ENT Devices Market Size, Share, Trends and Forecast, 2026-2034

REPORT DETAILS

ENT Devices Market Overview and Key Insights

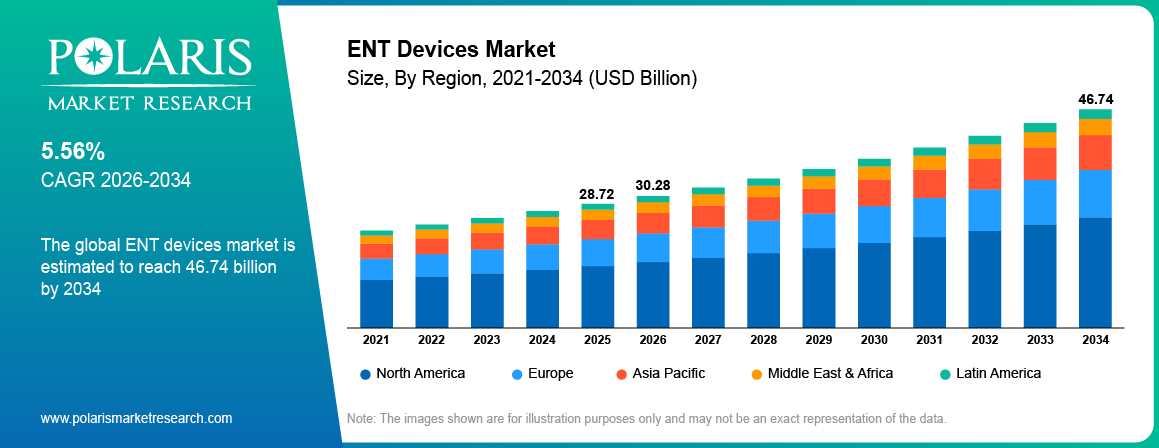

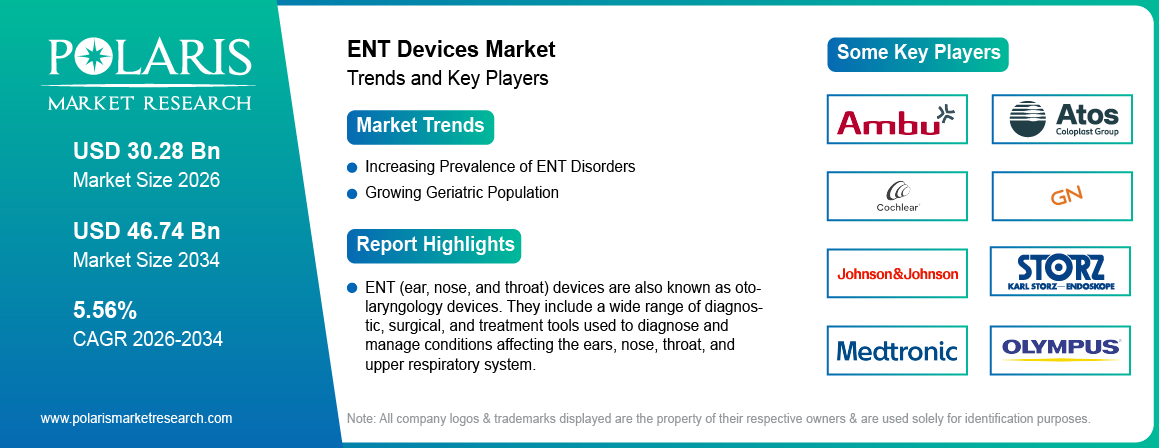

The global ear, nose, and throat (ENT) devices market size was valued at USD 28.72 billion in 2025, growing at a CAGR of 5.56% from 2026 to 2034. The growing number of ENT cases, an aging population, new technologies, and increased healthcare investments are driving market growth.

Market Statistics

ENT Devices Market Key Takeaways

- North America had the largest ENT devices market share of 37.80% in 2025. The regional market dominance is attributed to its well-developed healthcare infrastructure and early adoption of new medical technologies.

- Asia Pacific is projected to maintain the fastest growth rate of 6.24% during the forecast period. The regional market growth is driven by enhanced healthcare availability, rising spending, and increased patient awareness.

