Activated Carbon Market Size, Share, Growth Analysis, 2026-2034

REPORT DETAILS

What Is Activated Carbon Market Size?

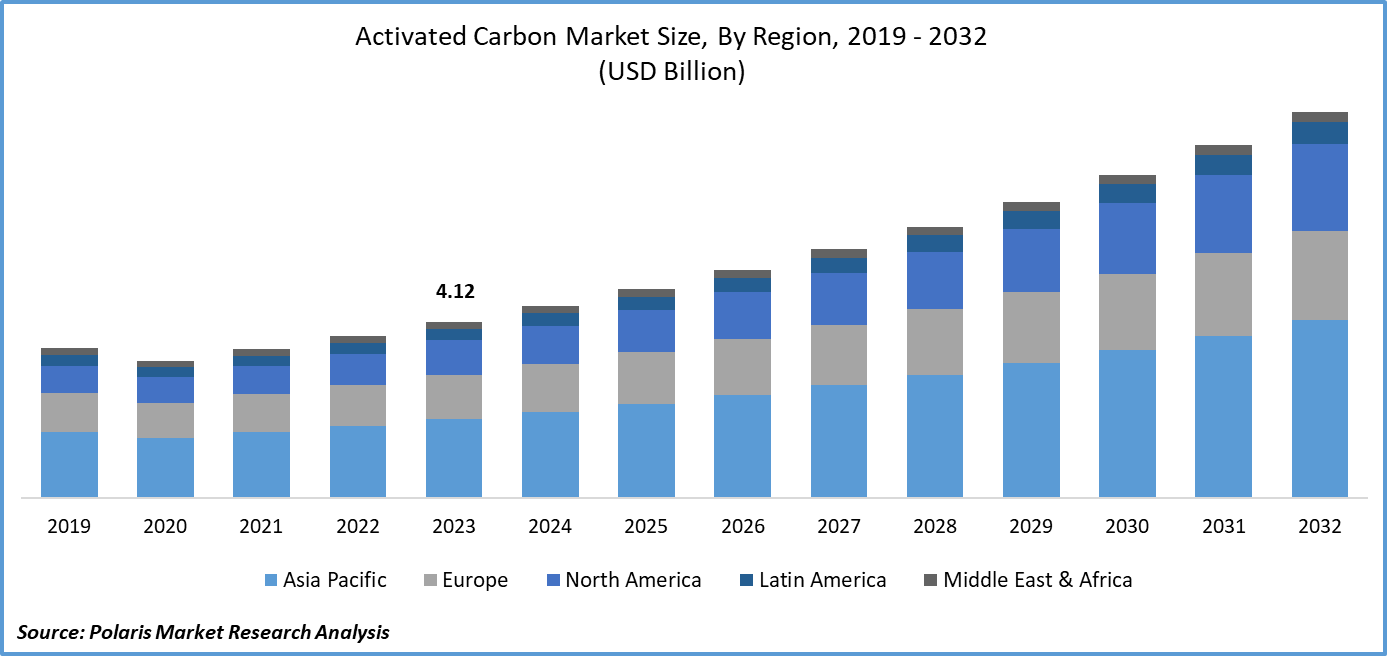

The global valuation of the activated carbon market was around USD 4.89 billion in 2025 and is expected to exhibit a growth rate of 9.2% from 2026 to 2034. This growth is driven by surging demand for water and air purification and improvement in technologies related to carbon capture. The market is also benefiting from increasing industrial air pollution control.

Market Statistics

Key Takeaways

- Asia Pacific dominated with a 53.59% share in 2025, fueled by swift industry and robust demand from major sectors.

- North America is expected to grow at a CAGR of 9.8%, supported by stringent environmental regulations.

- Europe is projected to expand at a CAGR of 8.8%, driven by environmental compliance and green technology adoption.

- The gas phase segment dominated the market in 2025, capturing 54.1% of the share. This was due to strong demand comming from air purification needs and the control of industrial emissions.

