U.S. Activated Carbon Market Demand, Industry Analysis, 2025-2034

REPORT DETAILS

REPORT DETAILS

Market Statistics

What is the Current Market Size?

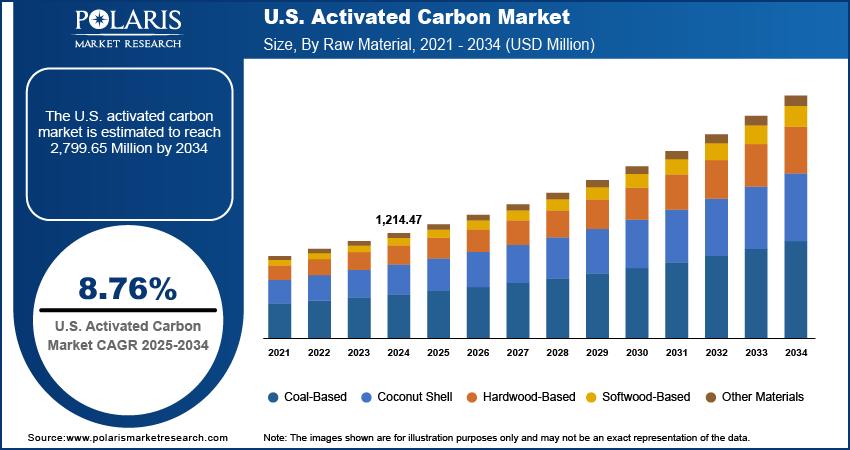

The global U.S. activated carbon market size was valued at USD 1,214.47 Million in 2024, growing at a CAGR of 8.8% from 2025–2034. Key factors driving demand for activated carbon include increasing industrial air pollution control requirements, technological advancements in activated carbon production, rising demand for water and wastewater treatment, and growth in food & beverage processing industry.

Key Insights

- The coal-based segment held 41.99% revenue share in 2024. This is due to their high pore volume and surface area, and they are good adsorbent for decontaminating several types of impurities in water treatment, air pollution control, and the removal of organic and inorganic chemicals.

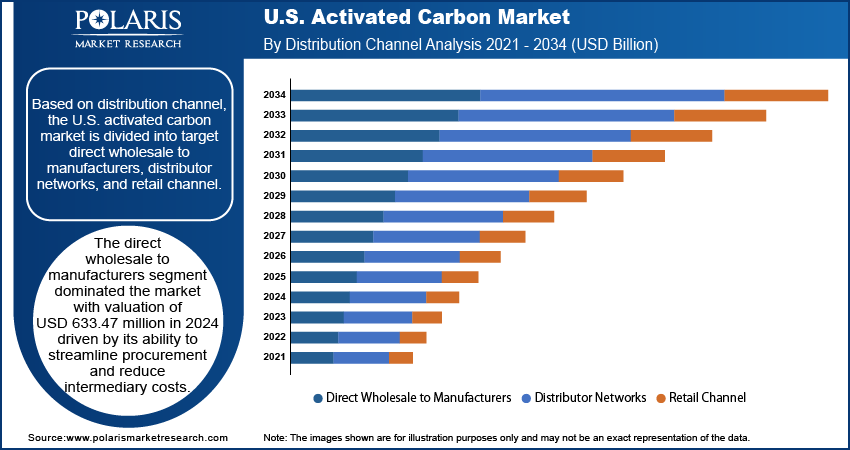

- The distributor networks segment is expected to witness the fastest growth at a CAGR of 9.1% during the forecast period. This is due to their technical support, multiple product grades, inventory to serve local markets better, and experience in customer service.

