U.S. Printing Inks Market Demand Senario, Forecast Report, 2025-2034

REPORT DETAILS

Market Statistics

Overview

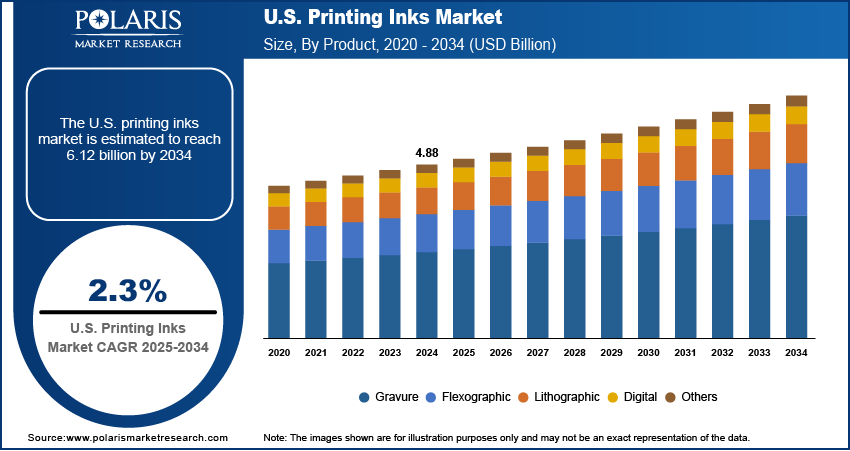

The U.S. printing inks market size was valued at USD 4.88 billion in 2024, growing at a CAGR of 2.3% from 2025 to 2034. Consumer preference for environmentally friendly products is driving demand for biodegradable, water-based, and low-VOC printing inks, especially in packaging applications. This factor prompts manufacturers to invest in greener formulations to align with sustainability goals and regulatory compliance.

Key Insights

- The lithographic segment captured ~47% of the market share in 2024, driven by widespread use in commercial printing, newspapers, and high-volume publishing applications.

- The acrylic segment held ~33% of the revenue share in 2024, supported by excellent adhesion, gloss retention, and resistance to chemicals and environmental factors.

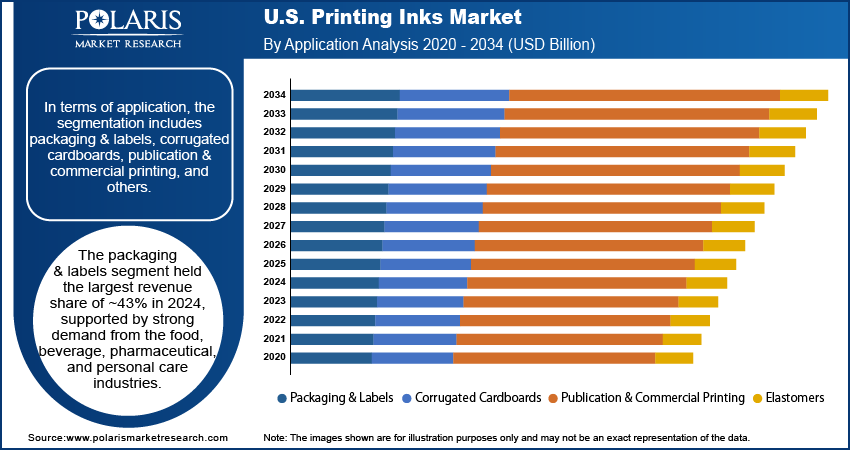

- The packaging & labels segment led with ~43% share in 2024, fueled by rising demand from food, beverage, pharmaceutical, and personal care industries for branded and compliant packaging.

Industry Dynamics

- Rising demand for sustainable and bio-based inks is driving innovation in eco-friendly formulations across packaging and commercial printing.

- Growth in e-commerce and food packaging is increasing the need for high-quality, durable, and branded printed materials.

- Adoption of digital printing technologies enables faster turnaround and customized packaging with reduced ink waste and energy use.

- Stringent environmental regulations and VOC emission increase compliance costs and challenge traditional ink manufacturing processes.

Market Statistics

- 2024 Market Size: USD 4.88 billion

- 2034 Projected Market Size: USD 6.12 billion

- CAGR (2025–2034): 2.3%

Source: Polaris Market Research Analysis

AI Impact on U.S. Printing Inks Market

- AI enhances performance optimization in the U.S. printing inks market by leveraging data analytics to fine-tune ink behavior across diverse substrates, regional climate conditions, and printing technologies for superior consistency and print quality.

- Integration of AI enables intelligent ink customization, dynamically modifying pigment concentration, flow properties, and curing parameters in response to print speed, material type, and application-specific demands.

- AI-driven monitoring systems support proactive maintenance by detecting early signs of component wear, formulation instability, or system inefficiencies, minimizing operational disruptions and maximizing uptime in high-volume printing environments.

- AI improves operational workflows by automating ink management, optimizing print settings in real time, and providing actionable insights, resulting in higher efficiency, reduced material waste, and enhanced competitiveness for U.S. commercial and packaging printers.

