Benign Prostatic Hyperplasia Surgical Treatment Market Share Forecast 2025-2034

REPORT DETAILS

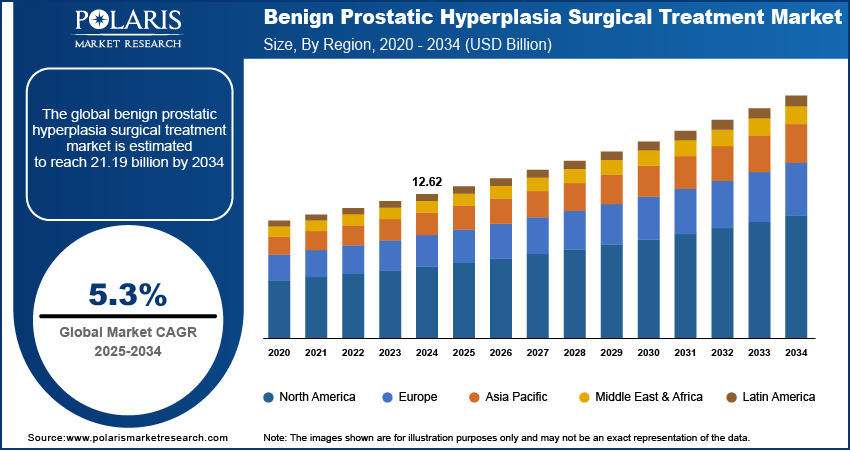

Benign Prostatic Hyperplasia Surgical Treatment Market Summary

The global benign prostatic hyperplasia (BPH) surgical treatment market size was valued at USD 2,042.94 million in 2024, growing at a CAGR of 5.3% from 2025 to 2034. The rising demand for BPH treatment among the aging male population, advancements in minimally invasive urology, and increased awareness of treatments with improved outcomes boost the market growth.

Market Statistics

Benign prostatic hyperplasia (BPH) surgical treatment refers to medical procedures aimed at clearing urinary obstruction caused by the noncancerous enlargement of the prostate gland. The market for BPH surgical treatment is witnessing steady growth, primarily driven by the rising preference for minimally invasive surgeries and increasing awareness of early urological care among aging male populations. Techniques such as laser therapies, transurethral resection of the prostate (TURP), and prostatic urethral lift (PUL) are gaining traction as patients increasingly seek effective treatment options with reduced recovery time. These advanced procedures are associated with fewer complications, shorter hospital stays, and improved patient outcomes, further reinforcing their appeal.

Source: Polaris Market Research Analysis

To Understand More About this Research: Download Sample Report

The growing awareness of prostate health, boosted by public health campaigns and enhanced diagnostic capabilities, is encouraging men to pursue timely intervention, thereby expanding the potential patient pool and driving demand for surgical solutions. In June 2025, Teleflex launched two Men’s Health Month initiatives, including a "Prostate Monster" ad campaign and a mobile education center, to raise awareness about BPH symptoms and rectal toxicity from prostate radiation. Aiming to promote physician and patient education.

The ongoing enhancement of healthcare infrastructure across developed and emerging economies boosts growth opportunities. According to a December 2024 report by the World Economic Forum (WEF), in 2022, the hospital sector accounted for ~40% of the global healthcare market, valued at over USD 3.9 trillion. The report projects this share will increase to 44% by 2029, reaching a market value of USD 5.19 trillion. Improved access to urological care, coupled with increasing investments in advanced surgical equipment, is enabling healthcare providers to offer specialized and precise treatments for BPH. The expansion of hospital networks, ambulatory surgical centers, and specialty clinics is supporting the adoption of modern surgical technologies, making them accessible to a broader demographic. Moreover, advancements in training programs and the availability of skilled urologists are contributing to the overall efficiency and success rates of BPH surgeries. This robust infrastructure development supports clinical capabilities and creates a favorable environment for innovation and procedural adoption, further enhancing development.