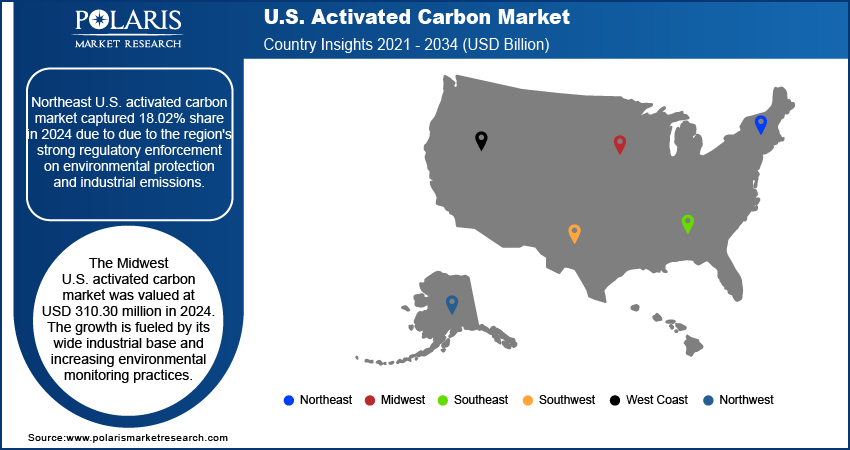

- Midwest U.S. activated carbon market accounted for 25.55% of market share in 2024. This is a diversified source of demand for activated carbon used in air emissions control, process filtration, and water treatment.

- The Southwest market is projected to grow at a CAGR of 9.6% from 2025 to 2034. This is due to the efficient use of resources and higher standards of treatment, leading to increased use of high-grade AC.

Industry Dynamics

- Rising demand for water and wastewater treatment drives the market growth

- Growth in the food & beverage processing industry boosts the demand.

- Supply chain disruptions affect raw material availability creates challenges.

- Water treatment and emerging environmental regulation create an opportunity to capitalize.

Market Statistics

- 2024 Market Size: USD 1,214.47 Million

- 2034 Projected Market Size: USD 2,799.65 Million

- CAGR (2025-2034): 8.8%

- Midwest: Largest market in 2024

AI Impact on the Industry

- Reduce operational cost and optimize production process.

- Enhance material science for advances on absorption capacities.

- Allow predictive maintenance to lower the supply chain disruptions.

- Customization of carbon solutions according to the specific industrial application.

What is included in the U.S. Activated Carbon Industry?

Activated carbon is a porey adsorbent material for purification and filtration, has a crucial role in the U.S. market. This is due to rising industry demand for environment-friendly operations and clean functioning. Increasing focus on industrial air pollution control requirements is one of the major factors fueling market growth. A 2024 EDGAR- Emissions Database for Global Atmospheric Research stated that, global GHG emissions reached 53.0 Gt CO2eq in 2023. Moreover, strict regulatory expectations in areas such as chemical, power generation, manufacturing have driven the demand for activated carbon to capture volatile organic compounds, odors, and other hazardous emissions. This regulatory-driven trend has helped expand the applicability of the material in more advanced filtration solutions. This makes it a critical proof-point as industrial users continue to pursue solutions that are effective, scalable and proven. Therefore, the continued focus on clean industrial processes and improvement in overall environmental performance are likely to keep activated carbon at the forefront, as the operating compliance frameworks evolve.

Technological evolution in production processes with improved performance and application possibilities has boosted the market growth. Improvement in the development of activation methods, raw materials usage and regeneration techniques allow the manufacture of greater capacity, more robust and specialized grades of carbon. These improvements enhance adsorption efficiency and further optimize cost-effectiveness for the end users. This enables them to consider activated carbon as a more feasible option in a wide range of applications such as water treatment, air treatment, and industrial processing. The technology-driven nature of the market is further expected to empower the emerging challenges in purification with greater accuracy and sustainability, meanwhile the advancement in production efficiency and product customization continues.

Drivers & Opportunities

What are the Factors Contributing for the Market Expansion?

Rising Demand for Water and Wastewater Treatment: Advancements in technology and performance of applications in the production process have led to the growth of the market. Serving over 80% of the population, the U.S. has approximately 152,000 public drinking water and wastewater systems. Advances in activation processes, raw materials and regeneration techniques enable the production of more advanced, higher capacity and more robust and application specific types of activated carbon. These modifications improve the efficiency of adsorption and also make the end users to realize more cost-effectiveness in the long run. This helps them to view activated carbon as a more viable solution across a wider variety of markets including water and wastewater treatment equipment, air treatment, and industrial application. The technology-led character of the market is likely to further subscribe to evolving purification challenges with more precision and sustainability, while production efficiency, and product customization, are expected to evolve further.

