U.S. Space Cybersecurity Market Size, Share, Forecast Report 2026-2034

REPORT DETAILS

REPORT DETAILS

U.S. Space Cybersecurity Market Summary

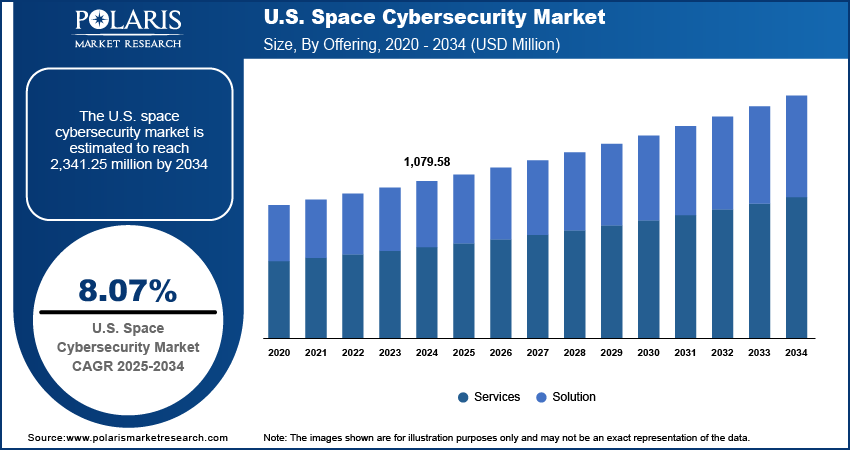

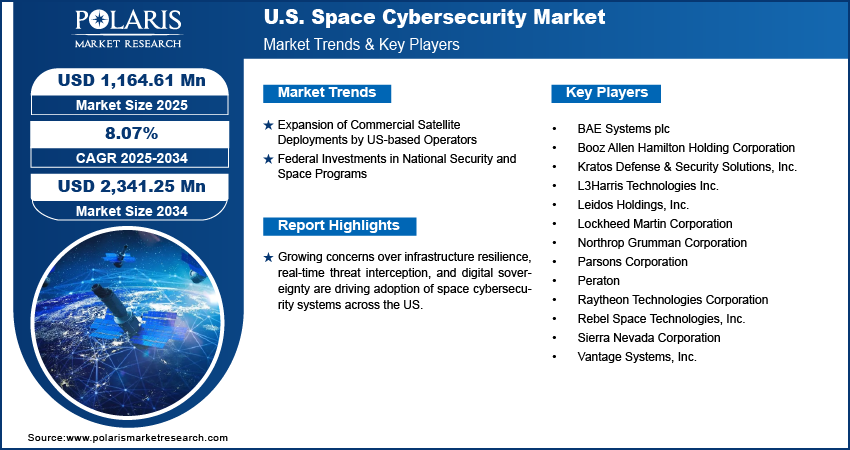

The U.S. space cybersecurity market size was valued at USD 1,164.61 million in 2025. The market is projected to grow at a CAGR of 8.07% from 2026 to 2034. Expansion of commercial satellite deployments by U.S. operators, coupled with increasing federal investment in national security and space programs, is driving the demand for advanced space cybersecurity solutions.

Market Statistics

Key Takeaways

- The solution segment is projected to grow substantially at a 7.4% CAGR. This growth is due to heightened investment in advanced encryption and secure communication frameworks.

- The services segment is projected to grow at a 9.0% CAGR, driven by the need for continuous monitoring and threat intelligence.

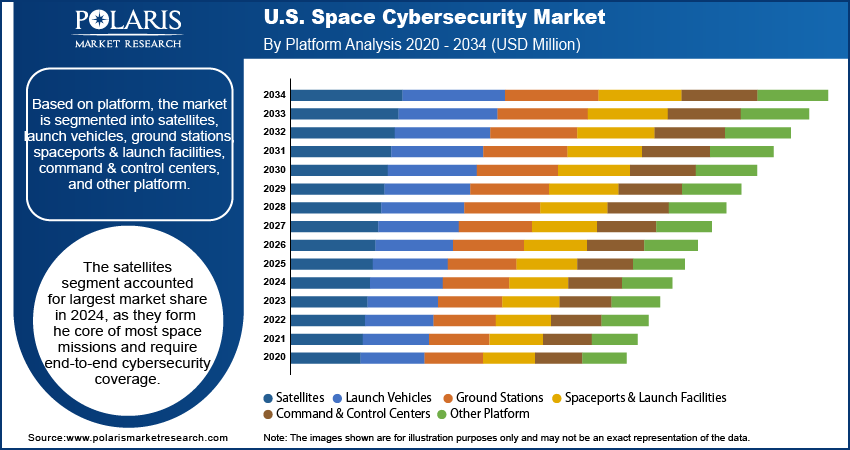

- The satellites segment accounted for the largest market share of 36.54% in 2025. It is fueled by the growing deployment of commercial and defense satellite constellations.

