Coalescing Agents Market Opportunity & Global Forecast, 2025-2034

REPORT DETAILS

Coalescing Agents Market

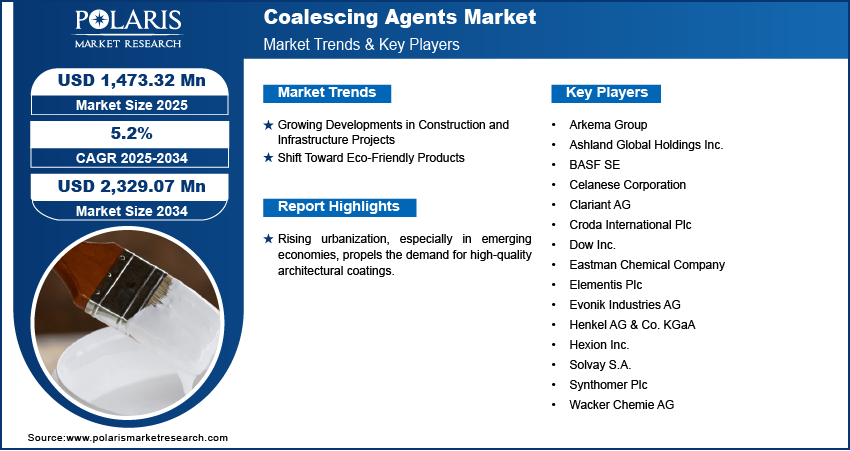

The global coalescing agents market size was valued at USD 1,401.56 million in 2024, growing at a CAGR of 5.2% during the forecast period. The growing demand for coalescing agents across various sectors and the rising introduction of eco-friendly formulations are a few of the key factors driving market growth.

Market Statistics

Key Takeaways

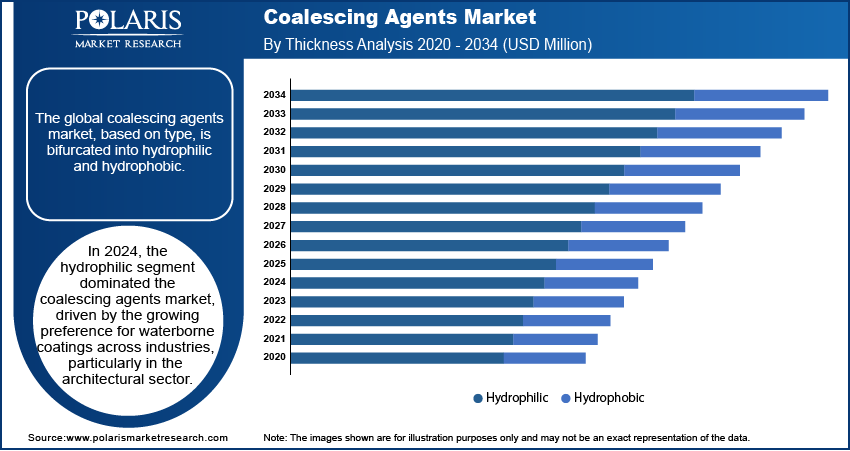

- The hydrophilic segment dominated the market in 2024. The rising preference for waterborne coatings across industries drives the segment’s leading market position.

- The personal care ingredients segment is projected to witness the fastest growth, owing to the growing demand for personal care products that need effective film-forming agents.

- The market in North America is growing due to the rising demand for coalescing agents across industrial, construction, and automotive sectors.

- Asia Pacific is projected to register the highest CAGR. The market growth in the region is driven by increased automotive production and a growing construction sector.

Industry Dynamics

- Growing urbanization, especially in emerging economies, is fueling the need for coalescing agents and driving market growth.

- Rising shift towards eco-friendly products owing to the introduction of stringent environmental regulations is fueling market demand.

- The increasing focus on sustainability and performance across various industries is expected to create several market opportunities.

- Increasing regulatory pressure regarding volatile organic compounds may present market challenges.

Source: Polaris Market Research Analysis

To Understand More About this Research:Download Sample Report

Coalescing agents are essential additives used to optimize the film formation process in waterborne coatings, enhancing properties such as durability and appearance. These agents facilitate the fusion of polymer particles in the coating, resulting in a smooth, continuous film. This property is particularly vital in the construction industry, where high-quality architectural coatings are required to withstand harsh environmental conditions and enhance aesthetic appeal. Government bodies of various countries across the world are introducing stringent environmental regulations, pushing manufacturers to develop low-VOC (volatile organic compounds) products. This shift is driving innovation, with a focus on sustainable and bio-based solutions that meet regulatory standards while delivering optimal performance.

