Service Robotics Market Size, Share & Growth Analysis Report, 2026-2034

REPORT DETAILS

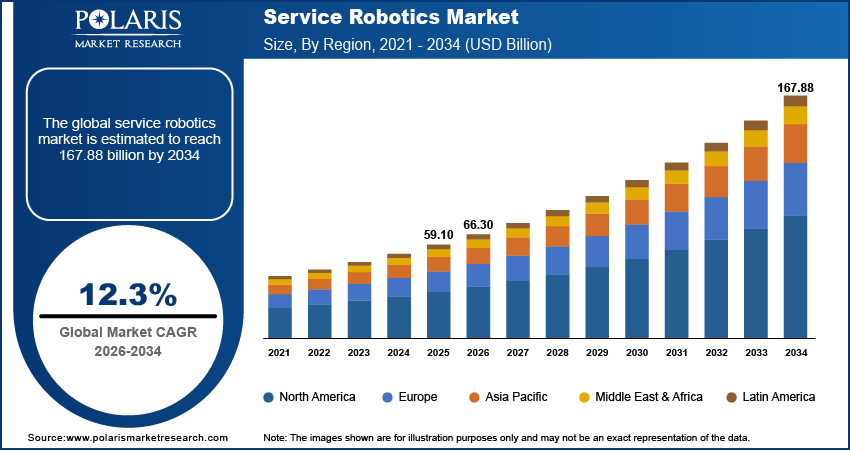

Service Robotics Market Summary

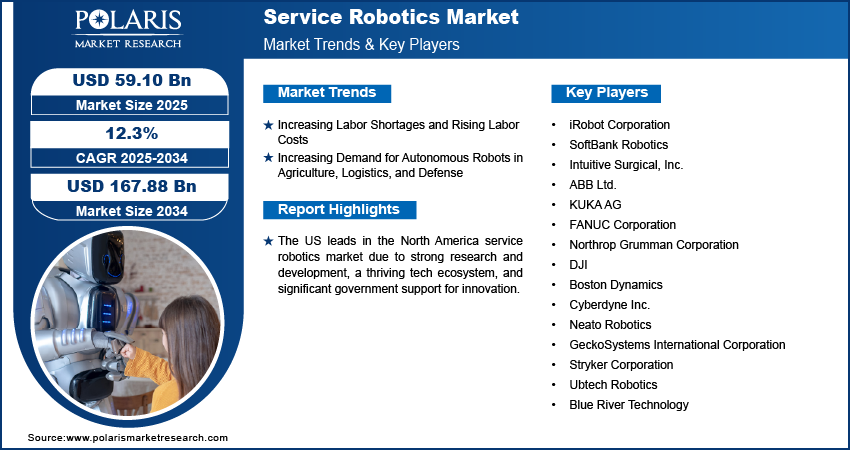

The service robotics market size was valued at USD 59.10 billion in 2025, exhibiting a CAGR of 12.3% during 2026–2034. Rising demand for automation, AI, and sensor technologies drives the market growth. Increasing applications of these robots in industries such as healthcare, agriculture, and logistics, fuel the market expansion.

Market Statistics

Key Takeaways

- North America accounted for the largest global revenue share accounting for 30.0% in 2025. Aggressive R&D, substantial technology spending, and early adoption in key sectors fuel the North America service robotics market growth.

- As per our service robotics market forecast, the Asia Pacific market is expected to witness the fastest growth with a CAGR of 13.6%, during the forecast period. It is driven by industrialization, a surging e-commerce industry, and increasing demand in China and Japan.

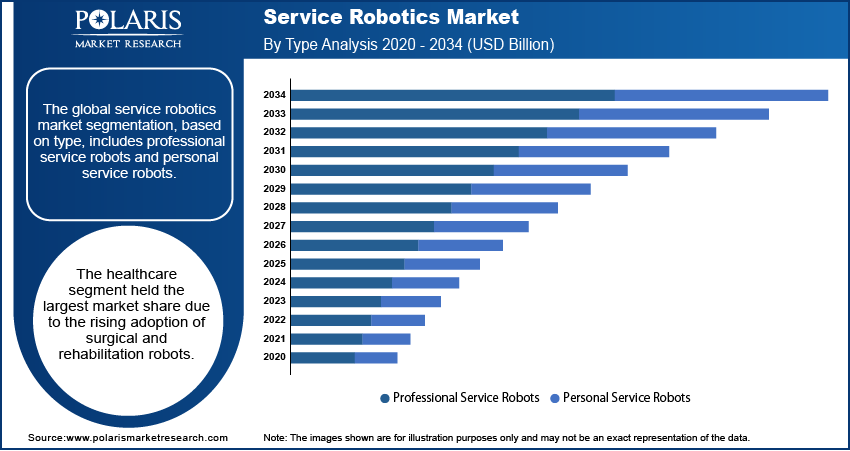

- The professional service robots segment led the market with 69.96% revenue share in 2025. An increase in demand for automation and labor efficiency in agriculture and logistics propels the segment growth.

