U.S. Medical Examination Lights Market Growth, Industry Analysis, 2025-2034

REPORT DETAILS

Market Statistics

Overview

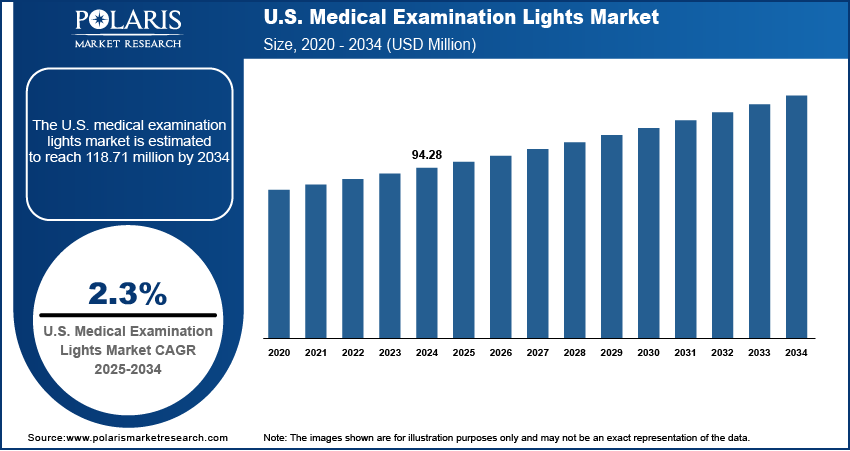

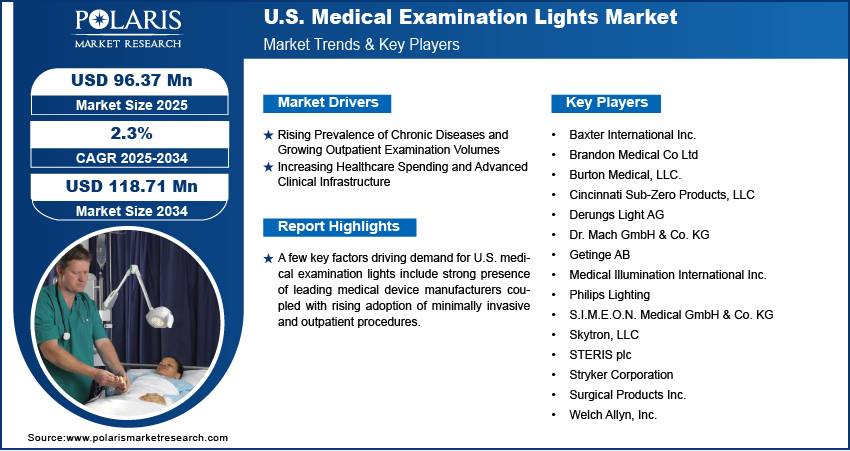

The U.S. medical examination lights market size was valued at USD 94.28 million in 2024, growing at a CAGR of 2.3% from 2025 to 2034. Key factors driving demand for U.S. Medical Examination Lights include rising prevalence of chronic diseases and growing outpatient examination volumes coupled with increasing healthcare spending and advanced clinical infrastructure.

Key Insights

- The LED examination lights segment held the largest market share in 2024, propelled by energy efficiency, extended lifespan, minimal heat output, and high-quality illumination.

- The general examination segment accounted for the highest share in 2024, driven by consistently high patient throughput in hospitals, outpatient centers, and specialized diagnostic facilities.

Industry Dynamics

- The growing prevalence of chronic diseases and rising outpatient examination volumes are boosting demand for advanced medical examination lighting solutions that enhance diagnostic precision and streamline clinical workflows.

- Increasing healthcare expenditure and the presence of sophisticated clinical infrastructure are supporting the adoption of state-of-the-art examination lights in hospitals, clinics, and specialty care centers.

- Integrating LED and laser-based illumination systems is creating market opportunities to improve brightness, color accuracy, energy efficiency, and customization for specific medical procedures.

- High purchase and maintenance costs of advanced examination lights remain a barrier to adoption in smaller clinics and healthcare facilities with limited resources.

Market Statistics

- 2024 Market Size: USD 94.28 Million

- 2034 Projected Market Size: USD 118.71 Million

- CAGR (2025–2034): 2.3%

Source: Polaris Market Research Analysis

To Understand More About this Research: Download Sample Report

AI Impact on U.S. Medical Examination Lights Market

- AI enhances performance optimization in U.S. medical examination lights by analyzing clinical workflows, lighting requirements, and room conditions to ensure consistent and efficient illumination.