- In 2025, the hearing aids segment dominated the ENT devices market with 30.50% share. This is due to the rising prevalence of hearing loss. Hearing aid technologies are also being adopted across all age groups.

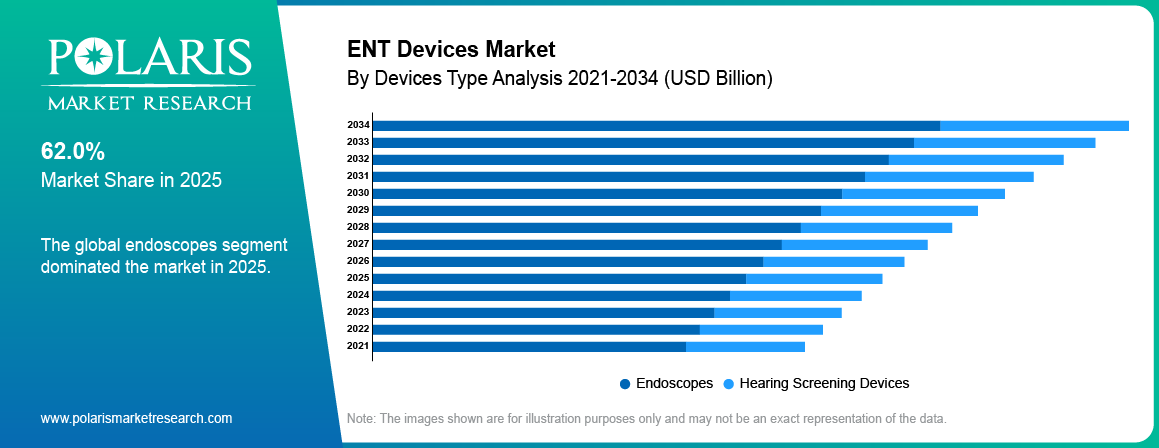

- The endoscopes segment held 62.0% share in 2025, as it can enhance the effectiveness of ENT examinations and procedures.

Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations.

Industry Dynamics

- Ongoing investments in the upgradation of healthcare centers and the installation of innovative equipment in ENT departments are driving expansion.

- Early diagnosis initiatives and the rising integration of ENT diagnostics services into primary healthcare systems are strengthening demand for ENT diagnostic and treatment devices.

- The rising ENT disorder prevalence is driving demand for diagnostic and treatment solutions, thereby propelling the market.

- The growing geriatric population underscores the need for ENT devices. This is because the geriatric population accounts for a large share of patients with ENT disorders.

- Lack of awareness in certain geographic regions and the very high prices of hi-tech ENT products act as barriers to the widespread acceptance of ENT devices.

Impact of Artificial Intelligence on the ENT Devices Market

- Increased accuracy in diagnostics: It is possible to analyze test results and images using AI. In this way, it assists a doctor in diagnosing hearing and sinus issues more accurately.

- Personalized treatment options: AI enables more personalized hearing aids and ENT products. It does so because AI adjusts settings according to patient needs.

- Easier and more efficient procedures: AI tools and systems make surgical procedures more precise. This directly aids in minimizing the time of procedures.

- Enhanced patient monitoring: AI-powered ENT devices are capable of monitoring patient progress over a period and triggering an alert in the doctor in case any modifications are required.

Source: Polaris Market Research Analysis

What Are ENT Devices and How Are They Used?

ENT (ear, nose, and throat) devices are also known as otolaryngology devices. They include a wide range of diagnostic, surgical, and treatment tools used to diagnose and manage conditions affecting the ears, nose, throat, and upper respiratory system. These devices include hearing aids, hearing implants, endoscopes, powered surgical tools, image-guided navigation systems, and ENT consumables. The ENT devices market is important in treating the growing number of people with hearing loss, chronic sinus problems, sleep apnea, and voice disorders, making it a key part of the overall ENT medical devices market.

