Spinal Implants Market Trends, Share, Global Analysis Report, 2026-2034

REPORT DETAILS

Spinal Implants Market Overview and Key Insights

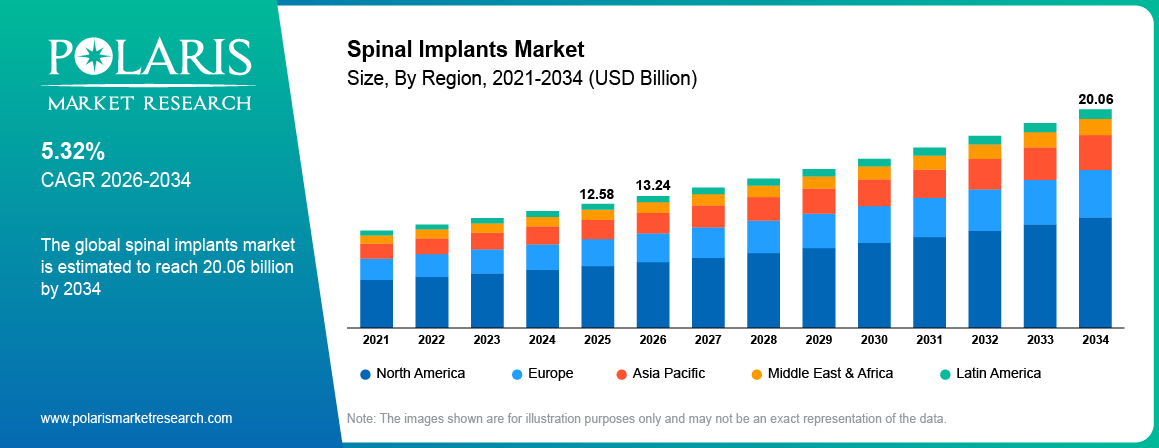

The global spinal implants market size was valued at USD 12.58 billion in 2025. It is projected to grow from USD 13.24 billion in 2026 to USD 20.06 billion by 2034, exhibiting a CAGR of 5.32% during 2026–2034.

Market Statistics

Spinal Implants Market Key Takeaways

- North America dominated the market in 2025. The region held 44.0% share due to advanced healthcare systems.

- Asia Pacific is projected to grow at a CAGR of 6.9% during 2026–2034. Rising healthcare investments are driving growth.

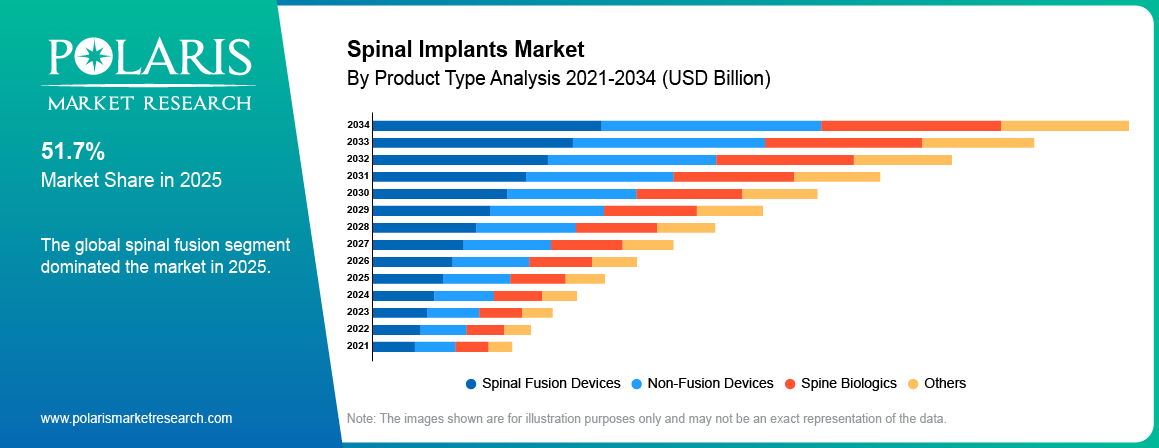

- Spinal fusion devices led the market in 2025. The segment accounted for 51.7% share due to high surgery volumes.

- Minimally invasive surgery is expected to grow at a CAGR of 7.6% through 2034. Faster recovery is boosting adoption.

