Hearing AID Market Trends and Revenue Analysis Report, 2026-2034

REPORT DETAILS

REPORT DETAILS

ABOUT THIS REPORT

Hearing Aid Market Summary

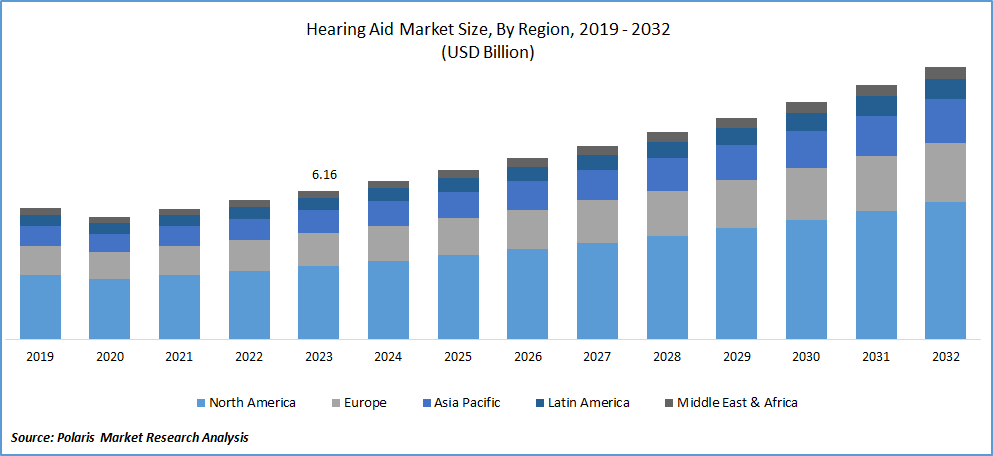

The global hearing aid market size was valued at USD 8.72 billion in 2025, at a CAGR of 6.60% during 2026–2034. The market expansion is fueled by an aging global population and increasing prevalence of hearing disorders.

Market Statistics

Key Takeaways

- North America dominated the global hearing aid market in 2025, accounting for 36% of the total share. This is because of strong healthcare systems and higher healthcare spending. Early use of advanced devices also supports demand.

- Asia Pacific is the fastest-growing region in the hearing aid market and is estimated to register a CAGR of 7.8% during 2026–2034. Growth is linked to a growing aging population and better access to healthcare. Awareness about hearing health is also rising.

- By product, the hearing aid devices segment led the market in 2025, with a revenue share of 71%. These devices are easy to use and widely available. They are noninvasive and cost less than implants.

- By platform features, the adult segment led the market in 2025, accounting for 82% share. This is due to higher cases of hearing loss in adults. Usage of hearing aids is also more common in this group.

- By platform features, the pediatric segment is projected to grow fastest, registering a CAGR of 8.5% during the forecast period. Growth is linked to early diagnosis and growing awareness. More focus on early treatment is also supporting demand.

Industry Dynamics

- The growing geriatric population is increasing demand for hearing aids. Age-related hearing loss is becoming more common among older adults.

- Hearing loss in elderly people affects communication and daily life. This is increasing the need for devices that support independence.

- Advancements in hearing technologies are supporting market growth. New features are improving device performance and user experience.

- Technologies such as digital processing, Bluetooth, and AI are making devices more effective. This is supporting improve sound quality and ease of use.

- High cost of advanced hearing devices remains a challenge. This can limit adoption among some users.

Impact of AI on Hearing Aid Market

- AI improves sound clarity by analyzing surrounding noise. It supports users hear better in different environments.

- AI supports personalized hearing settings based on user needs. It improves comfort and overall experience.

- AI enables devices to adjust automatically to changing sound conditions. It reduces the need for manual adjustments.

- AI improves speech recognition and reduces background noise. It supports clearer communication in daily use.

- AI supports ongoing improvement in device performance. However, high cost and data issues may limit adoption.

To Understand More About this Research: Download Sample Report

Hearing aids are compact electronic devices developed to amplify sound for people with hearing loss. Digital advancements are streamlining the user experience of hearing aids. Some models now connect directly to smartphones, offering users straightforward control and the ability to make adjustments easily. Audiologists can assist users through remote fitting and follow-up services

How Hearing Aids Work?

Hearing aids capture sound through a microphone, process it, and then deliver it to the ear, making it clearer and louder. Modern hearing aids use digital signal processing and noise reduction to improve speech clarity. These capabilities help better communication in everyday situations.