- Integration of AI enables adaptive lighting control, dynamically adjusting intensity, color temperature, and beam focus based on examination type and clinician positioning.

- AI-powered diagnostics assist in early detection of LED degradation, electrical issues, or thermal irregularities, supporting predictive maintenance and extending equipment lifespan in U.S. healthcare settings.

- AI improves clinician interaction by enabling hands-free controls, auto-adjusting light angles, and real-time system feedback, boosting precision, hygiene, and workflow efficiency in U.S. medical practices.

The U.S. medical examination lights market comprises advanced lighting systems engineered to provide consistent, shadow-free, and high-intensity illumination for accurate visualization during medical examinations, minor surgical procedures, and diagnostic assessments. Innovations in LED lighting technology, adjustable color temperature, and ergonomic designs enhanced the efficiency, durability, and energy performance of these systems. Precise illumination helps improve diagnostic accuracy, minimizes eye strain for healthcare professionals, and supports enhanced patient care across hospitals, outpatient facilities, academic institutions, and specialized clinics throughout the U.S.

The adoption of medical examination lights in the U.S. is accelerating due to the strong presence of leading medical device manufacturers, which is driving the availability and deployment of innovative lighting systems. These advanced solutions feature high-intensity LED illumination, adjustable color temperature, shadow reduction, and ergonomic designs that enhance visibility, reduce eye strain, and improve procedural efficiency. Continuous product development and strategic partnerships between manufacturers and healthcare providers are expanding the reach of these systems, supporting accurate diagnostics and optimized patient care throughout the country.

The rising adoption of minimally invasive and outpatient procedures is further fueling demand for specialized medical examination lighting solutions in the U.S. According to the American Society of Plastic Surgeons (ASPS) 2023 Procedural Statistics, plastic surgeries increased by 5% and minimally invasive procedures rose by 7% compared to the previous year, highlighting the growing need for precise, shadow-free illumination in surgical and diagnostic settings. Hospitals and outpatient centers are increasingly implementing LED-based examination lights with enhanced ergonomics and adjustable intensity to ensure accurate visualization, improve procedural efficiency, and support better patient outcomes.

Drivers & Opportunities

Rising Prevalence of Chronic Diseases and Growing Outpatient Examination Volumes: The increasing number of chronic diseases and lifestyle-related conditions in the U.S. is driving demand for advanced medical examination lights. According to the U.S. Centers for Disease Control and Prevention, nearly 6 in 10 Americans live with at least one chronic condition, while 4 in 10 are affected by two or more, necessitating frequent diagnostic evaluations and minor procedures. High patient examination volumes require reliable, shadow-free, and high-intensity illumination to ensure accurate diagnosis and effective treatment, supporting improved clinical outcomes and patient safety.

Increasing Healthcare Spending and Advanced Clinical Infrastructure: The presence of a well-established healthcare infrastructure and surging healthcare spending is boosting the adoption of technologically advanced examination lighting systems. According to the Centers for Medicare & Medicaid Services (CMS), national health expenditures in the U.S. are projected to reach USD 7.2 trillion by 2031, driven by investments in innovative medical equipment, clinical workflow optimization, and patient safety initiatives. Hospitals, outpatient centers, and academic institutions are increasingly integrating LED-based, adjustable color temperature, and ergonomic lighting solutions to enhance diagnostic accuracy, reduce eye strain for medical professionals, and streamline clinical operations, thereby fueling growth in the U.S. Medical Examination Lights market.