- The water treatment segment accounted for 42.1% of the market in 2025. This was largely due to its widespread application in both municipal and industrial water purification processes.

*Note: Figures and projections outlined in this report are the result of Polaris Market Research’s proprietary analytical processes, grounded in the latest available datasets and market observations.

Industry Dynamics

- The demand for purification and filtration solutions from industries and municipalities is growing rapidly. This, in turn, is driving the growth of the global activated carbon market.

- Extension of distributor networks is also hastening the coverage of markets by efficiently integrating manufacturers and smaller buyers.

- The premium pricing of value-added activated carbon commodities and regional regulatory variations are factors preventing market penetration & application.

- Research and development in green production technologies and formulation of custom-designed activated carbon even enhance performance and sustainability, thus encouraging more innovation in the activated carbon industry.

Source: Polaris Market Research Analysis

What Is Activated Carbon?

Activated carbon is also known as activated charcoal. This is the kind of carbon that is treated in such a way that it forms millions of tiny holes. This increases its surface area greatly. This substance is able to hold chemicals on its surface with the help of a process called adsorption. That is why water treatment activated carbon is being used on a large scale for the removal of chemicals from wastewater and drinking water. Similarly, air purification activated carbon is being used for the removal of chemicals from industrial emissions.

Comparison Matrix: PAC vs GAC vs EAC

| Type | Description | Key Applications | Key Characteristics |

| Powdered Activated Carbon (PAC) | PAC is a powder-like material. It is added directly to liquid streams. | Drinking water, food processing | Enhanced action, high adsorption capacity |

| Granular Activated Carbon (GAC) | GAC consists of large particles. They are used in filter systems for continuous treatment. | Water treatment systems, industrial processing | Long service life, stable performance |

| Extruded Activated Carbon (EAC) | EAC is a pellet-based carbon. It is made using binders for a uniform size. | Air purification, gas treatment | Low dust, high mechanical strength |

Source: Polaris Market Research Analysis

The rising investment in R&D by major pharmaceutical firms and the emerging focus of new biotech companies aim to increase the number of biologics in their pipelines. For example, in April 2022, Catalent spent USD 350 million at its facility in the state of Indiana to increase the manufacturing of biologics. The expansion of the facility involves the introduction of new bioreactors and prefilled syringes to cater to the growing demand for the manufacturing of more biologics. The focus on the development of large-molecule drugs involves complex processes. It requires sophisticated technologies and experience in the use of DNA diagnostics and the production of biologics. Thus, the decision to outsource represents a clever tactic for potential partners, considering the scale of experience, familiarity with regulations, and the quick turnaround of results to reduce the risk of the client and enable optimization of the discovery timeline.

Industry Dynamics

Advancements in Activated Carbon Production

There are new activation processes, such as the use of steam, chemicals, and microwaves, which have improved the efficiency of activated carbon. There are also improvements in the pore size distribution and functionality of the adsorption, which helps the activated carbon to remove pollutants more efficiently and even be reusable. The use of activated carbon, therefore, is even more effective for PFAS adsorption, VOC capture, and mercury removal activated carbon applications in water and air purification applications. The size distribution of pores also helps in the preparation of impregnated activated carbon.

Recently, reactivation technologies for activated carbon, or carbon regeneration, have also become widespread. These technologies can revive used carbon so that it can be reused without a reduction in performance. Thermal and chemical reactivation technologies enable companies to enhance sustainability by reducing their costs through lower raw material use.

Increasing Demand for Reducing Industrial Air Pollution

Industrial pollution from power stations, cement industries, and chemical processing is a prominent source of air pollution. According to a report published by the IEA in 2025, global CO2 emissions from energy use increased 0.8% in 2024, a record 37.8 Gt. Concentrations of CO2 climbed 422.5 ppm, three ppm above 2023 values and 50% above pre-industrial values. Activated carbon is widely recognized as a promising material for the capture of hazardous pollutants like mercury, VOC, and sulfur. Stringent emission policies like the Mercury and Air Toxics Standards (MATS) and the revised EPA air quality regulations have had a positive effect on the use of such superior materials. According to a report published by the Clean Air Fund in March 2024, the EPA lowered the annual PM2.5 standard from 12 μg/m³ to 9 μg/m³ due to industrial and vehicle pollution, thereby stimulating demand for vapor-phase technology.