Growth in Food & Beverage Processing Industry: The market is being propelled by the growth in food & beverage processing industry. That adds to an industry that depends on intense filtration and purification to guarantee the quality and safety of its products. Activated carbon is also used for decoloration, deodorization and purification of sweeteners, beverages, edible oil & fats and other raw materials, including foodstuffs and additives. In February 2024, Pall Corporation launched the SUPRA AKS FB range that is designed for food and beverage processing. The new solution is food contact compliant with a higher adsorption capacity allowing manufacturers to have process efficiency and guarantee quality and compliance. Additionally, as producers raise their level of production and clean up their processing, the demand for special grades of activated carbon also grows. The need for consistency and purity within the industry, along with stringent safety requirements, ensures filtration media has a good penetration in this application. The continued desire to provide high quality purification solutions has allowed for the active material in carbon to be an essential element in achieving efficient and valuable products in the food and beverage industry.

Premium Insights- Strategic Overview of U.S. Activated Carbon Market: Government Initiatives and Corporate Expansions (2020-2025)

| U.S. scope | |

| Regulatory driver – drinking water | U.S. EPA identifies granular activated carbon (GAC) as a proven technology with very high removal efficiency (up to about 99.9%) for many volatile organic compounds in drinking water. |

| Treatment technology status | EPA lists GAC among standard treatment technologies for public water systems for control of disinfection by‑products (DBPs) and synthetic organic chemicals, under the Stage 1/2 DBP Rules. |

| Historic policy context | National Research Council evaluation for EPA notes GAC was proposed by EPA as the option of choice for controlling synthetic organic chemicals in drinking water, shaping long‑term demand. |

| Federal climate / carbon‑removal context | DOE Carbon Dioxide Removal (CDR) program and Carbon Negative Shot support development of sorbent‑based carbon capture and storage solutions, creating indirect pull for advanced activated carbons. |

| Trade & export promotion context | U.S. Commerce Department’s Environmental Technologies Trade Advisory Committee (ETTAC) flags opportunities for U.S. environmental technology companies, including air and water treatment, in export markets. |

| Corporate capacity expansion – Calgon | Calgon Carbon (Kuraray Group) expanded its Pearlington, Mississippi, plant with a second virgin activated carbon line, adding about 50 million lb/year and taking total virgin GAC capacity above 200 million lb/year, with completion targeted for late 2022. |

| Corporate investment scale – Calgon | The Pearlington expansion involved about USD 185 million in capital expenditure and is expected to add roughly 38 new jobs at the site, reinforcing U.S. production for air and water purification markets. |

| Technology positioning – water utilities | EPA and utility case studies identify GAC as a preferred option for controlling DBP precursors (e.g., THMs, HAAs) thanks to high effectiveness, integration with existing plants, and regulatory fit. |

Segmental Insights

Which Segments Boost the Overall Growth of the Market?

Raw Material Analysis

Based on raw material, the segmentation includes coal-based, coconut shell, hardwood-based, softwood-based, and other materials. The coal-based segment held 41.99% revenue share in 2024. This is due to its higher adsorption capacity and the industrial application which is widely used in industrial applications. Activated carbon derived from coal has a high pore volume and surface area, and is a good adsorbent for decontaminating several types of impurities in water treatment, air pollution control and in organic and inorganic chemicals. It is also driven by the availability to be used by manufacturers for creating large-scale purification systems dependent on activated carbon and further preference. Furthermore, coal-based grades have competitive pricing and they can be manufactured as granular or powdered products to meet different customer needs. The combination of high reliability and good general-purpose characteristics makes coal-based carbon a leading raw material category in the market.

