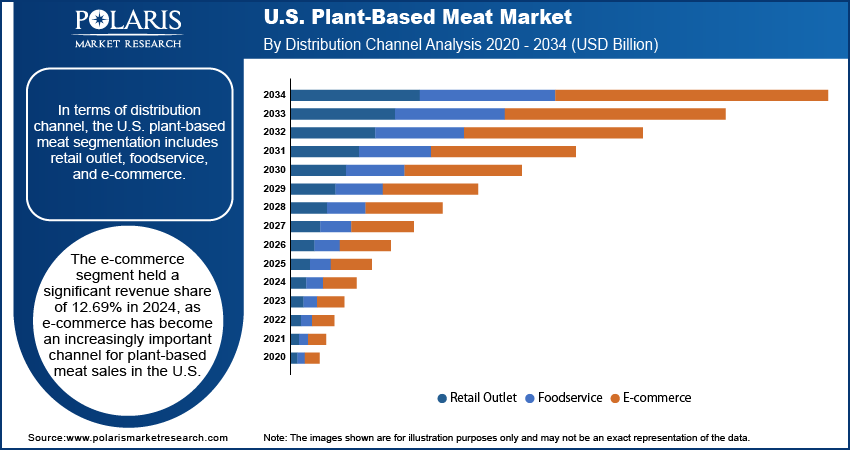

- The e-commerce segment held a 12.69% revenue share in 2025, reflecting the growing importance of online platforms in distributing plant-based meat products across the U.S.

*Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations.

Industry Dynamics

- The presence of leading U.S.-based plant-based brands is driving the demand for plant-based meat.

- The expansion of e-commerce and direct-to-consumer (D2C) sales is driving the U.S. plant-based meat market

- Industry participants are trying to expand their footprint by entering into partnerships with retail chains, as well as restaurants.

- High product prices compared to conventional meat limit the growth.

AI Impact on U.S. Plant-Based Meat Market

- AI speeds up product development by analyzing large datasets related to taste, texture, and nutrition, helping create plant-based meat that closely resembles traditional animal products.

- AI-driven tools provide deep insights into consumer behavior, preferences, and market trends, supporting more focused product innovation and marketing strategies.

- AI also streamlines supply chain and production processes, helping manufacturers reduce food waste, cut costs, and boost overall efficiency in plant-based meat production.

Source: Polaris Market Research Analysis

What are Plant-based meat?

Plant-based meat in simple terms can be defined as products manufactured by using plant ingredients that mimic the animal-derived meat both in terms of taste and appearance and are designed in a way to be indistinguishable from animal meat. These products are made by using a variety of sources such as peas, wheat, soy among others and as they directly substitute animal meat hence are often referred to as meat products.

Plant Based Meat vs Animal Meat

| Factors | Plant-Based Meat | Animal Meat |

| Nutrition | Lower cholesterol and saturated fat. Made using soy, wheat, peas, and other plant ingredients. | High in protein, iron, vitamin B12, and zinc. Can contain more saturated fat. |

| Environmental Impact | Lower carbon emissions and less water and land usage. | Higher greenhouse gas emissions and resource consumption. |

| Cost | Higher product prices compared to regular meat. | More affordable and widely available. |

| Taste & Texture | Made to copy the taste and texture of meat products. | Original meat taste and texture preferred by many consumers. |

| Sustainability | Considered more sustainable because of lower environmental impact. | Livestock farming creates higher environmental pressure. |

| Health Benefits | Preferred by consumers looking to reduce meat intake and follow healthier diets. | Provides essential nutrients but high processed meat consumption may cause health issues. |

| Availability | Growing presence in supermarkets, restaurants, e-commerce, and D2C channels. | Available across all retail and foodservice channels. |

| Consumer Demand | Demand increasing among vegans, vegetarians, and flexitarian consumers. | Continues to dominate overall meat consumption in the U.S. |

Source: Polaris Market Research Analysis

Rising concerns about health in the U.S. have significantly influenced food choices. Many Americans are aware of the negative effects of consuming red and processed meats, which have been linked to heart disease, obesity, diabetes, and certain types of cancer. This has led to a growing demand for healthier alternatives, such as plant-based meat, which is generally lower in saturated fat and cholesterol. The popularity of clean-label and protein-rich foods has further fueled the demand. Consumers are turning to plant-based meat as a nutritious substitute to traditional meat products as they prioritize wellness and preventive healthcare, thereby driving the growth.