Industry Dynamics

Rising Demand from Aging Male Population

The aging male population is significantly impacting the BPH surgical treatment sector as the prevalence of BPH increases with age. Hormonal changes and prostate tissue growth contribute to urinary obstruction as men grow older, necessitating medical or surgical intervention. According to a February 2025 WHO report, the global population aged 60 and above is expected to grow, rising from 1.1 billion in 2023 to 1.4 billion by 2030. This demographic shift is resulting in a larger patient pool seeking effective and lasting treatment solutions. Consequently, the demand for surgical procedures that offer symptom relief and improved quality of life is on the rise. The aging population also tends to witness higher rates of comorbidities, further reinforcing the need for timely and efficient urological care.

Advancements in Urology Technology

Advancements in urology technology are further accelerating the growth of BPH treatment. Innovations such as medical laser-based procedures, robotic-assisted surgeries, and real-time imaging systems have greatly improved the precision, safety, and efficacy of BPH treatments. In February 2025, SGMC Health acquired Intuitive's da Vinci 5 surgical robot system to advance minimally invasive care. The platform enhances precision, visualization, and control across various specialties, such as gynecology, urology, and general surgery, with the goal of improving surgical efficiency and patient outcomes. These technological developments enable minimally invasive techniques that reduce patient discomfort, shorten recovery periods, and improve clinical outcomes. The integration of advanced tools into surgical practice supports better procedural success. Additionally, it enhances the confidence of both healthcare providers and patients in opting for surgical intervention, thereby driving opportunities for expansion.

Source: Polaris Market Research Analysis

Segmental Insights

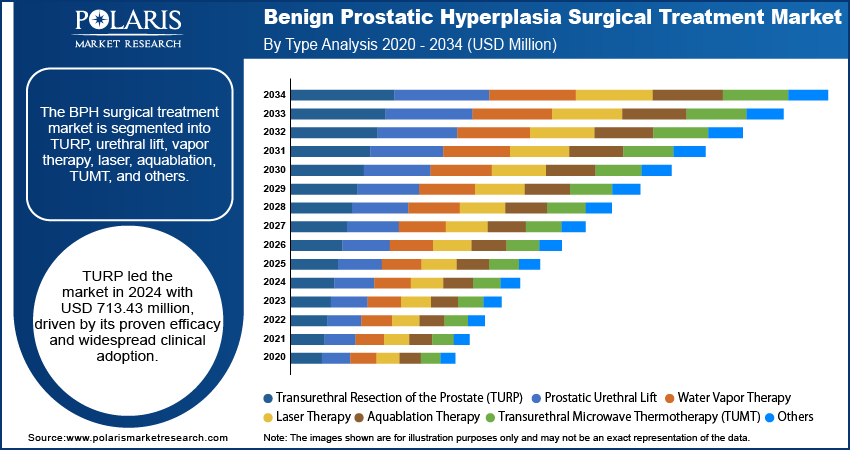

Type Analysis

The segmentation, based on type, includes transurethral resection of the prostate (TURP), prostatic urethral lift, water vapor therapy, laser therapy, aquablation therapy, transurethral microwave thermotherapy (TUMT), and others. The transurethral resection of the prostate (TURP) segment dominated with a valuation of USD 713.43 million in 2024 due to its long-standing clinical efficacy and widespread adoption as the standard of care. STURP has been widely recognized for delivering reliable symptom relief and improved urinary flow in patients affected by moderate to severe BPH. The technique’s vast procedural familiarity among urologists, along with its well-established safety profile, has contributed to its preference in both the primary and referral healthcare sectors. Additionally, its integration into clinical guidelines and accessibility across diverse healthcare systems further support its position.

The prostatic urethral lift segment is expected to witness robust growth during the forecast period, driven by its minimally invasive nature and preservation of sexual function. This procedure has gained attention for offering rapid symptom relief without the need for extensive tissue removal, making it especially appealing to younger or sexually active patients. The outpatient-friendly approach, shorter recovery time, and reduced risk of complications are fueling its increased adoption. Furthermore, growing awareness among patients and providers about alternatives to traditional resection techniques is improving the segment’s momentum.

