High Throughput Screening Market Demand & Industry Report, 2026-2034

REPORT DETAILS

High Throughput Screening Market Summary

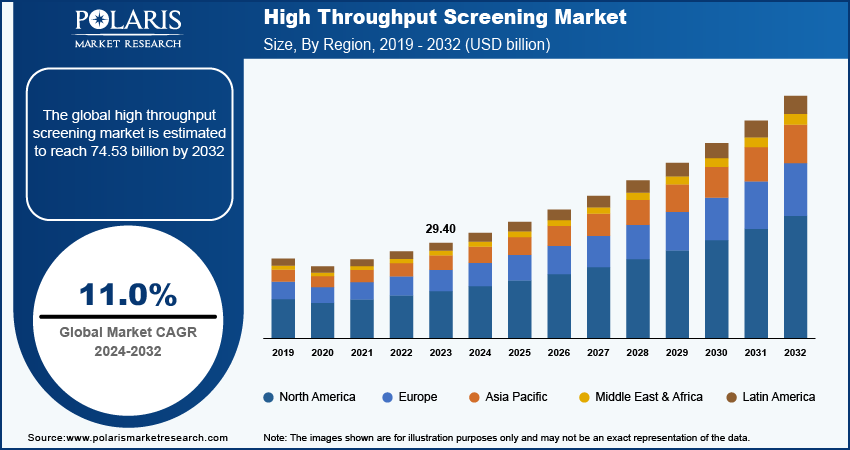

The high throughput screening market was valued at USD 35.79 billion in 2025. It is projected to grow at a CAGR of 11.3% during 2026–2034. The widespread use of high throughput screening (HTS) in drug discovery and research to test genes, chemicals, and antibodies is one of the key HTS market growth drivers.

Market Statistics

Key Takeaways

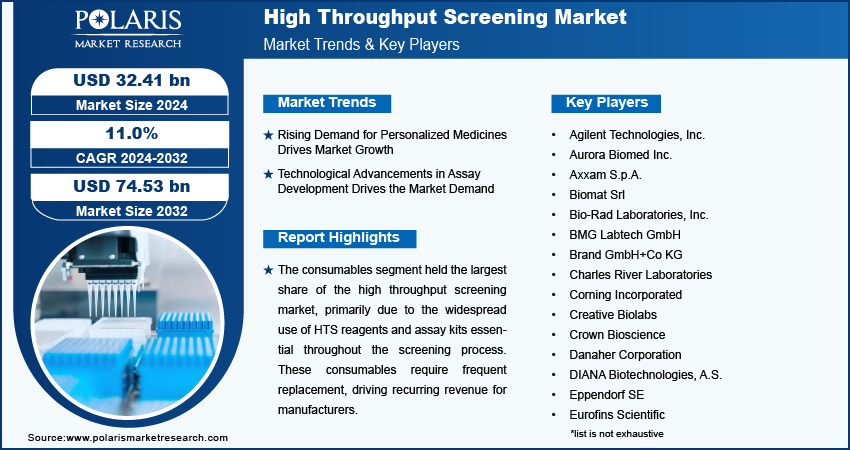

- The consumables segment dominated the high throughput screening market in 2025, owing to the widespread use of HTS reagents and assay kits, which are essential throughout the screening process.

