Sugar Confectionery Market Size, Trends Forecast Report, 2026-2034

REPORT DETAILS

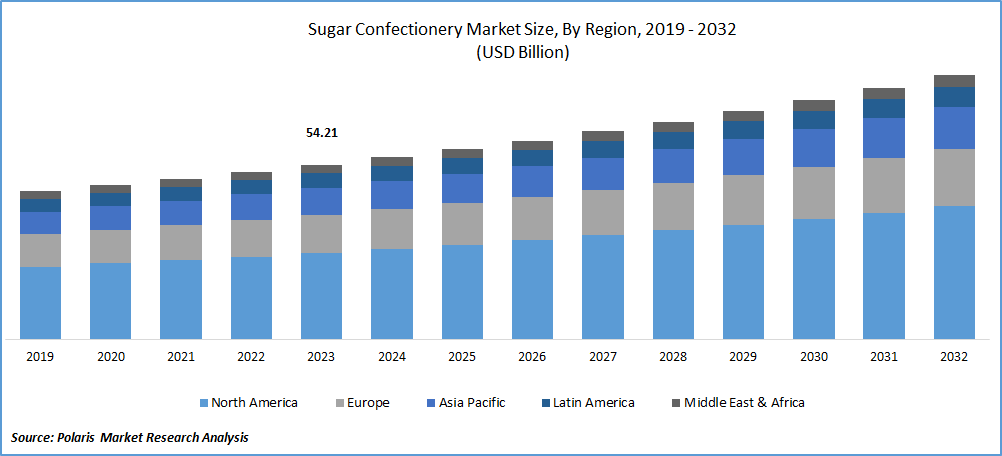

Sugar Confectionery Market Summary

The global sugar confectionery market size was valued at USD 52.59 billion in 2025 and is projected to grow at a CAGR of 4.8% during 2026–2034. The market growth is driven by rising disposable income, growing interest in premium confectionery products, and the introduction of innovative products by manufacturers.

Market Statistics

Key Insights

- Europe accounted 33.7% market share in 2025, owing to robust consumer demand for traditional confections and high cultural affinity for premium candies.

- North America is witnessing robust growth of 5.2% CAGR. The regional market growth is fueled by robust consumer demand for indulgent treats and ongoing innovation in texture and packaging.

- The hard candy segment accounted 25.4% market share in 2025. The segment’s dominance is driven by the extended shelf life of hard candies and high consumer preference across diverse age groups.

- The online retail segment is projected to register the highest CAGR of 5.4% during the projection period, primarily due to increasing digital penetration and the rise of direct-to-consumer confectionery brands.

- Supermarkets/Hypermarkets held the largest market share of 42.6% in the Sugar Confectionery Market in 2025 owing to their extensive product assortment and strong consumer footfall.

Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations.

Industry Dynamics

- The rising prominence of e-commerce platforms, which has increased accessibility to both niche and international brands, is driving market expansion.

- Rapid urbanization has transformed consumer consumption habits and is fueling market development. Consumers now prefer convenient products that align with their fast-paced lives.

- The introduction of attractive packaging and endorsements by celebrities helps boost brand visibility and consumer appeal.

- Health concerns related to high sugar intake may present market challenges.

Source: Polaris Market Research Analysis

To Understand More About this Research: Download Sample Report

Growing disposable incomes of consumers, especially in emerging economies, have increased spending on indulgent and premium confectionery products, which drives the market growth. In addition, increasing interest in artisanal and premium confectionery products and development of innovative products propel the demand for sugar confectionery products.

What is Sugar Confectionery?

Sugar confectionery refers to sweet food products primarily made with sugar, syrups, flavorings, and colorants. Candies, gummies, jellies, toffees, chewing gum, medicated confectionery, and hard-boiled sweets are a few examples of sugar confectionery. These products are widely consumed for indulgence, refreshment, gifting, and functional purposes. They are available across retail stores, online platforms, and foodservice distribution channels worldwide.