- The command & control centers segment is projected to grow at a 9.0% CAGR. The segment’s growth is driven by its central role in managing telemetry.

- The government & defense segment dominated the market with a 52.28% share in 2025. This is due to the presence of well-established agencies consistently funding advanced protective measures.

Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations.

Industry Dynamics

- The increasing commercial space activity across the U.S. is generating sustained demand for space cybersecurity.

- Federal funding allocated to space and defense initiatives is playing an important role in driving space cybersecurity solutions.

- The development of AI-driven threat detection and anomaly detection systems is creating several market opportunities.

- High costs of compliance may present market challenges.

AI Impact on U.S. Space Cybersecurity Market

- AI enables quicker identification of cyberattacks by analyzing satellite and earth-based system data in real time.

- It enhances cybersecurity for space infrastructure assets by identifying anomalies in network and communication infrastructures.

- AI helps provide faster responses to attacks by triggering automated alerts and security measures.

- It enhances cybersecurity by effectively monitoring space infrastructure.

US space cybersecurity solutions are designed to safeguard satellite internet, satellite ground stations, and space-based communication systems from digital threats. These systems integrate advanced encryption protocols, intrusion detection software, and secure command architectures within a unified framework to ensure operational integrity. Modular platforms allow for seamless upgrades and quick adaptation to emerging threat landscapes.

Source: Polaris Market Research Analysis

Vendors across the US are prioritizing standardized security protocols, AI-driven anomaly detection tools, and remote incident response capabilities to enhance threat resilience. The use of radiation-hardened hardware, secure firmware updates, and tamper-resistant data links addresses critical requirements for mission assurance. Space cybersecurity systems are increasingly deployed across both low Earth orbit (LEO) and geostationary (GEO) operations, offering scalability, interoperability, and high-level protection. These solutions continue to evolve in line with government directives and national security programs focused on critical infrastructure protection.

Growing attention to critical infrastructure resilience and digital sovereignty is shaping the adoption of space cybersecurity solutions across the US. Recently, in April 2025, US Space Force (USSF) launched the Orbital Watch initiative to enhance space domain awareness and bolster cybersecurity for commercial space assets, aiming to safeguard satellite operations against emerging cyber and orbital threats. These systems are incorporated into military-grade communication networks, ground control centers, and scientific missions due to their modular architecture, secure design, and compatibility with emerging command protocols. System integrators and federal contractors are selecting solutions that offer rapid deployment, tamper-resistant hardware, and compliance with evolving cybersecurity frameworks tied to space operations.

Rising focus on secure supply chains and controlled component sourcing is improving system reliability while reducing vulnerabilities tied to foreign interference. Manufacturers are offering pre-validated security modules with built-in diagnostics to support streamlined deployment and certification processes. In critical research programs and inter-agency space initiatives, these systems ensure long-term continuity, secure data relay, and coordinated threat response. Their usage expanding under contingency planning protocols, where space cybersecurity solutions serve as essential safeguards for command-and-control continuity across defense, civil, and commercial missions. These developments are driving deeper integration of cybersecurity across US space infrastructure strategy.

Space Cybersecurity vs Traditional Cybersecurity

| Aspect | Space Cybersecurity | Traditional Cybersecurity |

| Environment | Ensures security of satellites, spacecraft and ground stations in space-based system environment | Ensures security of information technology systems, servers, networks and devices in Earth-based environment |

| Latency | High latency because of long-distance space-based communication | Low latency with almost real-time communication |

| Accessability | Highly restricted physical accessibility after deployment in orbit | Easy physical and remote accessibility |

| Update | Hard to update frequently as hardware/software changes | Updates and patches can be easily deployed |

| Security Approach | Necessitates high level of autonomy of security system | Necessitates central control of security system |

Source: Polaris Market Research Analysis

Industry Dynamics

Expansion of Commercial Satellite Deployments by US-based Operators

Increasing commercial satellite activity across the US is generating sustained demand for robust space cybersecurity industry. As per the Ill-Defined Space, US launch providers carried out 154 launches, a 40% rise from 110 in 2023. These launches made up about 61% of all global orbital launches, averaging nearly 13 per month. Private sector operators are deploying small satellite constellations, Earth observation platforms, and communication relays to support applications ranging from broadband internet to climate monitoring. As mission volumes grow and orbits become more populated, the risk of unauthorized access, data interception, and system manipulation rises sharply. Thus, commercial entities are prioritizing embedded encryption systems, secure telemetry, and resilient communication protocols as part of standard satellite architecture to counter these risks.