- The mobile platforms segment accounted for 13.0% share in 2025. Their widespread use in warehousing, manufacturing, and smart infrastructure drives the dominance.

- The software segment is expected to grow at a CAGR of 14.6% during 2026 to 2034. This is due to the rising use in healthcare, customer service, and personal assistance is supporting the segment growth.

Industry Dynamics

- Labor shortages and increasing labor costs are compelling businesses in various industries, such as retail, healthcare, and hospitality to use service robots for repetitive tasks.

- Increasing connectivity with IoT and 5G will boost industry growth.

- Labor shortage and increased demand for operational efficiency propel the adoption of service robots.

- After the COVID-19 pandemic, the adoption of service robots is rising in healthcare and sanitation, driving demand for contactless and self-service-based solutions.

- The combination of 5G and IoT technologies is making device-to-robot communication more efficient, thus enhancing real-time operating coordination and efficiency.

Source: Polaris Market Research Analysis

AI Impact on Service Robotics Market

- Artificial intelligence (AI) allows service robots to move through complicated spaces and carry out tasks on their own.

- In healthcare, AI-based service robots assist with surgeries, monitor patients, and care for the elderly.

- AI in service robotics improves warehouse efficiency by balancing loads and reducing errors.

- Machine learning in robotics makes robots more flexible and allows them to learn from experience.

- In healthcare, AI-enabled service robots help with surgeries, patient monitoring, rehabilitation, and elderly care. They improve precision and lessen the clinical workload. In logistics and warehousing, AI enhances robot path planning, fleet coordination, and reduces errors. It significantly boosts throughput and operational efficiency.

What are Service Robots?

The service robotics market involves robots that assist humans in performing tasks across industries. The robots are adopted in various industries such as healthcare, agriculture, and logistics. They are used for cleaning, surgery, warehouse automation, and elderly care. Industries deploy these robots to enhance efficiency, reduce labor costs, and ensure precision in operations. Thus, the adoption of service robots increased after the COVID-19 pandemic, especially in healthcare and cleaning applications. Moreover, the integration of IoT and 5G connectivity enables seamless communication between robots and other smart devices. Thus, rising development of these technologies propel the service robotics market growth.

The service robotics industry is witnessing rapid growth due to rising labor shortages, increasing wages, and the need for precision-driven automation across multiple end-use industries. Service robotics can be semi-autonomous or autonomous. They are developed by using many technologies such as artificial intelligence (AI), machine learning (ML), and computer vision.

Procurement and Forecasting Comparison of Autonomous vs Semi-Autonomous Service Robotics

| Parameter | Autonomous Service Robots | Semi-Autonomous Service Robots |

| Level of Human Involvement | Minimal to none | Human supervision or intervention required |

| Navigation & Decision-Making | Fully AI-driven (SLAM, computer vision, ML) | Partially automated with manual overrides |

| Operational Environment | Dynamic, unstructured, high-variability settings | Structured or controlled environments |

| Key Use Cases | Warehouse AMRs, delivery robots, and field agriculture robots | Surgical assistance, tele-operated inspection, and security robots |

| Productivity Impact | High. Continuous 24/7 operations | Moderate. Dependent on operator availability |

| Safety & Compliance | Advanced obstacle avoidance and fail-safe systems | Relies on human judgment for critical decisions |

| Deployment Complexity | High (integration, testing, and mapping) | Lower, faster onboarding |

| Initial Cost (CAPEX) | High | Medium |

| Operating Cost (OPEX) | Lower over time due to reduced labor | Higher due to human involvement |

| Scalability | Highly scalable across multiple sites | Limited by the availability of trained operators |

| AI & Data Dependency | High (data-driven learning and optimization) | Medium |

| Buyer Profile | Large enterprises, logistics operators, and agriculture firms | Hospitals, defense, and regulated environments |

| Forecasting Impact | Strong long-term CAGR, recurring software revenue | Stable demand, slower growth |

| Risk Sensitivity | Higher regulatory and safety scrutiny | Lower technological risk |

Source: Polaris Market Research Analysis

What is Robots-as-a-Service (RaaS)?