The sugar confectionery market is involved in the production, distribution, and sale of confectionery products that are primarily based on sugar. Festive seasons and cultural celebrations drive temporary spikes in sales, particularly in regions such as Asia Pacific and Europe. Moreover, the rising popularity of candies infused with vitamins, probiotics, or herbal extracts is attracting health-aware consumers.

Manufacturers are introducing new flavors, textures, and formats such as functional candies with vitamins, herbal ingredients to attract health-conscious consumers, which is driving demand for sugar confectionery. Additionally, aggressive advertising, attractive packaging, and celebrity endorsements help boost brand visibility and consumer appeal.

Difference Between Sugar Confectionery Vs Chocolate Confectionery

| Aspect | Sugar Confectionery | Chocolate Confectionery |

| Primary Ingredients | Mainly produced using sugar, syrups, flavorings, and colorants | Primarily manufactured using cocoa, cocoa butter, milk, and sugar |

| Product Types | Candies, gummies, jellies, toffees, chewing gums, hard-boiled sweets, and medicated confectionery | Chocolate bars, pralines, truffles, filled chocolates, and chocolate-coated snacks |

| Flavor Profile | Fruity, minty, sour, and diverse sweet flavors | Rich cocoa-based, creamy, nutty, and premium flavors |

| Texture Variety | Chewy, hard, gummy, jelly-like, and soft textures | Smooth, creamy, crunchy, or filled textures |

| Consumer Usage | Popular for refreshment, impulse snacking, and functional purposes | Commonly associated with indulgence, gifting, and premium consumption |

| Pricing Range | Generally affordable and mass-market oriented | Includes both mass-market and premium-priced products |

| Functional Applications | Includes medicated confectionery and breath-freshening gums | Limited functional applications compared to sugar confectionery |

| Market Positioning | Focuses on variety, novelty, and convenience | Focuses on indulgence, taste richness, and premium appeal |

Source: Polaris Market Research Analysis

Market Dynamics

Expansion of E-commerce Platforms

The growing prominence of e-commerce platforms has significantly transformed the market, offering enhanced accessibility to a wide array of niche and international brands. The Census Bureau released its estimates for US retail e-commerce sales for Q1 2025, which stand at USD 300.2 billion. Consumers enjoy seamless purchasing experiences, diverse product assortments, and tailored recommendations, which encourage brand exploration beyond conventional retail. Small and emerging confectionery brands benefit from digital storefronts that lower entry barriers and facilitate direct-to-consumer models, enabling them to scale operations without significant physical infrastructure. Promotions, customer reviews, and influencer marketing across online platforms further amplify visibility and drive engagement. Enhanced logistics, cold-chain capabilities, and last-mile delivery services have also improved product preservation and consumer satisfaction, making e-commerce a critical channel for overall expansion and brand differentiation.

Urbanization and Changing Lifestyles

Rapid urbanization has led to evolving consumption habits, particularly a growing preference for convenient, ready-to-consume products that align with fast-paced city life. According to the United Nation, over 50% of the global population lives in urban areas, with projections suggesting this will reach two-thirds by 2050. Increased time constraints and fragmented meal patterns have driven the popularity of sugar confectionery items such as chewing gum, mints, and candies, which are perceived as portable indulgences. Consumers seek quick energy boosts or stress relief during commutes or work hours, positioning confectionery products as functional and emotionally satisfying. Retail formats such as vending machines, convenience stores, and impulse-buy sections in urban centers further cater to this demand. In response, manufacturers are innovating with flexible packaging, portion control, and multi-flavor offerings tailored to modern, on-the-go lifestyles.

What are the Future Trends in the Sugar Confectionery Market?

