Jewelry Market Opportunity, Growth & Trends Report, 2026-2034

REPORT DETAILS

REPORT DETAILS

What is the Jewelry Market Size?

The global jewelry market was valued at USD 286.15 billion in 2025, growing at a CAGR of 8.7% from 2026 to 2034. Strategic collaborations and acquisitions among major players and a growing trend for cross-cultural ornaments are driving the industry growth. Also, the market growth is attributed to jewelry e-commerce growth.

Market Statistics

Key Takeaways

- Asia Pacific dominated the market in 2025, by holding 58.50% revenue share. It is driven by strong cultural affinity toward precious metals and growing middle-class spending.

- The North America jewelry industry is expected to register a CAGR of 8.4% during 2026–2034. Increasing consumer interest in luxury goods and accessories and personalized adornments will boost the regional market growth.

- The ring segment accounted for 32.03% of the revenue share in 2025. Strong demand for engagement and wedding rings boost the segment dominance.

- The gold segment held the largest revenue share of 60.40% in 2025. The leading share is attributed to the material’s strong cultural value and high investment appeal.

- The offline segment accounted for 65.30% of the revenue share in 2025. Consumer preference for physical inspection contributes to the leading position. However, increasing availability of 5G networks and rising penetration of e-commerce platforms will fuel online jewelry penetration rate in rural areas.

- The rising acceptance of gender-fluid fashion and increasing disposable income will drive the men’s jewelry market growth.

Industry Dynamics

- Higher disposable income across emerging and developed economies drives the jewelry industry growth.

- There is a rising demand for ethically sourced, eco-friendly jewelry, which boosts the sales of lab-grown diamonds.

- The rising focus on recycled metals and transparent supply chains contributes to sustainable jewelry trends.

- The increasing adoption of 3D printing in jewelry manufacturing will create lucrative opportunities in the coming years.

- The emerging market future trends are personalized jewelry demand and lab-grown diamond adoption.

- There is a surging preference for name-engraved, birthstone, and custom-designed pieces. Thus, brands invest in digital design tools and tailored customer experiences. Due to this, the personalized jewelry market is expected to witness rapid growth in the coming years.

- Volatility in gold and silver prices, along with geopolitical tensions that affect raw material sourcing and logistics, pose cost and availability challenges.

AI Impact on Jewelry Industry

- Jewelry manufacturers, wholesalers, and retailers use artificial intelligence (AI) technology to enhance predictive demand forecasting and inventory planning.

- Machine-vision–based gemstone grading and authentication help reduce manual errors and enhance quality assurance.

- Retailers use AR/VR jewelry try-on tools to boost conversions. The tools enable brands to offer scalable virtual product catalogs to partners.

- AI-based sensors and analytics help in smart jewelry development. AI-driven jewelry design will create opportunities for OEM/ODM collaboration.

- Distributors use AI-powered personalization engines. It helps them tailor assortments for different retail channels.

- AI technology can be integrated in various jewelry supply-chain processes. The technology is used in sourcing, manufacturing, and logistics. It helps enhance traceability, compliance, and real-time visibility across.

To Understand More About this Research: Download Sample Report

Market Overview

The jewelry industry focuses on the design, production, and sale of ornaments. The jewelry items are made of precious metals, gemstones, and other materials. Fine jewelry, costume jewelry, and custom pieces are among the categories. Jewelry is purchased for personal, cultural, and investment purposes. The growing trend of cross-cultural ornaments is driving market expansion. Increased advertising budgets and new international campaigns will enable the distribution of a various products across the world.

Cultural significance and tradition drive strong jewelry sales. There are rising investments in premium items such as bridal jewelry and heirloom-quality pieces. Digital platforms expand access to global brands and personalized jewelry. Social media influencers and celebrities influence consumer choices. Also, high-impact campaigns on platforms such as Instagram, YouTube, and TikTok promote new collections and seasonal trends. The demand for personalized, design-driven pieces increasing. It prompts market players to adopt on-demand production and CAD-based customization. Also, market players emphasize flexible supply chains for on-time product delivery. Thus, the custom jewelry market is witnessing rapid growth.