Source: Polaris Market Research Analysis

To Understand More About this Research: Download Sample Report

Segmental Insights

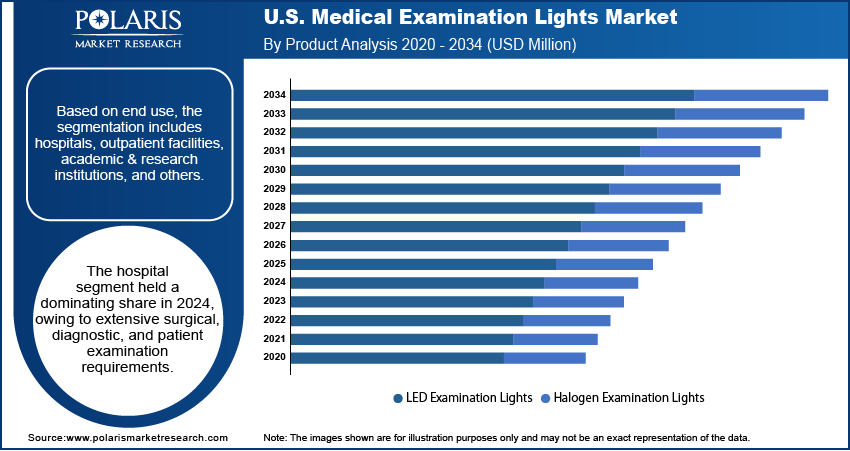

By Product

Based on product, the U.S. medical examination lights market is segmented into LED examination lights and halogen examination lights. The LED examination lights segment held the largest share in 2024, driven by factors such as energy efficiency, long operational lifespan, low heat emission, and superior illumination quality. Healthcare providers are increasingly deploying LED systems equipped with adjustable color temperature, shadow reduction, and dimming features to enhance diagnostic accuracy and improve patient comfort during general, dental, and minor surgical examinations.

Halogen examination lights are expected to experience the fastest growth during the forecast period. Their high-intensity illumination and precise light focus make them suitable for specialized diagnostic procedures, minor surgeries, and dental or ENT devices applications. Advances in energy efficiency, compact design, and portability are further supporting broader adoption across hospitals, outpatient centers, and specialty clinics.

By Mounting

Based on mounting, the market is classified into wall-mounted, ceiling-mounted, mobile/floor-standing, head lights/lamps/clamp-on, and combination systems. Wall-mounted systems accounted for the largest share in 2024, driven by stable and secure installation, optimal space utilization, and suitability for operating rooms, outpatient examination rooms, specialty clinics, and diagnostic centers.

Ceiling-mounted lights are projected to grow significantly during the forecast period, driven by their flexible positioning, superior shadow reduction, and adaptability in high-volume surgical, diagnostic, and procedural settings. These lights enable consistent, high-quality illumination, improving visibility and precision for healthcare professionals. Their integration into modern healthcare facilities supports enhanced workflow efficiency, reduced procedure times, and improved patient outcomes. Demand is further supported by advancements in lighting technology, energy efficiency, and ergonomic designs, making them suitable for a wide range of clinical environments.

By Application

Based on application, the market is divided into general examination, gynecological examination, dental examination, ENT examination, dermatology, and others. General examination held the largest share in 2024, driven by consistently high patient volumes across hospitals, outpatient clinics, and specialty diagnostic facilities requiring precise illumination for accurate and efficient assessments.

Gynecological and dental applications are projected to register the highest CAGR during the forecast period, fueled by the growing number of outpatient procedures, preventive care initiatives, and adoption of minimally invasive treatments. Increasing patient awareness regarding healthcare quality standards and early diagnosis is further boosting demand. These applications require highly accurate, shadow-free illumination to support precision during procedures. Advancements in examination light designs, including improved brightness, adjustable color temperature and energy-efficient LED systems is driving the segment growth.

By End-Use

Based on end-use, the market is segmented into hospitals, outpatient facilities, academic & research institutions, and others. Hospitals accounted for the largest share in 2024, driven by high surgical, diagnostic, and patient examination volumes and continued investment in modern, high-performance, and energy-efficient lighting systems.

Outpatient facilities are expected to record the fastest growth over the forecast period, driven by the rising number of outpatient procedures, diagnostic services, primary care visits, and specialized consultations. These settings require precise, reliable, and ergonomically designed illumination systems to support accurate diagnostics and efficient treatment delivery. Growing preference for outpatient care due to lower costs, reduced hospital stays, and improved patient convenience is encouraging facility upgrades.

Source: Polaris Market Research Analysis

To Understand More About this Research: Request Customization

Key Players & Competitive Analysis

The U.S. medical examination lights market is highly competitive, with prominent players such as Baxter International Inc., Brandon Medical Co Ltd, Burton Medical, LLC, Cincinnati Sub-Zero Products, LLC, Derungs Light AG, Dr. Mach GmbH & Co. KG, Getinge AB, Medical Illumination International Inc., Philips Lighting, S.I.M.E.O.N. Medical GmbH & Co. KG, Skytron, LLC, STERIS plc, Stryker Corporation, Surgical Products Inc., and Welch Allyn, Inc. shaping the industry through innovative lighting solutions, advanced technology integration, and extensive distribution networks. Baxter International Inc. focuses on delivering high-performance examination lights with precise illumination and ergonomic designs to enhance procedural accuracy, while Brandon Medical Co Ltd, Burton Medical, LLC, and Cincinnati Sub-Zero Products, LLC emphasize research-driven development, providing comprehensive solutions for surgical, diagnostic, and outpatient care settings.