Moreover, rising concerns about the environment, as well as companies' ESG efforts, are also contributing to the investments being made in eco-friendly air purification technologies. The industry is employing activated solutions to meet government regulations, making it paramount for clean air solutions.

Source: Polaris Market Research Analysis

Segmental Insights

Product Insights

On the basis of product, the activated carbon market is segmented into granular, powdered, and other products. The powdered segment accounted for the largest market wirh 42.98% share in 2025. The segment’s dominance is primarily attributed to its high adsorption efficiency and widespread applicability. Powdered activated carbon is widely used in liquid-phase activated carbon applications. Here, it supports PFAS removal activated carbon, and mercury capture. The fine particle size of the powdered form allows for more effective removal of contaminants. This benefit has made powdered activated carbon the preferred choice for emergency spill responses and batch treatment processes.

Comparison: Granular vs Powdered vs Pelletized Activated Carbon

| Parameter | Granular Activated Carbon (GAC) | Powdered Activated Carbon (PAC) | Pelletized / Extruded Activated Carbon (EAC) |

| Form | Irregular granules | Fine powder | Cylindrical pellets |

| Particle size | Larger particles (0.2–5 mm) | Very fine (<0.18 mm) | Uniform pellets (diameter ~0.8–5 mm) |

| Usage Method | Fixed beds / filters | Direct dosing in liquid | Packed beds / columns |

| Main Application | Water treatment, industrial filtration | Drinking water, wastewater, emergency treatment | Air purification, gas treatment |

| Adsorption Speed | Moderate | Fast (high surface contact) | Moderate |

| Pressure Drop | Low | Not Applicable | Very Low |

| Handling | Easy to handle | Dusty, handling difficult | Very easy, low dust |

| Regeneration | Possible | Generally not regenerated | Possible |

| Mechanical Strength | Moderate | Low | High |

| Cost | Moderate | Low | Higher |

| Key Advantage | Long service life | High efficiency, quick action | Strong structure, low dust |

| Limitation | Slower than PAC | Not suitable for continuous systems | Costlier |

Source: Polaris Market Research Analysis

Application Insights

By application, the market is segmented into liquid phase and gas phase. The gas phase segment led the market with 54.1% share in 2025. Growing global emphasis on industrial emission control and air quality management contributes to the high demand for gas phase activated carbon. Activated carbon is effective for VOC adsorption and the removal of sulfur-based pollutants. This has made it an essential component of flue gas treatment and solvent recovery systems. The presence of stringent emission regulations across industries has prompted them to adopt activated carbon-based gas purification solutions.

Raw Material Analysis

The market segmentation on the basis of raw material includes coal-based, coconut shell, hardwood-based, softwood-based, and other materials. The coal-based segment is anticipated to expand with a substantial CAGR of 8.9% during the forecast period because of the extensive use of coal-based carbon in large-scale filtration and purification methods and processes. It is well known for its strong absorption properties. As such, coal-based carbon can handle large quantities of contaminated water and gas. Cost-effectiveness and easy availability on a large scale have further escalated its adoption in the treatment of municipal water and purification of gas. Furthermore, advancements in activation technology are further improving the properties of coal-based carbon, thereby gaining prominent preference over other variants even in developed nations.

Distribution Channel Analysis

The activated carbon market, based on distribution channel, is divided into direct wholesale to manufacturers, distributor networks, and retail channel. Among these, the distributor networks segment is projected to grow at the fastest rate of 9.9% during the forecast period. This is due to its ability to fill the gap between large-scale manufacturers and smaller-scale or local consumers. They make market penetration easy by taking care of logistics, storing goods, and also providing local customer service. This is very useful when doing business in emerging markets. They also provide customized packaging, pricing, and technical support. Moreover, the increased complexities of these carbon products across different industry segments are also promoting the use of professional distributors who could provide customized solutions.

