Data Center Logistics Market Size, Share & Revenue Forecast 2034

REPORT DETAILS

Data Center Logistics Market Summary

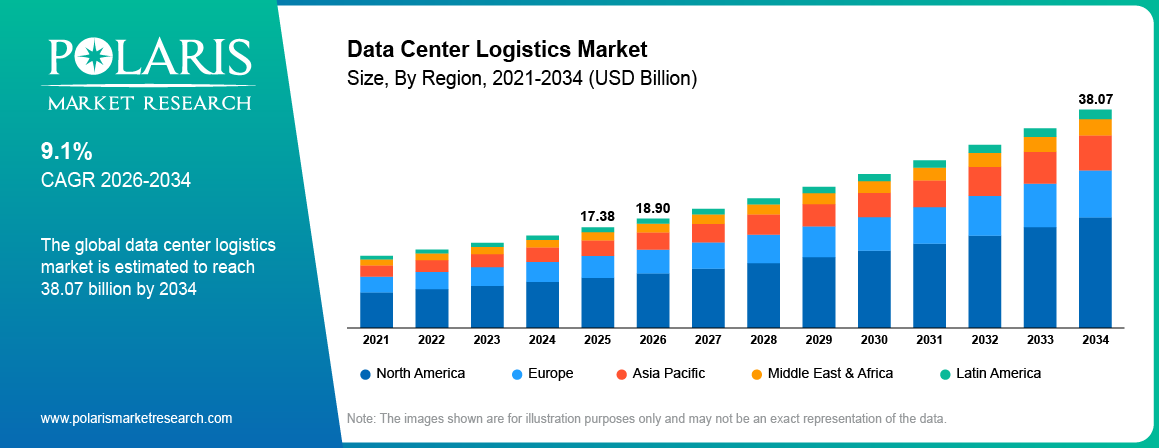

The global data center logistics market is estimated around USD 17.38 Billion in 2025,with consistent growth anticipated during 2026–2034. Rising hyperscale infrastructure investments, increasing AI infrastructure deployment, and growing cloud expansion activities are accelerating demand for specialized data center supply chain solutions worldwide. The market is projected to grow at a CAGR of 9.1% during the forecast period.

Market Statistics

Key Takeaways

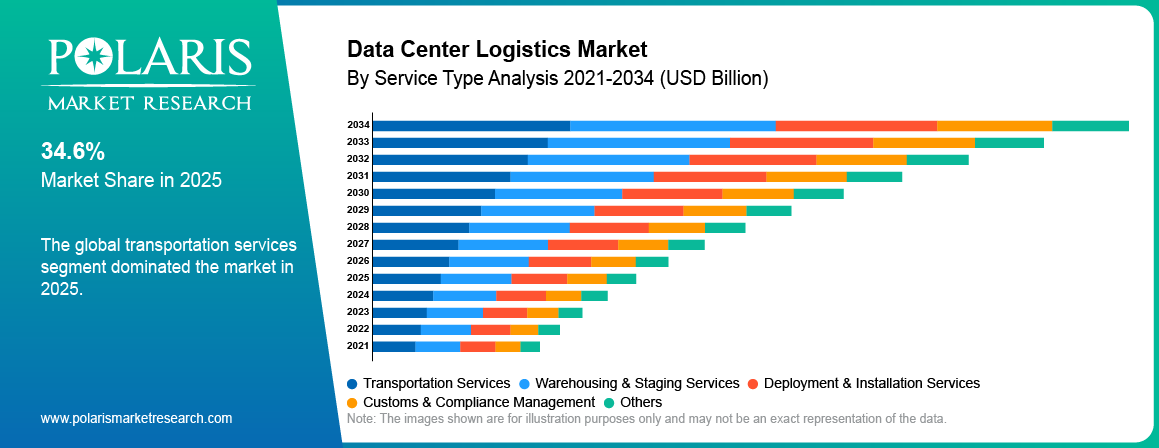

- Transportation services dominated the market in 2025 with 34.6% share, due to rising demand for server transportation services and precision IT equipment shipping.

- Hyperscale data centers dominated the market in 2025 with 42.8% share, driven by rapid cloud infrastructure expansion and AI-ready facility deployment.

- Warehousing & staging services segment is projected to grow at the fastest CAGR of 9.7% during the forecast period, owing to increasing deployment staging requirements for AI infrastructure logistics.