The market is witnessing increasing adoption of LED, halogen, and hybrid examination lights across hospitals, outpatient facilities, and academic institutions to optimize clinician performance, improve procedural accuracy, and ensure patient safety. Companies are investing in next-generation ceiling-mounted and mobile systems, head lamps, and combination lighting solutions that provide uniform illumination, minimize shadows, and support diverse clinical applications. Strategic partnerships and collaborations with hospital networks, healthcare providers, and diagnostic equipment manufacturers are expanding product reach and enhancing technological capabilities across the U.S., driving overall market growth.

Prominent companies in the U.S. Medical Examination Lights market include Baxter International Inc., Brandon Medical Co Ltd, Burton Medical, LLC, Cincinnati Sub-Zero Products, LLC, Derungs Light AG, Dr. Mach GmbH & Co. KG, Getinge AB, Medical Illumination International Inc., Philips Lighting, S.I.M.E.O.N. Medical GmbH & Co. KG, Skytron, LLC, STERIS plc, Stryker Corporation, Surgical Products Inc., and Welch Allyn, Inc.

Key Players

- Baxter International Inc.

- Brandon Medical Co Ltd

- Burton Medical, LLC.

- Cincinnati Sub-Zero Products, LLC

- Derungs Light AG

- Dr. Mach GmbH & Co. KG

- Getinge AB

- Medical Illumination International Inc.

- Philips Lighting

- S.I.M.E.O.N. Medical GmbH & Co. KG

- Skytron, LLC

- STERIS plc

- Stryker Corporation

- Surgical Products Inc.

- Welch Allyn, Inc.

Recent Developments:

In September 2024, S.I.M.E.O.N. Medical GmbH & Co. KG introduced its newest advancement in clinical lighting solutions—the Sim.LED 3000 series examination lights. The updated lineup features two sophisticated variants: the Sim.LED 3000 F, which provides adjustable field sizing, and the Sim.LED 3000 MC, designed with customizable color temperature settings.

In August 2024, Stryker strengthened its collaboration with the Dr. Lorna Breen Heroes’ Foundation to enhance clinician well-being by combating burnout, lowering mental health stigma, and promoting meaningful systemic improvements within healthcare environments. As a Signature Partner of the Foundation’s “ALL IN: Caring for Caregivers” initiative, Stryker contributes to programs that encourage safer and more supportive workplaces for healthcare professionals throughout the United States.

U.S. Medical Examination Lights Market Segmentation

By Product Outlook (Revenue, USD Million, 2020–2034)

- LED Examination Lights

- Halogen Examination Lights

By Mounting Outlook (Revenue, USD Million, 2020–2034)

- Wall-Mounted

- Ceiling-Mounted

- Mobile/Floor-Standing

- Head Lights / Lamps / Clamp-On

- Combination

By Application Outlook (Revenue, USD Million, 2020–2034)

- General Examination

- Gynecological Examination

- Dental Examination

- ENT Examination

- Dermatology

- Others

By End Use Outlook (Revenue, USD Million, 2020–2034)

- Hospitals

- Outpatient Facilities

- Academic & Research Institutions

- Others

U.S. Medical Examination Lights Market Report Scope

| Report Attributes | Details |

| Market Size in 2024 | USD 94.28 Million |

| Market Size in 2025 | USD 96.37 Million |

| Revenue Forecast by 2034 | USD 118.71 Million |

| CAGR | 2.3% from 2025 to 2034 |

| Base Year | 2024 |

| Historical Data | 2020–2023 |

| Forecast Period | 2025–2034 |

| Quantitative Units | Revenue in USD Million and CAGR from 2025 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, and segmentation. |

Source: Polaris Market Research Analysis

FAQ's

The market size was valued at USD 94.28 million in 2024 and is projected to grow to USD 118.71 million by 2034.

The market is projected to register a CAGR of 2.3% during the forecast period

A few of the key players in the market are Baxter International Inc., Brandon Medical Co Ltd, Burton Medical, LLC, Cincinnati Sub-Zero Products, LLC, Derungs Light AG, Dr. Mach GmbH & Co. KG, Getinge AB, Medical Illumination International Inc., Philips Lighting, S.I.M.E.O.N. Medical GmbH & Co. KG, Skytron, LLC, STERIS plc, Stryker Corporation, Surgical Products Inc., and Welch Allyn, Inc.

The LED examination lights segment dominated the market revenue share in 2024.

The ceiling-mounted lights segment is projected to witness the fastest growth during the forecast period.

Download Sample Report of U.S. Medical Examination Lights Market

Please fill out the form to request a customized copy of the research report.