End User Analysis

The market segmentation, by end user, is done into water treatment, air & gas purification, food & beverage processing, pharmaceutical, mining & metallurgy, automotive & transportation, and others. The market share of the water treatment segment was the highest in 2025 accounting for 42.1%. This is because of the high usage in the municipal and industrial sectors. This is the most effective segment, removing chlorine and other chemical contaminants from the water. This is the major attribute for the increasing demand for safe drinking water. Moreover, growing concern for environmental purity and rising costs of improper filtration have accelerated market growth.

Source: Polaris Market Research Analysis

Real-World Applications of Activated Carbon

| Application Area | Real-World Example | Purpose / Use |

| Drinking Water Filters | Household RO filters, municipal water treatment plants | Removal of chlorine, odor, organic contaminants |

| Air Purifiers | Indoor air purifiers, HVAC filtration systems | Removal of VOCs, smoke, and harmful gases |

| Industrial Emission Control | Power plants, cement plants, chemical industries | Capture of mercury, sulfur compounds, and toxic emissions |

| Food Processing | Sugar refining, edible oil purification, beverage processing | Removal of color, impurities, and unwanted taste |

| Pharmaceutical Purification | Drug manufacturing, API processing | Removal of impurities, purification of active compounds |

Source: Polaris Market Research Analysis

Regional Analysis

This report offers market insights into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. The Asia Pacific activated carbon market accounted for a 47.6% revenue share in 2024, driven by high demand across industries such as water treatment, air purification, and gold separation. The high level of air pollution is driving increased carbon use in air-cleaning technology, as air pollution continues to rise. A WHO report in November 2024 found that air pollution causes 6.5 million deaths each year, and 70% of those deaths occur in the Asia Pacific region. Also, due to large factories and the availability of raw materials, it is produced at an economical rate, making it more dominant in the market.

The China activated carbon market accounted for a 48.2% market share due to its large manufacturing base and easy access to raw materials. Moreover, demand in the Chinese market is high across the drinking water purification, food industry, and metal extraction sectors. Moreover, the Chinese government has been promoting clean air and clean water. This is boosting the demand for activated carbon.

The North America market for activated carbon is expected to experience substantial growth with 9.8% CAGR due to increasing environmental concerns and emission controls in this region. Adoption in the industrial and municipal water treatment process and increasing use in automobile emission controls and gas purification methods are contributing factors. In addition, the advent of the renewable and clean technology boom is expected to further boost the market for the use of activated carbon in the generation of power. The use of the material in the application of the circular economy model is also expected to contribute to the growth of the market.

The US activated carbon sector is growing due to stringent environmental regulations and rising investment in air and water purification technologies. With rising demand from industries such as automotive, healthcare, and chemicals, this market is expected to expand. Advances in technology are expected to further boost this industry.

Europe is also a key player. Environmentally mandated standards and the adoption of environmentally friendly technologies are driving factors for growth in the region. The shift toward clean industries in Europe is also driving demand for activated carbon in air filters and flue desulfurization. The use of high-performance filters and adsorbents due to government policies and strategies for industry carbon footprint reductions in various application segments is a contributing factor for market growth. Innovations have also widened their scope, driven by developments in areas of using activated carbon in consumer commodities like cosmetics and personal care products.

The UK activated carbon market is sustained by a growing emphasis on environmentally responsible industry processes and robust regulation concerning emissions and water treatment. The increased integration of biomedicine, consumer, and energy storage systems is opening up new end-use possibilities. Moreover, developments in materials science and a shift towards a more circular economy are enhancing its role in Europe.