Vendors are responding by offering modular cybersecurity tools that integrate directly with mission planning, satellite operations, and ground station management. These tools enable real-time threat detection, identity verification, and encrypted command exchanges across multiple orbital layers. The commercial segment focus on cost-efficiency and operational speed for the adoption of pre-certified, scalable security modules. With the US emerging as a global hub for commercial satellite innovation, cybersecurity requirements are embedded earlier in development cycles, ensuring compatibility with international regulatory expectations and cross-operator coordination standards.

Federal Investments in National Security and Space Programs

Federal funding allocated to space and defense initiatives is playing an important factor in driving the space cybersecurity solutions. The US Department of Defense (DoD), US Space Force, and other strategic agencies are investing in hardened communication infrastructure, secure orbital surveillance platforms, and anti-jamming capabilities to preserve mission integrity. As an example, in May 2024, the US DoD announced the FY2025 budget that includes USD 33.7 billion for space programs, with USD 2.4 billion for launch capabilities, USD 1.5 billion for stronger navigation systems, and USD 4.2 billion for secure satellite communications. These investments are boosting the development of resilient command systems, intrusion-resistant architecture, and advanced signal encryption tailored to military-grade operational conditions.

Programs under agencies such as National Aeronautics and Space Administration (NASA) and Defense Advanced Research Projects Agency (DARPA) are further contributing to research in quantum-resistant encryption, autonomous threat detection, and AI-based monitoring tools for space-based assets. Additionally, budget proposals continue to prioritize cybersecurity within multi-orbit missions and cross-domain coordination systems, ensuring protection across land, sea, air, and space operations. These efforts enhance national readiness and stimulate commercial innovation through technology transfer and procurement contracts, fostering a secure ecosystem that helps US dominance in space-related activities.

Challenges in Space Cybersecurity Market

The market has several constraints, including costly deployment and a complicated system design. Cybersecurity threats and the inability to upgrade existing satellites are also significant issues affecting the market. There is a lack of universal standards for cybersecurity in space applications, resulting in different security capabilities in each process. Furthermore, satellites have a prolonged lifecycle. This increases their vulnerability to emerging cybersecurity threats and necessitates more advanced security solutions.

Source: Polaris Market Research Analysis

Segmental Insights

Offering Analysis

The segmentation, based on offering includes, solution and services. The solution segment is projected to grow substantially with CAGR 7.4%. This growth is due to heightened investment in advanced encryption, secure communication frameworks, and threat detection software integrated across space assets. The demand for mission-specific software, onboard cyber defense tools, and hardened firmware is rising among both government and commercial operators. These solutions offer scalable protection across satellite constellations, launch platforms, and command infrastructure, making them a preferred choice for securing complex and distributed space systems.

The services segment is projected to grow at a robust pace of CAGR 9.0% in the coming years, driven by the need for continuous monitoring, threat intelligence, risk assessments, and compliance consulting. As new space missions adopt more sophisticated cybersecurity standards, operators are turning to specialized service providers for ongoing support, incident response, and systems training. This trend is further reinforced by evolving federal cybersecurity guidelines, which mandate third-party audits, managed security services, and lifecycle-based vulnerability assessments.

Platform Analysis

The segmentation, based on offering includes, satellites, launch vehicles, ground stations, spaceports & launch facilities, command & control centers, and other platform. The satellites segment accounted for largest market share of 36.54% in 2025, fueled by growing deployment of commercial and defense satellite constellations in low Earth orbit and geostationary orbit. These assets are exposed to a broad range of cyber risks, including signal interception, command spoofing, and malware intrusion. To mitigate these vulnerabilities, US operators are integrating secure communication layers, hardware-based authentication, and automated recovery mechanisms directly into satellite systems.

The command and control centers segment is projected to grow at a significant pace of CAGR 9.0% during the assessment phase, driven by their central role in managing telemetry, tracking, and secure mission execution. The concentration of high-value data, operational commands, and real-time decision-making processes made these facilities a priority for cybersecurity enhancement. Upgrades in access controls, network segmentation, and endpoint protection are rapidly adopted to secure critical nodes in the operational chain.