Types of Hearing Aids

- Behind-the-Ear (BTE): These devices fit behind the ear and are linked to an earmold placed inside the ear. They are ideal for mild to extreme hearing loss and are easy to handle and clean. BTE devices are known for their high performance and are commonly used by both adults and children.

- In-the-Ear (ITE): These devices fit perfectly inside the outer ear. They are less visible than BTE models and are easier to insert and remove. ITE hearing aids are useful for mild to severe hearing loss and can include basic control features.

- In-the-Canal (ITC) and Completely-in-Canal (CIC): These are smaller devices that fit partly or fully inside the ear canal. They are more concealed and less noticeable from the outside. Because of their small size, they may have fewer features and may require careful handling.

- Receiver-in-Canal (RIC): These devices are similar to BTE but smaller and lighter. The receiver is inserted into the ear canal, which supports deliver clearer sound. They are comfortable to wear and are commonly preferred for everyday use.

- Invisible-in-Canal (IIC): These are very small devices placed deep inside the ear canal, making them barely invisible. They are ideal for mild to moderate hearing loss and provide a natural listening quality. On the other hand, their small size can restrict battery life and features.

OTC Hearing Aids

Over-the-Counter hearing aids are devices that can be bought without a prescription. They are designed for users with mild to moderate hearing loss. Consumers can adjust settings on their own using simple controls or mobile apps. These devices boost access to hearing care and reduce dependency on clinical visits. They are also more affordable, making hearing options easier to adopt for a wider group of users.

Benefits of Hearing Aids

- Helps consumers hear speech and sounds more clearly. This improves everyday conversation.

- Supports day-to-day activities like phone calls and watching TV. It makes routine tasks easier.

- Helps users stay connected with others. This supports confidence and reduces social isolation.

- Increasing use of hearing aids supports growth in the healthcare market. It creates steady demand for hearing solutions.

- Rising adoption encourages companies to improve technology and design. This supports product development and innovation.

- Supports long-term healthcare cost management. Early use can reduce complications linked to untreated hearing loss.

A World Health Organization report from February 2025 anticipates that close to 2.5 billion individuals worldwide could face some degree of hearing loss by the year 2050. More than 700 million are expected to require hearing rehabilitation services. An aging population is increasing hearing loss cases. Rising noise pollution is also contributing. Chronic conditions such as diabetes and cardiovascular diseases are further adding to the number of cases. Demand for advanced and accessible solutions is increasing as awareness of hearing health continues to improve.

The hearing aid market is seeing increased use of telehealth and remote fitting services. Audiologists conduct hearing assessments, device calibration, and follow-up consultations remotely, especially in rural and underserved areas. In May 2024, hearX introduced hearOAE, a smartphone-compatible OAE testing device with Bluetooth connectivity and data management features. This shift is improving accessibility and reducing the need for frequent clinic visits. It is encouraging organizations to develop devices that support remote programming and real-time assistance.

Market Dynamics

Growing Geriatric Population

The growing geriatric population is boosting the market development as age-related hearing loss, known as presbycusis, becomes increasingly common among older adults. An October 2024 WHO report projected that the global population aged 60+ will rise from 1 billion in 2020 to 1.4 billion by 2030 and double to 2.1 billion by 2050. Those aged 80+ will triple to 426 million in the same period. The demand for effective hearing solutions is rising steadily. Hearing loss in elderly individuals often leads to social isolation, cognitive decline, and reduced quality of life, prompting a greater need for these devices to maintain communication and independence, with a higher proportion of the global population entering the senior age group. The healthcare focus on addressing age-associated conditions, such as hearing impairment, is intensifying as life expectancy continues to improve, thereby supporting the sustained market growth.

Advancement in Hearing Technologies

Advancements in hearing technologies are accelerating hearing aid market expansion by transforming the functionality and appeal of modern devices. Innovations such as digital signal processing, Bluetooth connectivity, artificial intelligence integration, and rechargeable battery have significantly enhanced user experience and device performance. In January 2021, Oticon launched Oticon More, the first hearing aid with an onboard deep neural network (DNN) trained on 12 million real-world sounds. The technology mimics brain processing to improve speech clarity and reduce listening effort in noisy environments. These technological improvements offer better sound quality, greater customization, and seamless integration with other smart devices, addressing many of the traditional limitations associated with hearing aids. Consumer acceptance is rising as hearing devices become more sophisticated, discreet, and user-centric, further fueling the adoption rate across diverse age groups.