Types of Jewelry

| Jewelry Type | Description | Major Components | Common Usage |

| Fine Jewelry | Jewelry made of expensive material that lasts long | Gold, platinum, diamonds | Wedding purposes |

| Fashion Jewelry | Jewelry designs based on trends and low price | Various metals, artificial gems | For everyday wear and fashion |

| Jewelry designs of superior quality by luxury brands | Rare diamonds, platinum | For special purposes and prestige | |

| Costume Jewelry | Inexpensive and decorative jewelry | Glass, plastic, inexpensive metals | For everyday wear and parties |

| Men-specific jewelry types | Gold, steel, leather | Everyday use and gifts |

Market Dynamics

Rising Disposable Income: The increasing disposable income of the middle-class population drives jewelry purchases. Consumers are increasingly preferring luxury jewelry. An expanding middle class, especially in urban populations, prefer branded, design-forward, and customized pieces over traditional jewelry purchases. This shift is elevating overall spending. It also propels demand for quality assurance, brand reputation, and post-sale services. Aspirational buyers are treating jewelry as an occasional purchase and as a regular fashion accessory. It complements their lifestyle and identity, leading to overall growth.

Growing E-commerce Sector: E-commerce platforms are emerging sales channels. Amid a hectic lifestyle and a tight work schedule, consumers prefer convenience and personalization when purchasing jewelry. According to the U.S. Census Bureau, e-commerce sales in the U.S. accounted for USD 300.2 billion in Q1 2025. It showed 6.1% growth from Q1 2024. Online retail platforms provide secure payment options and virtual try-on features. Buyers get detailed product descriptions and product reviews on these platforms. It helps them compare products and make decisions effectively. Such advantages enhance consumers’ shopping experience. Direct-to-consumer brands disrupt traditional distribution. The online retail industry helps smaller designers reach customers across the world. Brands integrate data analytics for targeted marketing and tailored promotions. Omnichannel jewelry retail combines online and offline experiences. Many jewelry brands are focusing on offering their products on these channels. Therefore, the growing shift toward omnichannel retail boosts sales of digital jewelry.

Emerging Trends in Jewelry Market

There has been a shift in the market towards customization and sustainability. People are buying jewelry customized to their own personal taste. For instance, some people have their names carved into jewelry. Birthstone jewelry is another example of the trend. There has also been an increase in the use of artificial diamonds, which are cheaper and more environmentally friendly than mined diamonds. Some of the other innovations in the market include the use of recycled metals and transparent sourcing. Besides, 3D printing technology has enabled rapid design innovation for manufacturing companies.

What are the Emerging Trends, Opportunities, and Restraints?

- Rising Adoption of Advanced Technologies: 3D printing in jewelry manufacturing, digital twins, AI-enabled product customization, and smart rings/wearable jewelry boost product development cycles. 3D printing jewelry manufacturing accelerates jewelry customization and prototyping. It enables rapid and precise mold creation. Use of 3D printing helps reduce production time and costs. It also supports intricate, design-driven manufacturing. The deployment of advanced technologies enables hyper-personalized designs. Retailers adopt augmented reality/virtual reality (AR/VR). The introduction of AR/VR jewelry shopping experience boosts conversion in the digital sales funnel. It also helps brands reduce return rates. These advantages reinforce the shift toward hybrid jewelry retail.

- Growing Demand from Younger Consumers: There is an increasing interest in self-purchase jewelry among Millennials and Gen Z jewelry buyers. Demand for fashion jewelry and everyday wear pieces is high among these generations. A few Gen Z jewelry trends are value personalization and modern minimalist designs.

- Increasing Emphasis on Sustainable Practices: Sustainability has become a defining theme in the ethical jewelry market. There is a rising consumer preference for recycled metal jewelry and CVD lab-grown diamonds jewelry. Also, the focus on conflict-free diamond certification is increasing. Thus, market players focus on ethical jewelry sourcing. Jewelry brands adhere to Responsible Jewellery Council (RJC) standards and strengthen ESG frameworks. It helps them improve transparency through traceability programs. The growing vintage and pre-owned jewelry market is contributing to circular economy in jewelry.

- Fluctuating Raw Material Prices: There is volatility in raw material prices, especially of gold, silver, and platinum. It creates constant cost instability for jewelry manufacturers and wholesalers. It negatively impacts profit margins and pricing strategies. Inconsistent gemstone prices disrupt inventory planning. Thus, B2B players struggle to maintain consistent pricing and manage long-term supply contracts. Thus, fluctuating raw material prices restrain the jewelry industry growth. Also, high import duty on gold jewelry and gold hinders the market growth.

Segmental Insights

Product Analysis

Based on product, the segmentation includes necklace, ring, earrings, bracelet, and other products. The ring segment accounted for 32.03% of the revenue share in 2025. The dominance is fueled by the upsurging demand for engagement and wedding rings. Growing interest in customization and minimalistic designs propels the demand for rings. Jewelry retailers are including vintage-inspired, gemstone-embedded, and stackable rings. Such collections appeal to a wide range of consumers. Consumer inclination toward rings as sentimental and fashionable pieces keeps this segment dominant in value and volume.