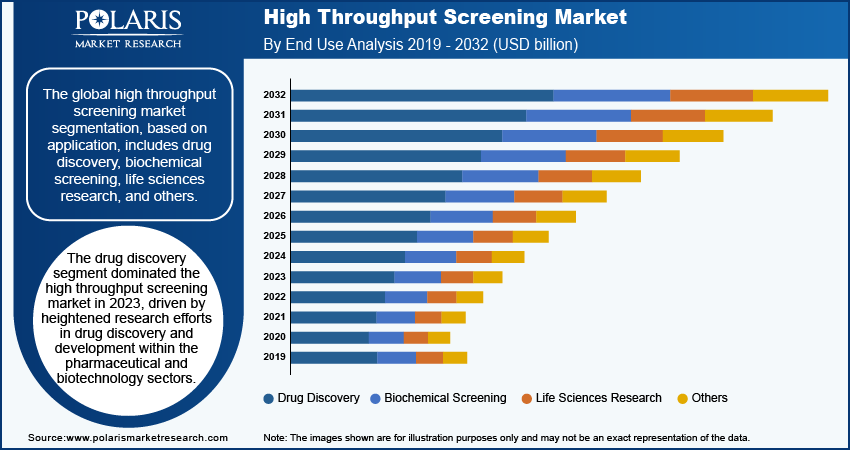

- The drug discovery high throughput screening segment accounted for the largest market share in 2025. The segment’s dominance is primarily attributed to increased research efforts in drug discovery and development within the biotechnology and pharmaceutical sectors.

- The HTS market in 2025 was led by North America, mainly because of the major increase in R&D investments by pharmaceutical and biotech companies for the development of biomarkers and drugs.

- The Asia Pacific high throughput screening market is expected to grow at the highest rate because of the diverse patient population in the region accepting a wide variety of drugs.

From an industry perspective, the market for high throughput screening is growing at a fast pace due to increased R&D investments in the pharmaceutical industry, the growing need for targeted therapies, and the adoption of automated laboratory workflows. HTS enables the identification of active compounds faster, which reduces the time and cost involved in early-stage drug development.

Industry Insights

- The increasing demand for screening technologies in personalized medicine is fueling the demand for high throughput screening. HTS helps in the rapid detection of biomarkers associated with the disease and treatment processes.

- HTS helps in large-scale phenotypic and biomarker-based screening, which enables more accurate drug development strategies that can be matched to individual patient profiles. This is a feature that is becoming increasingly important in the fields of oncology, rare diseases, and immunotherapy.

- Technological advancements in assay development, including the miniaturization of assays, are fueling market expansion.

- The rising demand for HTS consumables is expected to create several market opportunities in the coming years.

- Data management and analysis challenges may hinder high throughput screening market growth.

AI Impact on High Throughput Screening Market

- Artificial intelligence is transforming the high throughput screening market by the way in which large amounts of biological data are being analyzed and interpreted. AI tools help in the rapid screening of compounds by analyzing complex data quickly. That way, researchers can identify promising drug candidates faster.

- Machine learning in drug discovery screening enhances the accuracy of screening by reducing the number of false positives and false negatives, making the subsequent validation process more efficient. The use of AI, robotics, and cloud technology in automated HTS systems also enables pharmaceutical companies to expand their screening processes while maintaining consistent and reliable data.

- As the data required in drug discovery pipelines increases, the integration of AI in high throughout screening is becoming a major differentiating factor, which is helping the team make quicker go/no-go decisions and reduce overall R&D risk.

- AI integration with robotics and cloud technology allows for the process of screening on a large scale and at lower costs. This promotes innovation and helps pharmaceutical companies launch new therapies in the market.

Source: Polaris Market Research Analysis

The high throughput screening market is developing at a rapid pace, mainly due to the rise in the incidence of chronic diseases. There has been a rise in the number of drug discovery service initiatives, stimulated by the continuous need for effective treatments. HTS is a technique that finds broad application in drug discovery. It is employed to speedily evaluate millions of chemicals, genes, or pharmacological agents. The prime objective is to detect the active compounds, antibodies, or genes that influence particular biomolecular pathways. High throughput screening employs automated machines or software that assist significantly in analyzing huge quantities of samples. According to the WHO, non-communicable diseases (NCDs) result in the death of 41 million people each year, with 17 million early deaths occurring primarily in low- and middle-income nations. Here, cardiovascular diseases account for 17.9 million deaths, cancer causes 9.3 million deaths, chronic obstructive pulmonary disease results in 4.1 million deaths, and diabetes causes 2 million deaths. This increases the demand for high throughput screening tests.