ENT Devices vs. Traditional Treatment Methods: Key Differences

| Parameter | ENT Devices | Traditional Treatment Methods |

| Primary Method | Device-based diagnosis and intervention | Medication and conservative therapy |

| Treatment Precision | High | Moderate |

| Best for | Chronic or severe ENT disorders | Mild and temporary conditions |

| Invasiveness | Minimally invasive to surgical | Non-invasive |

| Cost | Higher upfront cost | Lower initial cost |

| Long-Term Outcome | Often more durable and effective | May require continuous treatment |

Source: Polaris Market Research Analysis

The ENT devices market is showing steady growth. It is mainly due to advances in minimally invasive ENT procedures and digital ENT technologies. In February 2025, GN introduced ReSound Vivia, the world’s smallest AI-powered hearing aid. The hearing aid uses Intelligent Focus and a DNN chip trained on 13.5 million speech samples. The company also launched ReSound Savi, an essentials-range model that supports Bluetooth LE Audio and Auracast. Innovations have helped improve treatment efficiency and shorten recovery times. They also deliver better patient outcomes. Technologies such as image-guided ENT surgery systems, video endoscopes, and robotic-assisted procedures are changing how ENT care is delivered. These technologies are improving precision and reducing tissue damage during procedures. In addition, the growing shift toward outpatient and day-care surgeries is increasing demand for advanced ENT devices.

The growth of the ENT devices market is driven by rising healthcare spending and infrastructure development, particularly in emerging countries. An April 2025 report by the IBEF stated that the Indian Union Budget for 2025-26 allotted USD 11.50 billion to the healthcare sector. This was a 9.78% increase from the previous allocation. Higher funding for the healthcare sector has facilitated the adoption of advanced diagnostic and ENT equipment. Infrastructure development has also enhanced access to specialized ENT facilities, particularly in the least developed areas. In addition, various governments and healthcare service providers are focusing more on modernizing hospitals and clinics, upgrading their ENT departments with advanced tools. Further government investments in healthcare systems will spur demand for innovative ENT devices and help the market expand.

ENT Devices Market Dynamics

Rising Prevalence of Hearing, Sinus and Throat Disorders

The incidence of ENT ailments is steadily increasing, thereby fueling demand for diagnostic services and treatment devices. This could be attributed to the rising cases of sinusitis, ear infections, hearing impairments, and voice pathologies that are being witnessed due to rising pollution, lifestyle changes, and the growing rates of allergy and infectious diseases. According to a January 2025 CDC report, about 2–3 out of every 1,000 children in the U.S. are born with detectable hearing loss. More than 98% of newborns receive hearing screenings, and over 6,000 infants were identified with hearing loss in 2022. This growing burden of ENT-related conditions increases the need for timely diagnosis and effective treatment. It encourages the use of advanced ENT devices across healthcare facilities. As awareness of early diagnosis and specialist care continues to rise, both patients and healthcare providers are increasingly adopting technology-driven ENT tools.

Growing Geriatric Population and Age-related Hearing Loss

The steady increase in the geriatric population is driving growth in the ENT devices market, as there is a strong association between advancing age and ENT-related health conditions. The elderly population is prone to health conditions such as presbycusis (age-related hearing impairment), balance disorders, and voice disorders, which need constant surveillance and treatment. A WHO report, released in October 2024, estimated that the population of 60 years and over might increase from 1 billion in 2020 to 1.4 billion in 2030 and double to 2.1 billion in 2050. The population of people aged 80+ might triple to 426 million over the same period. There is greater reliance on ENT devices for diagnostic and rehabilitative care owing to sensory function decay with advancing age. Also, this demographic tends to seek care and undergo procedures that improve their quality of life, thereby contributing to sustained demand for specialized care related to their health conditions. This demand is currently addressed through specialized solutions for their specific health-related needs related to ENT disorders.

Source: Polaris Market Research Analysis

ENT Devices Market Segment Analysis

ENT Devices Market, by Product

The ENT product segmentation includes diagnostic devices, surgical devices, hearing aids, hearing implants, CO2 lasers, and image-guided surgery systems. The hearing aids segment led the ENT devices market with 30.50% share in 2025. This is due to the rising prevalence of hearing loss and the growing adoption of hearing assistance technologies across all age groups. Hearing aids are commonly used as a first-line option for managing mild to moderate hearing impairment. Hearing impairments are increasingly being diagnosed due to enhanced awareness and accessibility to audiology devices. At the same time, technological progress has made modern hearing aids more appealing to users. Features such as Bluetooth connectivity, noise reduction, and longer battery life have improved ease of use. In addition, rising emphasis on maintaining quality of life in later years continues to drive the demand for hearing aids.