Type Analysis

In terms of type, the segmentation includes silver, gold, platinum, diamond, and others. The gold segment accounted for 60.40% of the revenue share in 2025. As per our gold jewelry segment analysis, strong cultural value and high investment appeal drive the segment growth. High use of gold jewelry during weddings and festivals also boost segment dominance. Consumers view gold as both an adornment and a financial asset it contributes to steady sales of gold jewelry. According to the World Gold Council, gold demand for Q1 2025 increased by 1% year-on-year. It reached 1,206 tonnes, including investment activity. Retailers offer hallmark-certified and lightweight gold jewelry. It attracts a broader consumer base. Promotional campaigns and seasonal discounts supported consistent demand for gold jewelry.

Lab-Grown vs Natural Diamonds

| Parameter | Lab-Grown Diamonds | Natural Diamonds |

| Cost Structure and Pricing |

|

|

| Supply Chain Reliability |

|

|

| Brand Positioning |

|

|

| Quality & Certification |

|

|

| Sustainability Narrative |

|

|

| Inventory and Working Capital |

|

|

| Technological Dependency |

|

|

| Market Dynamics & Regulation |

|

|

| B2B Sales Strategy |

|

|

Distribution Channel Analysis

By distribution channel, the segmentation includes offline and online. The offline segment accounted for 65.30% of revenue share in 2025. Consumer preference for physical inspection is rising, especially for high-value purchases such as gold and diamond jewelry. Therefore, they prefer offline distribution channels for jewelry purchase. Trust in legacy jewelers, personalized services, and immediate product availability encourage in-store purchases. Many consumers seek certification and secure billing. Therefore, they associate with established offline retailers. Flagship stores and showroom expansions in urban and semi-urban areas support this channel’s dominance.

Online vs Offline Behavioral Shifts

| Dimension | Online (E-commerce/Digital Buyers) | Offline (In-store/Traditional Buyers) |

| Product Discovery |

|

|

| Buying Behavior |

|

|

| Information Needs |

|

|

| Preferred Categories |

|

|

| Customer Experience Expectations |

|

|

| Payment |

|

|

| Trust Factors |

|

|

| Return & After-Sales |

|

|

| Technology Impact |

|

|

Category Analysis

In terms of category, the segmentation includes branded and unbranded. The unbranded segment accounted for 60.8% of the revenue share in 2025. Competitive pricing and design flexibility fuel the segment dominance. Also, the leading position is attributed to availability across local markets. In semi-urban and rural regions, people prefer non-branded jewelry over branded jewelry. The main factor in this case remains customization, which brands do not offer. Despite growing branded competition, the ability of local artisans and retailers to offer personalized designs at lower price points has kept this segment resilient.

Regional Analysis

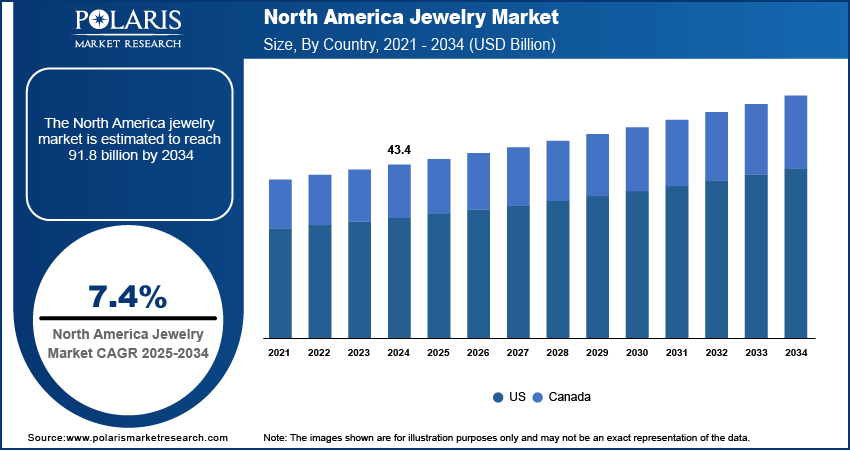

North America Jewelry Market

The North America market is expected to register a significant CAGR of 8.4% during the forecast period. It is driven by increasing consumer interest in luxury goods and accessories and personalized adornments. Higher disposable income and strong gifting culture drive the jewelry sales in the region. Further, the rising influence of celebrity and fashion trends boost demand. In 2024, the U.S. Census Bureau reported a steady rise in consumer spending on luxury goods. It also reported a 9.2% year-over-year increase in jewelry retail sales. There is a growing adoption of lab-grown diamonds and sustainable materials. It aligns with changing consumer values. Major brands leverage digital platforms and omnichannel strategies to attract a tech-savvy population. Customization services, smart/connected jewelry features, and augmented reality (AR) try-on tools accelerate market penetration.