HTS has become a technology in the healthcare industry that has revolutionized the rate of discovery of potential drug candidates. By automating the evaluation of large amounts of chemical compounds against target diseases, it has greatly accelerated the early stages of drug discovery. This technology has become critical in the development, treatment, and management of many diseases, especially those that would require traditional methods that are labor-intensive. For example, HTS has helped researchers identify potential drug candidates by speeding up the evaluation process, allowing thousands or even millions of compound evaluations. Therefore, this faster evaluation process has helped researchers discover potential lead compounds that contain pharmacological properties. Moreover, this technology increases the likelihood of discovering such potential compound properties. For this reason, many pharmaceutical companies and institutions are using HTS to enhance their pipelines with potential drug candidates. For example, Bruker's Sierra introduced its SPR-32 Pro platform in February 2022. The platform enables high-throughput multiplexed assays for precise insights into molecular interactions in drug discovery.

Continuing developments in robotics, automation, and software technology have also impacted HTS platforms, improving their efficiency and capabilities. For instance, these technologies automate processes such as sample handling, compound screening, and data analysis, thereby optimizing screening workflows and speeding up the assessment of vast compound sets. Additionally, developments in software technology have improved the interfacing between HTS data and analysis tools. This, in turn, has accelerated the drug discovery and development process.

Market Dynamics

Rising Demand for Personalized Medicines

The high throughput screening market is driven by the shift to personalized medicine. It represents a revolutionary concept in healthcare, providing tailored medicine to each patient according to their unique genetic base, environmental characteristics, and lifestyle. HTS plays an instrumental role in the revolution in health care by helping to identify the personalized medicine biomarkers related to disease and treatment responses.

Through HTS, various genetic analyses, proteins, and other molecular targets are filtered in large numbers to ensure accurate information for each patient's profile. This not only enables better comprehension and analysis of disease at the molecular level, but can also be used to develop targeted therapy approaches and personalize medications through overall process analysis. For example, in February 2024, SCIEX announced that its Echo MS system can enhance HTS in drug discovery, enabling personalized medicine therapy on an accurate qualitative and quantitative basis. Similarly, HTS can be used to validate biomarkers related to disease because of its ability to serve as a diagnostic and predictive tool. Healthcare providers can make effective decisions about personalized care strategies using HTS data analysis and thereby improve overall healthcare efficiency.

Increasing Advancements in Assay Development

Significant advances in assay development technology have revolutionized high-throughput screening (HTS), which has become the cornerstone of the pharmaceutical, biotechnology, and academic sciences. High throughput screening involves miniaturizing existing assays, enabling researchers to conduct screenings at much lower cost. In this way, the process has become much more streamlined for testing compound libraries against specific disease targets. In addition, the ability to use multiple molecular targets within a single assay is enabled by multiplexing technologies. This is vital for understanding biological processes and identifying potential therapeutic candidates.

High content screening (HCS) is the next level of advancement and encompasses all the features of HTS with the capabilities of imaging and data analysis. HCS allows scientists to evaluate cellular morphology, protein expression, and other complex phenotypic traits in large-scale assays. These technologies are the forerunners of advancing HTS capabilities and help scientists tackle various challenges in the biomedical field, developing treatments for a variety of diseases and providing personalized medicine.

Source: Polaris Market Research Analysis

Segment Insights

Assessment by Offering

The high throughput screening market by offering includes consumables, instruments, services, and software. The consumables segment accounted for the largest share in 2025, mainly attributed to the usage of HTS reagents and kits, which are required throughout the screening process. Consumables also need to be replaced regularly, thereby generating steady revenue for companies.

The growing demand for HTS consumables is also contributing to the growth opportunities in the market. The factors that are driving this demand include the growing pharmaceutical R&D and government funding for life sciences research and drug discovery. For instance, in July 2022, the Council of Scientific and Industrial Research (CSIR) in India invested USD 6.73 million in research and development (R&D) for drug discovery and development.