Source: Polaris Market Research Analysis

Key Players and Competitive Analysis

The activated carbon market is undergoing a technological transformation. It is driven by sustainable value chains. Leading activated carbon manufacturers and activated carbon suppliers are focusing on strategic investments to improve the efficiency of the production process and its applications in water and air purification. The industry analysis indicates an increase in demand for PFAS, which serve as filters to remove pollutants from the environment, especially in developed countries with stringent environmental regulations. The Asia Pacific region accounts for the majority of demand for the activated carbon market, driven by increased industrialization and environmental pollution, whereas the North America market emphasizes innovative technologies, such as sorbent systems in emerging applications. Small- and medium-scale businesses are experiencing success through innovation in niche applications, such as biogas purification. However, supply chain disruptions and fluctuations in raw material prices act as major factors hindering the growth of the activated carbon market.

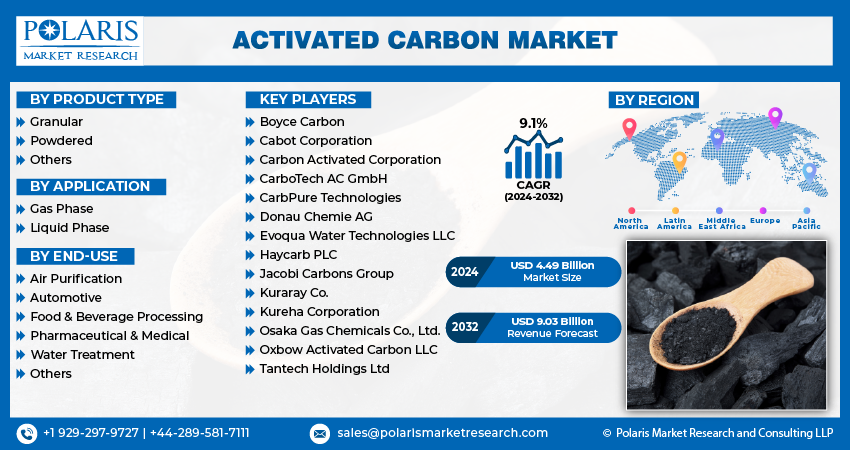

A few key players are Boyce Carbon; Cabot Corporation; Carbon Activated Corporation; CarboTech AC GmbH; CarbPure Technologies; Donau Chemie AG; Evoqua Water Technologies LLC; Haycarb PLC; Jacobi Carbons Group; Kuraray Co.; Kureha Corporation; Osaka Gas Chemicals Co., Ltd.; Oxbow Activated Carbon LLC; and Tantech Holdings Ltd.

The future outlook of the activated carbon market highlights sustainability and the circular economy, including reactivation services and bio-based materials. Expert insights point to the opportunity for expansion in the applications of storage in the energy and pharmaceutical industries, yet market competition depends on the innovation of advanced material applications by activated carbon manufacturers.

What Leaders Compete On

- Scale of reactivation services to extend the life cycles of a product and minimize operating costs for customers.

- Focused on developing specialty-activated-carbon products

- Regional production and distribution networks for security of supply

- Adherence to quality and certification standards and industry norms

Competitive Strategies

- Expanding capacity, upgrading activation and reactivation facilities

- Strategic partnerships for distribution networks and municipal utilities

- Investment in certification and compliance with increasing environmental standards

- Vertical integration for dealing with fluctuations in feedstock prices

- Expansion of the portfolio by introducing high-margin specialty activated carbon products

Key Players

- Boyce Carbon

- Cabot Corporation

- Carbon Activated Corporation

- CarboTech AC GmbH

- CarbPure Technologies

- Donau Chemie AG

- Evoqua Water Technologies LLC

- Haycarb PLC

- Jacobi Carbons Group

- Kuraray Co.

- Kureha Corporation

- Osaka Gas Chemicals Co., Ltd.