The U.S. is experiencing a steady rise in flexitarian diets, which means those who still consume meat but aim to reduce their intake for health, environmental, or ethical reasons. This lifestyle is more practical for many Americans than adopting a strict vegan or vegetarian diet. Flexitarians are a key consumer group for the U.S. plant-based meat market as they seek alternatives that offer the taste and texture of meat without the drawbacks. In the U.S., supermarkets and restaurants are increasingly offering plant-based meat options to cater to this trend. Flexitarian drive strong demand for meat alternatives as it becomes more mainstream in the U.S., thereby fueling the growth.

Drivers & Opportunities

Presence of Leading U.S.-Based Plant-Based Brands: The U.S. is home to a few of the most influential plant-based meat companies, such as Beyond Meat, Impossible Foods, and Eat Just. These companies have led the way in innovation, product development, and marketing. Their partnerships with major fast-food chains such as Burger King and Starbucks and retail giants such as Walmart and Target have made plant-based meat widely accessible. Their strong branding and continuous investment in improving taste and texture have made them household names. The presence of these pioneering brands has helped normalize plant-based meat consumption in the U.S., thereby driving the growth.

Expansion of E-Commerce and Direct-to-Consumer (D2C) Sales: Online shopping has transformed how U.S. consumers buy food, and plant-based meat brands have adopted this shift. Online retail platforms and D2C sales channels allow companies to reach consumers nationwide, even in areas without major retail stores. This model provides convenience, subscription options, and access to a wider product range. Brands further gain valuable customer insights through direct sales, helping them tailor marketing and improve products. Americans became comfortable buying groceries online during and after the COVID-19 pandemic, including alternative proteins, thereby accelerating the growth.

Source: Polaris Market Research Analysis

Segmental Insights

Source Analysis

Based on source, the segmentation includes soy, wheat, peas, and other sources. The soy segment dominated the market with 40.0% share in 2025, due to its high protein content and ability to replicate the texture of real meat. It is commonly used in products such as sausages, nuggets, and ground meat alternatives. In the U.S., consumers adopt soy-based products because they are familiar, affordable, and often fortified with additional nutrients. Soy continues to be a preferred base for many manufacturers as health and sustainability remain top priorities. Its long history in vegetarian diets and proven functionality fuel the segment growth.

The wheat segment is expected to witness CAGR of 17.8% during the forecast period as wheat-based ingredients, especially wheat gluten (seitan), are gaining popularity for their chewy, meat-like texture. These products appeal to consumers seeking high-protein alternatives that offer a satisfying bite. Many U.S. brands use wheat in deli slices, sausages, and meat-style strips. While gluten-free product concerns limit appeal for some, wheat remains a favored option for others due to its cost-effectiveness and availability. The segment continues to grow as companies refine formulations to improve taste and reduce allergens. Moreover, wheat-based meat alternatives offer versatility in cooking, which boosts the segment growth.

Product Analysis

In terms of product, the segmentation includes burger patties, sausages, strips & nuggets, meatballs, and other products. The burger patties segment accounted for 43.43% of the U.S. plant-based meat market revenue in 2025. American consumers, already familiar with traditional beef burgers, have quickly adopted plant-based versions offered by leading brands such as Beyond Meat and Impossible Foods. These patties are commonly found in restaurants, fast-food chains, and retail stores across the country. Their popularity is driven by taste improvements, high protein content, and broad availability. Many flexitarians choose plant-based burgers as an easy way to reduce meat consumption without sacrificing flavor, thereby fueling the segment growth.

Distribution Channel Analysis

In terms of distribution channel, the segmentation includes retail outlets, foodservice, and e-commerce. The e-commerce segment held a 12.69% revenue share in 2025, as e-commerce has become an increasingly important channel for plant-based meat sales in the U.S. Consumers appreciate the convenience of ordering products online and having them delivered directly to their homes. Brands are using direct-to-consumer (D2C) websites, grocery delivery apps, and online retailers such as Amazon to reach a wider audience. E-commerce further allows companies to test new products, offer subscriptions, and collect feedback. Plant-based meat brands are investing more in online marketing and distribution with digital shopping now a normal part of American life, thereby driving the segment growth.

Real-World Applications of Plant-Based Meat

- Plant-Based Burgers: Widely used in fast food chains, restaurants, and retail burger products.

