Canada Pharmaceutical Market Insight, Growth Report, 2024-2032

REPORT DETAILS

Canada Pharmaceutical Market Summary

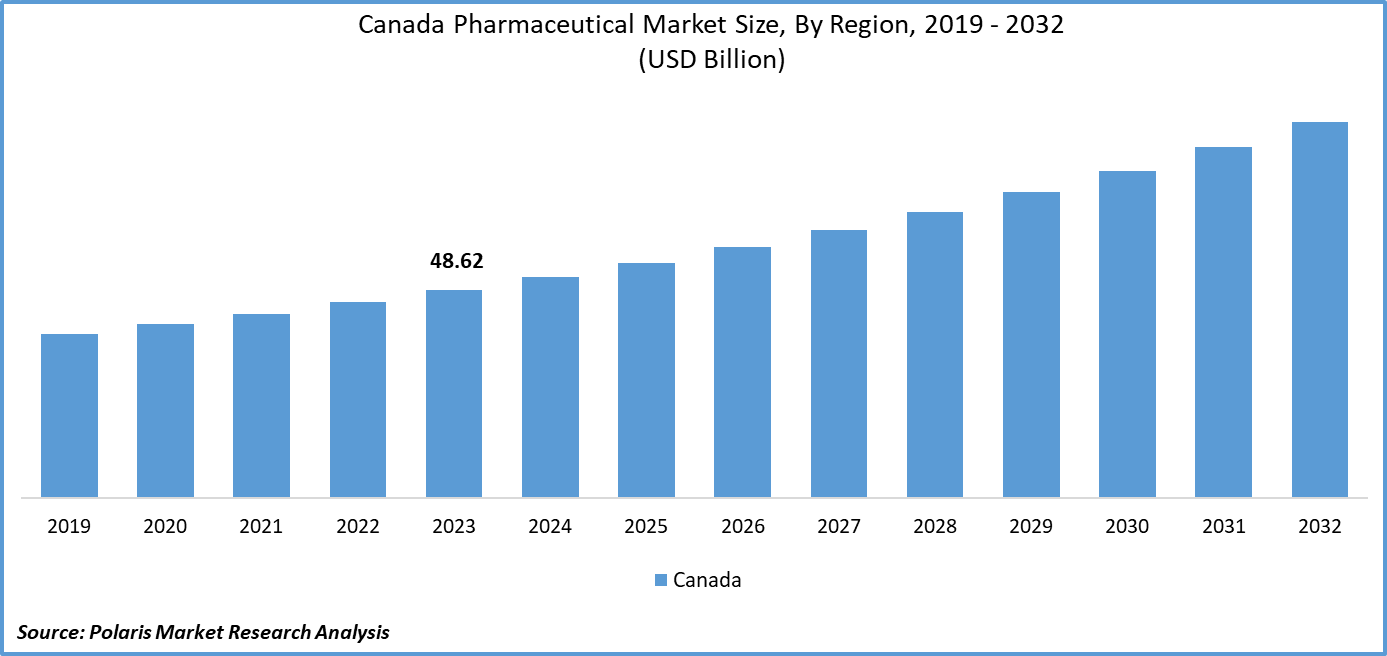

The canada pharmaceutical market size and share was valued at USD 48.62 billion in 2023. The market is anticipated to grow from USD 51.72 billion in 2024 to USD 88.11 billion by 2032, exhibiting a CAGR of 6.9% during the forecast period.

Market Statistics

The Canadian pharmaceutical market is propelled by various factors, such as a rising aging population, an increase in healthcare spending, a growing need for innovative drugs, and a significant emphasis on research and development. Furthermore, supportive government policies facilitating healthcare access and substantial investments in biotechnology play a crucial role in fostering the expansion of the market. These combined elements contribute to the continual growth and progress observed within the Canadian pharmaceutical industry.

The burgeoning elderly population in Canada stands out as a pivotal force propelling the pharmaceutical market forward. With a projected surge in the number of Canadians reaching the age of 65, expected to reach 5.1 million over the next decade, there is a substantial anticipated increase in the demand for pharmaceutical products and healthcare services. The elderly demographic, characterized by a higher prevalence of chronic health conditions and age-related ailments, underscores the imperative for pharmaceutical companies to focus on developing tailored drugs and healthcare solutions. This demographic shift underscores the prominence of geriatric medicine and healthcare services, playing a pivotal role in shaping the landscape of the Canadian pharmaceutical market.