Evaluation by Application

The global high throughput screening market segmentation, based on application, includes drug discovery, biochemical screening, life sciences research, and others. The drug discovery segment represented the largest market share in 2025. This is because there has been an increase in research activities in drug discovery and development. The combination of HTS with genomics, proteomics, and computational biology makes HTS more efficient in target discovery and validation. In addition, the increasing support from government bodies and research institutions to facilitate drug discovery has also contributed to the growth of this market segment.

Source: Polaris Market Research Analysis

Regional Insights

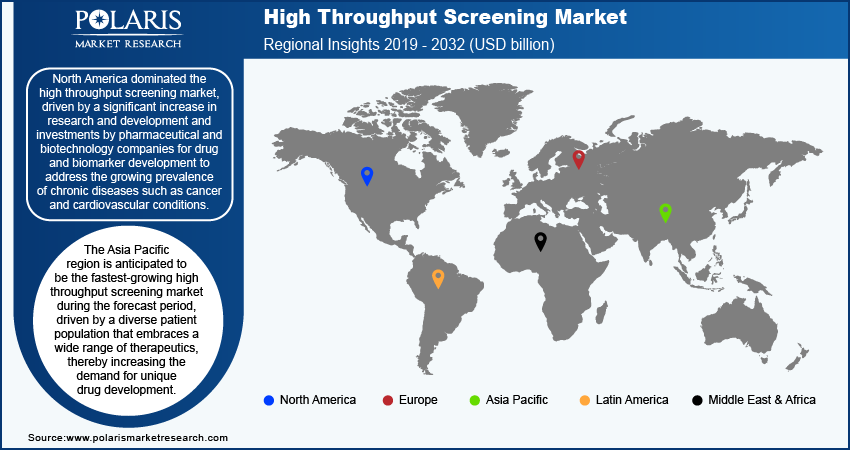

By region, the report provides the high throughput screening market insights into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. North America accounted for the highest revenue share in the high throughput screening market in 2025, driven by a substantial rise in research and development expenditures by pharmaceutical and biotech companies to develop drugs and biomarkers to address the growing number of patients with chronic diseases such as cancer and cardiovascular diseases. According to the International Agency for Research on Cancer, in 2022, there were 20 million new cases of cancer and 9.7 million cancer deaths worldwide, with estimates for 2040 to reach 29.9 million new cases and 15.3 million deaths. The increasing number of cancer patients in North America is thus fueling the growth opportunities. In addition, the high healthcare expenditure in North America supports the usage of advanced screening technologies.

The Asia Pacific high throughput screening market is expected to register the fastest growth rate during the forecast period, owing to a diverse patient base adopting a broad spectrum of treatments and digital therapeutics, thereby fueling demand for novel drug development. In addition, the market is fueled by the rapid expansion of the pharmaceutical and biotech sectors, investments, cost competitiveness, government support, and the rising burden of diseases. As per the Government of India initiatives projections, in January 2024, the Pharma-MedTech industry in India is working towards improving its position in the global arena through its strong R&D and innovation efforts, with the aim of growing the pharmaceutical industry from USD 50 billion to USD 120-130 billion and the medical technology industry from USD 11 billion to USD 50 billion by 2030. In addition, improvements in HTS technology are increasing the efficiency of drug discovery. All of these factors have made Asia Pacific a key region for pharmaceutical innovation.

Source: Polaris Market Research Analysis

Key Players and Competitive Analysis Report

The high throughput screening competitive landscape is undergoing evolution, mainly fueled by technological innovation in automation, miniaturization, and artificial intelligence integration. Analysis of the industry shows that major players, such as Thermo Fisher Scientific, Danaher Corporation, and Agilent Technologies, have established themselves in the market through comprehensive product offerings. The product offerings include reagents, equipment, and software solutions. The high throughput screening market leaders are now focusing on developing the partner & customer ecosystem to sustain their competitive edge. The industry is experiencing significant disruptions and trends in assay formats. Phenotypic screening is emerging as a new approach alongside conventional target-based screening. Small and medium-scale enterprises are creating their own unique niches by offering innovative assay development services and artificial intelligence-based data analysis solutions. Partnerships between instrument companies and reagent vendors are redefining value chains, especially in pharmaceutical discovery.