End User Analysis

The segmentation, based on end user, includes hospitals, ambulatory surgery centers and clinics, and homecare settings. The hospitals segment accounted for the largest revenue share in 2024, valued at USD 1,304.27 million, supported by their wide diagnostic capabilities, availability of specialized urologists, and access to advanced surgical infrastructure. Hospitals often serve as primary centers for urological interventions, particularly in cases requiring complex procedures or postoperative care. Their ability to manage a high volume of patients and perform a variety of BPH surgical techniques, such as TURP and laser therapies, makes them preferred for both elective and emergency treatments. Additionally, the presence of multidisciplinary teams further enhances procedural outcomes and patient trust.

The ambulatory surgery centers (ASCs) segment is projected to register the highest CAGR of 5.7% during the forecast period, due to the rising preference for outpatient procedures and cost-effective care delivery. ASCs offer a streamlined alternative for patients seeking minimally invasive BPH surgeries, often with shorter wait times and reduced hospital-associated costs. Technological advancements have enabled many BPH surgeries to be performed safely in these centers, enhancing procedural efficiency and patient satisfaction. Moreover, the expanding footprint of ASCs across urban and semi-urban areas is also making these facilities more accessible, driving their increasing role in the BPH treatment landscape.

Source: Polaris Market Research Analysis

Regional Analysis

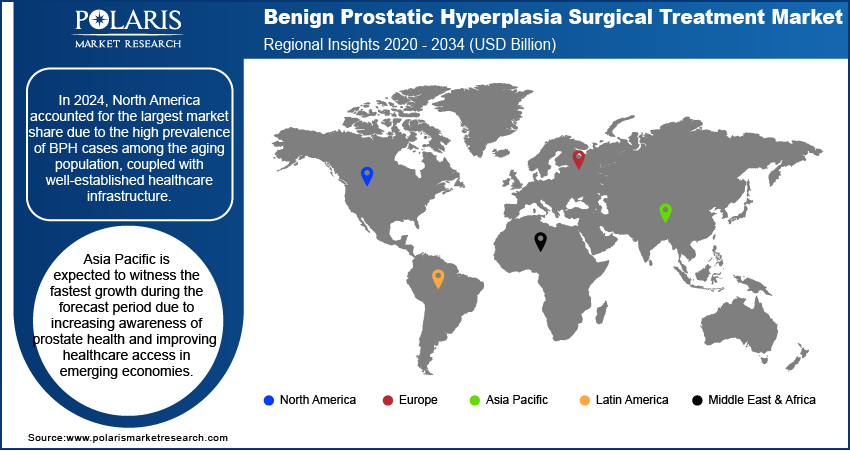

The report provides industry insights into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. The North America benign prostatic hyperplasia surgical treatment market held the largest revenue share, valued at USD 888.88 million in 2024, driven by a high majority of BPH, strong adoption of advanced surgical techniques, and robust healthcare expenditure. According to a December 2024 CMS report, U.S. healthcare expenditures rose by 7.5% in 2023, reaching USD 4.9 trillion nationwide, equivalent to ~USD 14,570 per capita. This growth reflects continued increases in medical costs and service utilization across the healthcare system. The region benefits from a well-established healthcare infrastructure and a proactive approach to men’s health, which encourages early diagnosis and intervention. Furthermore, continuous technological innovation, combined with the presence of leading medical device manufacturers, further enhances the availability and adoption of advanced surgical solutions across the healthcare sector.

U.S. Benign Prostatic Hyperplasia Surgical Treatment Market Trends

The U.S. market held the largest regional revenue share valued at USD 714.48 million in 2024, primarily due to its advanced healthcare infrastructure, high awareness of urological disorders, and widespread access to specialized surgical procedures. The presence of a large aging male population, with the rapid adoption of innovative and minimally invasive technologies, further supports dominance. Additionally, strong insurance coverage and established clinical guidelines contribute to higher procedural volumes across healthcare facilities.