In addition to the development in the field of hearing aids, there is also a growing use of implantable hearing equipment, such as cochlear and bone-anchored devices. This has broadened the treatment choices offered to patients with severe or profound deafness. At the same time, there is an increasing adoption of image-guided surgery systems and CO2 lasers in rather sophisticated ENT surgeries, where the demands for precision and minimizing tissue effect are extremely vital.

Diagnostic vs. Surgical ENT Devices: Product and Use-case Comparison

| Parameter | Diagnostic ENT Devices | Surgical ENT Devices |

| Purpose | Detect and evaluate ENT disorders | Treat and correct ENT conditions |

| Common Usage | Hearing tests, imaging, and endoscopy | Sinus surgery, cochlear implants, and tissue removal |

| Invasiveness | Non-invasive or minimally invasive | Minimally invasive to invasive |

| Treatment Role | Supports diagnosis and monitoring | Enables therapeutic and surgical intervention |

| Examples | Audiometers, otoscopes, and nasal endoscopes | Powered surgical instruments, lasers, and navigation systems |

| Operating Environment | Clinics and diagnostic centers | Hospitals and surgical settings |

Source: Polaris Market Research Analysis

Market Evaluation by Diagnostic Devices Type

The global ENT devices market segmentation, based on diagnostic devices type, includes endoscopes, and hearing screening devices. Among these, endoscopes dominated the market in 2025 with 62.0% share, driven by their ability to improve the accuracy and efficiency of ENT examinations and procedures. Endoscopic imaging enables clinicians to closely examine internal ear, nose, and throat structures with high precision, supporting earlier diagnosis and minimally invasive surgery. Continuous advancements in imaging clarity, ergonomics, and flexibility have made endoscopes a critical tool in both outpatient and surgical settings. The rising demand for precise and less invasive diagnostic procedures is accelerating the use of ENT diagnostic devices across both developed and emerging healthcare markets.

Source: Polaris Market Research Analysis

ENT Devices Market Regional Analysis

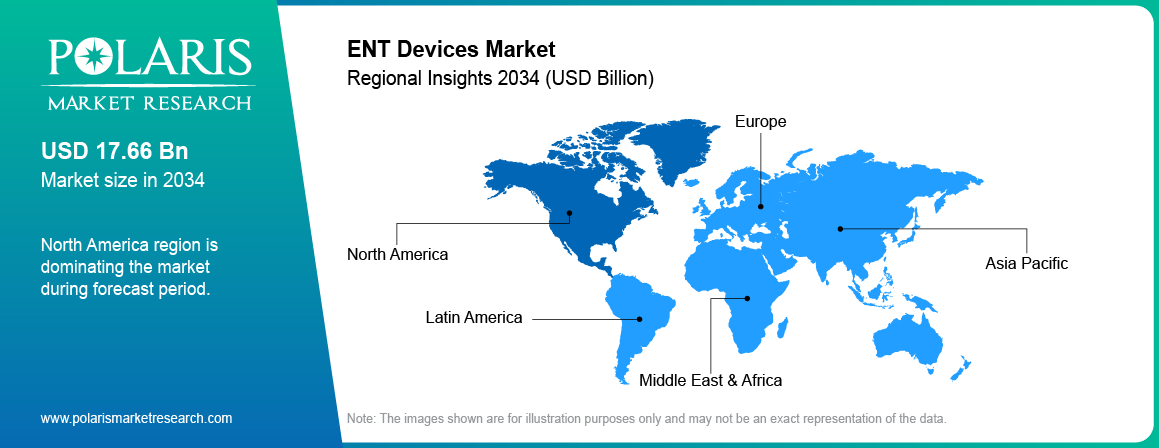

By region, the ENT devices market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa. North America accounted for the largest market share of 37.80% in the year 2025, and this is due to the well-developed healthcare infrastructure, awareness of ENT conditions, and early adoption of the latest technologies. There is a robust infrastructure of ENT specialists, payment support, and R&D investment in this region. In March 2025, for instance, Cochlear and GN renewed their collaboration on R&D innovation within the framework of the Smart Hearing Alliance, aiming for better bimodal solutions through AI and deep neural networking for better connectivity between devices and hearing experiences. Furthermore, the large number of ENT disorders, especially age-related hearing impairments, remains a contributing factor in maintaining the demand for diagnostic and treatment equipment in the market. Moreover, the presence of key competitors and a favorable government policy framework in the region has resulted in making North America a major contributor to the ENT devices market worldwide.