Segment Insights

Market Assessment by Product

The global market segmentation, based on product, includes hearing aid devices and hearing implants. The hearing aid devices segment dominated the market share in 2024 due to its widespread accessibility, ease of use, and a broad range of available designs tailored to varying degrees of hearing loss disease treatment. Traditionaldevices, such as behind-the-ear and in-the-ear models, offer noninvasive solutions that are often more affordable and readily available compared to hearing implants. Additionally, advancements in miniaturization, wireless connectivity, and sound processing technologies have particularly enhanced device performance and user comfort, reinforcing the strong preference for these devices among a diverse patient population.

Market Evaluation by Platform Features

The global hearing aid market segmentation, based on platform features, includes adult and pediatric. The pediatric segment is expected to witness the fastest growth during the forecast period, driven by increasing early diagnosis rates of congenital and early-onset hearing loss. Growing awareness among parents and healthcare providers regarding the critical importance of early auditory intervention for language and cognitive development is leading to higher adoption rates of pediatric hearing aids. Moreover, technological advancements specifically catering to children, such as tamper-proof designs, wireless streaming, and durable materials, are encouraging the use of these devices among younger populations, contributing to rapid expansion in this segment.

Regional Insights

The report provides market insights into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. North America dominated the market revenue share in 2024, supported by the presence of well-established healthcare infrastructure, high healthcare expenditure, and strong adoption of advanced medical devices. A 2021 ASTP report found that 78% of US office-based physicians and 96% of non-federal acute care hospitals had adopted certified electronic health record (EHR) systems, showing widespread healthcare digitization. A greater emphasis on early hearing loss screening programs, coupled with favorable reimbursement policies and widespread awareness initiatives, has greatly boosted the demand for hearing aids across the region. Additionally, the presence of major market players and continuous product innovations tailored to consumer needs have strengthened North America's leadership position in the global market.

The Asia Pacific hearing aid market is projected to witness the fastest growth during the forecast period fueled by a rapidly aging population, rising disposable incomes, and improving healthcare accessibility across emerging economies. Increasing awareness about hearing health, coupled with government initiatives to enhance audio logical care and early intervention programs, is creating a strong growth environment. According to a 2025 report by the NHE, the National Hearing Week campaign, led by the MATANAND Welfare Foundation and supported by ENTOD Pharmaceuticals, raised awareness about pediatric hearing loss and early intervention in India, reaching 30 million people, such as parents, educators, and healthcare providers. Furthermore, expanding urbanization and greater acceptance of technologically advanced hearing solutions are contributing to the rising demand for hearing devices across key countries such as China, India, and Japan.

Key Players and Competitive Analysis

The hearing aid industry is witnessing a transformation driven by technological innovation and shifting demographics. Major players such as Sonova, Demant, WS Audiology, and GN Store Nord collectively control the global industry, creating considerable barriers for new entrants. Consumer expectations are evolving toward discreet, AI-enhanced devices with connectivity capabilities, which has accelerated product development cycles and intensified competition based on innovation rather than price. Over-the-counter options following FDA regulatory changes have introduced new competitive dynamics, with companies such as Bose and Jabra entering this space. The competitive landscape shows differentiation through distribution strategies, with traditional manufacturers relying on audiologist networks while newer entrants leverage direct-to-consumer approaches. This bifurcation creates distinct competitive advantages depending on target demographics. Financial performance indicates high margins but increasing pressure from lower-cost alternatives. The competitive future will hinge on balancing innovative features with accessibility as the global population ages and hearing loss prevalence increases. A few key major players are Adicus; Audina Hearing Instruments, Inc.; Eargo, Inc.; GN Store Nord A/S; Horentek Hearing Diagnostics; Jabra; MD Hearing; Sebotek Hearing Systems, LLC; Sonova; Starkey Laboratories; and WS Audiology.

Sonova specializes in innovative hearing care solutions, with a strong focus on hearing aids as a core part of its business. Founded in 1947 and headquartered in Stäfa, Switzerland, Sonova operates through four main business segments: Hearing Instruments, Audiological Care, Consumer Hearing, and Cochlear Implants. Its renowned brands-Phonak, Unitron, AudioNova, Sennheiser (under license), and Advanced Bionics-deliver advanced hearing aids and accessories to consumers in over 100 countries. Sonova’s hearing aids are recognized for their advanced technology, including features such as Bluetooth connectivity, rechargeable batteries, and real-time artificial intelligence for speech enhancement, particularly in noisy environments. The company’s latest platforms, such as Phonak Audéo Sphere Infinio, leverage proprietary AI and chip technology to greatly improve speech understanding, addressing one of the most pressing needs for people with hearing loss. Sonova’s commitment to research, innovation, and comprehensive audiological care has positioned it at the forefront of the hearing aid industry, enabling millions to enjoy improved hearing, better communication, and enhanced quality of life.