The market is expected to witness sustained growth in the coming years. Rising consumer demand for premium and innovative sweet products across global markets would boost the growth. Rising penetration of online retail channels and increasing impulse purchasing through e-commerce platforms would strengthen product accessibility and brand reach. There is a growing popularity of gummies, functional candies, medicated confectionery, and novelty sweets. It is encouraging manufacturers to diversify product portfolios with health-oriented and experiential offerings. In addition, rising preference for sugar-free and low-calorie confectionery products will support market expansion among health-conscious consumers. This factor positions sugar confectionery as a continuously evolving segment within the global snacks and packaged food industry.

Source: Polaris Market Research Analysis

Segment Insights

Market Assessment by Product Type

Based on product type, the sugar confectionery market segmentation includes chewing gum, hard candy, soft candy, caramels & toffees, and others. The hard candy segment accounted 25.4% market share in 2025 owing to its extended shelf life, lower manufacturing cost, and high consumer preference across diverse age groups. Hard candies are particularly popular due to their wide flavor variety, ease of packaging, and suitability for impulse purchases. Their resistance to temperature fluctuations during transport and storage further enhances distribution efficiency. Brands leverage nostalgic appeal and traditional flavors to maintain a loyal customer base, while also experimenting with functional ingredients such as vitamins or herbal extracts to sustain demand. These attributes have helped hard candy dominate retail displays and retain a significant share.

The soft candy segment is expected to witness the highest CAGR during the forecast period due to its versatile texture, innovation in shapes and flavors, and rising popularity among younger demographics. Gummies, jellies, and marshmallows appeal strongly to consumers seeking indulgent and playful snack experiences. Increasing demand for gelatin-free and plant-based alternatives has also fueled product diversification in this segment. Brands are actively incorporating natural colors, fruit-based formulations, and even nutraceutical ingredients to align with evolving dietary preferences. Seasonal launches and limited-edition offerings, often promoted through digital campaigns, are further accelerating interest and expanding soft candy’s presence.

Market Evaluation by Distribution Channel

Based on distribution channel, the sugar confectionery market is segmented into supermarkets/hypermarkets, convenience stores, specialty stores, online retail, and others. Supermarkets/Hypermarkets held the largest market share of 42.6% in the Sugar Confectionery Market in 2025 due to its expansive shelf space, high product visibility, and the convenience of one-stop shopping. These retail formats provide an extensive selection of sugar confectionery products across various price points, flavors, and brands, often supported by in-store promotions and bundling offers. Consumers benefit from the ability to compare products directly, and the impulse-driven nature of candy purchases aligns well with the high foot traffic in these locations. Large-scale distribution networks and vendor partnerships allow supermarkets to maintain competitive pricing and continuously refresh inventory, making them the preferred destination for regular and bulk confectionery purchases.

The online retail segment is projected to register the highest CAGR of 5.4% during the projection period due to increasing digital penetration, changing consumer purchasing behavior, and the rise of direct-to-consumer confectionery brands. Personalized shopping experiences, subscription boxes, and access to exclusive or imported candy varieties attract younger, tech-savvy consumers seeking novelty. The convenience of doorstep delivery and promotional pricing through flash sales or seasonal campaigns enhances consumer engagement. Enhanced payment security, mobile-friendly interfaces, and integration with social media platforms further amplify reach and conversion. Smaller brands, particularly those offering artisanal or functional candies, leverage this channel to bypass traditional retail constraints and establish a loyal customer base.

Source: Polaris Market Research Analysis

Regional Analysis

By region, the study provides insights into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. Europe accounted 33.7% market share in 2025 due to strong consumer demand for traditional confections, well-established manufacturing infrastructure, and a deep-rooted cultural affinity for artisanal and premium candies. The presence of legacy brands with longstanding consumer loyalty, combined with innovation in organic and natural ingredient formulations, further sustains growth. Regulatory frameworks emphasizing quality and safety standards also support trust in local products, encouraging continued domestic and export sales across the region.