Robots-as-a-Service (RaaS) is a business and deployment model. Organizations subscribe to robotic capabilities on a recurring fee basis rather than purchasing robots outright. The subscription typically contains software, hardware, maintenance, updates, and support. It is shifting costs from CAPEX to OPEX. RaaS enables faster deployment and predictable costs. It is mostly preferred by small enterprises as it requires lower upfront investment and reduced operational risks. Due to these benefits, RaaS demand is high across logistics, healthcare, cleaning, and hospitality applications.

Buyer Decision Summary (ROI Lens): CAPEX Ownership vs RaaS Cost and Return Comparison

CAPEX maximizes ROI for high-utilization, operationally mature buyers. However, RaaS delivers faster, lower-risk ROI for scaling deployments and cost-sensitive procurement teams

| ROI Driver | CAPEX Ownership | RaaS Subscription |

| Upfront Cost | High | Low |

| Payback Period | Long | Short |

| Cost Predictability | Variable | High |

| Utilization Risk | Buyer-owned | Vendor-shared |

| Downtime Risk | Buyer-owned | SLA-backed |

| Scalability | Slower | Faster |

Source: Polaris Market Research Analysis

Market Dynamics

Increasing Labor Shortages and Rising Labor Costs

Many sectors, such as healthcare, hospitality, and retail, face difficulties in hiring staff due to an aging workforce worldwide. Also, higher wages and stricter labor regulations increase labor costs. Thus, businesses adopt robotic solutions to reduce reliance on human labor. Automating routine and repetitive tasks also helps them increase operational efficiency and lower long-term expenses. Service robots provide flexible solutions that work around the clock without relying on human labor. In October 2023, Amazon introduced two new ways to integrate robotic systems. These systems improve employee productivity and streamline customer delivery services. As a result, the growing labor shortages and increasing labor costs in many industries are driving up the demand for service robots.

Increasing Demand for Autonomous Robots in Agriculture, Logistics, and Defense

In agriculture, service robots are used for tasks like crop monitoring, planting, and harvesting. Agricultural robots help increase productivity and reduce the need for seasonal labor. In logistics, autonomous mobile robots (AMRs) are changing warehouses and supply chains. They boost efficiency, lower errors, and cut down on downtime. In defense, the AI robot dog is used for operations such as surveillance, bomb disposal, and reconnaissance. These robot dogs lower the risk to human personnel. With the rise of autonomous systems powered by advancements in AI and machine learning, sectors are using robots more frequently. These systems operate on their own, which leads to better safety, cost savings, and efficiency. Thus, the growing trend of automation in high-growth sectors such as agriculture, logistics, and defense drives the demand for service robots.

Source: Polaris Market Research Analysis

Segment Insights

By Type Outlook

The global service robotics market segmentation, based on type, includes professional service robots and personal service robots. In 2025, the professional service robots segment held a larger market share valued at 69.96%. Their rising deployment in industries such as logistics and agriculture propels the professional service robots market growth. Professional service robots are used for high-value, mission-critical tasks requiring autonomy, precision, and continuous operation. Moreover, in warehouses, use of autonomous robot’s streamlines operations, improving efficiency and reducing costs, which contributes to the market growth. Furthermore, in agriculture, robotic systems for precision farming and crop monitoring have gained traction, addressing labor shortages and increasing productivity which is significantly driving demand for the professional service robots.

Application Groups for Professional Use Units: Installations and Shares Captured in 2025

| Application | Units Installed | Share (%) |

| Transportation and Logistics | 102,925 | 52 |

| Hospitality | 42,030 | 21 |

| Professional Cleaning | 25,527 | 13 |

| Agriculture | 19,487 | 10 |

| Security | 3,128 | 1 |

| Others | 5993 | 3 |

Source: Polaris Market Research Analysis

Source: World Robotics 2025

The personal service robots segment is expected witness a significant growth rate in the coming years. Personal service robots are deployed for cleaning, assistance, elderly care, and other domestic applications. Increasing investments in these robots and rising disposable income contributed to the personal service robots market growth.

By End Use Outlook

The global service robotics market, based on end use, is segmented into defense, field, medical, transportation and logistics, mobile platforms, underwater systems, construction, and others. The mobile platforms segment held the largest share accounting for 13.0% in 2025. Many industries widely adopted them for automation, material handling, and navigation. These robots play a key role in warehousing, manufacturing, healthcare, and smart infrastructure. They help improve efficiency and cut labor costs. The growth of e-commerce and Industry 4.0 has increased the demand for autonomous mobile robots (AMRs) and automated guided vehicles (AGVs) in logistics and supply chain management. Moreover, improvements in AI, IoT, and sensor technology have boosted the capabilities of mobile platforms, making them essential for industrial automation and smart mobility solutions.