- India spinal implants market is projected to register a CAGR of 9.8% during 2026–2034. Medical tourism is supporting demand.

- Metallic material segment accounted for 58.0% share in 2025.

Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations.

Spinal Implants Market Dynamics

- Rising spinal disorders and poor lifestyle habits are increasing demand for spinal implants globally across global regions.

- Growing elderly population is driving demand for spine surgeries due to higher risk of degeneration and disorders.

- Technological advancements in spinal implants are improving surgical outcomes and increasing adoption of advanced treatment options globally.

- Increasing preference for minimally invasive spine surgeries is boosting market growth due to reduced pain recovery time.

- High cost of spinal implant surgeries and limited access to care in developing regions is restraining growth.

Impact of AI and Robotics on the Spinal Implants Market

- AI improves preoperative planning and surgical accuracy.

- AI-assisted robotics enhances implant placement precision.

- Machine learning enables personalized treatment planning.

- AI supports post-operative monitoring and recovery tracking.

What Are Spinal Implants and How Do They Work?

Spinal implants are medical devices used to support and stabilize the spine during or after spinal surgery, often to treat conditions such as fractures, deformities, or degenerative disc diseases. These implants include rods, screws, plates, and cages, and are designed to help maintain proper alignment and promote spinal fusion.

The increasing prevalence of spinal diseases such as degenerative disc disease, scoliosis, and spondylolisthesis propels the demand for spinal implants. Additionally, the rising geriatric population, who are more susceptible to spinal disorders, is contributing to the growth of the spinal implants market. Advancements in technologies and innovative product launches are driving spinal implant appeal to the general population, which fuels the market growth. In November 2023, Spinal Elements launched the Ventana 3D-Printed Interbody Portfolio, featuring innovative design maximizing bone graft volume and providing clear radiographic visualization for spinal fusion procedures. These product launches are driving the growth of the spinal implant industry.

Source: Polaris Market Research Analysis

To Understand More About this Research: Download Sample Report

The development of advanced technologies, such as minimally invasive techniques and biodegradable materials, provides patients with safer and more effective treatment options, which boosts the adoption of spinal implants. This growing demand for spinal implants is expected to continue, driven by advancements in medical technology.

Spinal Fusion vs. Non-fusion Implants: Benefits and Use Cases

| Parameter | Spinal Fusion Implants | Non-Fusion Implants |

| Mobility | Restricts motion by permanently joining vertebrae | Preserves natural spine movement |

| Recovery Time | Longer recovery due to bone healing and fusion process | Faster recovery with less tissue disruption |

| Long-term Outcomes | Stable but may increase stress on adjacent segments | Reduces adjacent segment degeneration risk |

| Surgical Complexity | Generally more invasive and technically demanding | Less invasive with advanced motion-preserving techniques |

Source: Polaris Market Research Analysis

Spinal Implants Market Trends

Rising Prevalence of Degenerative Spine Disorders

The growing number of spinal disorders, such as degenerative disc disease, scoliosis, spinal stenosis, and herniated discs, is significantly driving the spinal implant demand. According to a report published by NCBI, incidents of herniated discs are 5 to 20 cases per 1,000 adults annually in the US alone. These conditions cause severe pain and mobility issues, requiring surgical treatment involving implants. Sedentary lifestyles, poor posture, and increased screen time are further contributing to the rise in spinal problems among all age groups. The demand for reliable and effective spinal implants grows as more people experience these health issues, thereby boosting the industry growth.

Aging Population and Rising Spine Surgery Volumes

The growth in the global aging population is boosting the demand for spinal implants. According to the Statistics Canada, 7,820,121 persons aged 65 years and above in Canada alone as of July 2024, showcasing the growth in the elderly population. With the growing age, bones and spinal structures weaken naturally, making older people more vulnerable to conditions such as osteoporosis and spinal degeneration. Older adults often require surgical interventions to relieve pain and restore mobility, and spinal implants play a key role in these procedures. More elderly individuals are opting for surgeries to maintain their quality of life with improved life expectancy and better access to healthcare, thereby propelling the spinal implants market growth.