Asia Pacific Benign Prostatic Hyperplasia Surgical Treatment Market Overview

Asia Pacific captured 21.61% share of the global market in 2024, fueled by increasing awareness of urological health and growing healthcare investments. According to an IBEF report released in February 2025, India's 2025-26 Union Budget allocated USD 11.5 billion to healthcare, representing a 9.78% increase in system development and upgrades. Rapid urbanization, an expanding geriatric population, and improving access to surgical care are contributing to the rising demand for BPH treatment in the region. Countries within Asia Pacific are also experiencing a shift toward modern surgical techniques, supported by the expansion of healthcare infrastructure and government-led health initiatives. These factors collectively position the region as a promising growth frontier for BPH surgical interventions.

China Benign Prostatic Hyperplasia Surgical Treatment Market Assessment

The market in China is expected to register a CAGR of 6.4% during the forecast period, driven by increasing healthcare investments, rising awareness of prostate health-related conditions, and expanding access to surgical care in urban and semi-urban areas. The country is experiencing a demographic shift with a growing elderly population, which is driving demand for effective BPH management. According to a report by the Ministry of Civil Affairs and the China National Committee released in October 2024, China's elderly population aged 60 and above reached 297 million in 2023, representing 21.1% of its total population. Moreover, government support for healthcare modernization and the integration of advanced surgical technologies are further accelerating opportunities for expansion.

Europe Benign Prostatic Hyperplasia Surgical Treatment Market Insights

The market in Europe is projected to reach USD 963.03 million during the forecast period, driven by advancements in medical technology, supportive healthcare policies, and a well-organized reimbursement framework. The region demonstrates a strong inclination toward adopting minimally invasive and innovative treatment approaches, aligning with the broader focus on patient safety and cost-efficiency. Additionally, the increasing focus on improving men’s health outcomes, with the development of structured clinical guidelines for BPH management, is expected to support the ongoing expansion of surgical treatment options across European healthcare systems.

UK Benign Prostatic Hyperplasia Surgical Treatment Market Analysis

The market growth in the UK is driven by the increasing preference for minimally invasive procedures and continuous improvements in public healthcare delivery. The presence of well-structured referral systems and a strong focus on early diagnosis are contributing to timely intervention and procedural growth. Furthermore, the National Health Service’s focus on reducing surgical wait times and improving access to innovative treatment options is further supporting the ongoing expansion.

Source: Polaris Market Research Analysis

Key Players and Competitive Analysis

The benign prostatic hyperplasia (BPH) surgical treatment sector is shaped by emerging markets, revenue growth, and technological advancements. North America leads in adoption due to high BPH prevalence and strategic investments in advanced techniques such as TURP and laser therapies. Meanwhile, Asia Pacific shows strong expansion opportunities, driven by rising healthcare investments and urological health awareness. Competitive intelligence reveals ambulatory surgery centers (ASCs) as high-growth segments, fueled by cost-effective outpatient demand. Major players focus on sustainable value chains, leveraging partnerships and disruptive technologies to enhance precision and efficiency. Economic and geopolitical shifts, such as aging populations in developed markets and infrastructure gaps in emerging regions, influence vendor strategies. Moreover, companies prioritize region-wise market estimates to address latent demand, while pricing insights reflect competition between robotic systems and minimally invasive alternatives. Expert insights highlight the need for business transformation to align with outpatient trends and future development strategies.