The North America sugar confectionery market is witnessing robust growth of 5.2% CAGR, driven by strong consumer demand for indulgent treats and ongoing innovation in flavor, texture, and packaging. The growth is supported by high brand loyalty, established retail infrastructure, and the proliferation of premium and seasonal product lines. Companies are leveraging advanced manufacturing processes to introduce reduced-sugar and functional variants that align with rising health consciousness. In August 2024, Ingredion launched a suite of sugar reduction solutions that can reduce sugar content by up to 50%, effectively addressing consumer concerns about the taste of lower-sugar products. Increased snacking frequency and preference for nostalgic, comfort-oriented products also contribute to sustained sales. E-commerce and omnichannel retail strategies have expanded consumer access, while sustainability trends are pushing brands to adopt eco-friendly packaging solutions. The region’s focus on high-quality ingredients, coupled with aggressive marketing and product differentiation, reinforces its leading position in the global sugar confectionery landscape.

The Asia Pacific sugar confectionery market is projected to register the fastest CAGR during the forecast period, driven by rising disposable incomes, rapid urbanization, and shifting dietary patterns among younger consumers. According to the India Brand Equity Foundation, India’s per capita disposable income was approximately USD 2,540 in 2023 and is projected to increase to USD 4,340 by 2029. Furthermore, demand for novelty flavors, culturally tailored products, and convenient on-the-go packaging is accelerating sales in key industries such as India, China, and Southeast Asia. The expansion of modern retail formats and rapid growth of e-commerce platforms enable broader product availability and brand visibility. Additionally, a surge in cross-border trade and exposure to Western confectionery trends through media and travel are influencing consumer preferences. Local manufacturers are capitalizing on these shifts by introducing innovative, affordable offerings tailored to regional tastes.

Source: Polaris Market Research Analysis

Key Players & Competitive Analysis Report

The competitive landscape of the sugar confectionery market is characterized by dynamic strategic movements, driven by evolving consumer preferences and increasing demand for innovative, clean-label products. Industry analysis reveals that players are pursuing expansion strategies, including regional diversification and portfolio enhancement, to capture emerging demographics and niche taste preferences. Strategic alliances and joint ventures are increasingly utilized to leverage distribution networks, share manufacturing capabilities, and localize flavor profiles.

Mergers and acquisitions are facilitating entry into segments such as organic candies, fortified sweets, and vegan alternatives, often followed by post-merger integration aimed at streamlining operations and consolidating brand equity. Technology advancements in ingredient processing and packaging are enabling the development of low-sugar, functional, and allergen-free variants aligned with health-conscious trends. Rapid product launches, supported by agile supply chains and data-driven consumer insights, are becoming essential for maintaining relevance in an increasingly saturated market. Marketing strategies often blend nostalgia with novelty, targeting both traditional buyers and younger, trend-driven consumers. Sustainability is also shaping competitive differentiation, with a focus on biodegradable packaging and ethical sourcing. As global confectionery demand becomes more segmented and experiential, competitors are intensifying R&D investments to balance indulgence, nutrition, and regulatory compliance across an increasingly digital and diversified retail environment.

Kerry Group is a food and ingredients company that produces various food and beverage ingredients, flavors, and consumer foods. The company's product line includes ingredients for the dairy, meat, bakery, beverage, and convenience food sectors. Kerry Group offers a variety of functional components, such as emulsifiers, stabilizers, and sweeteners, which are used to improve texture, flavor, and nutritional value in food products. The company also produces a range of natural and artificial flavors used in food and beverage applications.

Cargill is a global provider of food, ingredients, agricultural solutions, and industrial products, serving multiple sectors with a focus on safety, responsibility, and sustainability. The company's diverse product and service offerings span agriculture, animal nutrition, beauty, bio-industrial solutions, data asset solutions, food and beverage, food service, industrial applications, meat and poultry, pharmaceuticals, risk management, supplements, and transportation. In the agricultural sector, Cargill supplies grains, oilseeds, cotton, and palm oil, contributing to global food systems. Cargill is actively engaged in the sugar confectionery sector, offering innovative solutions for products such as gummies, jellies, lollipops, and more. The company focuses on creating enjoyable, plant-based, and healthier confectionery options, leveraging deep expertise and a broad ingredient portfolio to meet evolving consumer demands.