The Asia Pacific market is projected to witness the fastest growth at a CAGR of 6.24%, during the forecast period due to better access to healthcare, rising healthcare expenditure, and growing patient education. As per a report published in July 2024 from the Ministry of Finance, Government of India, the country's healthcare expenditure was USD 70.5 billion, up from 1.4 percent of its share in FY2017-18 to 1.9 percent in FY 2023-24. Governments in the region have been making investments in the development of medical infrastructure, particularly in the urban as well as semi-urban areas, resulting in an improved availability of advanced services in the field of ENT. In addition, due to the rise in ENT diseases, an ageing population, and the adoption of technology, there is an increasing demand for these services. Encouraging government efforts regarding increased accessibility to ENT care, insurance coverage, and early screening programs are driving the ENT devices market in the Asia Pacific. With a vast population of underserved communities and the emerging trend of the use of affordable ENT diagnostic tools, the Asia Pacific market represents a huge growth opportunity for both international and local players.

Source: Polaris Market Research Analysis

ENT Devices Market Competitive Landscape

The ENT devices market competitive landscape includes a combination of large multinational medical device companies and specialized ENT technology providers. The key players differentiate themselves in terms of product lines that range comprehensively across the ENT sector, innovation in these technologies, collaboration in clinical settings, and the reach of these solutions geographically. Newer companies are focusing on niche applications and cost-effective solutions to build their presence in the market.

The ENT devices sector demonstrates robust structural dynamics. It is characterized by strategic mergers among major players, such as Medtronic, Karl Storz, and Olympus Corporation. Industry analysis indicates noteworthy technological advancements in minimally invasive diagnostic and surgical platforms, driving competitive differentiation across business segments encompassing rhinology, otology, and laryngology. Leading players are increasingly partnering with healthcare providers to launch broader product lines to cater to diverse healthcare needs. Digital transformation and the role of AI-based image and navigation systems are emerging as key differentiators in higher-end procedures. Penetration of the emerging Asia Pacific region is a key thrust area for established players to capitalize on unserved and underserved healthcare needs amid the developing healthcare infrastructure.

Looking forward, new directions for growth are increasingly focused on integrating medical devices and hospital information systems, and increasingly shifting towards value-based healthcare delivery. Innovation trends in the ENT devices market are evolving. There is a growing trend in single-use devices and remote monitoring solutions in postoperative care. Small firms are looking at opportunities in niches of innovative solutions in therapeutic areas. An increasing number of mergers and acquisitions suggests a trend of consolidation in this industry.

A few key major players are Ambu A/S; Atos Medical AB; Cochlear Limited; Demant A/S; GN Store Nord A/S; Johnson & Johnson Services, Inc.; KARL STORZ GmbH & Co. KG; Medtronic plc; Olympus Corporation; Pentax of America, Inc.; Rion Co., Ltd.; Siemens Healthineers AG; Smith & Nephew plc; Sonova Holding AG; and Stryker Corporation.

Medtronic plc is a leader in the development and manufacturing of advanced ENT devices. It provides a portfolio of over 5,000 products in its surgical solutions business in the area of sinus surgery, otology, neurotology, and base of the skull surgical approaches. In its ENT business, it provides diagnostic devices such as endoscopes and hearing screening devices, and it offers ENT surgical devices such as powered surgical devices, radiofrequency handpieces, balloon sinus dilation devices, and voice prosthesis. Medtronic's aim is to provide solutions that are "minimally invasive, improve patient outcomes, reduce recovery times, and increase procedural precision." It also has image-guided surgery solutions and biomaterial products for nasal and ear packing. Its competitive edge in the market for ENT products lies in innovation, the integration of new technologies, and the ability to address multiple patient requirements for the treatment of sinusitis, hearing loss, and sleep apnea.