Personal Service Robots vs Professional Service Robots

| Parameter | Personal Service Robots | Professional Service Robots |

| Usage | Home cleaning, elderly care, assistance | Logistics, healthcare, agriculture, defense |

| End users | Individuals, households | Industries, enterprises |

| Cost | Low to medium | High |

| Growth trend | Growing due to income and lifestyle change | Dominant due to industrial demand |

Source: Polaris Market Research Analysis

Source: Polaris Market Research Analysis

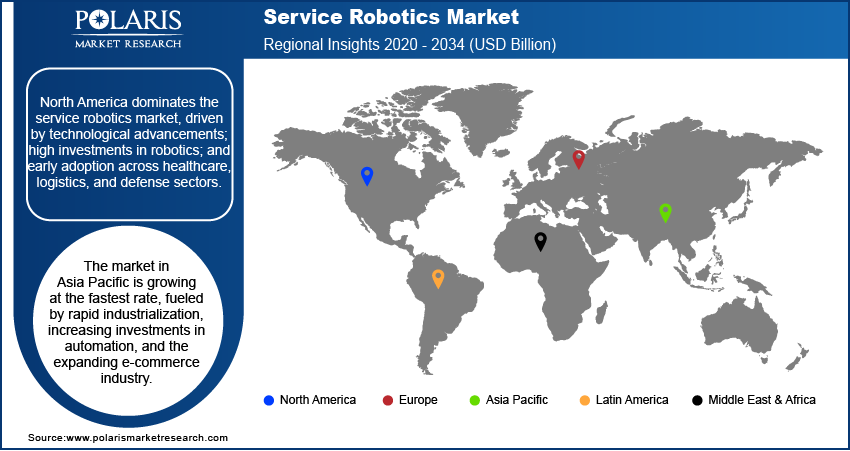

Regional Analysis

By region, the study offers market insights into North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa. North America dominated revenue share capturing 30.0% of the market in 2025. Technological advancements and significant investments in robotics boost dominance. The early adoption in healthcare, logistics, and defense sectors drives the regional market growth. The U.S. service robotics market leads in North America. Strong government support for automation and a robust startup ecosystem boost the U.S. market growth. Rising investments in AI-driven robotics solutions and strong research and development will propel the industry expansion in the country.

Asia Pacific is the fastest-growing region boosting with a CAGR of 13.6%. The Asia Pacific service robotics growth is fueled by rapid industrialization, increasing investments in automation, and the expanding e-commerce industry. The Southeast Asian internet economy is expected to grow from USD 194 billion in 2023 to around USD 330 billion by 2025. Indonesia is expected lead in the region in the coming years. China and Japan are leading in robotics manufacturing and adoption in Asia Pacific. Robust industrial base, growing healthcare needs, and investments in AI-powered robots drive the China service robotics market growth. Also, rising demand for assistive robots, particularly in elderly care, and the increasing aging population propel the Japan service robotics market expansion.

Source: Polaris Market Research Analysis

Key Players and Competitive Analysis Report

The service robotics market is led by global companies like iRobot Corporation, SoftBank Robotics, and Intuitive Surgical, Inc. These firms use innovative technologies and have strong distribution networks. ABB Ltd. and KUKA AG specialize in industrial and professional service robots. They provide scalable solutions for logistics and manufacturing.

Market players use strategies such as mergers, acquisitions, and collaborations to boost their presence. SoftBank Robotics teamed up with e-commerce companies to integrate robots into delivery services. At the same time, Boston Dynamics is well-known for its research in humanoid and quadruped robots, focusing on defense and logistics.

Regional companies, especially in Asia Pacific, seek cost-effective solutions to tap into emerging markets. DJI leads in drone manufacturing, while firms like Cyberdyne Inc. are making strides in healthcare robotics. The competitive landscape features ongoing innovation and a growing emphasis on sustainable, AI-driven robotic solutions.

iRobot Corporation; SoftBank Robotics; Intuitive Surgical, Inc.; ABB Ltd.; KUKA AG; FANUC Corporation; Northrop Grumman Corporation; DJI; Boston Dynamics; Cyberdyne Inc.; Neato Robotics; GeckoSystems International Corporation; Stryker Corporation; Ubtech Robotics; and Blue River Technology are a few key major players in the service robotics market.

List of Key Companies:

- ABB Ltd.