List of Key Companies in Sugar Confectionery Market

- Barry Callebaut

- Blommer Chocolate Company

- Cargill Inc.

- Ferrero

- Foley's Candies LP

- Kerry Group plc

- Mars, Incorporated

- Nestlé SA

- Olam Group

- PURATOS

- The Hershey Company

Sugar Confectionery Industry Developments

- May 2026: The Ferrero Group announced its plans to launch a new Wonka range to market, with a new collaboration with Netflix. It will launch with 10 seasonal and limited-edition products. The product will include chocolate, sugar confectionery, ice creams, and cereals. (Source: PRNewswire)

- June 2025: A new Nestlé Travel Retail dedicated space was launched by Ospree at Mumbai Duty Free Arrivals. Ospree stated that the area is designed to provide an exceptional experience for travelers. The new space will feature iconic brands such as Smarties, KitKat, and Nestlé Sustainably Sourced Cocoa. (Source: nestletravelretail.com)

- January 2025: Nestlé enhanced its US manufacturing by opening a beverage production facility in Arizona. This site employs advanced technologies to improve efficiency and quality, strengthening Nestlé’s regional supply chain. (Source: nestleusa.com)

- August 2024: Cargill launched a blending facility in Indonesia, aimed at enhancing the production of multi-sensory sugar confectionery products tailored for the Asia. This facility is designed to leverage advanced formulations and innovative processing techniques to create products that appeal to diverse consumer preferences across the region. (Source: cargill.com)

- May 2023: Barry Callebaut launched Callebaut NXT and SICAO Zero in Mexico, targeting Millennials and Centennials with dairy-free, low-sugar, and sustainable chocolate options. These products align with the growing demand for healthier and ethically sourced confections. (Source: barry-callebaut.com)

Sugar Confectionery Market Segmentation

By Product Type Outlook (Revenue, USD Billion, 2021–2034)

- Chewing Gum

- Hard Candy

- Soft Candy

- Caramels & Toffees

- Others

By Distribution Channel Outlook (Revenue, USD Billion, 2021–2034)

- Supermarkets/Hypermarkets

- Convenience Stores

- Specialty Stores

- Online Retail

- Others

By Nature of Product Outlook (Revenue, USD Billion, 2021–2034)

- Traditional Sugar-Based

- Sugar-Free/Low-Calorie

By Regional Outlook (Revenue, USD Billion, 2021–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Sugar Confectionery Market Report Scope

| Report Attributes | Details |

| Market Size Value in 2025 | USD 52.59 billion |

| Market Size Value in 2026 | USD 54.95 billion |

| Revenue Forecast by 2034 | USD 80.17 billion |

| CAGR | 4.8% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Sugar Confectionery Market FAQ's

The global market size was valued at USD 52.59 billion in 2025 and is projected to grow to USD 80.17 billion by 2034.

The global market is projected to register a CAGR of 4.8% during the forecast period.

Europe accounted 33.7% market share in 2025 due to strong consumer demand for traditional confections.

A few of the key players include Barry Callebaut; Blommer Chocolate Company; Cargill Inc.; Ferrero; Foley's Candies LP; Kerry Group plc; Mars, Incorporated; Nestlé SA; Olam Group; PURATOS; and The Hershey Company.

The hard candy segment accounted 25.4% market share in 2025 owing to its extended shelf life, lower manufacturing cost, and high consumer preference across diverse age groups.

The online retail segment is projected to register the highest CAGR of 5.4% during the projection period due to increasing digital penetration and changing consumer purchasing behavior.

Download Sample Report of Sugar Confectionery Market

Please fill out the form to request a customized copy of the research report.