U.S. Jewelry Industry Insight

In 2025, the U.S. dominated the North America market by holding 93.09% of the revenue share. Rising consumer spending power and strong demand for bridal and fashion jewelry drive the dominance. Also, widespread availability of premium and affordable product ranges contributed to the U.S. fine jewelry market growth. Department stores, luxury boutiques, and online platforms offer a broad collection. They focus on catering to diverse preferences. Aggressive marketing by global brands and the rising popularity of customized and ethically sourced pieces play a key role in U.S. jewelry market growth.

Asia Pacific Jewelry Market Trends

Asia Pacific held the largest revenue share of 58.50% in 2025. Importance of gold jewelry in festivals and wedding ceremonies propels the market dominance. Also, rising spending power of middle-class population, due to increasing disposable income boosts jewelry sales across the region. According to the India Brand Equity Foundation, in Q2 2024, India’s gem and jewelry exports reached USD 7.1 billion. It reflects a 12% increase compared to the same period in 2023. Thus, growth jewelry export contributes to the regional market growth.

India Jewelry Industry Overview

India held the largest share of 28.2% in Asia Pacific in 2025. Deep-rooted cultural significance of jewelry drives the India jewelry market growth. Also, expanding consumer base propels the growth. Weddings, festivals, and religious ceremonies drive consistent jewelry demand. The shift toward branded and hallmarked gold jewelry is gaining momentum. Government regulations and awareness campaigns boost the preference for such jewelry items. Millennial preferences are also influencing trends. They prefer to purchase lightweight designs, gemstone fusion pieces, and artisanal craftsmanship.

China Jewelry Market Overview

China accounted for 24.6% of the revenue share in 2025. High demand for gold and diamond ornaments during cultural festivals and personal milestones boost the industry expansion. Urbanization and a rising female workforce have led to greater self-purchase trends. Consumers seek brand identity and certified products. Thus, premiumization is gaining traction across China. Jewelry retailers focus on smart stores, D2C practices, and digital innovation to attract young buyers. It contributes to China jewelry e-commerce trends. However, heritage brands continue to benefit from long-standing consumer trust in product purity and design heritage.

Europe Jewelry Market Analysis

The industry in Europe is expected to register a CAGR of 7.5% from 2026 to 2034. Increased interest in luxury fashion accessories and sustainable fine jewelry boosts the market growth. European consumers prefer high-quality craftsmanship, traceable sourcing, and limited-edition collections. High-end watches, vintage jewelry styles, and heritage-inspired pieces are high in demand. E-commerce growth and influencer marketing boost the jewelry sales across the region. Also, collaborations between fashion houses and jewelry designers enhance visibility. The regional market is witnessing rising sales of men’s jewelry. France luxury jewelry brands market is expected to witness a significant growth. The presence of iconic heritage brands will drive the growth. Increasing penetration of e-commerce platforms, along with increasing availability of 5G networks, boosts the UK online jewelry sales

Germany Jewelry Market Insights

Germany held 21.5% of the revenue share in 2025. Demand for elegant and practical gold and silver items is rising across the country. Customers prefer certified and durable products, as well as artisanal craftsmanship. Family-owned brands and independent jewelers remain popular in Germany. They offer jewelry items with unique designs that showcase local heritage. Surging interest in online shopping and increasing focus on ethically sourced gold influence buying choices. Minimalistic, stackable jewelry is emerging as a trend across the country.

Italy Jewelry Market Overview

The jewelry industry in Italy is projected to witness fastest growth from 2026 to 2034. The country is well-known for luxury and premium jewelry designs. The country consists of specialized regional hubs. Italy jewelry manufacturing cluster focuses on high craftsmanship. Strong export-oriented production contributes to the market growth in Italy. Younger consumers are interested in contemporary styles with Italian elegance. Local brands use different materials such as enamel, ceramic, and eco-friendly metals. They focus on making jewelry that aligns with sustainable fashion trends. Export strength, fashion week collaborations, and tourism-related purchases boost the premium jewelry segment in Italy.