Sebotek Hearing Systems, LLC, headquartered in Tulsa, Oklahoma, is a privately held company renowned for revolutionizing the hearing aid industry with its patented receiver-in-the-canal (RIC) technology. SeboTek introduced the first-ever modular RIC hearing device to the global market in 2003, addressing long-standing challenges of traditional hearing aids, such as discomfort, occlusion effects, and the need for frequent remakes of plastic ear molds. SeboTek’s innovative approach separates the sound processor and the speaker, placing the receiver deep inside the ear canal, which allows for a discreet, comfortable fit and improved sound quality. The company’s flagship products, such as the High Definition 2 (HD2) series and the Voice-Q PAC system, offer advanced digital signal processing, wideband frequency response up to 14,000 Hz, and sophisticated noise reduction algorithms that prioritize speech clarity in noisy environments. SeboTek’s modular design enables instant fittings for a wide range of hearing losses, from mild to severe, and reduces barriers for first-time users by providing a more natural listening experience and greater cosmetic appeal.

List of Key Companies in Hearing Aid Industry

- Adicus

- Audina Hearing Instruments, Inc.

- Eargo, Inc.

- GN Store Nord A/S

- Horentek Hearing Diagnostics

- Jabra

- MD Hearing

- Sebotek Hearing Systems, LLC

- Sonova

- Starkey Laboratories

- WS Audiology

Industry Developments

- In July 2025: Cochlear received U.S. FDA approval for the Nucleus Nexa System. It is a smart cochlear implant with upgradable firmware, helping expand its product range. [Source: www.cochlear.com]

- June 2025: Starkey and MED-EL launched DualSync through a joint collaboration. It improves Bluetooth connectivity for users with both hearing aids and cochlear implants. [Source: www.starkey.com/]

- March 2025: Cochlear and GN expanded their R&D partnership under the Smart Hearing Alliance to develop integrated hearing solutions combining cochlear implants and hearing aids. The collaboration focuses on AI-driven connectivity improvements and seamless device integration for enhanced user experiences.[Source: www.cochlear.com]

- March 2025: NewSound launched its first AI-powered OTC hearing aid featuring Femtosense's Clara AI technology. The deep neural network enhances speech clarity by 7-13 dB in noisy environments while consuming minimal power through advanced compression techniques. [Source: hearingreview.com/]

- August 2024: Sonova launched Phonak's Audéo Infinio and Audéo Sphere Infinio hearing aids featuring dual-chip technology with real-time AI sound processing. The platform enhances speech clarity, connectivity, and power efficiency. [Source: www.sonova.com]

Hearing Aid Market Segmentation

By Product Outlook (Revenue, USD Billion, 2021–2034)

- Hearing Aid Devices

- Receiver in the Ear

- Behind the Ear

- Canal Hearing

- Other Hearing Devices

- Hearing Implants

- Cochlear Implant

- Bone Anchor

By Type Outlook (Revenue, USD Billion, 2021–2034)

- Conductive Hearing Loss

- Sensorineural Hearing Loss

By Patient Type Outlook (Revenue, USD Billion, 2021–2034)

- Adult

- Pediatrics

By Technology Outlook (Revenue, USD Billion, 2021–2034)

- Digital Hearing Devices

- Analogue Hearing Device

By Regional Outlook (Revenue, USD Billion, 2021–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Hearing Aid Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 8.72 billion |

| Market Size in 2026 | USD 9.28 billion |

| Revenue Forecast by 2034 | USD 15.50 billion |

| CAGR | 6.60% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD Billion and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

FAQ's

The global market size was valued at USD 8.72 billion in 2025 and is projected to grow to USD 15.50 billion by 2034.

The global market is projected to register a CAGR of 6.60% during the forecast period.

North America dominated the market share in 2025.

A few of the key players in the market are Adicus; Audina Hearing Instruments, Inc.; Eargo, Inc.; GN Store Nord A/S; Horentek Hearing Diagnostics; Jabra; MD Hearing; Sebotek Hearing Systems, LLC; Sonova; Starkey Laboratories; and WS Audiology.

The hearing aid devices segment dominated the market share in 2025.

The pediatric segment is expected to witness the fastest growth during the forecast period.

Download Sample Report of Hearing Aid Market

Please fill out the form to request a customized copy of the research report.