Source: Polaris Market Research Analysis

Spinal Implants Market Segment Analysis

Spinal Implants Market, by Surgical Procedure

The spinal implants market segmentation, based on procedure, includes open surgery and minimally invasive surgery. The minimally invasive surgery is expected to witness significant growth at a CAGR of 7.6% during the forecast period during the forecast period. MIS techniques offer benefits such as reduced damage to surrounding tissues, shorter hospital stays, and quicker recovery times compared to traditional open surgeries. Growing patient preference for less painful and faster procedures is driving demand for spinal implants designed for MIS. Advancements in surgical equipment and improved imaging methods are improving the precision and accessibility of these procedures, thereby driving the segment growth.

Spinal Implants Market, by Product Type

The market segmentation, based on product type, includes spinal fusion devices, non-fusion devices, spine biologics, and others. The spinal fusion segment dominated the market with 51.7% share in 2025. As spinal fusion surgeries are commonly performed to treat various spinal conditions such as degenerative disc disease, spondylolisthesis, and fractures. These surgeries involve the use of spinal fusion devices, which help stabilize and align the spine, promoting bone growth and healing. Additionally, advancements in technology have led to the development of innovative fusion devices, such as motion-preserving devices and minimally invasive, which have increased their adoption rate among orthopedic surgeons. Further, the aging population and increasing prevalence of spinal disorders also contribute to the high demand for spinal fusion devices, contributing to the dominance of this segment.

Source: Polaris Market Research Analysis

Spinal Implants Market Regional Analysis

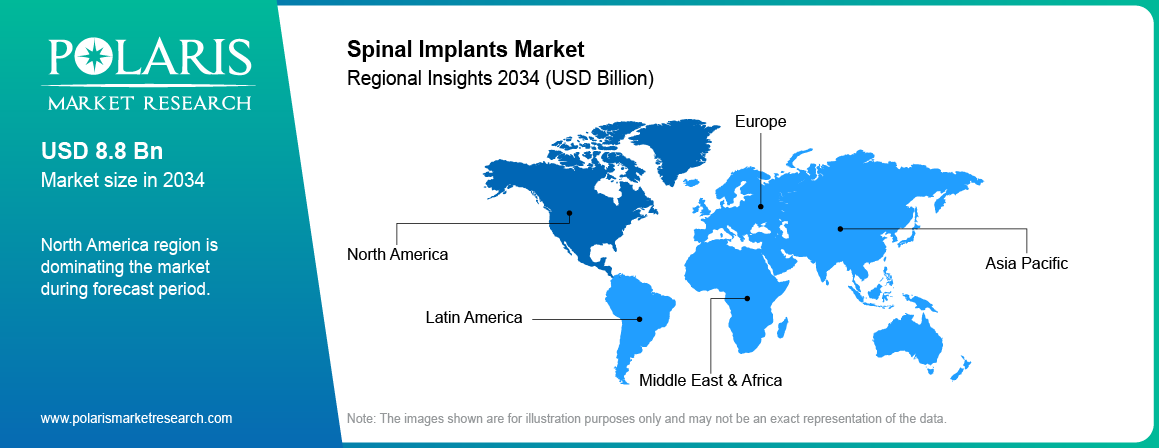

By region, the study provides the spinal implants market insights into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. In 2025, North America dominated the market with 44.0% share, due to the increasing prevalence of spinal disorders and injuries in the region, which has led to a growing demand for advanced spinal implant technologies. The National Spinal Cord Injury Statistical Center reports an annual incidence of around 54 cases of spinal cord injury per one million people in the US, leading to ∼17,500 new SCI cases each year. The presence of well-established healthcare infrastructure, high healthcare expenditure, and favourable reimbursement policies contributed to the spinal implants market expansion in North America. Additionally, the region is home to many prominent players in the spinal implant industry, which has boosted innovation and advancements in technology, leading to increased adoption rates among patients and healthcare professionals.

Source: Polaris Market Research Analysis

Asia Pacific is expected to record the highest CAGR of 6.9% during the forecast period due to a rising elderly population, increasing cases of spinal disorders, and growing awareness of advanced treatment options. Countries such as China, Japan, South Korea, and Australia are investing heavily in healthcare infrastructure and technology. Economic development in the region has improved access to quality medical care, while medical tourism is further boosting demand for spinal surgeries. Additionally, increasing adoption of minimally invasive procedures and technological advancements in spinal implants are attracting both domestic and international companies, thereby driving the market growth in Asia Pacific.