Market Dynamics

Growing Developments in Construction and Infrastructure Projects

Rising urbanization, especially in emerging economies, propels the demand for high-quality architectural coatings. For instance, the United Nations Population Fund reports that over 50% of the global population currently resides in urban areas. Projections indicate that by 2030, this figure will rise to approximately 5 billion individuals, highlighting the significant trend toward urbanization on a global scale. These coatings require effective coalescing agents to ensure durability and an attractive finish. Rising development of large-scale infrastructure projects, growing construction of residential and commercial buildings, and increasing renovation activities fuel the requirement for advanced paints and coatings. This trend is expected to continue as governments and private sectors invest significantly in infrastructure development to support economic growth, further boosting the growth.

Shift Toward Eco-Friendly Products

There is an increasing emphasis on reducing VOC (volatile organic compounds) emissions in paints and coatings owing to the introduction of strict environmental regulations across the world. For instance, a Gratitude survey reveals a pivotal shift in consumer behavior, with 72% prioritizing eco-friendly products, highlighting the growing demand for sustainable offerings. This has led to a shift toward sustainable, low-VOC, and bio-based coalescing agents. Manufacturers are investing heavily in research and development to create innovative products that meet these regulatory requirements while maintaining high performance. Consumers are also becoming environmentally conscious, driving demand for green products that offer ecological benefits and superior quality.

Technological Advancements and Product Innovation

Companies are focusing on developing new formulations and improving existing ones to enhance performance characteristics such as weather resistance, durability, and ease of application. Innovations in nanotechnology and the development of hybrid coalescing agents that combine the benefits of different types of agents are opening new possibilities. Additionally, there is a growing trend toward customizing products to meet customer requirements, which is driving competitive differentiation and expanding the application scope of coalescing agents across various industries.

Source: Polaris Market Research Analysis

Segment Insights

Market Assessment by Type Outlook

The global market, based on type, is bifurcated into hydrophilic and hydrophobic. In 2024, the hydrophilic segment dominated the industry, driven by the growing preference for waterborne coatings across industries, particularly in the architectural sector. These agents' ability to comply with stringent environmental standards and their suitability for low-VOC formulations make them highly attractive. Furthermore, the increasing investments in green building projects and the global trend toward sustainable development is driving hydrophilic segment. The push for reducing VOC emissions and the advancements in hydrophilic coalescing agent technology are key factors contributing to the demand for hydrophilic coalescing agents.

Hydrophobic coalescing agents is expected to experience fastest CAGR over the forecast period due to their robust performance in industrial applications. These agents are highly valued for their ability to enhance film formation and durability in coatings, adhesives, and sealants, especially under challenging environmental conditions. Their hydrophobic nature ensures resistance to water and moisture, making them ideal for high-performance requirements in sectors such as construction, automotive, and industrial maintenance. This gradually transitioning toward hydrophilic coalescing agents, propelled by stringent environmental regulations and the growing demand for sustainable, eco-friendly solutions. Hydrophilic agents are gaining traction due to their lower volatile organic compound (VOC) emissions and improved compatibility with water-based systems. This shift reflects the industry's focus on balancing performance with environmental responsibility, as manufacturers strive to meet regulatory standards while addressing consumer preferences for greener products.

Market Evaluation by Application Outlook

In terms of application, the global market is segmented into paints & coatings, adhesives & sealants, inks, personal care ingredients, and others. In 2024, the paints & coatings coalescing agents segment dominated the industry, driven by the extensive use of coalescing agents in architectural, automotive, and industrial coatings. The increasing construction activities and urbanization, particularly in emerging economies, fuel the demand for high-performance coatings, which, in turn, boosts the requirement for effective coalescing agents. Additionally, the shift toward waterborne and low-VOC coatings in response to stringent environmental regulations supports the dominance of this segment.

The personal care ingredients segment is expected to witness the fastest CAGR during the forecast period. The growing demand for personal care products, such as lotions, creams, and sunscreens, that require effective film-forming agents, is driving this segment's expansion. The increasing consumer awareness regarding personal grooming and the rising disposable incomes in developing regions are contributing to the rapid growth for this segment. Furthermore, advancements in formulation technologies and the introduction of innovative personal care products are expected to fuel the demand for coalescing agents in this application, making it the fastest-growing segment.