Opportunities are emerging in the applications of precision medicine. In precision medicine, the capability of HTS in high-content analysis allows complex drug development. Future approaches to development are centered on integrated workflows, reduced sample sizes, and enhanced data analysis tools. Digitalization of the drug development process is expanding the total addressable market, but the regulatory framework for clinical validation is a strategic challenge. A few key high throughput screening market players are Agilent Technologies, Inc., Aurora Biomed Inc., Axxam S.p.A., Biomat Srl, Bio-Rad Laboratories, Inc., BMG Labtech GmbH, Brand GmbH+Co KG, Charles River Laboratories, Corning Incorporated, Creative Biolabs, Crown Bioscience, Danaher Corporation, DIANA Biotechnologies, A.S., Eppendorf SE, Eurofins Scientific, Gilson Incorporated, Greiner AG, Hamilton Company, HighRes Biosolutions, Lonza, Merck KGaA, Mettler-Toledo International Inc., Porvair Plc, Revvity, Inc., Sartorius AG, Sygnature Discovery Limited, Tecan Group Ltd., Thermo Fisher Scientific Inc., Waters Corporation.

Agilent Technologies, Inc. operates in the life sciences, diagnostics, and applied markets. With its headquarters in Santa Clara, California, the company serves over 110 countries. Established in 1999 as a spin-off of Hewlett-Packard, Agilent Technologies has established a strong reputation for providing innovative instruments, software, consumables, and services that facilitate research, diagnostics, and quality assurance in the pharmaceutical, biotech, and environmental science sectors. In the HTS industry, Agilent Technologies is recognized as an innovator with highly customizable and flexible solutions that optimize complex screening processes in drug discovery, genomics, and functional biology. Agilent's HTS systems, including the BioCel System, integrate automation, liquid handling, and environmental control to accommodate a wide range of assay formats and protocols, ensuring high accuracy and speed in compound screening and analysis. Agilent’s systems provide seamless sample preparation, data acquisition, and analysis. In this regard, scientists can easily analyze large libraries of compounds or genetic material. Strategic investments in R&D and technology collaborations have enabled Agilent to continue to improve its HTS product lines. Agilent is a trusted partner for laboratories seeking to accelerate scientific discovery and innovation in a high-throughput environment.

Thermo Fisher Scientific Inc., based in Waltham, Massachusetts, is a science-solutions provider. Established in 2006 through the merger of Thermo Electron and Fisher Scientific, the company offers a broad range of analytical instruments, laboratory equipment, specialty diagnostics, and life sciences solutions for pharmaceutical, biotechnology, clinical diagnostics, and research markets. In the area of HTS, Thermo Fisher Scientific supplies automation platforms, detection systems, and assay solutions that are aimed at speeding up drug discovery and biological research. Their HTS solutions allow researchers to quickly screen large libraries of compounds or biological materials, facilitating the identification of potential drug leads and biomarkers. The HTS offering from Thermo Fisher Scientific integrates precision robotics, liquid handling, high-content imaging, and data analysis software. This allows for scalability and reproducibility across different assay types. The company’s emphasis on innovation makes it a dependable partner for laboratories seeking to improve productivity and facilitate scientific discovery in high-throughput settings. Thermo Fisher Scientific is also the parent company of famous brands such as Thermo Scientific, Applied Biosystems, and Invitrogen.

List of Key Companies

- Agilent Technologies, Inc.

- Aurora Biomed Inc.

- Axxam S.p.A.

- Biomat Srl

- Bio-Rad Laboratories, Inc.