The printing inks market comprises the production and supply of colored fluids used in printing applications across packaging, publishing, commercial, and industrial sectors. These inks, based on various formulations such as solvent-based, water-based, or UV-curable, are essential for delivering text, images, and graphics onto diverse substrates such as paper, plastics, and metals. Increasing adoption of digital printing in textile, ceramic, and promotional product sectors is propelling the demand for specialized inks that offer superior adhesion, chemical resistance, and color vibrancy for diverse substrates.

The demand for faster curing times, enhanced durability, and minimal environmental impact is supporting the growth of UV-curable inks, especially in label printing, commercial graphics, and electronics applications, where performance and efficiency are critical. Moreover, growing emphasis on product differentiation and personalized branding across consumer goods is driving demand for specialty inks with enhanced color vibrancy, texture, and finish. It encourages innovation in pigment dispersion and print performance.

Drivers & Opportunities

Expansion of E-commerce Sector: Expansion of the e-commerce sector is driving a shift in printing ink demand, especially for packaging applications. According to the Census Bureau U.S., retail e-commerce sales for Q1 2025 was at USD 300.2 billion. Online retailers rely heavily on corrugated boxes, which require high-quality printed surfaces for brand visibility and consumer engagement. This has created a strong need for inks that offer fast drying times, abrasion resistance, and sharp image reproduction on diverse substrates. Manufacturers are responding by developing inks compatible with high-speed digital and flexographic presses used in packaging lines. These inks must perform well across various climates and shipping conditions. The rise in personalized packaging and short-run print jobs further accelerates the adoption of innovative ink formulations tailored to e-commerce needs.

Growth in Food and Beverage Packaging: Growth in food and beverage packaging is significantly influencing the U.S. printing inks market. In the U.S., retail and food services sales reached $720.1 billion in June 2025, up 0.6% from May and 3.9% year-on-year, reflecting strong consumer spending in food and beverage sectors, driving increased demand for packaging and printing inks. Changing lifestyles and rising demand for convenience foods have led to increased consumption of packaged items, which require strict regulatory compliance in terms of ink safety and performance. Food packaging printing inks must meet FDA guidelines for low migration and avoid substances that can contaminate contents. This has spurred investments in developing water-based, solvent-free, and UV-curable inks designed for safe use on flexible films, cartons, and labels. Innovations are focused on maintaining print clarity and adhesion while ensuring chemical stability under refrigeration or heating conditions.

Source: Polaris Market Research Analysis

Segmental Insights

Product Analysis

Based on product, the U.S. printing inks market segmentation includes gravure, flexographic, lithographic, digital, and others. The lithographic segment accounted for the largest revenue share of ~47% in 2024 due to its broad adoption across commercial printing, newspapers, and high-volume publishing. The process offers cost-efficiency in large-scale production, high image quality, and compatibility with a wide range of substrates, including paper, cardboard, and plastics. Its established infrastructure in print houses and adaptability to both traditional and hybrid printing setups further support its large market share. Continuous improvements in eco-friendly inks used in lithographic presses have also helped align the segment with evolving sustainability goals, reinforcing its preference among print service providers.

The flexographic segment is expected to register the highest CAGR in the U.S. printing inks market from 2025 to 2034, supported by their expanding use in flexible packaging, labels, and corrugated boxes. The segment is benefiting from innovations in low-viscosity, water-based, and UV-curable inks that enhance print clarity and drying speed. Print converters are increasingly adopting flexographic presses due to their faster setup times, substrate versatility, and suitability for high-speed runs. Demand for visually appealing, durable, and environmentally safer packaging for food, beverage, and personal care products is prompting manufacturers to invest in flexographic technology and specialized inks that meet industry-specific performance and compliance standards.

Resin Analysis

In terms of resin, the U.S. printing inks market segmentation includes modified resin, modified cellulose, acrylic, polyurethane, and others. The acrylic segment held the largest revenue share of ~33% in 2024, driven by their strong adhesion, gloss retention, and chemical resistance across diverse printing applications. The segment benefits from widespread use in water-based and UV-curable ink formulations, particularly for packaging and commercial print media. Acrylic-based inks offer fast drying times and compatibility with high-speed printing processes. Therefore, they are suitable for flexographic and digital technologies. Increasing focus on low-VOC and non-toxic ink solutions has further boosted demand for acrylic resins, given their environmental advantages.

The polyurethane segment is expected to register the highest CAGR from 2025 to 2034 in the U.S. printing inks market, due to rising adoption in high-performance ink systems used for flexible packaging, textiles, and industrial labels. Their excellent abrasion resistance, elasticity, and chemical stability make them suitable for applications that require durability and moisture resistance. These properties are particularly valued in food packaging, where surface integrity and compliance with migration limits are crucial. Ongoing research into bio-based and waterborne polyurethane inks is aligning the segment with sustainability demands. Rising demand for solvent-free and VOC-compliant ink solutions in regulated sectors is further pushing investments in polyurethane-based formulations.