Indian spinal implant demand is growing rapidly at a CAGR of 9.8% during the forecast period, due to its large population, rising healthcare awareness, and a growing number of spine-related conditions. Urbanization, changing lifestyles, and longer life expectancy are leading to more cases of back and spinal problems. The country is also reporting a rise in the number of skilled spine surgeons and specialty hospitals offering affordable yet advanced surgical procedures. Government initiatives and private investments are improving healthcare access, particularly in tier 2 and tier 3 cities. Furthermore, India’s cost-effective treatment options are attracting international patients, making it a hub for medical tourism and boosting demand for spinal implants.

Key Players and Competitive Analysis

The market opportunity is constantly evolving, with numerous companies striving to innovate and distinguish themselves. Leading global corporations dominate the market by leveraging extensive research and development, and advanced techniques. These companies pursue strategic initiatives such as mergers and acquisitions, partnerships, and collaborations to enhance their product offerings and expand into new markets.

New companies are impacting the industry by introducing innovative products to meet the demand of specific sectors. The competitive trend is amplified by continuous progress in product offerings. A few major players in the industry include Alphatec; Braun Melsungen AG; Globus Medical; Johnson & Johnson Services, Inc.; Medtronic Plc; NuVasive, Inc.; Orthofix Medical Inc.; Spinal Simplicity; Stryker Corporation; and Ulrich Medical.

Medtronic plc is a developer, manufacturer, and seller of device-based medical therapies. The company's business operations are divided into the Cardiovascular Portfolio, Medical Surgical Portfolio, Neuroscience Portfolio, and Diabetes Operating Unit. Medtronic's cardiovascular portfolio segment specializes in implantable cardiovascular devices such as defibrillators, pacemakers, and resynchronization therapy devices. Additionally, it offers insertable cardiac monitor systems, cardiac ablation products, TYRX products, and remote patient-centered and monitoring software. The Medical Surgical Portfolio segment provides a range of surgical products, including vessel sealing instruments, surgical stapling devices, wound closure and electrosurgery products, hernia mechanical devices, surgical artificial intelligence and robotic-assisted surgery products, mesh implants, lung products, gynecology, and various therapies to treat diseases. It also offers products in the fields of minimally invasive gastrointestinal and hepatologic diagnostics and therapies. The Neuroscience Portfolio segment offers products for various medical professionals, including neurosurgeons, spinal surgeons, neurologists, anesthesiologists, pain management specialists, orthopedic surgeons, urologists, interventional radiologists, urogynecologists, and throat specialists. The segment also provides intra-operative imaging systems, image-guided surgery systems, and robotic guidance systems used in robot-assisted spine procedures. The Diabetes Operating Unit segment specializes in continuous glucose monitoring systems, insulin pumps and consumables, smart insulin pen systems, and consumables and supplies.

Johnson & Johnson Services, Inc. is a multinational corporation based in New Brunswick, New Jersey, USA. The company operates through pharmaceuticals, medical devices, and consumer health products operations. The company's subsidiary, Janssen Pharmaceuticals, Inc., develops and markets drugs in various therapeutic areas, including neuroscience, oncology, infectious diseases, and immunology. Janssen Pharmaceuticals, Inc. is creating many well-known drugs, such as Risperdal (risperidone), Remicade (infliximab), and Zytiga (abiraterone). The company also has a medical devices division, which develops and markets a wide range of products, including surgical instruments, orthopedic implants, and diabetes care products. It also has a consumer health division, which develops and markets over-the-counter products such as Band-Aids, Tylenol, and Listerine. The company's consumer health business also includes subsidiaries such as Neutrogena, Aveeno, and Johnson's Baby. The company was founded in 1886. Johnson & Johnson sells its products under the brand The DePuy Synthes, an orthopedic company that was acquired in 1998. DePuy Synthes under J&J offers advanced spinal implants and devices, including personalized surgical solutions, deformity correction, trauma fixation, and innovative materials for craniomaxillofacial and orthopedic procedures.

List of Key Companies in Spinal Implants Market

- Alphatec

- Braun Melsungen AG

- Globus Medical

- Johnson & Johnson Services, Inc.