- BMG Labtech GmbH

- Brand GmbH+Co KG

- Charles River Laboratories

- Corning Incorporated

- Creative Biolabs

- Crown Bioscience

- Danaher Corporation

- DIANA Biotechnologies, A.S.

- Eppendorf SE

- Eurofins Scientific

- Gilson Incorporated

- Greiner AG

- Hamilton Company

- HighRes Biosolutions

- Lonza

- Merck KGaA

- Mettler-Toledo International Inc.

- Porvair Plc

- Revvity, Inc.

- Sartorius AG

- Sygnature Discovery Limited

- Tecan Group Ltd.

- Thermo Fisher Scientific Inc.

- Waters Corporation

High Throughput Screening Industry Development

September 2025: Axxam announced a strategic collaboration with B’SYS. According to Axxam, the collaboration aims to provide access to tested ion channel cell lines for identifying potential drug candidates using high-throughput electrophysiology.

April 2025: CytoTronics launched its Neural application for Pixel systems, enabling high-throughput drug screening for neurological diseases. The platform combines electrical imaging and electrophysiology in multiplexed assays. It supports 2D/3D cultures and scaling to 384-well plates for large-scale HTS workflows.

March 2025: HORIBA launched the PoliSpectra Rapid Raman Plate Reader (RPR) for high-throughput screening. The RPR enables non-destructive, real-time analysis of 96 wells in just 1 minute. The automated platform is compatible with liquid handlers. It allows real-time process monitoring using patented rapid Raman technology.

May 2024: Twist Bioscience launched Twist Multiplexed Gene Fragments (MGFs). The new fragments enable high-throughput screening with pools of directly synthesized DNA fragments up to 500 base pairs in length.

High Throughput Screening Market Segmentation

By Offering Outlook (Revenue, USD Billion, 2021–2034)

- Consumables

- Reagents & Assay Kits

- Laboratory Consumables

- Instruments

- Liquid Handling Systems

- Detection Systems

- Imaging Systems

- Others

- Services

- Software

By Technology Outlook (Revenue, USD Billion, 2021–2034)

- Cell-based Assays

- 2D Cell Culture

- 3D Cell Culture

- Scaffold-based Technology

- Scaffold-free Technology

- Reporter-based Assays

- Perfusion Cell Culture

- Lab-on-a-Chip Technology (LOC)

- Label-free Technology

By Application Outlook (Revenue, USD Billion, 2021–2034)

- Drug Discovery

- Biochemical Screening

- Life Sciences Research

- Others

By End User Outlook (Revenue, USD Billion, 2021–2034)

- Pharmaceutical & Biotechnology Companies

- Academic & Research Institutes

- Contract Research Organizations (CROs)

- Others

By Regional Outlook (Revenue, USD Billion, 2021–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

High Throughput Screening Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 35.79 billion |

| Market Size in 2026 | USD 39.57 billion |

| Revenue Forecast by 2034 | USD 93.11 billion |

| CAGR | 11.3% |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD billion, and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape | High Throughput Screening Industry Trend Analysis (2025) Company profiles/industry participants profiling include company overview, financial information, product/service benchmarking, and recent developments |

| Report Format | PDF + Excel |

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

FAQ's

The high throughput screening market size is projected to reach USD 93.11 billion by 2034. It is anticipated to account for a CAGR of 11.3% between 2026 and 2034.

HTS screening is primarily used in drug discovery and biochemical screening. It also finds applications in life sciences research, compound testing, and biomarker identification.

The consumables segment accounted for the largest share in 2025. This is due to the usage of HTS reagents and kits, which are required throughout the screening process.

AI accelerates compound screening. The technology is capable of analyzing vast datasets rapidly and identifying molecular interactions with precision.

North America leads the market for high throughput screening. This is due to growing R&D investments by pharmaceutical and biotech companies.

The drug discovery segment dominated the market in 2024.

Download Sample Report of high throughput screening market

Please fill out the form to request a customized copy of the research report.