End User Analysis

The segmentation, based on end user includes, government & defense and commercial. The government and defense segment dominated the market share of 52.28% in 2025, due to the presence of well-established agencies including the Department of Defense, US Space Force, and NASA are consistently funding advanced protective measures to safeguard national assets, classified data streams, and secure communications. For instance, in June 2025, the Pentagon proposed a USD 1.01 trillion budget for FY2026, focusing on cybersecurity and space systems to better protect satellites and U.S. assets from growing cyber threats. These efforts are backed by long-term contracts, defense-grade standards, and dedicated cybersecurity divisions focused on threat resilience in space operations.

The commercial segment is estimated to hold a substantial market share in 2034, as private companies expand their presence in satellite communications, Earth observation, and space-based research. These operators are increasingly investing in cybersecurity tools to meet regulatory compliance, protect proprietary data, and ensure operational reliability. The rapid onboarding of digital infrastructure and rising cyber risk awareness is pushing cybersecurity to the forefront of mission planning in the private space sector.

Source: Polaris Market Research Analysis

Key Players & Competitive Analysis Report

The space cybersecurity industry is highly competitive, shaped by rapid advancements in space technology, growing threat exposure, and expanding national security requirements. Companies operating in this domain are focusing on integrated solutions that combine satellite protection, ground infrastructure security, and encrypted communication systems. Development strategies are centered around real-time threat detection, AI-based anomaly monitoring, and modular cybersecurity platforms capable of supporting diverse mission profiles. There is a strong emphasis on systems that reduce cyber risk exposure, support interoperability across defense and commercial networks, and maintain operational continuity in high-risk environments.

Key companies in the US space cybersecurity industry include Lockheed Martin Corporation, Northrop Grumman Corporation, Raytheon Technologies Corporation, L3Harris Technologies Inc., Booz Allen Hamilton Holding Corporation, BAE Systems plc, Parsons Corporation, Leidos Holdings, Inc., Kratos Defense & Security Solutions, Inc., Peraton, Sierra Nevada Corporation, Rebel Space Technologies, Inc., and Vantage Systems, Inc.

Key Players

- BAE Systems plc

- Booz Allen Hamilton Holding Corporation

- Kratos Defense & Security Solutions, Inc.

- L3Harris Technologies Inc.

- Leidos Holdings, Inc.

- Lockheed Martin Corporation

- Northrop Grumman Corporation

- Parsons Corporation

- Peraton

- Raytheon Technologies Corporation

- Rebel Space Technologies, Inc.

- Sierra Nevada Corporation

- Vantage Systems, Inc.

Industry Developments

- April 2025: Frontgrade Gaisler collaborated with wolfSSL to deliver advanced security for its radiation-tolerant space processors. The joint effort combines Gaisler's space-hardened microprocessors, such as the GR740, with wolfSSL's wolfCrypt library to ensure protection against cyber threats. (source: gaisler.com)

US Space Cybersecurity Market Segmentation

By Offering Outlook (Revenue, USD Million, 2021–2034)

- Solution

- Network security

- Endpoint and IoT security

- Application security

- Cloud security

- Others

- Services

- Professional Services

- Managed Services

By Platform Outlook (Revenue, USD Million, 2021–2034)

- Satellites

- Launch Vehicles

- Ground Stations

- Spaceports & Launch Facilities

- Command & Control Centers

- Other Platform

By End User Type Outlook (Revenue, USD Million, 2021–2034)

- Government & Defense

- Commercial

US Space Cybersecurity Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 1,164.61 Million |

| Market Size in 2026 | USD 1,259.21 Million |

| Revenue Forecast by 2034 | USD 2,341.25 Million |

| CAGR | 8.07% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Million and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

The US market size was valued at USD 1,164.61 million in 2025 and is projected to grow to USD 2,341.25 million by 2034.

The US market is projected to register a CAGR of 8.07% during the forecast period.

A few of the key players in the market are Lockheed Martin Corporation, Northrop Grumman Corporation, Raytheon Technologies Corporation, L3Harris Technologies Inc., Booz Allen Hamilton Holding Corporation, BAE Systems plc, Parsons Corporation, Leidos Holdings, Inc., Kratos Defense & Security Solutions, Inc., Peraton, Sierra Nevada Corporation, Rebel Space Technologies, Inc., and Vantage Systems, Inc.

The satellites segment accounted for largest market share of 36.54% in 2025.

The services segment is projected to grow at a robust pace in the coming years.

Download Sample Report of U.S. Space Cybersecurity Market

Please fill out the form to request a customized copy of the research report.