The research study provides a comprehensive analysis of the industry, assessing the market on the basis of various segments and sub-segments. It sheds light on the competitive landscape and introduces Canada pharmaceutical market key players from the perspective of market share, concentration ratio, etc. The study is a vital resource for understanding the growth drivers, opportunities, and challenges in the industry.

Source: Polaris Market Research Analysis

To Understand More About this Research: Download Sample Report

The rising need for early and accurate disease diagnosis, coupled with an increasing demand for advanced therapies, is anticipated to drive market growth. According to data from the Canadian Cancer Society, cancer stands as the leading cause of death in Canada, contributing to over 28% of annual fatalities. In 2022, Canada reported approximately 233,900 new cancer cases and 85,100 cancer-related deaths. Among these, around 121,100 men and 112,800 women received cancer diagnoses. The prevalent types of cancer in the country include lung, breast, colorectal, and prostate cancers.

Cancer and cardiovascular diseases stand as the primary culprits behind fatalities in Canada. A notable 18.5% of the total annual deaths in the nation can be attributed to cardiovascular diseases. The escalating incidence and mortality rates of cancer and heart-related ailments are contributing to the expansion of the nuclear medicine and radiopharmaceutical market. As per data released by the Canadian Institute for Health Information (CIHI) in July 2022, approximately 2.4 million individuals in the country are grappling with heart disease. Additionally, the Heart and Stroke Foundation of Canada reveals that 9 out of 19 Canadians possess at least one risk factor predisposing them to heart conditions, stroke, and vascular cognitive impairment.

The economic burden of cardiovascular disease in Canada totals approximately USD 21.2 billion, encompassing both direct and indirect costs, while stroke incurs an annual cost of around USD 3.6 billion. Furthermore, the Canadian Institute for Health Information (CIHI) has partnered with the Canadian Cardiovascular Society (CCS) with the aim of enhancing the quality of cardiac care services nationwide. With government entities launching supportive initiatives and a rising prevalence of targeted diseases accompanied by elevated mortality rates, the demand for innovative and efficacious therapeutic products is anticipated to surge in the forthcoming years.

Source: Polaris Market Research Analysis

Market Dynamics

A Rise in the Elderly Population Bolstered the Growth of the Canada Pharmaceutical Market

The growing number of elderly individuals, who are more susceptible to various metabolic and lifestyle disorders, is contributing to an increase in the occurrences of chronic diseases within the Canadian population. The associated comorbidities with these diseases are expected to have a favorable impact on the pharmaceutical market's growth in the forecast period. The pharmaceutical industry in Canada is continually advancing, incorporating technologies like automated dispensing systems and electronic prescription systems. These innovations have the potential to enhance efficiency and accuracy, thereby fueling market expansion.

Market Restraints

Intensely Competitive, and Numerous Pharmacies are Competing for Customers are Likely to Hamper the Growth of the Market

Pharmacies face challenges in distinguishing themselves from competitors and drawing in customers due to the heightened competition. The recent surge in the number of pharmacies in Canada has resulted in market saturation in certain regions, posing difficulties in both attracting and retaining customers. Government regulations play a significant role in the heavily regulated pharmaceutical industry in Canada, acting as barriers for new pharmacies to enter the market and limiting the operational scope of existing ones.