Middle East & Africa Jewelry Market

The Middle East & Africa jewelry industry growth is supported by strong cultural affinity for gold and growing tourism-driven retail. The UAE gold jewelry demand remains high due to Dubai’s role as a global gold-trade hub. Its competitive pricing will boost the Dubai jewelry industry. Rising demand for diamond-centric designs and premium branded pieces contribute to Saudi Arabia luxury jewelry trends. Modern styles aligned with Vision 2030’s evolving consumer lifestyle will drive the Saudi Arabia jewelry industry growth.

Key Players and Competitive Landscape Jewelry Market

Dynamic industry analysis and evolving expansion strategies shape the competitive landscape. According to our jewelry market competitors analysis, leading players are pursuing joint ventures and strategic alliances. These strategies help them strengthen global distribution networks. It will also help them enter emerging markets. Luxury jewelry brands strategies emphasize investing in high-value markets. They focus on investing in China, the U.S., and the Middle East. Mergers and acquisitions consolidate design expertise. They also diversify product portfolios. Efficient post-merger integration enhances operational synergy. Emerging D2C jewelry brands adopt technology advancements such as AI-driven customization and augmented reality. It helps them redefine the consumer experience. Companies invest in sustainable sourcing and digital transformation. Thus, they can meet evolving consumer expectations. Innovation in branding and personalized offerings remains central to competitive differentiation.

Key Players in Jewelry Industry

- Buccellati

- Cartier

- Chow Tai Fook Jewellery Group Limited

- LVMH Group

- Malabar Gold & Diamonds

- PANDORA JEWELRY LLC

- SHR Jewelry Group LLC

- Swarovski

- Swatch Group AG

- Titan Company Limited

Jewelry Industry Developments

- April 2026: Linkest Limited announced the launch of a bespoke lab-grown diamond jewelry line, offering customizable and sustainable luxury pieces. These pieces are both luxurious and environmentally friendly. This change shows how people are looking for ethical, affordable, and personalized jewelry. (Source: globenewswire.com)

- June 2025: De Beers introduced Ombré Desert Diamonds. This jewelry collection features multi-stone pieces inspired by desert colors. The company launched Origin. The program offers polished diamonds with blockchain-backed traceability. The traceability emphasizes diamond’s origin, rarity, and social impact. (Source: debeersgroup.com)

- May 2025: Dialog Solutions Inc. partnered with Kunming Diamonds. The partnership aims to feature Kunming's collection of natural yellow diamonds on the Dialog platform. It enhances accessibility for gem enthusiasts and industry professionals. (Source: jewelers.org)

Jewelry Market Segmentation

By Product Outlook (Revenue, USD Billion, 2021–2034)

- Necklace

- Ring

- Earrings

- Bracelet

- Other Products

By Type Outlook (Revenue, USD Billion, 2021–2034)

- Silver

- Gold

- Platinum

- Diamond

- Others

By Category Outlook (Revenue, USD Billion, 2021–2034)

- Branded

- Unbranded

By Distribution Channel Outlook (Revenue, USD Billion, 2021–2034)

- Offline

- Online

By End User Outlook (Revenue, USD Billion, 2021–2034)

- Men

- Women

- Children

By Regional Outlook (Revenue, USD Billion, 2021–2034)

- North America

- U.S.

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Jewelry Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 286.15 Billion |

| Market Size in 2026 | USD 304.87 Billion |

| Revenue Forecast by 2034 | USD 608.65 Billion |

| CAGR | 8.7% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2022–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD billion, 2022–2034 and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format | PDF + Excel |

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

The global jewelry market will reach USD 608.65 billion by 2034. It will register a CAGR of 8.7% during the forecast period. Luxury demand and personalization trends will boost the market growth.

Asia Pacific held the largest share of 58.50% in 2025. Cultural significance in India and China drives the regional market growth. Also, rising disposable incomes propel the segment dominance.

The gold segment led revenue share by holding 60.40% in 2025. Strong cultural value and high investment appeal fuel the dominance.

The rings segment held the largest share, 32.03%, in 2025. The rising demand for wedding and engagement rings drives the ring market growth.

Smart jewelry, gender-neutral designs, and 3D printing technology are among the key future trends.

The gold segment accounted for 60% of the revenue share in 2024 due to strong cultural value, high investment appeal, and enduring demand for gold during weddings and festivals.

Download Sample Report of Jewelry Market

Please fill out the form to request a customized copy of the research report.