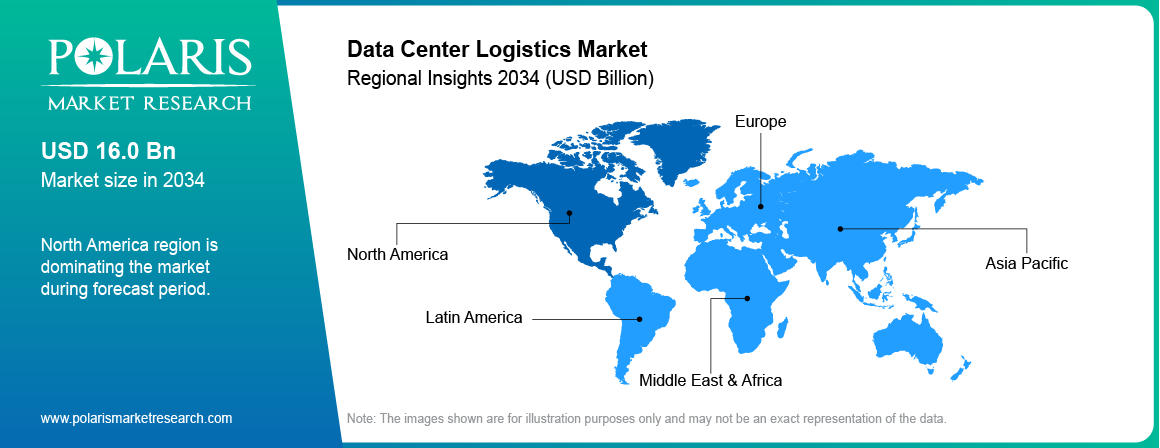

- North America dominated the market by 41.7% revenue share in 2025 driven by strong hyperscale expansion and rising investments in AI infrastructure deployment.

- Asia Pacific data center logistics market is projected to grow at the fastest CAGR of 9.7% during the forecast period due to increasing internet penetration.

Industry Dynamics

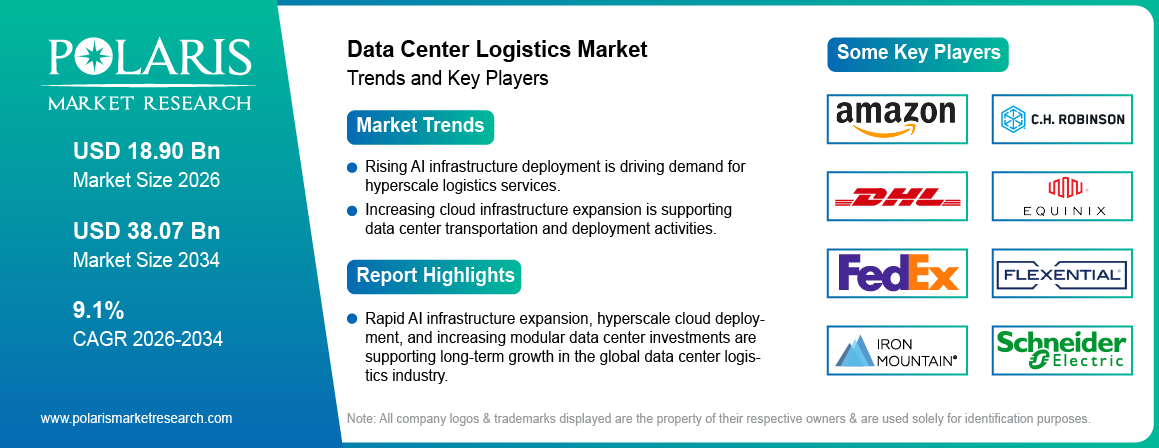

- Rising AI infrastructure deployment is driving data center logistics market growth.

- Increasing hyperscale data center expansion is supporting demand for IT equipment transportation services.

- Semiconductor supply chain disruptions are restraining market expansion.

- Growing modular and prefabricated data center deployment is creating market opportunities.

What is the Data Center Logistics Market?

Data center logistics involves transportation, warehousing, deployment coordination, customs management, and infrastructure supply chain services supporting hyperscale, colocation, and edge computing facilities. These services are widely used for server transportation, rack deployment, cooling infrastructure movement, and mission-critical equipment handling across digital infrastructure projects.