- Vegan Sausages: Commonly sold in supermarkets and grocery retail stores.

- Plant-Based Nuggets & Strips: Popular for quick meals, snacks, and frozen food products.

- Restaurant Menu Items: Used in tacos, sandwiches, pizzas, pasta, and wraps.

- Ready-to-Eat Frozen Meals: Included in packaged frozen meals for convenience-focused consumers.

- Foodservice Applications: Used in hotels, cafeterias, schools, and catering services across the U.S.

Source: Polaris Market Research Analysis

Key Players & Competitive Analysis

The U.S. plant-based meat market features a competitive landscape dominated by both specialized plant-based companies and major food corporations. Leading innovators like Beyond Meat Inc. and Impossible Foods Inc. have set industry benchmarks with their realistic meat alternatives, strong retail presence, and partnerships with fast-food chains. Amy’s Kitchen Inc., Tofurky, and Quorn Foods maintain steady consumer bases with a focus on natural ingredients and vegetarian heritage. Large players such as Conagra Brands, Inc., Unilever, Kellogg, and Maple Leaf Foods Inc. have expanded into the space through innovation and acquisitions to meet rising consumer demand. VBites Foods Limited adds further competition with its diverse range of products. These companies compete on innovation, taste, texture, price, and sustainability. Increasing investments in R&D, marketing, and direct-to-consumer models reflect the market’s growth potential. As consumer preferences evolve, competition is expected to intensify, particularly in product quality, distribution, and health-focused offerings.

Key Players

- Amy’s Kitchen Inc.

- Beyond Meat Inc.

- Conagra Brands, Inc.

- Impossible Foods Inc.

- Kellogg

- Maple Leaf Foods Inc.

- Quorn Foods

- Tofurky

- Unilever

- VBites Foods Limited

U.S. Plant-Based Meat Industry Developments

- May 2026: Beyond Meat shifted focus beyond meat alternatives toward broader plant-protein products. The company introduced a high-protein drink targeting GLP-1 medication users in New York. (Source: foodnavigator.com)

- May 2026: Taco Bell partnered with Beyond Meat to test a new plant-based protein product in the U.S. market. (Source: greenqueen.com.hk)

Challenges in Plant Based Meat Market

- High product prices compared to conventional meat limit adoption among price-sensitive consumers.

- Many consumers still feel plant-based meat does not fully match the taste and texture of animal meat.

- Consumer perception regarding processed ingredients and additives affects product acceptance.

- Strong competition from the traditional meat industry creates challenges for market penetration and pricing.

- Limited awareness and hesitation among some consumers continue to restrict large-scale adoption.

Future Outlook

The U.S. plant-based meat market is expected to grow steadily over the forecast period. Rising adoption of alternative proteins and the growing flexitarian population are supporting demand. Companies are focusing on improving taste, texture, and nutritional value through product innovation. Better price parity with animal meat is also expected to increase consumer adoption. Investments in sustainable food technologies and plant-based food ecosystems across the U.S. are further driving market growth.

U.S. Plant-Based Meat Market Segmentation

By Source Outlook (Revenue, USD Billion, 2021–2034)

- Soy

- Wheat

- Peas

- Other Sources

By Product Outlook (Revenue, USD Billion, 2021–2034)

- Burger Patties

- Sausages

- Strips & Nuggets

- Meatballs

- Other Products

By Distribution Channel Outlook (Revenue, USD Billion, 2021–2034)

- Retail Outlet

- Foodservice

- E-commerce

U.S. Plant-Based Meat Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 4.55 Billion |

| Market Size in 2026 | USD 4.58 Billion |

| Revenue Forecast by 2034 | USD 23.86 Billion |

| CAGR | 20.2% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

FAQ's

The market size was valued at USD 4.55 billion in 2025 and is projected to grow to USD 23.86 billion by 2034.

The market is projected to register a CAGR of 20.2% during the forecast period.

A few of the key players in the market are Amy’s Kitchen Inc.; Beyond Meat Inc.; Conagra Brands, Inc.; Impossible Foods Inc.; Kellogg; Maple Leaf Foods Inc.; Quorn Foods; Tofurky; Unilever; and VBites Foods Limited.

The soy segment dominated the market with 40.0% share in 2025.

The e-commerce segment held a 12.69% revenue share in 2025.

Download Sample Report of U.S. Plant-Based Meat Market

Please fill out the form to request a customized copy of the research report.