- Oxbow Activated Carbon LLC

- Tantech Holdings Ltd

Industry Developments

- February 2026: Kuraray Co., Ltd. expanded its activated carbon capacity in Asia. This supports rising demand from air filtration and water purification sectors. Focus is on improving regional supply availability. (Source: kuraray.com)

- December 2025: Calgon Carbon Corporation introduced advanced activated carbon solutions for PFAS removal. The launch strengthens capabilities in environmental remediation and water treatment applications. (Source: calgoncarbon.com)

- December 2025: AFRY was awarded a contract to design Kemira’s sustainable activated carbon reactivation plant in Sweden. The facility will recycle used activated carbon so it can be used again in water treatment. This is needed because stricter environmental rules are making demand rise. It should be up and running by 2027. (Source: afry.com)

- May 2025: Jacobi announced a 15–20% price increase across all coconut-shell grades, effective July 1, attributing the change to sustained inflation in raw-material costs. (Source: jacobi.com)

- October 2024: CarbonFree announced a zero-carbon mineralization process for CO₂ capture and industrial CO₂-to-usable products conversion. The company revealed that the innovation provides sustainable carbon management solutions. It could help reduce greenhouse gas emissions across industries. (Source: carbonfree.com)

- May 2024: Organic Recycling Systems Limited introduced GAC-01, the biomass-based activated carbon granule for water treatment. Made from waste biomass, this product can effectively purify water to contribute towards sustainability in both domestic and global markets. (Source: organicrecycling.com)

- November 2024: SOLEVO entered into an exclusive distribution agreement with Carbonitalia for the supply of activated carbon products for water treatment and mining applications within African markets. (Source: solevogroup.com)

Activated Carbon Market Segmentation

By Product Outlook (Volume, Tons; Revenue, USD Billion, 2021–2034)

- Granular

- Powdered

- Other Products

By Application Outlook (Volume, Tons; Revenue, USD Billion, 2021–2034)

- Liquid Phase

- Gas Phase

By Raw Material Outlook (Volume, Tons; Revenue, USD Billion, 2021–2034)

- Coal-Based

- Softwood-Based

- Coconut Shell

- Hardwood-Based

- Other Materials

By Distribution Channel Outlook (Volume, Tons; Revenue, USD Billion, 2021–2034)

- Direct Wholesale to Manufacturers

- Distributor Networks

- Retail Channel

By End User Outlook (Volume, Tons; Revenue, USD Billion, 2021–2034)

- Water Treatment

- Air & Gas Purification

- Food & Beverage Processing

- Pharmaceutical

- Mining & Metallurgy

- Automotive & Transportation

- Others

By Regional Outlook (Revenue, USD Billion, 2021–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Future of Activated Carbon Market

The market is shifting toward sustainable carbon sources such as coconut shells and bio-based feedstocks to reduce environmental impact. Regeneration technologies are gaining traction, allowing reuse of spent carbon and lowering operational costs. Emerging uses in energy storage, including supercapacitors and battery systems, are opening new growth avenues. At the same time, stricter environmental regulations on air and water quality are accelerating adoption in industries. Overall, innovation and sustainability will remain the important growth drivers.

Activated Carbon Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 4.89 billion |

| Market Size in 2026 | USD 5.33 billion |

| Revenue Forecast by 2034 | USD 10.81 billion |

| CAGR | 9.2% |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD billion, 2021–2034 and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape | Activated Carbon Industry Trend Analysis (2025) Company profiles/industry participants profiling includes company overview, financial information, product/service benchmarking, and recent developments |

| Report Format | PDF + Excel |

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Activated Carbon Market FAQ's

The activated carbon market is estimated to be valued at USD 4.89 billion in 2025. It is also projected to reach USD 10.80 billion by 2034.

Market growth is driven by the increasing needs of the market for water treatment, air filtration, environmental regulations, and the expanding uses of the market in the food, beverage, and pharmaceutical industries.

There are various types of activated carbon. Some major types are granular activated carbon (GAC), powdered activated carbon (PAC), and extruded or pelletized carbon.

Uses of activated carbon are dominated by water treatment, air purification, processing in the field of foods and beverages, pharmaceutical uses, and gas treatment in various industry divisions.

The market for activated carbon is expected to have an impressive compound annual growth rate (CAGR) of 9.2% from 2026 to 2034.

The distributor networks segment is expected to witness the fastest growth during the forecast period.

Download Sample Report of Activated Carbon Market

Please fill out the form to request a customized copy of the research report.