Distribution Channel Analysis

In terms of distribution channel, the segmentation includes direct wholesale to manufacturers, distributor networks, and retail channels. The distributor networks segment is expected to witness the fastest growth at a CAGR of 9.1% during the forecast period. This is due to its function in increasing the availability of products to various commercial and industrial users. Distributors contribute to a more efficient supply chain by providing technical support, multiple grades of products, inventory to serve the local markets better and experience in dealing with customers. Sales channels are more structured, and so they serve to bridge the gap between manufacturers and small or regional buyers. Furthermore, in many cases the distributors also offer additional services such as bulk handling, tailored packaging and even recommendations related to the specific application, which can facilitate the customer adoption. This increasing focus on configuration and scalable delivery models will enable a huge growth in the market for this channel over the forecast period.

Regional Analysis

Which U.S. Regions Contributed to the Growth?

Midwest U.S. activated carbon market accounted for 25.55% of market share in 2024. This dominance is attributed to the established industrial activities and the application agriculture, water purification technology and more. Heavy industry in the Midwest also provides a major, diversified source of demand for air emissions control, process filtration and water treatment uses of activated carbon. The products are also available for the region’s developed production lines and an integrated supply chain. Moreover, activated carbon use is further reinforced by growing attention to cost efficiency and regulatory adherence in industrial activities. These aspects, combined, bring about a solid Midwest presence in the overall market.

Southwest U.S. Activated Carbon Market

The market in Southwest is projected to grow at a CAGR of 9.6% from 2025-2034, owing to the demand for purification products in the water, industrial, and environmental applications. Growing focus on efficient use of resources and higher standards of treatment is leading to an increased usage of high-grade AC. The diversification of industry in the region demands the use of filtration media to help ensure clean operations. Moreover, growing commercial and municipal infrastructure boost the demand for treatment solutions utilizing AC. This combination of operating requirements with regional growth provides a solid foundation for increasing demand for activated carbon in the Southwest.

Key Players & Competitive Analysis Report

A competitive analysis of the U.S. activated carbon industry reveals intense competition driven by technological advancement and sustainable value chains. Strategic alliances through mergers/acquisitions and/or investments will be pursued by many vendors to enhance their competitive positions and increase the range of products offered. Many experts have predicted that considerable revenue opportunities will eventually appear in new markets for companies involved in activated carbon product manufacture and distribution, as there are further environmental regulations imposed on these industries. Small to medium-sized companies must establish a well-defined market-entry strategy and have plentiful reliable competitive intelligence to effectively compete with larger companies and comprehend the latent demands from customers. Additionally, larger vendors are also utilizing joint ventures as a means to mitigate supply chain disruptions while capitalizing on growing opportunities. Therefore, by monitoring trends and events within the global economy, companies within the activated carbon industry should maintain a pulse on both their own industries’ businesses as well as the external factors affecting where raw materials are sourced, so that they can develop and implement long-term strategies to remain competitive in the future.

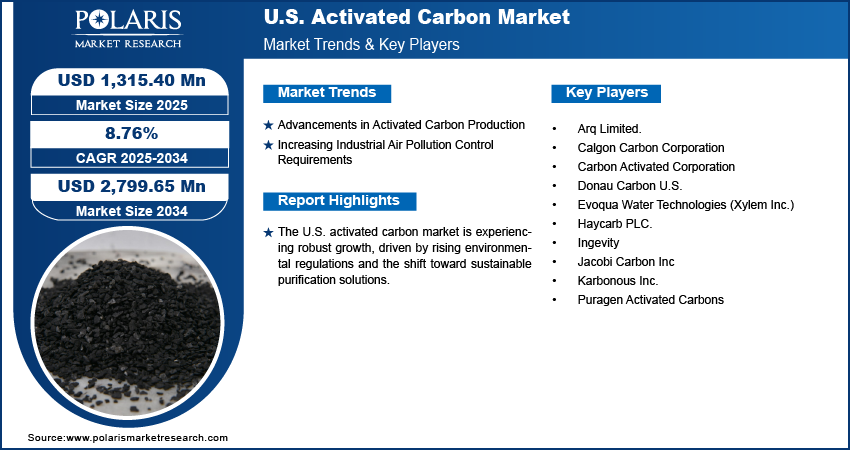

Major companies operating in the U.S. activated carbon industry include Arq Limited, Calgon Carbon Corporation, Carbon Activated Corporation, Donau Carbon U.S., Evoqua Water Technologies (Xylem Inc.), Haycarb PLC, Ingevity, Jacobi Carbon Inc, KarbonoU.S. Inc, and Puragen Activated Carbons.