- Medtronic Plc

- NuVasive, Inc.

- Orthofix Medical Inc.

- Spinal Simplicity

- Stryker Corporation

- Ulrich Medical

Challenges in Spinal Implants Market

- Implant failure risk: Possibility of implant loosening, breakage, or misalignment affecting long-term outcomes.

- High surgery cost: Expensive procedures and implant systems limiting affordability for patients.

- Post-operative complications: Risks such as infections, nerve damage, and prolonged recovery impacting patient outcomes.

- Limited access in developing regions: Lack of advanced healthcare infrastructure and skilled professionals restricting treatment availability.

Spinal Implants Market Future Outlook

Future growth of the spinal implants market is expected to be driven by the rising prevalence of spinal disorders and increasing adoption of minimally invasive procedures. Expansion of robotic-assisted spine surgeries is likely to improve surgical precision and outcomes. Growing use of 3D-printed personalized implants is supporting customized treatment approaches. Continuous innovation in biomaterials is enhancing implant safety, durability, and recovery outcomes. These factors are expected to collectively support sustained market expansion.

Spinal Implants Market Recent Developments

- February 2026: Medtronic received FDA clearance for its Stealth AXiS surgical platform. It integrates AI-based planning, real-time navigation, and robotic assistance. (Source: medtronic.com)

- July 2025: Osteotec entered an exclusive UK distribution agreement with Ulrich Medical to supply its advanced spinal implant systems. The partnership expands Osteotec’s spine portfolio by introducing Ulrich’s vertebral body replacement and dynamic stabilization solutions to both NHS and private healthcare providers. The collaboration is intended to enhance surgical outcomes for complex spinal procedures across the UK. (Source: osteotec.com)

- August 2025: Carlsmed secured USD 100.5 million through its IPO to accelerate the expansion of its aprevo platform, which provides 3D-printed personalized spinal implants. The company additionally received CMS approval for New Technology Add-On Payment (NTAP) reimbursement for cervical fusion procedures, enabling hospitals to receive up to USD 21,125 per case beginning in October 2025. (Source: carlsmed.com)

Spinal Implants Market Segmentation and Forecast

By Product Type Outlook (Revenue USD Billion, 2021–2034)

- Spinal Fusion Devices

- Thoracic Fusion & Lumbar Fusion Devices

- Cervical Fusion Devices

- Expandable Fusion Cages

- Others

- Non-Fusion Devices

- Dynamic Stabilization Devices

- Artificial Discs

- Annulus Repair Devices

- Nuclear Disc Prostheses

- Others

- Spine Biologics

- Others

By Material Outlook (Revenue USD Billion, 2021–2034)

- Metallic Material

- Polymers Material

- Ceramic Material

- Others

By Procedure Outlook (Revenue USD Billion, 2021–2034)

- Open Surgery

- Minimally Invasive Surgery

By End User Outlook (Revenue USD Billion, 2021–2034)

- Hospitals

- Orthopedic Centers

- Others

By Regional Outlook (Revenue USD Billion, 2021–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Spinal Implants Market Report Scope and Methodology

| Report Attributes | Details |

| Market Size Value in 2025 | USD 12.58 billion |

| Market Size Value in 2026 | USD 13.24 billion |

| Revenue Forecast by 2034 | USD 20.06 billion |

| CAGR | 5.32% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Spinal Implants Market Frequently Asked Questions

The market size was valued at USD 12.58 billion in 2025 and is projected to grow to USD 20.06 billion by 2034.

The global market is projected to register a CAGR of 5.32% during the forecast period.

North America dominated the market in 2025. The region held 44.0% share due to advanced healthcare systems.

A few key players in the market are Alphatec; Braun Melsungen AG; Globus Medical; Johnson & Johnson Services, Inc.; Medtronic Plc; NuVasive, Inc.; Orthofix Medical Inc.; Spinal Simplicity; Stryker Corporation; and Ulrich Medical.

Spinal fusion devices led the market in 2025. The segment accounted for 51.7% share due to high surgery volumes.

Minimally invasive surgery is expected to grow at a CAGR of 7.6% through 2034. Faster recovery is boosting adoption.

Download Sample Report of Spinal Implants Market

Please fill out the form to request a customized copy of the research report.