The data center logistics market functions using a value chain consisting of hardware vendors, semiconductor vendors, logistics companies, warehouse operators, deployment firms, cloud service providers, and end-users. The logistics firms coordinate infrastructure movement, staging processes, equipment testing, customs processes, and on-site deployment services for major data centers.

Source: Polaris Market Research Analysis

To Understand More About this Research: Download Sample Report

This market is growing due to increasing utilization of artificial intelligence and cloud computing technology and the growth in deployment activities related to hyperscale infrastructure. Demand for edge computing, modular data centers, and investments in liquid cooling infrastructure is expected to help increase logistics services demand.

Drivers & Opportunities

Rising AI Infrastructure Deployment is Driving Market Growth: The rapid adoption of generative AI, machine learning, and supercomputing technology has led to an increase in demand for AI infrastructure logistics services around the world. There has been increased spending by hyperscalers on GPU servers, high-density server racks, and enhanced cooling equipment that require specialized handling and coordination during transportation and installation. According to statistics published by Microsoft Corporation, generative AI utilization rose to above 30% from almost 26% of the total population, registering a remarkable 80% growth in October 2024.[Microsoft, "Global AI Adoption 2025 Report", microsoft.com]

Increasing Hyperscale Data Center Expansion is Supporting Market Demand: The rising trend of the construction of hyperscale cloud data centers is making it essential to have transportation services that helps to transport data centers from one place to another. Companies constructing large-scale clouds are increasingly dedicating more efforts towards developing hyperscale clouds, which involve the transportation of racks, servers, cooling systems, and power systems. For example, Microsoft Corporation has invested USD 1.7 billion in India in December 2025 for promoting Artificial Intelligence and Digital Transformation.[Microsoft News, "Microsoft Invests US$17.5 Billion in India to Drive AI Diffusion at Population Scale", news.microsoft.com]

Restraints & Challenges

Semiconductor Supply Chain Disruptions are Limiting Market Expansion: With semiconductor shortage issues and disruption in supply chains, there are delays in infrastructure implementation timelines throughout various data center projects. Logistics companies have encountered some logistical hurdles with respect to customs delays, freight fluctuations, and GPU procurement cycles. Higher logistics expenses and political trade barriers are creating more complexities with mission-critical infrastructure implementation processes.

Opportunity

Growing Modular Data Center Deployment is Creating Market Opportunities: With the increasing trend towards modular data centers, there is an opportunity for the growth of logistics companies offering integrated solutions. The construction of such facilities involves coordinated transportation, cranes, staging, and other specialized logistics operations. Rising edge computing deployment and rapid infrastructure scalability requirements are supporting demand for modular data center logistics and deployment coordination services.

Source: Polaris Market Research Analysis

To Understand More About this Research: Download Sample Report

Segmental Insights

The report provides a comprehensive analysis of the Data Center Logistics Market by service type, infrastructure type, end use, and deployment model to identify key revenue generating and high-growth segments.

By Service Type

-

Transportation Services

Transportation services dominated the market in 2025 with 34.6% share, driven by increasing movement of servers, GPU clusters, racks, and cooling systems across hyperscale infrastructure projects. The increasing trend towards AI-ready data centers and the growing requirement for precision transport of IT infrastructure is expected to drive segment growth. Logistics providers are increasingly providing real-time tracking and shock-resistant delivery solutions for mission-critical infrastructure deployment.

-

Warehousing & Staging Services

Warehousing & staging services segment is projected to grow at the fastest CAGR of 9.7% during the forecast period, owing to rising demand for integrated deployment staging environments. Hyperscale providers are turning to warehouses that are equipped with capabilities for rack assembly, equipment testing, management of inventory, and deployment coordination prior to installation on-site. Increasing automation within infrastructure deployment is driving segment growth.

By Infrastructure Type

-

Hyperscale Data Centers

Hyperscale data centers dominated the market in 2025 with 42.8% share due to heavy investment in cloud infrastructure by leading technology companies. These data centers demand very well-coordinated logistics ecosystems that facilitate quick deployment of servers and cooling solutions. Increasing investments in hyperscale cloud campuses across North America and Asia Pacific are strengthening segment demand.