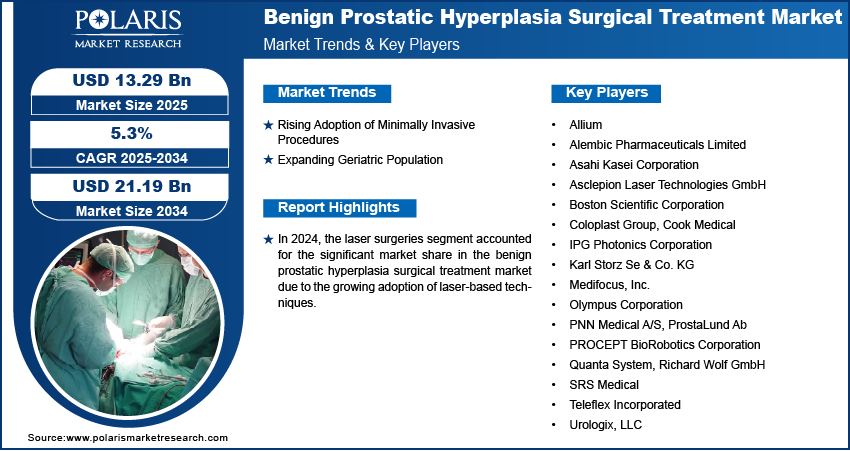

A few key players are Alembic Pharmaceuticals Limited; Asahi Kasei Corporation; Boston Scientific Corporation; Cleveland Clinic; Coloplast Group; Cook Medical; Karl Storz SE & Co. KG; Medifocus, Inc.; Medtronic; Olympus Corporation; and The Johns Hopkins Hospital.

Key Players

- Alembic Pharmaceuticals Limited

- Asahi Kasei Corporation

- Boston Scientific Corporation

- Cleveland Clinic

- Coloplast Group

- Cook Medical

- Karl Storz SE & Co. KG

- Medifocus, Inc.

- Medtronic

- Olympus Corporation

- The Johns Hopkins Hospital

Industry Developments

April 2025: Rivermark Medical enrolled the first patient in its RAPID III clinical trial (NCT06849258), a multicenter study evaluating the FloStent System for treating lower urinary tract symptoms caused by benign prostatic hyperplasia (BPH).

February 2025: Olympus APAC expanded the availability of its iTind device for BPH treatment across Asia Pacific, including a planned March launch in Korea. The minimally invasive device was previously available in the U.S. and Europe.

November 2024: Cook Medical invested in Zenflow, a company developing a minimally invasive device for benign prostatic hyperplasia (BPH).

Benign Prostatic Hyperplasia Surgical Treatment Market Segmentation

By Type Outlook (Revenue, USD Million, 2020–2034)

- Transurethral Resection of the Prostate (TURP)

- Prostatic Urethral Lift

- Water Vapor Therapy

- Laser Therapy

- Aquablation Therapy

- Transurethral Microwave Thermotherapy (TUMT)

- Others

By End User Outlook (Revenue, USD Million, 2020–2034)

- Hospitals

- Ambulatory Surgery Centers and Clinics

- Homecare Settings

By Regional Outlook (Revenue, USD Million, 2020–2034)

- North America

- U.S.

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Benign Prostatic Hyperplasia Surgical Treatment Market Report Scope

| Report Attributes | Details |

| Market Size in 2024 | USD 2,042.94 million |

| Market Size in 2025 | USD 2,142.22 million |

| Revenue Forecast by 2034 | USD 3,412.57 million |

| CAGR | 5.3% from 2025 to 2034 |

| Base Year | 2024 |

| Historical Data | 2020–2023 |

| Forecast Period | 2025–2034 |

| Quantitative Units | Revenue in USD Million and CAGR from 2025 to 2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Industry Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Benign Prostatic Hyperplasia Surgical Treatment Market FAQ's

The global market size was valued at USD 2,042.94 million in 2024 and is projected to grow to USD 3,412.57 million by 2034.

The global market is projected to register a CAGR of 5.3% during the forecast period.

North America dominated the market share in 2024.

A few of the key players in the market are Alembic Pharmaceuticals Limited; Asahi Kasei Corporation; Boston Scientific Corporation; Cleveland Clinic; Coloplast Group; Cook Medical; Karl Storz SE & Co. KG; Medifocus, Inc.; Medtronic; Olympus Corporation; and The Johns Hopkins Hospital.

The transurethral resection of the prostate (TURP) segment dominated the market with a valuation of USD 713.43 million in 2024

The ambulatory surgery centers (ASCs) segment is projected to register the highest CAGR of 5.3% during the forecast period.

Download Sample Report of Benign Prostatic Hyperplasia Surgical Treatment Market

Please fill out the form to request a customized copy of the research report.