- Blue River Technology

- Boston Dynamics

- Cyberdyne Inc.

- DJI

- FANUC Corporation

- GeckoSystems International Corporation

- Intuitive Surgical, Inc.

- iRobot Corporation

- KUKA AG

- Neato Robotics

- Northrop Grumman Corporation

- SoftBank Robotics

- Stryker Corporation

- Ubtech Robotics

Industry Developments

- April 2026: Locus Robotics launched Locus Array, physical AI robot for warehouse. It works on autonomous and handles dynamic fulfillment tasks. (Source: robotics247.com)

- August 2025: NVIDIA launched Jetson Thor robotics computer for humanoid robots. It helps advanced AI processing and complex task handling. (Source: nvidia.com)

- April 2025: Canadian marine tech company Kraken Robotics introduced a new synthetic aperture sonar service for the global offshore energy sector. The system delivers real-time 3 cm by 3 cm resolution and scans up to 200 meters on each side, offering one of the fastest and most detailed seafloor coverage capabilities in the industry. (Source: krakenrobotics.com)

- June 2024: ABB launched next-generation Robotics control platform OmniCore. The platform is faster, more precise, and more sustainable to empower, enhance, and futureproof businesses. OmniCore’s motion performance delivers robot path accuracy at a level of less than 0.6mm. This opens new automation opportunities in precision areas such as arc welding, mobile phone display assembly, gluing, and laser cutting. (Source: abb.com)

Service Robotics Market Segmentation

By Type Outlook (Revenue, USD Billion, 2021–2034)

- Professional Service Robots

- Personal Service Robots

By End Use Outlook (Revenue, USD Billion, 2021–2034)

- Defense

- Field

- Medical

- Transportation and Logistics

- Mobile Platforms

- Underwater Systems

- Construction

- Others

By Component Outlook (Revenue, USD Billion, 2021–2034)

- Hardware

- Software

- Services

By Regional Outlook (Revenue, USD Billion, 2021–2034)

- North America

- U.S.

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Future Outlook

The future of service robotics market is driven by deeper integration of AI and machine learning across applications. Robots are becoming more autonomous and capable of handling complicated and unstructured environments. Growth of smart automation in logistics, healthcare, and agriculture will rise adoption. Rising use of connected technologies like IoT and 5G will improve real-time decision making and coordination. Increasing demand for human-robot collaboration and Robots-as-a-Service models will support market expansion. Continuous improvements in sensors, data processing, and software will make robots more efficient and scalable across industries.

Service Robotics Market Report Scope

| Report Attributes | Details |

| Market Size in 2025 | USD 59.10 Billion |

| Market Size in 2026 | USD 66.30 Billion |

| Revenue Forecast by 2034 | USD 167.88 Billion |

| CAGR | 12.3% from 2026 to 2034 |

| Base Year | 2025 |

| Historical Data | 2021–2024 |

| Forecast Period | 2026–2034 |

| Quantitative Units | Revenue in USD billion, 2022–2034 and CAGR from 2026 to 2034 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format | PDF + Excel |

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Service Robotics Market FAQ's

The global service robotics market was valued at USD 59.10 billion in 2025 and is projected to reach USD 167.88 billion by 2034. It is expected to register a CAGR of 12.3% during 2026–2034.

North America dominated the revenue share in 2025. It is driven by technological advancements and high investments in robotics.

Service robot types are professional robots (used in healthcare, defense, logistics, and agriculture applications) and personal/domestic robots (used for home cleaning, entertainment, lawn mowing, and elderly assistance).

AI and IoT integration and the rising demand for automation in healthcare and logistics drive market growth. Benefits such as labor cost reduction propel the demand for service robots. Also, government investments in robotics research and development initiatives will fuel the industry expansion.

A few top players are iRobot Corporation; SoftBank Robotics; Intuitive Surgical, Inc.; ABB Ltd.; KUKA AG; FANUC Corporation; Northrop Grumman Corporation; DJI; Boston Dynamics; Cyberdyne Inc.; Neato Robotics; GeckoSystems International Corporation; Stryker Corporation; Ubtech Robotics; and Blue River Technology.

In 2024, the professional service robots segment held the dominant market share, driven by their deployment in industries such as logistics and agriculture.

Service robots cut down on manual work, make things run more smoothly, and save time. They do the same tasks over and over with greater accuracy.

Service robots operate outside manufacturing environments and interact with humans. Industrial robots are used in factories for production tasks.

Download Sample Report of Service Robotics Market

Please fill out the form to request a customized copy of the research report.