-

Edge Data Centers

Edge data centers are projected to grow at the fastest CAGR during the forecast period driven by increasing deployment of low-latency computing infrastructure. Rising adoption of IoT devices, 5G connectivity, and distributed cloud applications is increasing demand for edge computing deployment logistics services. According to IoT Analytics, the number of connected IoT devices increased by 12% year-over-year to reach 18.5 billion units in 2024. The installed base is expected to grow by 14% in 2025 and reach around 39 billion connected devices by 2030, which will exceed 50 billion by 2035.[IoT Analytics, "State of IoT Summer 2025: 19.5 Billion Connected IoT Devices", iot-analytics.com]

By Deployment Model

-

New Infrastructure Deployment

New infrastructure deployment led the market in 2025, owing largely to growing construction in the area of hyperscale and AI-enabled facilities in global markets. Growing investment in cloud build-out, modular facilities, and edge computing infrastructure have increased demands for transportation and logistics services.

-

Upgrade & Expansion Deployment

Upgrade & expansion deployment is expected to exhibit the highest CAGR through the forecast period due to the high retrofitting activity for AI and liquid cooling. Upgrades are taking place in data centers in order to support new advanced workloads, including those involving artificial intelligence.

By End Use

-

Cloud Service Providers

Cloud service providers held the dominant position in the global market for AI deployment in 2025 due to the growth of hyperscale infrastructure and AI computing capabilities. Companies are increasingly investing in high-capacity data center campuses requiring advanced infrastructure transportation and deployment coordination services. Rising enterprise cloud adoption and digital transformation activities are supporting segment growth.

-

Colocation Providers

Colocation providers are projected to grow at the fastest CAGR during the forecast period owing to increasing enterprise demand for third-party data center infrastructure services. Expansion of multi-tenant data centers and rising investments in regional colocation facilities are increasing demand for integrated logistics and deployment management solutions.

Source: Polaris Market Research Analysis

To Understand More About this Research: Request Customization

Regional Analysis

North America Data Center Logistics Market Overview

North America dominated the market by 41.7% revenue share in 2025 driven by strong hyperscale investments and rapid AI infrastructure deployment across the US and Canada. Major cloud providers are expanding large-scale AI-ready campuses requiring specialized transportation, staging, and infrastructure deployment services. In March 2026, Digital Realty secured USD 3.25 billion in equity commitments for its inaugural US hyperscale data center fund focused on Tier I markets including Northern Virginia, Dallas, and Santa Clara, supporting rising regional demand for hyperscale infrastructure logistics services.

Asia Pacific Data Center Logistics Market Insights

Asia Pacific data center logistics market is projected to grow at the fastest CAGR of 9.7% during the forecast period due to rising cloud adoption, increasing internet penetration, and expansion of digital infrastructure investments across China, India, Singapore, Indonesia, and Malaysia. Governments and hyperscale operators are investing heavily in sovereign cloud ecosystems and AI infrastructure projects across the region. According to the International Trade Administration, India has more than 650 million smartphone users and over 950 million internet subscribers as of April 2026.[International Trade Administration, U.S. Department of Commerce, "India Digital Economy", trade.gov] This is supporting rapid expansion of cloud infrastructure and regional data center deployment activities.

Europe Data Center Logistics Market Assessment

Europe data center logistics market is witnessing stable growth of 8.7% due to increasing colocation expansion and rising investments in sustainable digital infrastructure across Germany, the UK, France, and the Netherlands. The logistics companies are increasingly engaging in emission-free transportation services and energy-saving deployment practices to adhere to regional sustainability laws. According to the Europe Data Centre Association, colocation data centers contributed nearly USD 59.9 Billion to Europe’s GDP in 2025 while supporting regional energy, climate, and digital infrastructure targets.[European Data Centre Association, "2026 State of European Data Centres", eudca.org]

Source: Polaris Market Research Analysis

To Understand More About this Research: Request Customization

Competitive Landscape

Key Players & Competitive Strategies

The market is moderately fragmented due to the presence of global freight companies, specialized IT logistics providers, and regional infrastructure deployment firms. Competition is based on deployment speed, infrastructure coordination capabilities, pricing, real-time visibility, and secure transportation services. Companies are concentrating on warehouse automation, AI-powered monitoring, collaborative business models, and regional growth strategies to enhance their market share in hyperscale infrastructures.