Key Players

- Arq Limited.

- Calgon Carbon Corporation

- Carbon Activated Corporation.

- Donau Carbon U.S.

- Evoqua Water Technologies (Xylem Inc.)

- Haycarb PLC.

- Ingevity.

- Jacobi Carbon Inc.

- KarbonoU.S. Inc.

- Puragen Activated Carbons.

Industry Developments

August 2025: Arq, Inc. commissioned its first Granular Activated Carbon production line at the Red River Plant in Colorado, with its operations team actively optimizing processes to achieve the designated nameplate capacity.

January 2025: Calgon Carbon Corporation and American Water, the largest regulated water and wastewater utility company in the U.S., have collaborated for a nine-year exclusive supply contract for granular activated carbon, equipment, and reactivation services at more than 50 American Water sites in ten states.

December 2024: Xylem, a global water solutions firm, acquired Idrica, a water data management and analytics company. This acquisition is expected to provide water utilities with intelligent solutions to their most important difficulties.

May 2024: Kuraray Co., Ltd., a leading global producer of activated carbon, selected Calgon Carbon Corporation to assume control of the industrial reactivated carbon business previously operated by Sprint Environmental Services, LLC.

U.S. Activated Carbon Market Segmentation

By Raw Material Outlook (Volume, Ton, Revenue, USD Million, 2020–2034)

- Coal-Based

- Coconut Shell

- Hardwood-Based

- Softwood-Based

- Other Materials

By Distribution Channel Outlook (Volume, Ton, Revenue, USD Million, 2020–2034)

- Direct Wholesale to Manufacturers

- Distributor Networks

- Retail Channels

By End User Outlook (Volume, Ton, Revenue, USD Million, 2020–2034)

- Water Treatment

- Air & Gas Purification

- Food & Beverage Processing

- Pharmaceutical

- Mining & Metallurgy

- Automotive & Transportation

- Others

By Regional Outlook (Volume, Ton, Revenue, USD Million, 2020–2034)

- U.S.

- Northeast

- Midwest

- Southeast

- Southwest

- West Coast

- Northwest

U.S. Activated Carbon Market Report Scope

| Report Attributes | Details |

| Market Size in 2024 | USD 1,214.47 Million |

| Market Size in 2025 | USD 1,315.40 Million |

| Revenue Forecast by 2034 | USD 2,799.65 Million |

| CAGR | 8.8% from 2025 to 2034 |

| Base Year | 2024 |

| Historical Data | 2020–2023 |

| Forecast Period | 2025–2034 |

| Quantitative Units | Volume, Ton, Revenue in USD Million and CAGR from 2025 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report Customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

The global market size was valued at USD 1,214.47 Million in 2024 and is projected to grow to USD 2,799.65 Million by 2034.

The global market is projected to register a CAGR of 8.8% during the forecast period.

Midwest U.S. activated carbon market accounted for 25.55% of market share in 2024.

A few of the key players in the market are Arq Limited, Calgon Carbon Corporation, Carbon Activated Corporation, Donau Carbon U.S., Evoqua Water Technologies (Xylem Inc.), Haycarb PLC, Ingevity, Jacobi Carbon Inc, KarbonoU.S. Inc, and Puragen Activated Carbons.

The coal-based segment held 41.99% revenue share in 2024.

The distributor networks segment is expected to witness the fastest growth at a CAGR of 9.1% during the forecast period.

Download Sample Report of U.S. Activated Carbon Market

Please fill out the form to request a customized copy of the research report.