Atos Medical AB primarily operates in the development and marketing of ENT (ear, nose, and throat) medical devices, with a key focus on enhancing the lives of people with a neck stoma post laryngectomy and tracheostomy procedures. Established in 1986 in Sweden, the organization has emerged as a key player in neck stoma care. It offers voice and pulmonary rehabilitation to assist patients with breathing, speaking, and living with ease. Its main Provox product line consists of voice prostheses, heat and moisture exchangers (HME), and adhesives. These product types contribute to the rehabilitation of speech function as well as respiratory function in patients who have undergone the total laryngectomy procedure. There are other products known as Provox ActiValve, Provox Vega, and Provox FreeHands FlexiVoice, which are aimed at addressing a particular demand in the market. Its Freevent line is evidence of its expertise not only in laryngectomy but also in tracheostomy care. Atos Medical prioritizes clinical research, education, and ongoing product development in collaboration with ENT specialists and patients. It ensures that its solutions are evidence-based and user-friendly. Today, it is a subsidiary of Coloplast A/S and operates in over 90 countries. Atos is also known for placing strong emphasis on innovation and patient focus in the ENT sector.

Leading ENT Device Companies and Manufacturers

- Ambu A/S

- Atos Medical AB

- Cochlear Limited

- Demant A/S

- GN Store Nord A/S

- Johnson & Johnson Services, Inc.

- KARL STORZ GmbH & Co. KG

- Medtronic plc

- Olympus Corporation

- Pentax of America, Inc.

- Rion Co., Ltd.

- Siemens Healthineers AG

- Smith & Nephew plc

- Sonova Holding AG

- Stryker Corporation

ENT Devices Market Recent Developments

March 2026: Medtronic announced that it had received U.S. Food and Drug Administration (FDA) clearance of the Stealth AXiS. It is a surgical system for cranial and ENT procedures. (Source: medtronic.com)

March 2025: Ear Solutions partnered with Audientes to launch the world’s first self-fitting digital hearing aid, Ven. According to Ear Solutions, the partnership will leverage its distribution network in India. It aims to expand access to hearing care for millions. (Source: earsolutions.com)

ENT Devices Market Segmentation and Forecast

By Product Outlook (Revenue, USD Billion, 2021–2034)

- Diagnostic Devices

- Surgical Devices

- Hearing Aids

- Hearing Implants

- CO2 Lasers

- Image-Guided Surgery Systems

By Diagnostic Devices Type Outlook (Revenue, USD Billion, 2021–2034)

- Endoscopes

- Hearing Screening Devices

By Surgical Devices Type Outlook (Revenue, USD Billion, 2021–2034)

- Powered Surgical Instruments

- Radiofrequency (RF) Hand pieces

- Handheld Instruments

- Balloon Sinus Dilation Devices

- ENT Supplies

- Ear Tubes

- Voice Prosthesis Devices

By End User Outlook (Revenue, USD Billion, 2021–2034)

- Hospitals and Clinics

- Homecare

- Ambulatory Centers

- Others

By Regional Outlook (Revenue – USD Billion, 2021–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

ENT Devices Market Report Scope and Methodology

| Report Attributes | Details |

| Market Size in 2025 | USD 28.72 billion |

| Market Size in 2026 | USD 30.28 billion |

| Revenue Forecast by 2034 | USD 46.74 billion |

| CAGR | 5.56% |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD billion, 2021–2034 and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape | ENT Devices Industry Trend Analysis (2025) Company profiles/industry participants profiling include company overview, financial information, product/service benchmarking, and recent developments |

| Report Format | PDF + Excel |

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

ENT Devices Market Frequently Asked Questions

The global ENT devices market is expected to reach USD 46.74 billion by 2034, growing at a 5.56% CAGR, driven by technological advancements and aging populations.

In 2025, the hearing aids segment dominated the ENT devices market with 30.50% share.

Growing ENT disorder prevalence, aging populations, investments in healthcare infrastructure, and advancements in minimally invasive technologies are key drivers of market expansion and innovation opportunities.

North America had the largest ENT devices market share of 37.80% in 2025.

A few key major players are Ambu A/S; Atos Medical AB; Cochlear Limited; Demant A/S; GN Store Nord A/S; Johnson & Johnson Services, Inc.; KARL STORZ GmbH & Co. KG; Medtronic plc; and Olympus Corporation.

The endoscopes segment held 62.0% share in 2025.

Download Sample Report of ENT Devices Market

Please fill out the form to request a customized copy of the research report.