Application Analysis

In terms of application, the U.S. printing inks market segmentation includes packaging & labels, corrugated cardboards, publication & commercial printing, and others. The packaging & labels segment held the largest revenue share of ~43% in 2024. The dominance is supported by strong demand from the food, beverage, pharmaceutical, and personal care industries. Growth in consumer packaged goods and increasing brand competition have driven the need for high-quality, vibrant, and durable inks that enhance shelf appeal and meet regulatory compliance. Technological advancements in inkjet and flexographic printing have enabled faster turnaround and greater customization in packaging design. The rise of smart packaging and demand for eco-friendly labels has also contributed to innovation in UV and water-based inks that offer performance without compromising environmental standards.

The publication & commercial printing segment is expected to register a significant CAGR in the U.S. printing inks market from 2025 to 2034. The growth is driven by niche demand in magazines, catalogs, brochures, and corporate print materials. While digital media continues to disrupt traditional print, certain applications still rely on high-quality print finishes and tactile experiences. Improvements in digital and offset printing technologies are helping reduce costs and turnaround time while maintaining image quality. Premium and customized marketing materials continue to attract demand from retail, hospitality, and real estate sectors. Print service providers are also shifting toward sustainable and low-VOC inks to meet environmental expectations from clients across commercial sectors.

Source: Polaris Market Research Analysis

Key Players & Competitive Analysis

The competitive landscape of the U.S. printing inks market is defined by active industry analysis and aggressive market expansion strategies among key players. Companies are increasingly engaging in mergers and acquisitions to consolidate market share, streamline production capabilities, and gain access to specialized technologies. Joint ventures and strategic alliances are being used to enhance supply chain efficiency and broaden product portfolios, particularly in eco-friendly and food-safe ink formulations.

Post-merger integration is a focal point for achieving cost synergies and operational alignment. Technology advancements remain at the core of competition, with firms investing in high-speed digital printing, low-VOC formulations, and sustainable resins to meet evolving consumer demands. Competitive differentiation is also driven by customized ink solutions tailored for specific substrates, applications, and regulatory compliance needs. This dynamic environment reflects a shift toward innovation-led growth and customer-centric strategies, allowing companies to maintain relevance in a rapidly changing packaging and commercial printing ecosystem.

Key Players

- ALTANA AG

- Ashland Inc.

- DIC Corporation

- DuPont

- Flint Group

- Huber Group

- Royal Dutch Printing Ink Factories Van Son

- Siegwerk

- Sun Chemical

- TOKYO PRINTING INK MFG Co. Ltd

- Wikoff Color Corporation

- Zeller+Gmelin GmbH & Co. KG

U.S. Printing Inks Industry Developments

April 2025: Sun Chemical introduced its SunPak PowerPace series of printing inks specifically designed for paper and board applications in North America

September 2024: DuPont launched Advanced Artistri Digital Printing Ink Technology at PRINTING United 2024.

April 2025: INX International introduced its new RUCOINX product lines and rebranded TRIANGLE to INXJet, signaling a strategic shift in its branding and product offerings within the market.

U.S. Printing Inks Market Segmentation

By Product Outlook (Revenue, USD Billion, 2020–2034)

- Gravure

- Flexographic

- Lithographic

- Digital

- Others

By Resin Outlook (Revenue, USD Billion, 2020–2034)

- Modified Rosin

- Modified Cellulose

- Acrylic

- Polyurethane

- Others

By Application Outlook (Revenue, USD Billion, 2020–2034)

- Packaging & Labels

- Corrugated Cardboards

- Publication & Commercial Printing

- Others

U.S. Printing Inks Market Report Scope

| Report Attributes | Details |

| Market Size in 2024 | USD 4.88 billion |

| Market Size in 2025 | USD 4.99 billion |

| Revenue Forecast by 2034 | USD 6.12 billion |

| CAGR | 2.3% from 2025 to 2034 |

| Base Year | 2024 |

| Historical Data | 2020–2023 |

| Forecast Period | 2025–2034 |

| Quantitative Units | Revenue in USD billion and CAGR from 2025 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

FAQ's

The U.S. market size was valued at USD 4.88 billion in 2024 and is projected to grow to USD 6.12 billion by 2034.

The U.S. market is projected to register a CAGR of 2.3% during the forecast period.

A few of the key players in the market are ALTANA AG, Ashland Inc., DIC Corporation, DuPont, Flint Group, Huber Group, Royal Dutch Printing Ink Factories Van Son, Siegwerk, Sun Chemical, TOKYO PRINTING INK MFG Co. Ltd, Wikoff Color Corporation, and Zeller+Gmelin GmbH & Co. KG.

The lithographic segment accounted for the largest revenue share of ~47% in 2024, due to its broad adoption across commercial printing, newspapers, and high-volume publishing.

The acrylic segment held the largest revenue share of ~33% in 2024, driven by their strong adhesion, gloss retention, and chemical resistance across diverse printing applications.

Download Sample Report of U.S. Printing Inks Market

Please fill out the form to request a customized copy of the research report.