Major companies operating in the data center logistics market include Amazon.com Inc., C.H. Robinson Worldwide, Inc., DHL Supply Chain & Global Forwarding, Equinix, Inc., Federal Express Corporation, Flexential, Iron Mountain Inc., Kuehne + Nagel International AG, Logistics Plus Inc., MG Moving Services, Nielsen Logistics, Inc., Schneider Electric, UPS Supply Chain Solutions, United Parcel Service of America, Inc., and Winning Solutions Inc.

Premium Insights

The next phase of growth in the data center logistics market is expected to be driven by rapid AI infrastructure expansion, rising deployment of liquid cooling systems, increasing adoption of modular data centers, and ongoing diversification of global supply chains. Demand for faster delivery timelines and high-value equipment handling is strengthening the importance of specialized logistics capabilities across hyperscale and colocation facilities.

Companies that use predictive logistics analytics, automation in their warehouses, and deployment lifecycle management is expected to have a competitive edge. With real-time inventory visibility and automated logistics processes, the potential of downtimes can be avoided, resulting in efficient deployment.

Infrastructure logistics for AI has become a strategic aspect rather than merely an operational one. The logistics companies are increasingly taking on an important responsibility for deployment time, infrastructure reliability, and cloud expansion economics.

Key Players

- Amazon.com Inc.

- C.H. Robinson Worldwide, Inc.

- DHL Supply Chain & Global Forwarding

- Equinix, Inc.

- Federal Express Corporation

- Flexential

- Iron Mountain Inc.

- Kuehne + Nagel International AG

- Logistics Plus Inc.

- MG Moving Services

- Nielsen Logistics, Inc.

- Schneider Electric

- UPS Supply Chain Solutions

- United Parcel Service of America, Inc.

- Winning Solutions Inc.

Industry Developments

- March 2026: DHL Group has expanded its logistics network throughout North America to cater to growing demands from growth industries such as data centers, semiconductors, health care, and e-commerce. [source: group.dhl.com]

- June 2025: Schneider Electric introduced new data center technologies that are ideal for high-density AI and accelerated computing. The portfolio includes advanced power distribution, cooling, and infrastructure management technologies designed to address increasing rack densities, energy consumption, and operational complexity in next-generation AI data centers. [source: se.com]

Data Center Logistics Market Segmentation

By Service Type Outlook (Revenue, USD Billion, 2021–2034)

- Transportation Services

- Warehousing & Staging Services

- Deployment & Installation Services

- Customs & Compliance Management

- Others

By Infrastructure Type Outlook (Revenue, USD Billion, 2021–2034)

- Hyperscale Data Centers

- Colocation Data Centers

- Edge Data Centers

- Modular & Prefabricated Data Centers

By Deployment Model Outlook (Revenue, USD Billion, 2021–2034)

- New Infrastructure Deployment

- Upgrade & Expansion Deployment

By End Use Outlook (Revenue, USD Billion, 2021–2034)

- Cloud Service Providers

- Colocation Providers

- Enterprises

- Others

By Regional Outlook (Revenue, USD Billion, 2021-2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Data Center Logistics Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 17.38 Billion |

| Market Size in 2026 | USD 18.90 Billion |

| Revenue Forecast by 2034 | USD 38.07 Billion |

| CAGR | 9.1% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

FAQ's

The global market size was valued at USD 17.38 Billion in 2025 and is projected to reach USD 38.07 Billion by 2034 at a CAGR of 9.1%.

North America dominated the market by 41.7% revenue share in 2025 due to extensive investment in hyperscale infrastructure and fast-growing AI-enabled cloud facilities.

Major companies operating in the market include DHL Group, FedEx Corporation, Kuehne+Nagel, United Parcel Service, and DB Schenker.

Major growth drivers include increasing AI infrastructure deployment, rapid hyperscale data center expansion, rising cloud computing investments, and growing edge computing deployment activities.

Transportation services dominated the market in 2025 with 34.6% share due to the rise in server transportations, GPU cluster transfers, and hyperscale infrastructure installations.

Edge data centers are projected to grow at the fastest CAGR of 9.7% during the forecast period due to rising low-latency computing demand and distributed infrastructure expansion.

The market outlook remains positive due to increasing AI-driven infrastructure deployment, rising modular data center expansion, and growing investments in advanced logistics automation technologies.

Download Sample Report of Data Center Logistics Market

Please fill out the form to request a customized copy of the research report.