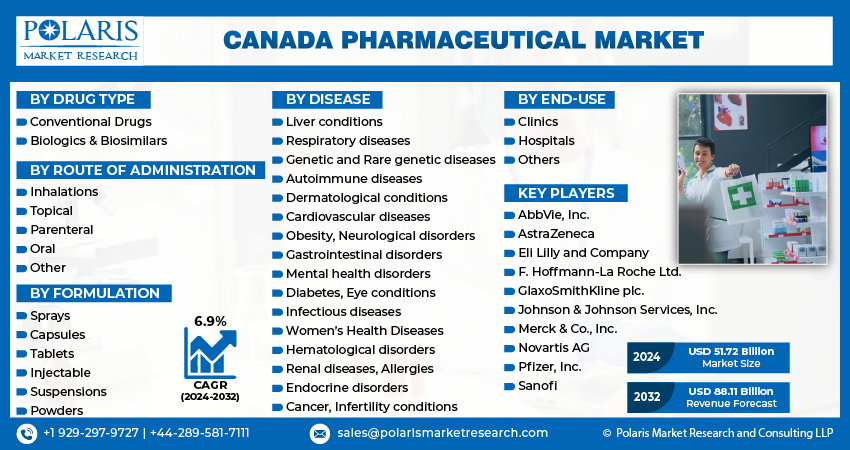

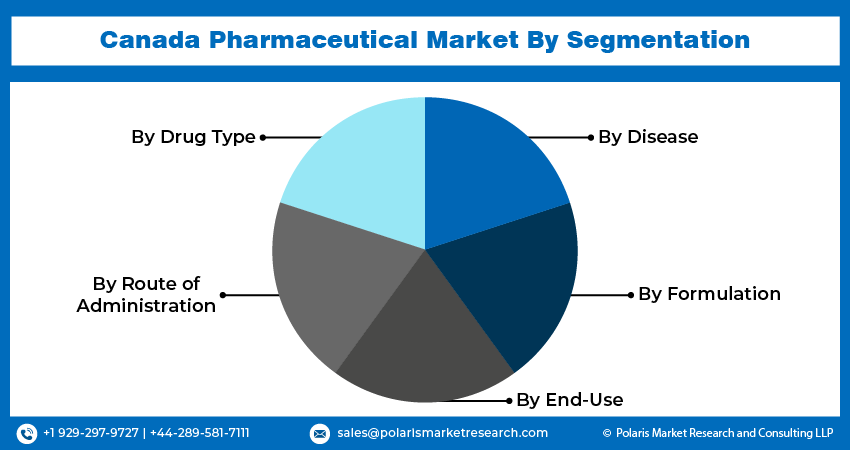

Report Segmentation

The market is primarily segmented based on drug type, route of administration, disease, formulation, end-use.

| By Drug Type | By Route of Administration | By Disease | By Formulation | By End-Use |

|

|

|

|

|

Source: Polaris Market Research Analysis

To Understand the Scope of this Report: Request Customization

Canada Pharmaceutical Market Segmental Analysis

By Drug Type Analysis

- In 2023, the largest market share was held by the segment of conventional drugs (small molecules) based on drug type. Small molecules play a crucial role in driving Canada's pharmaceutical market, serving as the cornerstone of drug development and contributing to ongoing research and innovation in the sector. Their effectiveness in treating various medical conditions contributes to sustained high demand, fostering market growth and ensuring economic stability. Additionally, substantial investments and strategic partnerships enhance Canada's standing in the pharmaceutical industry, facilitating the creation of innovative medications and advancing the nation's impact on healthcare solutions worldwide.

- Furthermore, the growth of the segment will be accelerated by strategic initiatives undertaken by key market players. For instance, in April 2023, the global pharmaceutical company Takeda engaged in an exclusive licensing agreement with Treventis for a set of small molecules designed to target tau, a protein associated with misfolding and aggregation believed to contribute to Alzheimer's disease. Leveraging Treventis' expertise in Alzheimer's and neurodegenerative research, these molecules were developed. The significance of this collaboration lies in the potential to create an effective drug targeting tau in the brain, an area currently lacking suitable treatments. With prevalent brain-related conditions in Canada, such as Alzheimer's, Parkinson's, and epilepsy, this partnership holds promise for advancing treatments and finding cures through state-of-the-art patient care and research endeavors.

By Route of Administration Analysis

- In the forecast period, the oral route of administration emerged as the leading revenue contributor in the market. This method of delivering medications is widely preferred due to its non-invasive nature, cost-effectiveness, and ability to promote patient compliance. The versatility of oral medications across various medical conditions solidifies the prominence of this administration route, ensuring broad accessibility and effectiveness in drug delivery. The impact of these factors is pivotal in shaping pharmaceutical markets, enhancing treatment accessibility, and providing a user-friendly experience for patients.