Source: Polaris Market Research Analysis

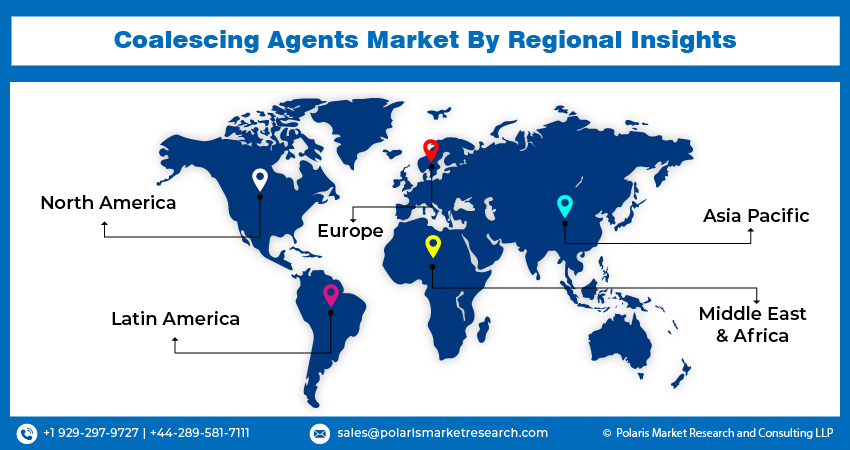

Market by Regional Outlook

By region, the study provides insights into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. The North America coalescing agents market is experiencing significant growth, supported by rising demand from the construction, automotive, and industrial sectors. For instance, according to the US Department of Treasury, there has been a remarkable escalation in construction expenditures targeting manufacturing facilities. Specifically, real investment in manufacturing construction has increased twofold since the conclusion of 2021. Additionally, the EPA’s regulations on volatile organic compounds (VOCs) are encouraging the use of low-VOC coalescing agents.

The industry growth in Latin America is propelled by the construction and automotive sectors, despite economic fluctuations. The Middle East & Africa witnesses increasing demand from construction and infrastructure projects, with a gradual shift toward eco-friendly solutions driven by growing awareness and regulatory measures.

Europe coalescing agents market is characterized by a high demand for sustainable and environmentally friendly products. The Europe is experiencing notable growth, driven by the expanding construction, automotive, and industrial sectors. Coalescing agents are crucial additives used in paints, coatings, and adhesives to enhance film formation and improve the performance of these products. As the European construction industry sees increased activity, the demand for high-quality, durable coatings is rising. Additionally, the automotive sector’s emphasis on advanced, eco-friendly coatings further fuels the growth. Regulatory support for low-VOC (volatile organic compounds) products is also pushing the industry towards innovative, environmentally friendly coalescing agents. According to recent industry reports, the European market is expected to witness substantial expansion, with significant investments in research and development leading to the introduction of new, efficient products. The increasing focus on sustainability and performance in various industrial applications continues to drive dynamics and opportunities.

The paints & coatings industry in countries such as Germany, France, and the UK is a major contributor to the Europe, with a focus on green building practices and energy-efficient solutions boosting the demand for advanced coalescing agents.

The Asia Pacific is expected to experiencing the fastest CAGR during the forecast period. The growing construction industry and increasing automotive production are significant drivers of the regional market. Increasing investment in infrastructure development in the countries like India, China and Japan is also driving the industry. For instance, according to the Press Information Bureau, India's infrastructure budget allocations have surged to USD 120.48 billion for 2023-24 Additionally, the growing middle-class population and rising disposable incomes are leading to higher demand for quality consumer goods, including paints and personal care products, further supporting growth. The region's regulatory environment is also gradually moving toward stricter VOC controls, which is expected to boost the adoption of eco-friendly coalescing agents in the coming years.

Source: Polaris Market Research Analysis

Key Players and Competitive Insights

The competitive landscape of the market is shaped by robust industry analysis and an increasing emphasis on sustainable chemistry and low-VOC technologies. Leading market players are adopting comprehensive expansion strategies, targeting high-growth application areas such as architectural coatings, wood finishes, and industrial paints. The industry is witnessing a surge in joint ventures, strategic alliances, and mergers and acquisitions aimed at strengthening distribution networks, enhancing technological competencies, and accelerating access to green chemistry platforms. Several product launches in the low-emission and bio-based coalescing agent’s category signal the shift toward regulatory compliance and environmental stewardship.

Firms are engaging in post-merger integration efforts to align innovation pipelines, optimize operational synergies, and unify R&D infrastructure for accelerated formulation development. Technology advancements such as reactive coalescing systems, multifunctional additives, and high-performance polymers are driving differentiation and cost-efficiency across end-use sectors. Industry participants are also investing in predictive modeling and formulation software to fine-tune product performance while meeting VOC content regulations. The growing demand for environmentally responsible coatings, combined with increasing pressure for sustainability certifications, is intensifying competition and prompting continuous innovation. The is evolving into a highly specialized and innovation-led landscape, where technical expertise, strategic collaborations, and regulatory foresight are critical to maintaining a competitive edge.

The industry is highly competitive, with several key players striving to enhance their presence through innovation, strategic partnerships, and mergers and acquisitions. Arkema Group; Ashland Global Holdings Inc.; BASF SE; Celanese Corporation; Clariant AG; Croda International Plc; Dow Inc.; Eastman Chemical Company; Elementis Plc; Evonik Industries AG; Henkel AG & Co. KGaA; Hexion Inc.; Solvay S.A.; Synthomer Plc; Wacker Chemie AG are among the prominent players in the market.