- The parenteral segment is projected to experience the most rapid CAGR throughout the forecast period. This administration method entails directly injecting medications into the bloodstream, bypassing the digestive system. It plays a crucial role in ensuring swift drug delivery, and precise dosing, and is particularly valuable in situations demanding immediate and consistent blood levels. Parenteral routes, encompassing intravenous and intramuscular injections, are indispensable in critical care, emergency scenarios, and for patients facing challenges in swallowing or absorbing oral medications, thus serving as an essential component in modern medicine.

Source: Polaris Market Research Analysis

Competitive Landscape

The Canada Pharmaceutical market trend is fragmented and is anticipated to witness competition due to several players' presence. Major service providers in the market are constantly upgrading their technologies to stay ahead of the competition and to ensure efficiency, integrity, and safety. These players focus on partnership, product upgrades, and collaboration to gain a competitive edge over their peers and capture a significant market share.

Some of the major players operating in the global market include:

- AbbVie, Inc.

- AstraZeneca

- Eli Lilly and Company

- F. Hoffmann-La Roche Ltd.

- GlaxoSmithKline plc.

- Johnson & Johnson Services, Inc.

- Merck & Co., Inc.

- Novartis AG

- Pfizer, Inc.

- Sanofi

Recent Developments

- In January 2025, Sandoz Canada, a Novartis subsidiary, introduced its biosimilar adalimumab, Hulio, to the Canadian market, representing the first biosimilar introduction in the country for treating inflammatory conditions patients nationwide (Sandoz, 2025).

- In October 2024, Shoppers Drug Mart, a prominent Canadian pharmacy retailer, formed a strategic collaboration with Curative Health Services to broaden its Healthcare Services and provide COVID-19 testing nationwide throughout its stores (Shoppers Drug Mart, 2024).

Report Coverage

The Canada Pharmaceutical market report emphasizes key regions across the globe to provide a better understanding of the product to the users. Also, the report provides market insights into recent developments and trends and analyzes the technologies that are gaining traction around the globe. Furthermore, the report covers an in-depth qualitative analysis pertaining to various paradigm shifts associated with the transformation of these solutions.

The report provides a detailed analysis of the market while focusing on various key aspects such as competitive analysis, drug type, route of administration, disease, formulation, end-use, and futuristic growth opportunities.

Canada Pharmaceutical Market Report Scope

| Report Attributes | Details |

| Market size value in 2024 | USD 51.72 billion |

| Revenue Forecast in 2032 | USD 88.11 billion |

| CAGR | 6.9% from 2024 – 2032 |

| Base year | 2023 |

| Historical data | 2019 – 2022 |

| Forecast period | 2024 – 2032 |

| Quantitative units | Revenue in USD billion and CAGR from 2024 to 2032 |

| Segments Covered | By Drug Type, By Route of Administration, By Disease, By Formulation, By End-Use, By Region |

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Uncover the dynamics of the Canada pharmaceutical sector in 2024 with detailed statistics on market share, size, and revenue growth rate meticulously curated by Polaris Market Research Industry Reports. This all-encompassing analysis extends to a forward-looking market forecast until 2032, complemented by a perceptive historical overview. Immerse yourself in the profound insights offered by this industry analysis through a Download Sample Report.

Browse Our Top Selling Reports

Ovulation Testing Kits Market Size, Share 2024 Research Report

Halloysite Market Size, Share 2024 Research Report

Chemoinformatics Market Size, Share 2024 Research Report

Canada Pharmaceutical Market FAQ's

key companies in Canada Pharmaceutical Market AbbVie, AstraZeneca, Eli Lilly, F. Hoffmann-La Roche, GlaxoSmithKline

Canada Pharmaceutical Market exhibiting the CAGR of 6.9% during the forecast period

The Canada Pharmaceutical Market report covering key segments are drug type, route of administration, disease, formulation, end-use

key driving factors in Canada Pharmaceutical Market are A rise in the elderly population

The global Canada Pharmaceutical market size is expected to reach USD 88.11 billion by 2032

Download Sample Report of Canada Pharmaceutical Market

Please fill out the form to request a customized copy of the research report.