Eastman Chemical Company is a global player in the coalescing agents, known for its extensive range of high-performance additives and specialty chemicals. The company focuses on innovation and sustainability, offering products that meet stringent environmental regulations and customer demands for low-VOC and eco-friendly solutions. Eastman's global reach and strong distribution network enable it to serve various industries effectively. A recent news highlight for Eastman is its strategic partnership with automotive and specialty materials companies to develop sustainable materials, showcasing its commitment to driving innovation and sustainability.

BASF SE is another major player in the coalescing agents, renowned for its comprehensive portfolio of chemical products and solutions. BASF's emphasis on research and development has positioned it at the forefront of innovation, particularly in creating advanced and sustainable coalescing agents. The company serves diverse industries, including paints & coatings, adhesives, and personal care. Recently, BASF announced the expansion of its production capacity for waterborne dispersion products in Europe, aimed at supporting the growing demand for environmentally friendly products and strengthening its position.

List Of Key Companies

- Arkema Group

- Ashland Global Holdings Inc.

- BASF SE

- Celanese Corporation

- Clariant AG

- Croda International Plc

- Dow Inc.

- Eastman Chemical Company

- Elementis Plc

- Evonik Industries AG

- Henkel AG & Co. KGaA

- Hexion Inc.

- Solvay S.A.

- Synthomer Plc

- Wacker Chemie AG

Industry Developments

- In May 2024, Dow launched a new EcoDry coalescing agent for water-based paints and coatings, reducing VOC emissions while preserving performance.

Market Segmentation

By Type (Volume, kilotons; Revenue, USD Million; 2020–2034)

- Hydrophilic

- Hydrophobic

By Application (Volume, kilotons; Revenue, USD Million; 2020–2034)

- Paints & Coatings

- Adhesives & Sealants

- Inks

- Personal Care Ingredients

- Others

By Region (Volume, kilotons; Revenue, USD Million; 2020–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Coalescing Agents Report Scope

| Report Attributes | Details |

| Market size value in 2024 | USD 1,401.56 million |

| Market size value in 2025 | USD 1,473.32 million |

| Revenue forecast in 2034 | USD 2,329.07 million |

| CAGR | 5.2% from 2025 to 2034 |

| Base year | 2024 |

| Historical data | 2020–2023 |

| Forecast period | 2025–2034 |

| Quantitative units | Volume in kiloton, Revenue in USD million and CAGR from 2025 to 2034 |

| Report coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments covered |

|

| Regional scope |

|

| Competitive landscape |

|

| Report format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentations. |

Source: Polaris Market Research Analysis

coalescing agents market FAQ's

The global coalescing agents market size was valued at USD 1,401.56 million in 2024 and is projected to grow to USD 2,329.07 million by 2034.

The global market is projected to witness a CAGR of 5.2% during 2025–2034.

North America accounted for the largest share of the global market in 2024.

Arkema Group; Ashland Global Holdings Inc.; BASF SE; Celanese Corporation; Clariant AG; Croda International Plc; Dow Inc.; Eastman Chemical Company; Elementis Plc; Evonik Industries AG; Henkel AG & Co. KGaA; Hexion Inc.; Solvay S.A.; Synthomer Plc; Wacker Chemie AG are a few key players in the market.

The hydrophilic segment dominated the market in 2024.

The paints & coatings segment held the largest share of the global market in 2024.

Coalescing agents are additives used in water-based paints, coatings, adhesives, and other products to enhance film formation. They work by temporarily softening the polymer particles in these formulations, allowing them to fuse together as the water evaporates.

A few key trends observed in this market are described below: Increasing Demand for Eco-Friendly Products: Rising environmental regulations and increasing consumer preference for low-VOC and bio-based coalescing agents. Growing Construction and Infrastructure Projects: Boosted demand for high-performance architectural coatings, particularly in emerging economies. • Companies producing coalescing agents and related additives, firms in the paints and coatings industry, adhesives and sealants manufacturers, personal care and cosmetic companies, developers and contractors, and other consulting firms. Shift Toward Waterborne Coatings: Greater adoption of waterborne formulations due to environmental benefits and regulatory compliance

For a new company entering the global coalescing agents market, prioritizing innovation by developing advanced, low-VOC, and bio-based coalescing agents will be crucial, as environmental regulations continue to tighten and demand for sustainable products rises. Investing in research and development to create high-performance, cost-effective solutions that cater to the needs of various industries, such as construction, automotive, and personal care, will help differentiate the company. Additionally, forming strategic partnerships and collaborations with established industry players can enhance market reach and credibility.

Companies producing coalescing agents and related additives, firms in the paints and coatings industry, adhesives and sealants manufacturers, personal care and cosmetic companies, developers and contractors, and other consulting firms.

Download Sample Report of coalescing agents market

Please fill out the form to request a customized copy of the research report.